A New Study on Integration of Renewables in Germany

Posted by Euan Mearns on November 8, 2012 - 4:53am

This is a guest post by Paul-Frederik Bach. Paul-Frederik has more than 40 years experience in power system planning. He worked with grid and generation planning at ELSAM, the coordinating office for west Danish power stations, until 1997. As Planning Director at Eltra, Transmission System Operator in West Denmark, he was in charge of West Denmark's affiliation to the Nordic spot market for electricity, Nord Pool, in 1999. Until retirement in 2005 his main responsibility was the integration of wind power into the power grid in Denmark. He is still active as a consultant with interest in safe and efficient integration of wind power. See here for a previous post on the Oil Drum. This is a link to his website.

DENA[1] published its first grid study in 2005 and a second grid study in 2010. The first report stressed the vulnerability of the power grid by demonstrating that UCTE’s European security rules for electricity transmission grids were violated already in 2003.

The energy turnaround in 2011 (“die Energiewende”) has eroded the validity of the first two reports.

In August 2012 DENA has published a third study on the integration of renewables in Germany [3]. The study was made in cooperation with Aachen University[2].

It is the purpose of the study to analyse how the political targets will change the electricity supply system by 2050 and to identify infrastructure challenges. The study is mainly based on the Guiding Scenario 2009 [1], published by the Federal Ministry for the Environment, Nature Conservation and Nuclear Safety (BMU)[3]. The Guiding Scenario 2010 [2] was not yet published when DENA began working on the integration study.

BMU’s guiding scenarios as the official targets

The guiding scenarios are important references in German energy policy. They include three basic scenarios with different penetrations of renewable energy, A, B and C. The DENA study is based on the basic scenario A.

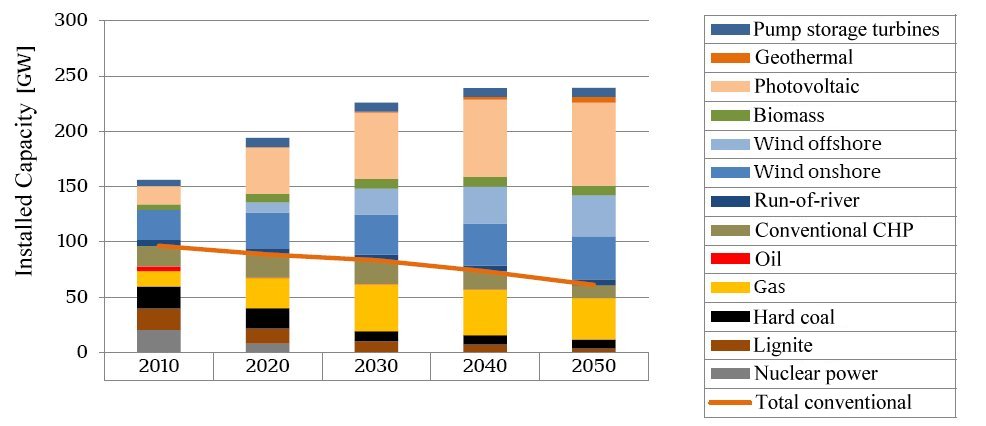

Figure 4-17 in the DENA report presents an overview of the expected future capacity pattern for the electricity industry:

PSW is pump storage and KWK is combined heat and power (CHP). The peak load in Germany is assumed to be approximately 83 GW for all years.

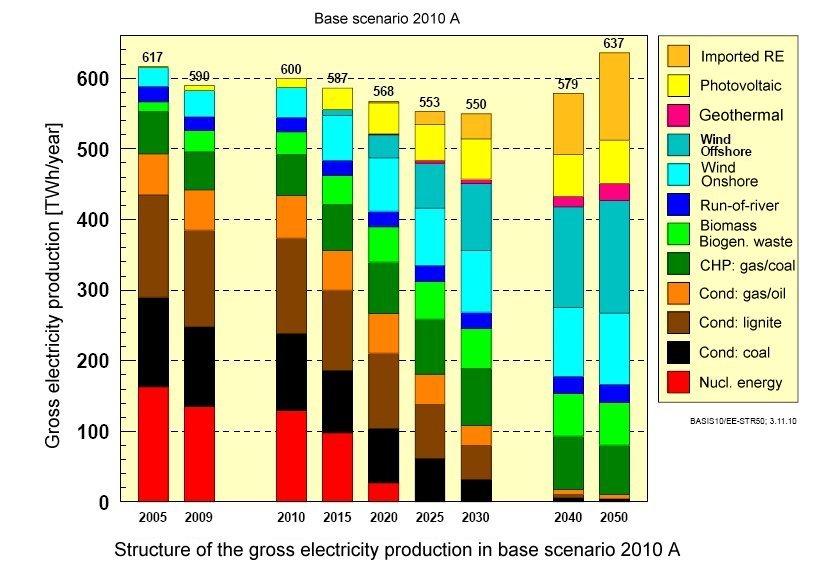

The corresponding production pattern (from Guiding Scenarios 2010):

It appears from this graph that Germany is expected to import an increasing part of the electricity consumption. Even 80 GW of controllable capacity and 160 GW of variable capacity will be insufficient for covering the full demand in 2050.

The import is assumed to be renewable electricity (EE). 123 TWh or about 20% of the consumption must be imported. PV covers 12% of the consumption with 31% of the installed capacity.

It may be a reasonable conclusion that Germany cannot be self-sufficient in renewable energy. For a neighbouring country the assumed origin of the import is interesting.

BMU expects the windy countries in North-West-Europe (region 3: Belgium, Ireland, Luxembourg, the Netherlands and Great Britain) to be the main European source of renewable electricity. Besides that the production of solar electricity in North Africa will be of importance.

The import will require new transmission facilities with a double-figure capacity in GW. The model has calculated necessary transfer capabilities in 2050. Between Germany and region 2 (Denmark, Norway, Sweden and Finland), and between Germany and region 4 (France, Portugal and Spain), 0 GW will do, while 71 GW will be needed between Germany and region 3.

The results indicate a simplified theoretical model and preliminary results. Good estimates of future transfer patterns in Europe will be very interesting. Therefore a further improvement of data and models should be encouraged.

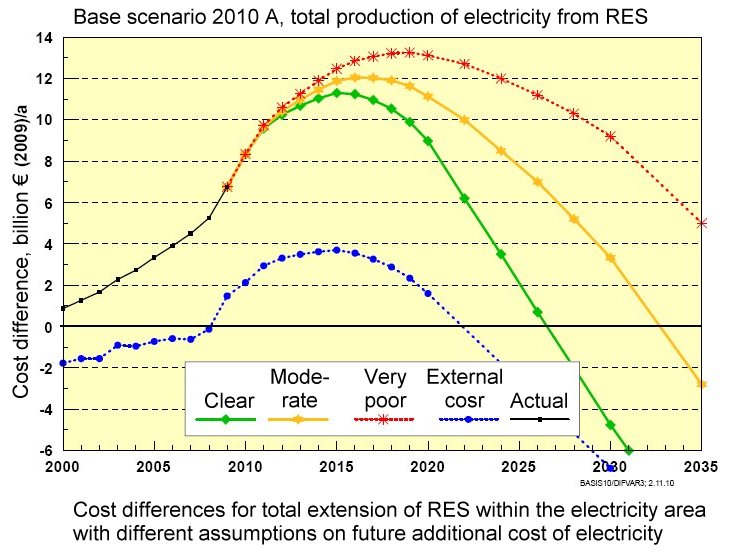

Even the economic impact of the renewable energy has been estimated. The additional cost is expected to peak between 2016 and 2020 with €11-13 billion and then gradually decrease.

External costs can reduce the additional cost considerably (the blue curve). However, external costs are not well defined, so the adjusted cost has limited information value.

For scenario A the total German share of renewables will be 55% in 2050 and the emission of CO2 will be reduced by 85%. For the electricity production the share of renewables will be 86% (table 1 in [2]).

The authors of the Guiding Scenarios 2010 are convinced that the transition is possible for all scenarios between 2010 and 2050. Balancing of the variable production will be possible with additional storage facilities. A list of measures is organized in the following groups:

1. Conversion of power generation to a large renewables share

2. Increasing efficiency in heat supply, especially energy-related modernisation of buildings

3. Increasing efficiency in the electricity sector

4. Increasing efficiency in the transport sector

5. Expansion of renewables in the heat sector

6. Expansion of renewables in the transport sector

The DENA study aims at a closer analysis of the electricity sector

The new DENA study analyses the electricity sector, mainly based on the Guiding Scenario 2009. It does not discuss the likelihood or the relevance of the scenario.

The modeling for the DENA study includes:

-Necessary reserve capacity

-Development of the production system

-Market simulation including price formation

-Necessary grid reinforcements

The results seem to some degree to be replications of the results in the guiding scenarios.

