| Tech Talk - California Oil and Hubbert Linearization | The Oil Drum | An alternative version for three of the “key graphs” in IEA’s 2010 World Energy Outlook |

Peak Coal and China

Posted by JoulesBurn on July 4, 2011 - 10:56am

This is a guest post by Dr. Minqi Li. Dr. Li was a political prisoner in China from 1990 to 1992. He received a PhD in economics from University of Massachusetts Amherst in 2002, and he has been teaching economics at University of Utah since 2006. He has published many articles on peak oil, climate change, and global economic crisis in journals such as Monthly Review, Science & Society, Review, Journal of World Systems Research, Development & Change, and Journal of Contemporary Asia. His book, The Rise of China and the Demise of the Capitalist World Economy, was published by the Pluto Press and the Monthly Review Press in 2009.

This post is excerpted from a longer paper which can be read in its entirety here.

World coal production is dominated by China. China's coal production is projected to peak in 2027 with a peak production level of 5.1 billion tons. World (excluding China)'s coal production is projected to peak in 2027 with a peak production level of 4.1 billion tons.

Coal is mainly used for “base load” electricity generation (to meet the part of the electricity demand that requires constant flows) and is an essential input in the iron and steel industry. In 2008, coal accounted for 22 percent of the world’s energy consumption in the industrial sector (including non-energy uses) and 4 percent of the energy consumption in the residential and commercial sector. Coal accounted for 41 percent of the world’s electricity generation (IEA 2010).

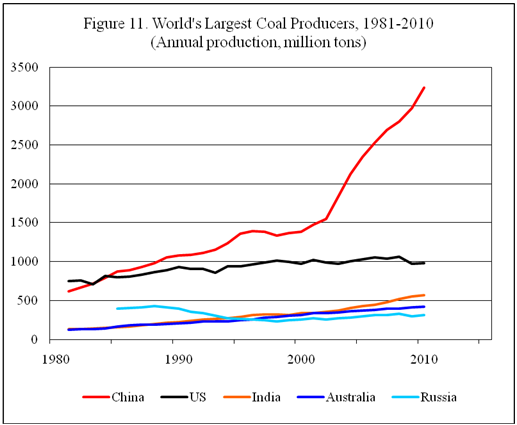

In 2010, world coal production was 7,273 million tons. Figure 11 shows the annual coal production of the world’s largest five producers. The world coal production and consumption is dominated by China. In 2010, China accounted for 45 percent of the world coal production (by volume) and 48 percent of the world coal consumption (by energy content).

The BP Statistical Review of World Energy reports China’s coal reserves to be 114.5 billion tons. This is the number that is widely cited by media and used by virtually all international energy institutions as China’s “proved” coal reserves. In fact, the BP number has not been updated since 1992. Given the observed rapid growth of China’s coal production, the reserves number reported by BP is likely to have substantially underestimated China’s remaining recoverable coal resources. Some earlier studies that relied upon the BP number suggested that China’s coal production could peak before 2020 and the peak production level would be less than 3 billion tons (see Heinberg 2009: 55-73). In fact, China produced 3.2 billion tons of coal in 2010.

Tao and Li (2007) used China’s official coal reserves at the end of 2002 published by China’s Ministry of Land and Natural Resources and estimated that China’s coal production could peak between 2025 and 2032, and the peak production level was likely to be between 3.3 and 4.5 billion tons. However, the Chinese government does not regularly publish the official coal reserves. According to various news releases, at the end of 2001, 2002, and 2003, China’s official coal reserves were 189.1, 188.6, and 189.3 billion tons respectively.

Since 2001, The Statistical Yearbook of China (published by China’s National Bureau of Statistics) has published regularly China’s coal “reserve base.” While “reserves” refer to the economically recoverable coal that can be actually produced after mining losses have been subtracted, “reserve base” refers to the economically recoverable coal before the subtraction of mining losses. For 2001, 2002, and 2003, China’s reserve base was reported to be 334.1, 331.8, and 334.2 billion tons respectively. A comparison of the two sets of numbers suggests that the implied recovery factor (the ratio between reserves and the reserve base) is about 57 percent.

