Tech Talk - The Oil and Natural Gas Around Sakhalin Island

Posted by Heading Out on February 12, 2012 - 7:07am

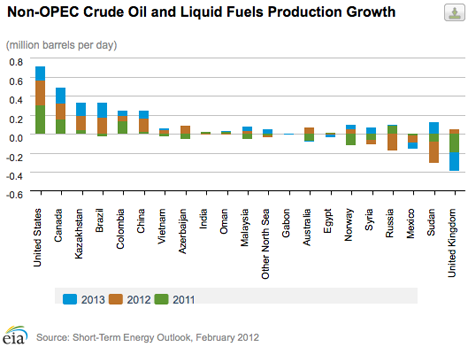

The EIA Short-Term Energy Outlook (STEO) for February 2012 included a chart for anticipated changes in production for countries outside OPEC over the next two years.

(Note the change from January moves Mexico past Sudan where over 200 kbd have been shut-in through conflict, and that Russia is showing negative and is towards the back of the pack).

In regard to Russian production, the January STEO commented:

EIA expects Russia's crude oil and liquid fuels production to fall by about 190,000 bbl/d in 2012 and an additional 12,000 bbl/d in 2013. These declines follow production of 10.3 million bbl/d in 2011, a post-Soviet record-high that positioned Russia as the world's top producer. Russia's government introduced tax decreases on some petroleum exports, which seems to have affected total exports in the last quarter of 2011. Additionally, production in the eastern part of the country offset the Western Siberia declines to some extent. EIA expects, however, that absent meaningful tax structure reform, investment will remain scarce, contributing to the projected drop in Russia's production in 2012 and 2013.

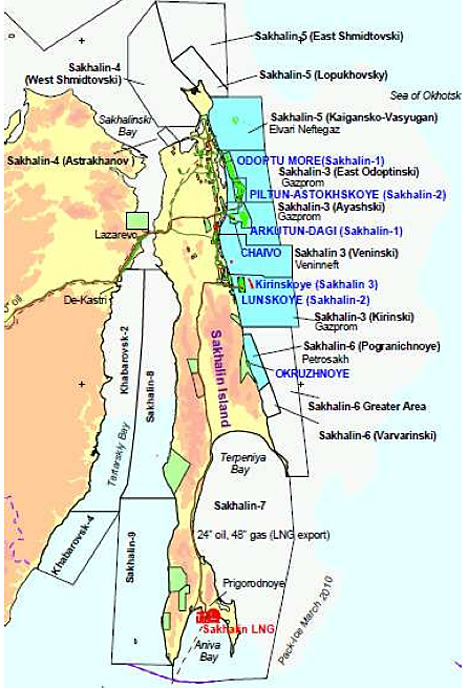

Having discussed the production declines in the Western Siberian Basin, and the increasing production from the smaller Eastern Siberian region, it's time to move further East, as Russian exploration has, to find and discuss the oil and gas resources found around Sakhalin Island. The Island lies just north of Japan and off the Amur River, within the Sea of Okhotsk.

At the time that we first began writing about the island back in 2005, it was still being developed and could only produce and ship product for six months a year when the weather allowed. Sakhalin 1, the first phase of development, began production of natural gas in 2005, with oil production being ramped up from the seasonal production at the start in 1996 to 250 kbd by 2010. The major gas production came with Sakhalin 2.

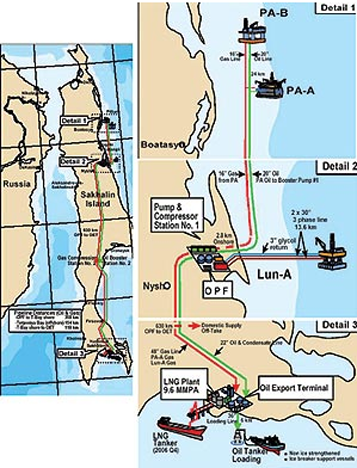

At present, production from the Chayvo and Odoptu fields are feeding the Chayvo Onshore Processing facility, which can handle up to 250 kbd of oil, and 800 million cu ft of natural gas per day. As Chayvo declines into 2014, then Arkutun-Dagi will be brought on stream to sustain production levels. The oil feeds through the pipeline to an ice-free terminal where it is loaded onto dedicated Aframax tankers, each moving 100,000 tons (720 kb) of oil at a time, and with the terminal it is possible to load year-round. A new pipeline is also being installed to carry natural gas to Vladivostok. However, it is being run by Gazprom, who have found that it cannot be filled with the natural gas supplied from Sakhalin 2 and Sakhalin 3, and so Gazprom is negotiating with Exxon Neftgas to purchase all the natural gas that is produced from Sakhalin 1 (which will, in time, include more from Chayvo in Phase 2). On the other hand, Exxon would prefer, because of the profit, to sell the natural gas to China rather than to domestic Russian consumers, but they are going to be over-ruled. The fields of Sakhalin 1 are considered to have reserves of 2.25 billion barrels of oil and 17 Tcf of natural gas.