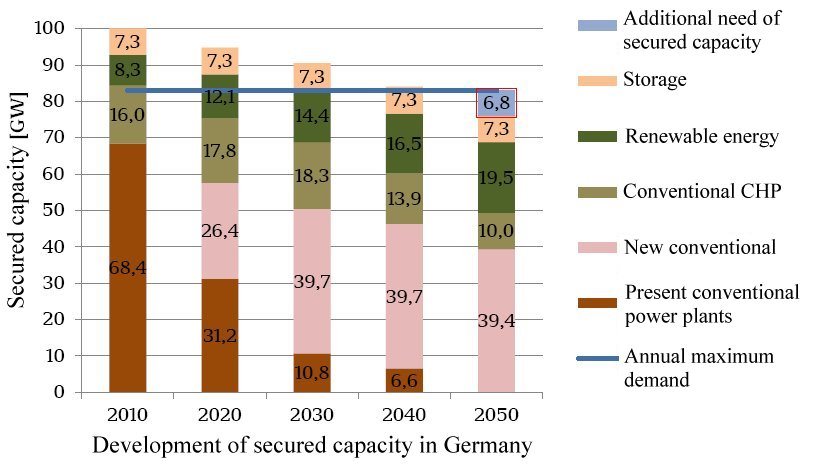

An interesting chart shows the development in “secured production capacity”:

New conventional capacity provides 39.4 GW and CHP 10 GW. The 6.8 GW at the top is additional need for secured capacity.

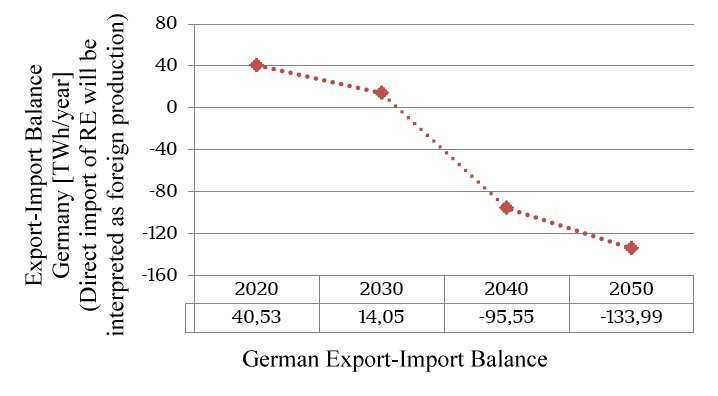

The DENA study emphasizes the development in the annual export-import balance.

It is obvious that the need for import of renewable electricity develops between 2030 and 2050.

The DENA study quantifies the negative residual demand. A part of this cannot be eliminated by available means. It is called “not integrative power”.

| From table 4-3 and fig. 4-35 | 2020 | 2030 | 2040 | 2050 | |

| Negative residual demand | Number of hours | 29 | 1056 | 2764 | 3829 |

| Maximum value [GW] | -8.7 | -38.7 | -58.7 | -70.6 | |

| Average value [GW] | -3.4 | -8.6 | -13.6 | -17.3 | |

| Energy [TWh] | 0.1 | 9.1 | 37.5 | 66.3 | |

| Not integrative power | Number of hours | 0 | 86 | 603 | 1969 |

| Maximum value [GW] | - | -14.5 | -40.0 | -62.5 | |

| Average value [GW] | - | -3.8 | -8.9 | -10.7 | |

| Overflow [TWh] | 0 | 0.3 | 5.4 | 21.1 | |

The study does not specify the necessary grid extensions. It says (section 4.6.2) that a virtual grid has been assumed for the calculations.

The DENA study also includes calculation of additional cost of the renewables program. The results are slightly higher than that in Guiding Scenarios 2010.

The main conclusions of the DENA study:

-Conventional power plants will still be needed to a considerable extent in 2050. A new generation of efficient and flexible units must be able to interact efficiently with the uncontrollable production.

-Germany cannot remain self-sufficient in electricity supply. Import of electricity will increasingly be necessary after 2030. Both production capacity abroad and transmission facilities must be secured in due time. In Germany a well balanced mix of technologies including renewables, conventional power plants, storage facilities, grid extensions and demand side management will be needed in order to maintain security of supply.

-A complete integration of renewables in the power system is not possible. The production from renewables and CHP in one hour can exceed the electricity demand by 70 GW in 2050. A part of this production can be exported or stored. In case of delayed grid reinforcements or limitations in other countries the challenges within Germany will be even harder.

-Grid extensions are urgently necessary in both transmission and distribution systems. The extensions are already now considerably behind schedule.

-Electricity supply will be clearly more expensive in 2050 than today. The present market arrangement will not be able to cover the cost. New market arrangements must therefore be developed.

The DENA study does not add much to BMU’s guiding scenarios

During the reading of the DENA study the necessity of understanding the underlying guiding scenarios became increasingly clear. The DENA study is for practical reasons based on the Guiding Scenarios 2009. The difference is not significant. Therefore results from the 2010 edition have been presented in this paper.

A comparison of the two reports leaves the impression that much more specific data and results are presented as tables in the scenario report than in the DENA study. Section 7.3 of the scenario report gives quite specific guidelines and recommendations for the transition, while the conclusions of the DENA report (summarized above) are of rather general nature.

This observation does not mean that the scenario report is adequate for all purposes, but the DENA analysis of the electricity sector deserves more details in the presentation and probably also a more detailed modeling.

Some necessary research and development activities deserve special attention:

-A new generation of conventional thermal power plants must meet nearly contradictory specifications such as operational flexibility, multi-fuel operation, high energy efficiency, low environmental impact, robustness and economic efficiency.

-It will take new sophisticated market arrangements to give market participants investment incentives for the development and construction of the right mix of production technologies.

References

- Langfristszenarien und Strategien für denAusbau erneuerbarer Energien in Deutschland - Leitscenario 2009. Bundesministerium für Umwelt, Naturschutz und Reaktorsicherheit. August 2009. [http://pfbach.dk/firma_pfb/bmu_leitszenario2009_bf.pdf]

- Langfristszenarien und Strategien für den Ausbau erneuerbarer Energien in Deutschland bei Berücksichtigung der Entwicklung in Europa und global – „Leitstudie 2010“. DLR[4], Frauenhofer IWES[5]und IfnE[6]. Dezember 2010. (Summary in English: page 31-60)[http://pfbach.dk/firma_pfb/bmu_leitstudie2010_bf.pdf]

- Integration der erneuerbaren Energien in den deutsch-europäischen Strommarkt. Deutsche Energie-Agentur GmbH (dena). 15.08.2012. [http://pfbach.dk/firma_pfb/dena_endbericht_integration_ee_2012.pdf]

Endnotes

[1] Deutsche Energie Agentur, Berlin

[2] Institut für Elektrische Anlagen und Energiewirtschaft der Rheinisch-Westfälischen Technischen Hochschule Aachen

[3] http://www.bmu.de/erneuerbare_energien/downloads/doc/45026.php(in German)

[4] Deutsches Zentrum für Luft- und Raumfahrt, Stuttgart

[5] Frauenhofer Institut für Windenergie und Energiesystemtechnik, Kassel

[6] Ingenieurbüro für neue Energien, Teltow

Contact

- Content: editors at theoildrum dot com

- Tech support: support at theoildrum dot com

License

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.

Thanks for this article.

A few things I pick up from these figures at first glance:

- new renewable will mostly be used for increased power consumption and only secondary for reducing conventional.

- new coal is in danger of becoming a stranded investment.

- if the Germans would operate their nuclear plants for longer then (theoretically) fossil could be phased-out by 2030.

Germany (as any other country) should focus first on efficiency and reducing energy consumption. Much cheaper, requires less pan-European coordination, reduces vulnerability and may result in a faster phaseout of conventional power.

Btw, I recommend this site for anyone who wants to stay up-to-date with the renewable developments.

The assumption is that actual consumption is to remain more-or-less constant. Germany is definitely concentrating first on efficiency; less so on reducing absolute consumption. It is assumed that some non-electric energy consumption (eg. gas for building heat and some transportation fuel) will be switched to electricity, even as electricity demand declines somewhat in existing consumption sectors.

Fossil-fuelled electric generation capacity must remain at or close to present levels in order to be able to accomodate the intermittency of ever-increasing penetration of intermittent renewable generation, even as actual consumption of fossil fuels declines. In order to maintain the capacity with ever-lower consumption and faster ramp rates, either fixed capacity payments or extremely variable spot prices (fairer perhaps but more risky in the financial sense) will be needed for to maintain the fossil generators. Since both are probable, fossil generation assets are unlikely to become uneconomical or "stranded" before 2050.