As with other regions of Russia, the interplay and conflict between the government and their agencies and the Western oil companies brought in to develop the reserves has also been evident over the past few years. By 2006, when development of the total estimated 45 billion barrels of oil and natural gas oil equivalent was moving into the second phase of production, Shell, who was running this part of the program, ran into an environmental problem. It had actually started with the initial agreement signed back in 1996:

. . . most observers agree (it) was inherently unfair to Russia - a deal signed in 1996, when oil was $22 a barrel and Russia was on its knees, that gave the Shell-controlled Sakhalin Energy Investment Corp. the right to recoup all its costs plus a 17.5% rate of return before Russia would get a 10% share of the hydrocarbons coming out of the ground.

Then there was the cost of the second phase of the project, which ballooned from $10 billion in 1997 to $20 billion in 2005, fueling a perception that the company was profligate while Russians picked up the tab. The chapters in between include a calamitous safety record, a failure to meet local expectations for new roads and schools, a fuel spill in Sakhalin's third-largest city, and environmental concerns that caused anger and resentment toward Shell's leadership, earning it a reputation for stubbornness and for consistently misreading political realities.

The end result was that while Shell initially had 55% of the shares, with Mitsui and Mitsubishi having 25% and 20% each, Gazprom stepped in to buy, for a total of $7.5 billion, half the shares of each partner so that Sakhalin Energy is now owned by Gazprom (50%), Royal Dutch Shell (27.5%), Mitsui (12.5%), and Mitsubishi Corp (10%).

The LNG terminal, supposed to come on line in 2008, was targeted to supply 156 tankers a year, with the output pre-sold for the next 20-years. The terminal did not come on stream until 2009, when the first 67,000 tons of LNG were shipped to Sodegaura, Japan. Japan is taking some 60% of production, with the remainder initially going to South Korea and the United States. This was followed by shipments to Tohuko in May 2010, and while production still lagged the original delivery volumes, it was increased in 2010 to a total volume of 10 million tons of LNG. Additional volumes are now being shipped to South Korea and the shortfall appears to have been abated. However, such is the demand for LNG in the Pacific that the partners are now considering the addition of a third gas train for another 5 million tons/yr at the terminal in order to meet the increased demand from Japan, following the closure of some nuclear plants following last year’s tsunami. The reserves in the Piltun-Astokhoye and Lunskoye fields (Sakhalin 2) are estimated at 1.3 billion barrels of oil, and 33 Tcf of natural gas.

There will be additional projects carried out over time, going all the way up to Sakhalin-7, with Gazprom having the largest share of Sakhalin-3. That project contains an estimated 3.3 billion barrels of oil and 25 Tcf of natural gas, with the natural gas estimated to come into the pipeline in 2014. (Note that the reserve figures come from the Minister of Investment and Internal Affairs of the Sakhalin Region on Jan 30, 2012).

Even with those phases included, and they reach far out in years, it is difficult to see much increase being achieved over the 310 kb of production that was achieved in 2009. There will be increases in natural gas production, and this will be of benefit to Japan and South Korea, being a resource that it not that far away. But with a declining crude oil production from Western Siberia, it is hard to see how Sakhalin Island production will do much to sustain overall Russian production, let alone increase it.

Contact

- Content: editors at theoildrum dot com

- Tech support: support at theoildrum dot com

License

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.

World's Longest Extended Reach Wells

BD-04A (Maersk Oil) Al Shaheen (Qatar) 12.298 m (40.320 f) 2008

Z-12 (Exxon Mobil) Chayvo (Russia) 11.680 m (38.320 f) 2008

Z-11 (Exxon Mobil) Chayvo (Russia) 11.288 m (37.014 f) 2007

M-16SPZ (BP) Wytch Farm (UK) 11.285 m (37.001 f) 1999

Cullen Norte 1 (Total) Austral (Argentina) 11.191 m (36.693 f) 1999

Z-2 (Exxon Mobil) Chayvo (Russia) 11.133 m (36.529 f) 2004

Z-1 (Exxon Mobil) Chayvo (Russia) 10.994 m (36.072 f) 2004

Z-7 (Exxon Mobil) Chayvo (Russia) 10.916 m (35.817 f) 2006

Z-3 (Exxon Mobil) Chayvo (Russia) 10.674 m (35.023 f) 2005

M-11Y (BP) Wytch Farm (UK) 10.665 m (34.967 f) 1998

Thanks for the info - which I had not caught on to. Seven of these are in the fields I commented on in the main post.

Strange how the U.S. was able to increase so much. Unexpected. I know that fracking the Bakken is part of that. What else?

Heading Out,

Just a few points as I am working up that way.

1/The word is the 3rd LNG train has been dropped

2/The Gas pipeline to the mainland is going full steam ahead

3/There plans for a Piltun C platform, but SEIC have not fully committed as yet

4/The gas wells are completed with 9 5/8" tubing, and produce up to 350mmscf/d, they are big wells

Small world, I've also been working up there the last several years. It's been how shall we say it, "a learning experience" for sure.

Regarding point 3, I remember SEIC said the results from their logging program on the last PA-B well would play a role in determining whether to proceed with PA-C or not. But I haven't heard anything firm as yet on a decision. One of the guys I speak with daily seems to think it will go through but you never know.

RC

It maybe a smaller world then you think.

Ot: I've always anted to go fly fishing on Sakhalin Island.