I can't offer a comment on nuclear generation. As a nation already committed to dealing with an existing nuclear waste stockpile and numerous nuclear sites, Germany would have been a good candidate for maintaining and increasing its nuclear energy investment. Yet it has chosen to do otherwise, and somehow even reduced fossil fuel consumption in its electricity sector at the same time (while modestly increasing fossil fuel generation capacity).

In 2011, the part of conventional fossil means in Germany's mix was 57.8% for 56.9% in 2010. The very minor reduction in fossil fuel consumption is actually the result of much lower export.

It can be materially demonstrated that Germany artificially made the fuel consumption appear lower by reducing exports, by calculating that the 2010 mix of 56.9% fossil applied to the 610,4 TWh of actual consumption results into 347,3 TWH of local fossil consumption, whilst the 2011 mix of 57.8% fossil applied to the 605,8 TWh of actual consumption results into 350,2 TWH of local fossil.

Therefore a 3 TWh year to year local increase of fossil based power consumption.

A much higher increase was expected by most proponents of nuclear. They were not fully informed of the fact that 7GW of solar, and also some very significant wind capacity would be added to the grid, with as a result solar production going in one year from 11.7 to 19.3 TWh, and the whole renewable production going up around around 20% and 20 TWh up to 122TWh. This was quite an incredible year for renewable production, but which effect on CO2 emissions has been entirely wasted by the nuclear reduction.

2012 will another very good year in this regard, but still not really any reduction in fuel consumption because of the cold winter early this year.

The trouble is that Germany is now hitting hard the limits how how much renewable can be integrate into it's grid, and even the DENA chief is calling for a stop as reported here : wiwo.de : Energiewende „Liebe Leute, so geht es nicht weiter!“

And also maybe some people think the 2050 aims of 85% CO2 reduction and 86% carbon-free electricity is great, but what that actually means is that Germany, after the execution an extremely expensive, optimistic, and 40 years long plan, aims to have in 2050 an electricity mix that's a little bit less clean than the one France had in 2011 with 90% of energy generated by carbon free sources (when summing the production of nuclear, hydro and other renewables).

And France will make further progress soon, since half of it's coal capacity will be gone within the next 3 years (it'll be partially replaced by gas, and if that gas ends up being intensively used because of the new socialist power reservation on nuclear, maybe the CO2 reduction won't be as big).

Thank you for your work, Mr. Bach! It is IMHO a very good starting point for a useful discussion of the German Energiewende and led to a few remarks from and questions on my side. :-)

The expert group for environment of the German parliament (Sachverständigenrat für Umweltfragen, SRU) has published in January/June 2011 a quite comprehensive study (396 pages, German) on the issue of 100% energy production with renewables in Germany in 2050:

http://www.umweltrat.de/SharedDocs/Downloads/DE/02_Sondergutachten/2011_...

The goal of this study was to evaluate an extrem case (100% renewable); if this could work, the assumption was, that less extreme appoaches like the Guiding Scenario of the BMU would also do.

The study of the SRU comes to quite different conclusions:

a) For three different scenarios and various sub-scenarios the authors saw no problem with 100% renewables. In all(!) cases (500/600/700 TWh demand) the domestic potential is in principle sufficient to provide enough energy, the economically best versions in the 600/700 TWH scenarios required only 15%, i.e. 100 TWh, (re)import of electricity from either Scandinavia or Africa.

b) Transmission capacity to Denmark/Norway has to be increased to ~50 GW. UK does not play any special role.

c) The 700 TWh scenario would allow complete transition of transport and heating to electricity, provided by reneables.

My own rough calculations for a 700 TWh demand with 600 TWh domestic production requires:

70 GW onshore wind (2500 FLH) 175 TWh

70 GW off-shore wind (4000 FLH) 280 TWh

hydro power 30 TWh

bio-mass 60 TWh

PV at least 100 GW 100 TWh

These assumptions are quite conservative and usually come from other serious studies (Fraunhofer institutes etc.), at least PV and wind (higher FLH) could even be higher.

So my questions:

Do you assume that the SRU study is basically faulty?

Could it be that the transmission capacity in your study is wrong? To UK much too high, to Scandinavia much too low?

Do you assume that large scale storage in Scandinavia does not work?

Paul-Frederik Bach

Thanks!

Could you give an estimate for the costs of the storage in Norway per kwh? What losses can be expected for transmission, storage etc., what's the price for a GW transmission capacity?

A recent paper by Richard Green and Nicholas Vasilakos estimates the Danish cost of storing energy in Norway between 2001 and 2008 at "just under €1.5/MWh". The cost of the 700 MW Skagerrak 4 link between Denmark and Norway is expected to be 3.2 billion DKK or about 600 million €/GW. Statnett's Grid Development Plan 2010 envisages 7 GW new transfer capacity to the UK, the Netherlands, Germany, Denmark and Sweden and a total Norwegian investment at 12-20 billion NOK. I suppose that Statnett expects the other countries to invest at least the same amount of money.

Construction of new transmission is extremely expensive, and the build out of both transmission and distribution networks would have to be enormous. It would cost hundreds of billions and take decades, and Europe will have energy difficulties long before that.

A major change in power flows would be very difficult to accommodate, as Germany is already discovering. A large increase in power wheeling is really not affordable and will also lead to increased potential for grid instability. Smart grids add greatly to complexity. Intermittent renewables assume system parameters but do not offer the ability to control them - no frequency control, no voltage control, no spinning reserve, no black start capacity.

Building in a huge infrastructure dependency to what are already typically low EROEI energy sources risks tipping the EROEI below unity in some instances. In any case, we will have neither the time nor the money to build out the grid as would be required. Europe is already tipping into economic depression.

Here's my take on renewables, particularly in Europe, and with emphasis on off-shore wind and grid issues: Renewable Energy: The Vision and a Dose of Reality.

Correct, building of transmission lines is bloody expensive. However, Germany's infrastructure was replaced after WWII is has to be replaced again in the next two decades, so much money has to be spent anyway. The other aspect is, with 85 billions per year for imported fuels and steep increase of energy prices the transition makes more and more sense. According to German industry (BDI) the costs are around 370 billion until 2050, 170 billion are due anyway, of the rest we have already paid 80 billions. To stop at the current point is IMHO stupid, esp. for an industrial power which is doing very well and with many consumer willing to invest in reneables.

Net instability has decreased in 2011, sorry. "Intermittent renewables assume system parameters but do not offer the ability to control them - no frequency control, no voltage control, no spinning reserve, no black start capacity." Acoording to German electrical engnieers this is wrong.

"Building in a huge infrastructure dependency to what are already typically low EROEI energy sources risks tipping the EROEI below unity in some instances. " To call wind a low EROIE energy source is funny, with around 40 for on-shore and high potential for more savings. Most of the investments for off-shore wind are one-time (grid connection), the overall balance is still very good. PV with EROEI of around 10 is acceptable.

"In any case, we will have neither the time nor the money to build out the grid as would be required. Europe is already tipping into economic depression." Yes, we should simply do BAU, great alternative - not for me! Maybe stupid question: The money for the transition to 100% nuclaer energy is available?

The money can only be spent if it is available, and I am arguing that it will not be. The single currency crisis has barely begun, and Germany will be affected too, probably to the tune of at least 20% of GDP in the first year following the end of currency union. German exports are already down now that the artificial stimulus of purchasing power in southern Europe is essentially over. Germany's banks funded everyone else's housing bubble, and are over-exposed to sovereign debt that is getting much closer to default. This is going to end badly for all of Europe, not just the periphery.

Security of supply is a major future concern for Europe, given that the alternative is dependence on Russian gas, which would be very uncomfortable. I can certainly see why people wish to develop as much indigenous energy potential as possible. Some of it makes sense, where it is decentralized and adjacent to demand, where it is dispatchable or where it has a reasonable match with the load profile. The FIT programmes are being cut back though, due to financial squeeze, so fewer people will be willing or able to invest in the future. I am very familiar with FIT programmes, having been involved in negotiating one in Canada. Personally, I have little faith in governments to keep long term promises when circumstances change radically, as they are about to do.

So how exactly does intermittent generation deliver ancilliary services according to German power engineers?

EROEI calculations need to include all the inputs, including the energy invested in the necessary grid infrastructure and the procurement of all the non-renewable components. The time component also needs to be taken into account, as Nate Hagens wrote here some time ago. This will lower the numbers substantially.

I am no fan of nuclear power. My field as an academic was power systems, with an emphasis on (lack of) nuclear safety in the former Eastern Bloc. Even to maintain existing nuclear capacity would not be financially possible, let alone any expansion.

I am not suggesting BAU. What I am saying is that BAU is not going to be physically possible, and nor are the currently discussed alternatives going to be able to maintain anything like it. We are going to have to lower our expectations. Simpler grids with less power wheeling are going to be a part of that, as is getting used to interruptible supply (I have recently written about this in the Indian context, as well as in the article linked to above in relation to Europe).

The money can only be spent if it is available, and I am arguing that it will not be. The single currency crisis has barely begun.... BAU is not going to be physically possible

Well, let's decide what we're arguing about. Are we arguing about biophysical reality, or are we arguing that humanity's economic systems are in disarray?

The biophysical reality is quite optimistic. Wind is scalable, high-EREOI, affordable, etc. So is solar, though not quite as much.

Your predictions were completely wrong about the 2008 economic events: people who took the related advice to pull all of their money out of the financial markets would have lost half their money.

I doubt if you have read what I had to say on the matter since I left TOD. My predictions were not wrong. I said in 2007 that there would be a financial crisis and there was. I said in early 2009 that there would be a major rally and there was. Now I am saying that the rally is over and phase 2 of the credit crunch is beginning. We are not in a recovery, but I realize that people think we are. Things always look good at tops and people typically extrapolate current trends forward. IMO it's far better to anticipate trend changes.

If you are interested in what I have to say on reality and renewables, then by all means read the article I linked to above.

Here's a prediction from November 2008:

"We appear to be beginning a market rally at the moment, which should lead to precisely this set of trend reversals. Such a rally is only temporary relief however. It may last for a couple of months, but then the decline should resume with a vengeance."

http://theautomaticearth.blogspot.com/2008/11/debt-rattle-november-29-20....

That was 48 months ago...

------------------------

More stuff from 2008:

"Also in the real world, trade itself is increasingly in danger. "The Baltic Dry shipping index, a proxy for world trade flows, suffered its second biggest-ever fall yesterday, to 11%, which took it down under the $2,000 mark and it fell another 8% today to $1,809. The drop means it has fallen more than 80% since July's peak of around $12,000 and is now at a three-year low." Translation: there will be a lot less goods on the shelves in your neighborhood stores, and a lot less raw materials to process in your factories."

http://theautomaticearth.blogspot.com/2008/10/debt-rattle-october-15-200...

"We are seeing the beginning of a global demand collapse, as the credit crunch takes an ever increasing toll on global economic activity and international trade. Already we are seeing the dire effects on shipping in the Baltic Dry index, thanks to the difficulty in obtaining letters of credit for shipments. Consumers in developed countries are tapped out and trying to repair their tattered balance sheets by cutting back, as are companies and banks. Consumption is therefore falling, which will hit exporting economies very hard indeed. They have spent vast sums, and used huge amounts of raw materials, to build what will now be shown to be an enormous excess of productive capacity. Their demand for raw materials will not recover any time soon, as there will be no demand for their products for a very long time. "

http://theautomaticearth.blogspot.com/2008/12/debt-rattle-december-7-200...

You quote a piece from November 2008 which was talking about a shorter term move preceding the beginning of the major rally. That was a short term market timing prediction that has nothing to do with the point you are trying to make. I called the bottom of phase one of the credit crunch and the imminent beginning the the rally a few days before it began. A the time I said it would last AT LEAST 6 months. Please do not confuse short term forecasts with big picture ones. Also, I did not write all the material you quoted. Some was written by my writing partner Ilargi.

We are going to see those other forecasts borne out. It is only a matter of time. In some places, notably the European periphery, they are already people's reality. Note the European day of protest against austerity that happened today. Many more countries will be Greece in the future.

The trend has already changed again in North America, and we are the beginning of a major move to the downside. Once the market trend changes, the real economy is living on borrowed time.

That was a short term market timing prediction that has nothing to do with the point you are trying to make.

It seems to speak for itself - the prediction was that the 2008 Great Recession would continue, not turn into the recovery we've seen.

A the time I said it would last AT LEAST 6 months.

2 months or 6 months, we're at 48 months and continuing.

We are going to see those other forecasts borne out. It is only a matter of time.

That's the classic cry of the permabear - "just wait, sooner or later, things will crash!" I remember reading a biography of a permabear, who lost money for 20 years until he went into real estate - ironically, he made money from a bubble that did eventually crash (but after he got out, lucky for him).

March 31st, 2008, Ilargi: "Not that I see a significant rally this year, not even a bear one, the model is already too broken." http://theautomaticearth.blogspot.com/2008_03_01_archive.html

In November 08, you were advising people to short the stock market: "Sell equities, real estate, most bonds, commodities, collectibles (or short if you can afford to gamble)". This strategy would have lost a lot of money in the last 4 years.

Similarly, in 2009 your blog said the Dow would crash that year, and reach 1,000 in 2010: instead, the US stock market was up for the year, and has continued to recover. The blog predicted sharp, dramatic price deflation - three years later all measures of prices show growth.

This is not a recovery. It is a counter-trend rally. The financial crisis that began in 2007 is not over. The evidence is everywhere if you know what to look for.

You are taking things I wrote out of context. The short term prediction from November 2008 was for a rally at a small degree of trend, which is what happened (a 2 month sideways correction). The downtrend then resumed, as I said it would until early 2009. At that point I said to expect a much larger rally, which is what happened.

The advice to cash out still stands. Sitting on the sidelines in cash, or cash equivalents, is the safest place to be. Real estate has crashed and has much further to go. People trying to make back the money they lost in the market are likely to hang on too long and give back all their gains and then some. Investors are chasing yield, but high yield bonds are going to crash. People will lose the income and the capital. This is a time to preserve capital as liquidity.

Those who began to prepare in 2008 will not be sorry they did. Others will be surprised, again, as they were in 2008. By the time they realize what is happening, it will be too late to do anything about it.

In times of economic stress, investing in long lived energy producing infrastructure with excellent returns seems like an ideal thing to do. At some point in the decline, it may no longer be possible to continue such massive investments - but you have the already installed generation generating.

So, if Germany is to "hit the wall" in X years, they should make as large investments as they can as the wall approaches. Better more than less renewable power (minimum input once in service) as society crumbles.

Several years ago I saw a financial analysis of a US wind power project. Other than land lease costs, 90% of the lifetime costs of the wind farm were invested on the day it was finished. This implies that if EROEI of wind is 40 to 1, just maintaining and operating an existing wind farm has an EROEI of 400 to 1.

I suspect the EROEI of maintaining and operating existing solar PV is even higher. (Dust it off and remove bird droppings are good, but not required. Maintaining transformers is required, but new ones should last 50+ years).

A society going into a stressed situation should have as large an installed base of renewable power as they can possibly install - along with pumped storage and redundant transmission capacity (at least redundant during an economic depression). Very well insulated homes & buildings, structural efficiency in all areas are also to be prized and developed to the max as the "wall" approaches.

Best Hopes for Germany,

Alan

"The money for the transition to 100% nuclaer energy is available?"

Nobody has ever asked for such a thing, in the case of Germany some people, who are in favor of nuclear power, have questioned the fact that instead of stopping 8 GW of heavily polluting coal Mrs.Merkel pushed by her green friend has stopped 8 reactors, 7 of which perfectly functioning, because of a danger of tsunamis in the middle of Germany...that's completely different story.

OK, this aspect of the German Energiewende is IMHO a clear mistake, we should simply have used the nuclaer reactor 10 years longer and could have used the 14 billion the utilities were willing to pay for useful stuff like off-shore transmission lines or socializing the transmission net etc. You can add that some of the public relation work of the German government was very weak, so we were lucky that the French had last winter much more problems than we had. :-)

However, to claim as many nuclear supporter do that this political U-turn led to an increased CO2 production in Germany is nonsense, according to the hard data we have for the years 2000-2011 it slowed down the decrease. BTW the pro nuker use the same useless "tsunami" style argumentatuion as the greenies in case of the Japanese power plants.

From a purely economic POV the current situation is not sustainable for Germany and with a majority of the people rejecting nuclaer power the transition makes sense. BTW after the last three years with dramatic price increases of imported energy nobody is any longer arguing that a changed energy structure would work for less money. The transition costs money, no question, but what is the point of waiting?

The only alternative - nuclear fusion - can be expected as lab bench version in 2026, the first reactor which gives us information about real prices around 2035, this is too late.

"However, to claim as many nuclear supporter do that this political U-turn led to an increased CO2 production in Germany is nonsense"

Well... the electric sector of Germany had a 4% increase in the emissions, that is official data from the federal agency... it's not the nuclear supproters who invented it...the overall emissions went down, but that incluse everything else which is not electricity production.

"The only alternative - nuclear fusion - can be expected as lab bench version in 2026, the first reactor which gives us information about real prices around 2035, this is too late."

I am afraid you are wrong on this... the ITER project is being left down by the very people who fought for it... the wonderful politicians bureaucrats in the various commissions and panels who oversight the project are hitting the brakes, asking the project management to go slow "because there is no money in this time of economic slowdown"... and every delay at this stage means additional costs... it's a never ending series of delay-cost increase-further delay- further cost increase...and so on. Sure, some people/labs are working already on DEMO,the successor of ITER and the first real fusion power plant, but that's decades away, more than 2 decades... it would have a plasma volume 3-4times as big as the one for ITER... no way to have it funded.

ITER: My version was the best case scenario with the infos I got from the ITER homepage 2011. My personal opinion after some discussions with physisists is that it will be much later. The crucial point for me is, even in the best case scenario we will very likely have reached a point of no return with renewables in Germany around 2035-40, i.e. a fusion reactor would not longer fit in the production landscape and has very likely to compete with wind that delivers electricity for less than 5 cent/kWh.

You are wright that this was a political screw-up, first the decision to run this as international project, than the permanent political problems (see the discussion after 9/11). It would have been much better to run some national projects. May the fittest win.

Construction of new transmission is extremely expensive...hundreds of billions and take decades

If we're talking, say, $200B over 30 years, that's $7b/ year - that's pretty small in the normal range of expenditures in the very large energy economy.

Intermittent renewables assume system parameters but do not offer the ability to control them - no frequency control, no voltage control, no spinning reserve, no black start capacity.

That's not really true. Frequency and voltage control are available in newer turbines, and spinning reserve and black start capacity are just a matter of design - they haven't been needed at this point, but like hydro they could do so.

typically low EROEI energy sources

Wind is about 50:1, and modern solar is pretty good (though we don't have great figures - solar EROEI research pretty much stopped when it got "good enough" - all we know is that's improved since then).

we will have neither the time nor the money to build out the grid

That's the time to invest. Heck, business investment continued strong through the Great Depression.

@ulenspiegel:

"PV at least 100 GW 100 TWh

These assumptions are quite conservative and usually come from other serious studies (Fraunhofer institutes etc.), at least PV and wind (higher FLH) could even be higher."

The actual 30+ GWp of PV installed in Germany produce with a capacity factor of 10%... i.e. less than the 11.5% implied by your 100 TWh/year with 100 GWp... to do that Germany would need a lot more sunshine, for the 70 additional GWp to be able to increase the production.

PV in Germany is a total oxymoron, you'd better make international agreements with southern Europe countries, to produce for you and send it over to the factories in southern Germany, the big consumption centers... although then you'd have to deal with the grid losses... ah!... never mind, just junk the idea of running a modern heavily industrialized country with PV!

From november to february the production of PV installations in Germany is pityful to say the least...

http://www.sma.de/en/company/pv-electricity-produced-in-germany.html

Check the past two weeks!... change the date and check last winter's production!... and the worst has still to come!

Remember: reality beats fantasy 100% of the time.

You once again only show that you do not get it :-)

The idea is to store part of the summer excess production either as chemicals or as potential energy in Norway; therefore, the low winter production is not the real problem. And your main problem is, that 2/3 of Germany's projected productions comes from wind which provides energy when PV stinks:

http://www.ise.fraunhofer.de/de/downloads/pdf-files/aktuelles/stromprodu...

(esp. page 13 is interesting :-))

1 kW(p) produces on avarage 960 kWh electricity per year in Germany, therefore, 100 GW will produce around 100 TWh, any problems? Please get at least the simple math problems straight before you post. :-)

But I have to admit at least you got one thing right: "reality beats fantasy 100% of the time."

I noted that apparently the data was not adjusted for the # of days/month (29 for February 2012).

Depending on where in the months the highs & lows are, using hydroelectric & pumped storage to shuft power from January to February may be all that is needed.

Alan

The January 2012 was an exceptionally good month for wind so in an average year we can expect more days with no production from PV and wind, check the last days in October (23rd-26th) to get a feeling for the need of a reliable long term storage, the same could happen in February.

"1 kW(p) produces on avarage 960 kWh electricity per year in Germany, therefore, 100 GW will produce around 100 TWh, any problems? Please get at least the simple math problems straight before you post. :-)"

My math is just fine, it is your data which stink, dear ulenspiegel!... show me a reference to data which show an 11% capacity factor for German PV as a whole... and I'll believe you... I have seen data hinting at a 10% max CF... so each kWp produces less than 900 KWh/year.

So, it is up to you to back-up your claims, you will not have any problems at finding the data in a yearly report from the German federal agency, right?... I, not speaking/reading german fluently, would have a much harder time. Thanks in advance.

Going to the chemical storage thing/fantasy... just tell us, data at hand please!... what percentage of TODAY'S wind/PV production is actually stored as such... and, again, I will believe you and change my mind.... you see, I do not have an agenda behind me to defend, contrary to you.

You or others in the business may have an "idea", but idea do not produce electricity automatically, they need a practical, economically sound, technologically attainable implementation... otherwise they move quickly from the category "potentially good ideas" to "impractical dreams", of which the history of technology and science is full!

Looking forward to seeing your data, cheers.

. what percentage of TODAY'S wind/PV production is actually stored as such

Why the heck would anyone do that now? Any storage of wind/PV inevitably has conversion losses, and wind/PV aren't large enough to need storage yet. So, it would make no sense.

On the other hand, electrolysis of water into hydrogen accounts for 4% of hydrogen production even now, and underground long-term storage of hydrogen is an old and proven technology:

"Underground hydrogen storage is the practice of hydrogen storage in underground caverns[1], salt domes and depleted oil/gas fields[2][3]. Large quantities of gaseous hydrogen have been stored in underground caverns by ICI for many years without any difficulties[4]. The storage of large quantities of hydrogen underground in solution-mined salt domes[5], aquifers[6] or excavated rock caverns or mines can function as grid energy storage[7] which is essential for the hydrogen economy[8]. By using a turboexpander the electricity needs for compressed storage on 200 bar amounts to 2.1% of the energy content[9]."

http://en.wikipedia.org/wiki/Underground_hydrogen_storage

"Why the heck would anyone do that now? "

What the heck do YOU mean with that? If not now that they have installed 60+ GW of combined wind and PV... when do you think they should START doing it?

I simply asked to the seemingly well informed posters from German-speaking countries to point out to my (everybody's) attention what percentage they do store as hydrogen... because reading some posts it seems that already now that is being done... while the reality is different, right?... there are only some R1D exploratory projects, aiming at verifying the feasibility of the whole thing.

That's all.

when do you think they should START doing it?

When wind & PV get rather larger than now, and rather more conventional generation has been retired.

The whole point of these projects is seasonal storage, and there's more than enough conventional generation available to handle a week of low wind production.

Again - underground hydrogen and methane storage are very old, large, tried & tested systems. Right??

As pointed out by Nick, hydrolysis provides 4% of the hydrogen today.

Research at the University of Iceland has shown that using hot water reduced the electricity required (from memory 25 C > 90 C water reduced electricity by -19%).

Hydrolysis is about the simplest chemical reaction.

It will work, I am very confident of that.

Alan

According to the AG Energiebilanzen, THE source for Germany when it comes to energy, 19.3 TWh electricity were produced in 2011 by PV, the installed PV power was end of 2010 17 GW, end of 2011 24 GW, so we have on average 20 GW installed PV in 2011. Therefore, ~965 kWh per kW(p) were produced. Still problems with math and results?

http://www.ag-energiebilanzen.de/viewpage.php?idpage=65

http://www.solarwirtschaft.de/fileadmin/media/pdf/bsw_solar_fakten_pv.pdf

Re storage: Why don't you try some academic papers, the Fraunhofer Institut publishes IIRC in English. However, since you behave like my 15 year old son, I will not do more of your homework and will not provide links for storage systems.

And a fair warning: As long as you do not know the basics of scientific methodology stop nonsense like "You or others in the business may have an "idea", but idea do not produce electricity automatically, they need a practical, economically sound, technologically attainable implementation... otherwise they move quickly from the category "potentially good ideas" to "impractical dreams", of which the history of technology and science is full!"

"Re storage: Why don't you try some academic papers, the Fraunhofer Institut publishes IIRC in English. However, since you behave like my 15 year old son, I will not do more of your homework and will not provide links for storage systems."

Well, thanks for the compliments, it's always a pleasure to discuss with you... I just would like to point out that if you don't answer to this 15 year old all the other readers will be left in the blank too, and not all of them will take your conclusions for granted. But I see that your posts keep on being "commercial time"... sorry for interrupting it.

Anyway, time will tell... I'll just wait a bit longer, until it will become more evident how nonsense this all is... for the time being I keep on looking at the daily production of German PV... and in the last weeks (not few days) it has never exceeded a peak around noon of 7-8 GW... for a daily production of 20~40 GWh, during days when the consumption of the country is probably more than 1000 GWh... and the shorter days of the year are not coming soon, more than two months to go...

By the way, I work as a scientist since more than 20 years, so spare me your nonsense on scientific methodology, OK?... in fact, talking about methodology... I have this bad habit of always checking the data... and if I look at the right document... which, as a matter of fact, is this one...

http://www.erneuerbare-energien.de/files/pdfs/allgemein/application/pdf/...

... and not the one you gave which compares only the first 3 quarters of 2011 and 2012... I see that the average PV power installed in 2011 (as per your methodology of taking the average of Jan 1st and Dec 31st, is 21.3 GWp, not 20 as you've stated, and if you divide 19.34 TWh by 8760 hours and by 21.3 GW you get an average capacity factor of 0.104... which, to be methodologically precise is closer to my 10% than your 11%... don't it? :-)

And please, provide any serious study that claims a 100% renewable with only PV? That is one of your cheap strawmans. The main contribution in all scenarios come from wind! And you waste a lot of time to follow the daily production of PV in winter, but you know that. :-)

Changing your opinion must really hurt. :-)

You work as scientist, welcome in the club. Why then your permanent problem to get good data? Fraunhofer, DLR et al. are the most serious sources for applied sciences and technology in Germany, why don't you use their data, much of the stuff is even in English. Are you really able to publish with your approach in your field? Lucky guy.

More serious, we have a new study of the Fraunhofer Institut für Solare Energieforschung, unfortunately only in German yet:

http://www.ise.fraunhofer.de/de/veroeffentlichungen/veroeffentlichungen-...

They try, in contrast to most of the older studies, to align the demand for electricity and heat; the IMHO most interesting aspect of this study is their assumptions for required power from PV and wind, page 16. The shift to much more PV is very likely a result of the dramatically decreased hardware prices of PV. The models seem to be very flexible and allow easily the incorporation of imports or other technologies like fuel cells.

And here something on methane from electricity, the document is a book in English by a Professor form Uni Kassel in cooperation with a Fraunhofer Institut; power to methane is discussed in chapter 4:

http://www.uni-kassel.de/upress/online/frei/978-3-89958-798-2.volltext.f...

Please avoid personal attacks while commenting.

Best,

K.

"You work as scientist, welcome in the club. Why then your permanent problem to get good data? Fraunhofer, DLR et al. are the most serious sources for applied sciences and technology in Germany, why don't you use their data, much of the stuff is even in English. Are you really able to publish with your approach in your field? Lucky guy."

I am a scientist but NOT in this field, if my day had 36 hours I could probably find all the data I need...on the other hand if you need a particle accelerator, I can be of some help immediately...

Cheers, and relax.

At least 190 MWh per annum (400kg of hydrogen per month) ... call it 0.1% of total intermittent generation ... at this single installation :

http://de.wikipedia.org/wiki/Kraftwerk_Prenzlau

http://www.spiegel.de/wissenschaft/technik/energiewende-dank-wasserstoff...

There are others. All are pilot plants. It's early days. Natural gas and coal *are* chemically-stored energy, after all.

It should be noted that the topic of the future development of the German electricity supply is quite controversial and that lots of studies about this question have been published with quite different outcomes.

DENA, which is a somewhat strange entity with government-private funding (somewhat similar to the International Energy Agency IEA), is among the most conservative and its studies have received harsh criticism, especially from NGOs. A few years ago DENA's boss was even about to change his job for a job in a major fossil-nuclear based power company. Until Fukushima DENA was energetically "lobbying" for building new fossil power plants, by warning of an "energy gap" - which even didn't happen when several nuclear power plants were shut down after Fukushima.

The conclusions "Conventional power plants will still be needed to a considerable extent in 2050." and "Germany cannot remain self-sufficient in electricity supply." should be viewed in this context.

Other studies came to the conclusion, that a power supply from 100% renewables is possible and on the long run cheaper than a conventional supply.

One example is the above mentioned study from the independent Environmental Council (in English: "Pathways towards a 100 % renewable electricity system"), which calculated 3 scenarios: A national self-supply scenario, a scenario with renewables distributed in a power network all over European and a German-Scandinavian scenario (taking advantage the huge pumped storage capacities of Norway).

From the German government is another study from the Federal Environmental Agency, which until now only calculated a national self-sufficiency scenario, which expects that the power storage problem is mainly solved storing methane created by electrolysis from excess electricity. The agency announced further studies with scenarios on an European and on a local level.

Speaking of Norwegian pumped storage I've been curious about how much pumped storage (and run of river generation) development to the current level has affected Norway's wild salmon stocks. Is there good informantion (in English) readily available on that subject? I'm aware that Norway has a large salmon farming industry--which can and does impact wild stocks--but I've really not much clue about how Norway's wild salmon runs have changed over the last two centuries.

I don't have that much of an ax to grind here as my commercial salmon fishing days passed near two decades ago, but I do value having large wild salmon runs and my home state has the largest one left in the world.

I understand any of our energy decisions are all about tradeoffs. I would like to know what sort of tradeoffs Norway has made for its run of river/pumped storage development to date. And just for the record I currently do support a fairly large run of river project here in Alaska--it should have minimal impact on the salmon run in that river if water temperature issues (reservoirs tend to raise river temps) are able to be addressed.

Here is the reality as I see it for Germany or any other industrial society. It's really quite simple.

First an assumption: We must maintain a sustainable environment or game over!

Therefore: Large scale use of Fossil Fuels and Nuclear Energy in the long term are pretty much verboten!

We have X amount of possible energy available from renewables

All societies must function with an amount of energy less than or equal to X

That means smaller and less energy intensive societies organized according to a different paradigm than our current one.

Deal with it!

Any questions?!

ah , we have this thing called "demos-ocracy "

If I state I can keep BAU going and delivery bountiful Supermarkets with food and X-factor on the box..

I guess I'll be voted in over anyone else advocating that , they , the voting public, should be going without......anything at all......

reality is that we'll get the BAU good an proper like

Got some popcorn in ?

going to be quite a show!

Forbin

In physics there ain't such thing as dem-o-cracy, something presidential candidates, congress and senate members should be acutely aware of.

No, sorry to burst your bubble but I don't think so!

actually I agree that BAU will not be possible - but that doesn't stop someone being elected who promises it .

the people will follow them

those that will make them feel richer and more safer - regardless of any facts to the contrary...

Forbin

PS: When their granny dies in hospital due to a wind power outage or the baby freezes to death the cry will go out - why here? why now ? who done this to us? the political astute will be on that band wagon and we'll have that "strong man" in charge.....

but thats life and the price of democracy is eternal vigilance ...

Some thoughts on Reserve to Production (R/P) Ratios, in regard to oil supplies

(Or why it's much later than we think)

I've been recently running some numbers on Reserve to Production Ratios (R/P), i.e., EUR divided by most recent annual production.

In general I think that this is the key, and largely overlooked, problem that we are facing, especially in the context of the ratio of CNE (Cumulative Net Exports) to annual net exports of oil.

When we divide reserves by annual production per year, you get the number of years of production, at that production rate. Of course, this is somewhat of an artificial metric, given that production declines are inevitable, but it is nevertheless a useful metric. And of course, we are generally looking forward, i.e., dealing with estimated reserves.

But in general, we are replacing older long field life reserves, with high R/P ratios, with short field life reserves, with low R/P ratios, e.g., US shale oil plays. This of course leads to the “Red Queen” problem, where one has to run faster and faster, just to stay in place. Note that slowly increasing production from unconventional sources like the Canadian tar sands play would be an exception to the generally falling R/P trend.

Some net export numbers:

IUKE + VAM (Indonesia, UK, Egypt, Vietnam, Argentina, Malaysia):

The combined Six Country case history hit a production plateau in 1995, at 6.9 mbpd, with production ranging from 6.9 to 7.0 mbpd (total petroleum liqudis) for 1995 to 1999 inclusive. In 2001, production was only 6% below the 1995 production rate. These six countries, as of 2011, were all members of AFPEC (Association of Former Petroleum Exporting Countries).

Remaining Six Country post-1995 CNE (Cumulative Net Exports) at end of 2001: 1.8 Gb, annual of 0.73 Gb. RCNE = Remaining CNE.

Actual RCNE to NE ratio at end of 2001 was 2.5 (2.5 years of actual net exports at 2001 net export rate).

If we extrapolate the 1995 to 2001 rate of decline in the ECI ratio (ratio of total petroleum liquids production to consumption), the predicted RCNE to NE ratio at the end of 2001 was: 3.7/0.73 = 5.1 years.

In other words, the predicted Six Country RCNE to NE ratio was twice as optimistic, based on extrapolating six years of data, as the actual RCNE to NE ratio.

So, with that, let's extrapolate some six year (2005 to 2011) GNE* (Global Net Exports) and Available Net Exports (ANE, or GNE less Chindia's net imports) data.

For GNE, we extrapolate the 2005 to 2011 rate of decline in the Global ECI ratio. For ANE, we extrapolate the 2005 to 2011 rate of decline in the GNE/CNI ratio (ratio of GNE to Chindia's Net Imports).

GNE:

Estimated RCNE to NE ratio at end of 2011:

347 Gb/16 Gb per year = 22 years

ANE:

Estimated RCNE to NE ratio at end of 2011:

87/12.8 = 7 years

In other words, using a methodology that was too optimistic--by a factor of two--for the Six Country case history suggests that at the 2011 ANE net export rate, the total remaining supply of cumulative net exports that will be available to importers other than China & India would be depleted in about 7 years.

*GNE = Top 33 net exporters in 2005, BP + Minor EIA data, total petroleum liquids

"Gap" Charts:

Global Net Exports, 18 mbpd Gap:

(2002-2005 rate of change: +5.3%/year; 2005-2011 rate of change: -0.7%year)

http://i1095.photobucket.com/albums/i475/westexas/GNE_02-11_Gap-1.jpg

Available Net Exports (GNE Less Chindia’s Net Imports), 17 mbpd Gap:

(2002-2005 rate of change: +4.4%/year; 2005-2011 rate of change: -2.2%year)

http://i1095.photobucket.com/albums/i475/westexas/ANE_02-11_gap-1.jpg

And IF (and it's a big IF) ANE did drop to zero towards the end of the decade, countries like the UK would be dependent upon their own production which would be around 0.5 mbpd by 2020 if recent production decline rates are anything to go by. That's 1 mbpd less than the UK consumed in 2011, or down two thirds from 2011 to 2020.

What is also interesting in the UK context is that Scotland (where the UK's oil is) has a referendum on independence from the rest of the UK at the end of 2014 by which time the UK will be getting 40% of its oil from imports (assuming recent production and consumption decline trends continue and assuming oil imports are available). Apparently the people of Scotland are likely to vote upon independence based upon which which option leaves them better off. The question is are they better off being a net oil exporter as a small independent country of 5.25 million people or as a net oil importer as part of the much larger UK?

As noted in my comment, the R/P ratio metric can be misleading, since a region doesn't maintain constant production for a period of time and then go to zero.

However, the extrapolation for a point in time when the Chindia region alone would theoretically consume 100% of GNE is not a whole lot better. If we extrapolate the 2005 to 2011 rate of decline in the GNE to CNI ratio (Global Net Exports divided by Chindia's Net Imports), ANE would approach zero in about 18 years.

There's no doubt that net export math is a real killer.

Not that many are aware. In the UK new car sales are up 12% in October.

There's a glimmer of hope in the form of efficiencies being achieved by local bus manufacturer Alexander Dennis:

and the reintroduction of the Borders railway line.

Meanwhile, I'm off this evening for a preview of the Renault Zoe electric supermini with orders opening in a couple of days time.

Scotland is an Energy Economy. England/UK is a financial and service Economy. Scotland is in the process of diversifying from an Oil/Gas focus to a renewable energy focus, but still an energy economy overall.

So your question is not representative of the situation. Going forward Scotland is not only reliant on Oil and Gas as a major revenue source. Yes, it will remain an exporter of Oil and Gas for decades (declining) but will be an increasing exporter of RE electricity (currently about 20% of total generation is exported to NI and England, some of it from Nuclear which is being phased out).

However, the South of the UK has a major problem. It is an increasing importer of OIL /GAS / ELECTRICITY and water from its neighbours. In parallel England has high population growth. Also In parallel the UK government strategy (not in Scotland, where generation is under Scottish control thankfully) is New Nuclear, but is way behind schedule and current decommissioning costs are going up all the time.

So, when discussing the UK on Energy, even if Scotland becomes independent or not, it is really much more accurate to separate the Scottish and English cases, as they are so completely different.

Note also that there is currently talks of a future grid connection between Scotland and Norway to mutual benefit.

An example of misleading info:

The longest undersea gas pipleine in the World from the Norwegian Sleipner field to England accounts for 40% of the UK gas imports. Except Scotland also exports Gas to England, much less than we actually use. The Sleipner pipeline costs the UK taxpayer and effectively Scottish taxpayers are paying towards something they do not use or need.

Lastly, the Economy of an independent Scotland is not the only reason people will vote for independence but it certanly is a key element. Another key element is for example the placement of Trident in Scotland, at huge costs. People in Scotland are overwhelmingly against trident in all polls on this topic, either morally or for cost reasons. The only way to get rid of them is independence.

North Sea oil and gas production peaked a few years ago and is now going into a very steep decline. I don't think the people or government of the UK have thought the implications of this through very carefully. They are on a ski jump, going downhill faster and faster, and don't have any plans for what they are going to do when they get to the end of the jump at the bottom.

Neither England nor Scotland is going to be an "energy economy" except in the sense of providing technical and financial services to the remaining oil exporters of the world. The days when the UK was an energy exporter are over and it will be an energy importer for the foreseable future. England, Scotland, it won't matter. The oil and gas is out in the North Sea and the fields are mostly depleted. The Brits and Scots I know are mostly working on developing projects in Africa.

Importing oil and gas from Norway is not a long term option, either. The oil and gas fields on the Norwegian side of the North Sea are not as badly depleted as those on the UK, but their production is now also in decline. The Norwegians, however, have a plan for what happens when it runs out. They have $600 billion Euros in their national retirement fund, and their large hydro-electric capacity to fall back on. They never did become as dependent on their own oil and gas as the UK did because they recognized that its day would come to an end..

I agree.

From the above post that you responded to:

Decades?

I don't think the author has much understanding of the very high costs involved in operating offshore.

You have a very poor opinion of myself and my post but no facts for this opinion.

Scotland has one tenth the needs of the UK and will with absolute certainty remain an oil exporter for decades to come. However this is not opinion it is fact. Current production and forecast figures are freely available. A good example is from the industry itself:

http://www.oilandgasuk.co.uk/2012economic_report/production.cfm

As for Scotland as an energy economy. Currently Scotland is massively surpassing the renewable energy targets set by the Scottish government till 2020. Scotland as I said is in transition from oil and gas to renewables (Onshore wind - in rampup, offshore wind - just starting, and later tidal power) but if you just want to mock these facts feel free.

Did you miss this part of the link you just posted?

North Sea oil production is going into a period of rapid and terminal decline, sort of like a jet airliner running out of fuel. It won't help Scotland to have a bigger piece of a rapidly shrinking pie. You need a better strategy. If England exits the EU, staying in could be a good strategy for Scotland.

Scotland really isn't in a much better situation than England. A friend of mine from Scotland invested in supposedly safe securities from the Royal Bank of Scotland, and lost about 5 million pounds, which I think was almost his entire pension savings.

Hi,

No I did not miss it, I pointed you straight at it but please go on and read the the details ahead of WHY there was such a large drop last year, rather than selectively posting to suit a given position. It wasn't because there was suddenly less oil left than thought. At least other viewers can read the entire content and decide for themselves. I actually thought people on the Drum tended to look at the full story and give balanced opinion? Nevertheless, what you failed to mention is the long term forecast showing that I was indeed correct in my orignal post: a steady decline over decades. That is what I was criticised about.

As for losing money in Bank securities, I wasn't aware this was a malady limited to UK banks? In any case what is your argument? Some speculators lose money in a UK bank (RBS is a UK bank, under UK financial services authority oversight that happens to have the Word 'Scotland' in it for historic reasons), due to risky investment policy of that bank and many others, largely into the US. So yes England and Scotland are not in great shape after that. Sorry for your friend but it does rather sound like he put all his eggs in one, unsafe, basket.

Finally, you are completely wrong about the shrinking pie imo.

It is indeed a rapidly shrinking pie. Yet, currently there is 0% to 8% 'extra regio' share of the pie going to Scotland as opposed to 100% (Where 100% of the pie = the 93% that is in Scottish territory). I could be wrong but you don't seem to appreciate that the already diminished pie still represents a large share of UK taxes. That shrinking share would still be of great benefit to Scotland if it is used to diversify our economy. That is a big IF, but if Scotland remains part of the UK state there is no IF, there will be no investment in Scotland from any of the proceeds of the remaining revenues at all. So, just how important is the remaining Pie to the UK? Well in the same year that seen the large drop you quoted this was the impact to the UK:

"In 2011/12, the industry paid £11.2 billion in tax on production, which is almost one quarter of total corporation taxes received by the Exchequer. The wider supply chain is estimated to have contributed another £6 billion in corporate and payroll taxes."

A quarter of the total corporation tax received by the UK.

I worked in the oil industry for 35 years, much of it as a business analyst, so I tend to look on oil industry forecasts with a somewhat jaundiced eye. When I see oil fields go into a steep decline such as the North Sea has seen, and companies claim it is a temporary setback, I tend to disbelieve them and suspect something has gone seriously wrong with their operations.

Offshore oil fields are very expensive to operate, and companies cannot afford to operate wells at low flow rates, unlike onshore fields where they can operate low flow "stripper" wells for decades - in some cases for over a century. Offshore, they have to produce their wells at their maximum flow rates to cover their costs, and when production falls too low, they have to abandon the wells and cease production from the field. This results in very rapid decline rates and early shutdown of fields.

The fields tend to decline on an exponential curve. If the UK North Sea produced 1.8 million b/d in 2011, and the decline rate was 50% per decade, then in 2021 it would produce 900,000 b/d, and in 2031 it would be 450,000 b/d. This is not a formula for long-term prosperity.

will with absolute certainty remain an oil exporter for decades to come.

"Decades" is at least twenty years, but many people would infer 30+ years from such a statement.

In the lives of nations, not a very long period at all.

The graphs do not go out to 2033 (20 years) or 2045/2050 (30+ years)

The output from fields currently in production is expected to halve within ten years without further investment.

The overhead to maintain operations in the North Sea is high - in both financial and energy terms. Once fields decline to the breakeven point, they are abruptly terminated. Or a 40 year old platform is judged not "sea worthy" and the remaining reserves do not justify a replacement. That will be the fate of many British North Sea oil field platforms by 2033 and even more by 2045/50.

Given the paucity of new discoveries in the southern half of the North Sea, established fields are quite unlikely to be replaced. Some very small fields not worth developing at much lower oil prices will come on-line - but hardly enough to fill Scottish domestic demand in the future.

I would not be so absolutely certain as you are,

Alan

BP shows 1999 UK production (almost exclusively offshore) and consumption of 2.9 and 1.1 mbpd respectively. In 2011, the numbers were 1.1 and 1.5 respectively, resulting in net imports of about 0.4 mbpd.

Here's an item I found:

http://www.guardian.co.uk/politics/scottish-independence-essential-guide...

So, for the sake of argument, let's assume that Scotland gets 81% of the production, and that their consumption is about 10% of overall UK consumption. The Scottish ECI ratio (Export Capacity Index, or ratio of total petroleum liquids production to consumption) would be 13.8 in 1999 and 5.9 in 2011, a rate of change of -8.5%/year. The 2011 numbers for Scotland would be approximately as follows:

Production: 0.89 mbpd

Consumption: 0.15

Net Exports: 0.74

An extrapolation of the 1999 to 2011 rate of decline in the ECI ratio would give Scotland about 21 years of net exports, but this method tends to be on the optimistic side, and as noted above and below, very high operating costs cause offshore production to be abandoned much earlier than onshore production.

Also, an extrapolation of the ECI decline rate suggests post-2011 CNE (Cumulative Net Exports) of about 2.6 Gb, with 2011 net exports of 0.27 Gb. This results in a post-2011 CNE to 2011 annual net export ratio (CNE/NE per year ratio) of 9.6 years, i.e., Scotland would have 9.6 years of net exports at 2011 current net export rate (which of course is declining).

I should note that when I applied this methodology to a combined six country case history (including the UK), the estimated CNE/NE per year ratio was twice as optimistic as what the actual data showed.

In any case, a pretty consistent rule of thumb suggests that post-2011 CNE would be at least 50% depleted by the end of 2018, six years hence.

First, thanks Westtexas, Alan and all for the latest replies, they all make good points, and I certainly cannot fully answer / challenge them.

For oil share: Scottish Government GERS 2012 report is the best official estimate.

The industry currently predict a 7.5% decline year on year, if conditions are favourable and only a slower decline if more funding comes forward as was mentioned. However the funding is very likely.

One point that is missed is that while the North sea basin is on the ramp down, WOS (West of Shetland°) is on the rampup, but discoveries so far are lower than expected and conditions are more extreme than in the North sea.

Also WOS does not have the benefit of the mutual support structure in the North of the North Sea shared by Norway and Scotland that will keep extraction profitable for longer than it would if they were by themselves which is ths case WOS.

Lastly, even when Scotland stops as net exported the revenue and economic benefit is still 10x greater that it would be as part of the UK.

As ever, I am impressed by and generally agree with the analysis from Westexas - many thanks for doing the net export math.

While North Sea oil and gas is in rapid terminal decline, the big push in Scotland at present is to renewable electricity generation. In 2011, renewable electricity generation was 35% of Scottish electricity demand. The target for 2015 is 50% and 100% by 2020 when a subsea link to Norway is due to be in place.

Scotland has 25% of western Europe's wind resource and 1% of its population. Most wind capacity is onshore at present, but there are plans for offshore arrays. Similarly there are some of the best wave and concentrated tidal resources in Europe in Scottish waters and tidal energy is already being tapped on a small scale, with plans to scale up to around 1 - 2 GW capacity by the end of the decade. Pumped storage is being expanded in the highlands with plans for a 600 MW facility at Lochaber and the coal fired power station at Cockenzie is to be replaced with a gas fired one.

The power distribution network is being strengthened with a higher capacity power transmission interconnect between Beauly and Denny due for completion by 2014 to bring wind, wave and tidal generated power south. Similarly new HVDC subsea bootstrap links will export power down the west coast (from Hunterston to Liverpool) and east coast to England.

Well drillo didn't come back up above, maybe a Scott can help. How are your wild salmon stocks faring? A while back I saw salmon return numbers the Icelanders were very proud of but those figures looked awful anemic when compared the likes of Bristol Bay returns. I don't really know much about Atlantic salmon. Do you know of any good material on historical distribution and run sizes relative to present day available in English on the web? West coast hydro projects decimated huge parts of the Pacific salmon population over the last hundred years, was the situation in Europe comparable or entirely different?

Fred. I hope you send this to drumbeat every other day. They seem to forget awful fast.

No questions, Sir.

Even before reading the article through I saw a "red herring" at the top.

Pumped storage does not increase. MASSIVE investments in every other area, but the best alternative to adapt renewables to the grid is ignored.

Germany & Austria have signed an agreement to develop more pumped storage in Austria (and I think Bavaria). This agreement seems to be ignored, as do basic economic drivers.

Given the above, I will read the rest of the article later - if I have time. With no other information, I can sense a slam against renewables using "selected data". I will work on my webinar instead.

Alan

Alan, the pump storage capacity is not a real fix for the winter problem because even if Austria has nice pump storage power it does not provide meaningful long term storage capacity.

Germany can expect 15 days per year without sun due to high fog and without wind. Therefore, you need at least 25 TWh energy (15 d * 1.7 TWh/d) in long term storage (~half a year). Biomass should go into chemical industry, PV summer excess energy should be stored, esp. when some models work with more than 150 GW PV. In addition you need in the 100% renewable scenarios for these 15 days a lot of power (75 GW). The only countries which can deliver both, 30 TWh energy storage and power are in principle Sweden and Norway.

The second approach is to convert summer excess energy into hydrogen or better methane, the latter could easily be stored in Germany's large caverns. However, with around 6-7 cents /kWh costs only for the production facilties, the large scale synthesis of methane looks for me as chemist less promising than the Scandinavia storage solution.

Without reading the article in full -

I thought Nord Sea wind was strongest in the winter. A good balance to solar. Pumped storage can shift a few days.

For the United States maximum non-carbon grid, I assumed highly variable pricing. Floor was where synthesis of ammonia or methanol (my preferred chemical storage mediums) could use hydrolysis of heated water (less electricity required) to make hydrogen - which would be stored & feed into ammonia/methanol synthesis. My guess was between 3 & 4 cents/kWh.

Upper bound was where carbon would be burned - set by carbon taxes. Say 40 to 60 cents/kWh.

Overall electircity prices would be higher (say +60%) but bills would be stable due to -40% lower per capita use (0.6 x 1.6 ~= 1).

Since Germany is steadily reducing their energy use while growing their economy (-1.8%/year) such an approach may be viable in Germany. Planning should be for steadily reduced TWh/year, not stable. Perhaps 2/3rds today by 2050 due to electricity being a higher % of total energy.

Best Hopes for Germany,

Alan

In principle all three compounds should cause very similar production costs, methane has the advantage of already available infra structure, methanole would be nice in case of cheap fuel cells, what do you make with ammonia? Nitrate? Any chance to burn this in local power plants?

After WWII the worst case were 8 consecutive days without wind and sun for Germany during winter, that is the absolute minimum (15 TWh) you find for long term storage demand in studies, around 15 days (25 TWh) for the whole winter, 20 days worth of energy with some buffer.

The available biomass in Germany can either cover the demand of the chemical industry if I calculated correctly or provide the energy for the winter gaps, not both. The decision what to do with biomass may lead to quite different scenarios, the current situation with biomass in base load is nonsense.