In this study, a 60 percent recovery factor is applied to China’s coal reserve base from 2001 to 2009 to derive a “standardized” estimate of China’s remaining recoverable coal resources. The remaining recoverable coal resources in 2010 are assumed to be the same as in 2009 (the official data for 2010 are not yet available). From 1981 to 2000, The Statistical Yearbook of China published annually China’s “identified coal resources.” In 2001, the identified coal resources were 1.02 trillion tons or three times the reserve base. This study applies a 20 percent recovery factor to China’s identified coal resources from 1981 to 2000 to estimate the remaining recoverable coal resources during the period.

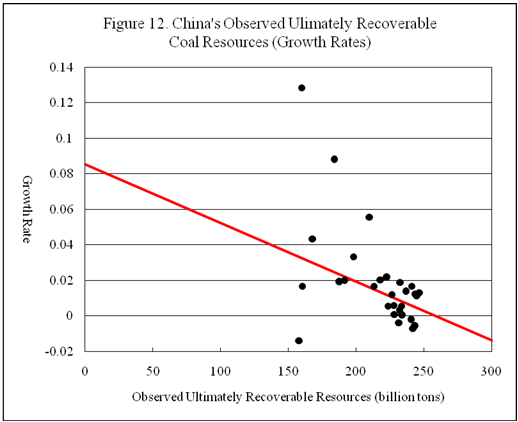

The sum of the estimated remaining recoverable coal resources and the cumulative coal production is defined as the “observed ultimately recoverable coal resources.” Figure 12 shows the historical growth rates of China’s observed ultimately recoverable coal resources.

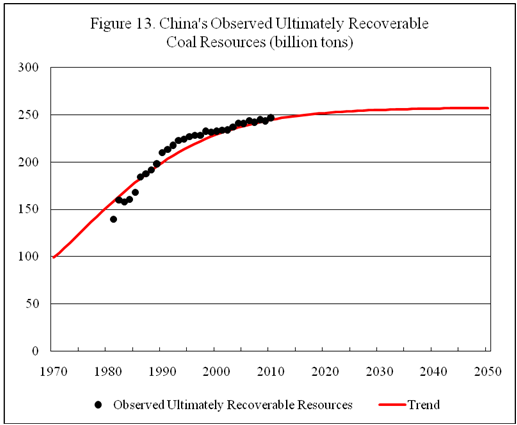

Regression for the period 1991-2010 leads to a downward linear trend suggesting China’s ultimately recoverable coal resources to be 257 billion tons. Figure 13 compares the historical evolution of the observed ultimately recoverable resources and the projected trend.

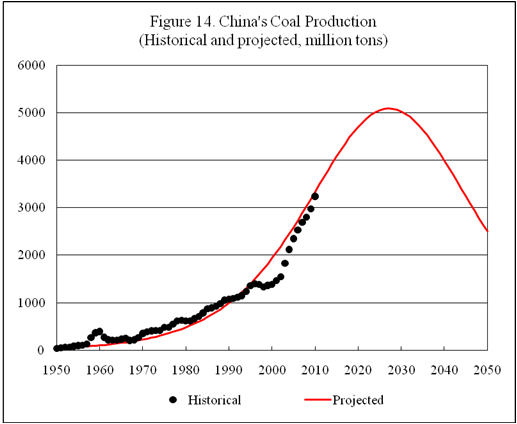

This report assumes that China’s ultimately recoverable coal resources will be 260 billion tons. Given this assumption, China’s future coal production can be projected by fitting a logistic curve to historical production levels. Figure 14 compares China’s historical coal production and the projected production. China’s coal production is projected to peak in 2027 with a production level of 5.1 billion tons.

In 2010, China overtook the United States to become the world’s largest energy consumer. China now accounts for about 20 percent of the world’s energy consumption and about 25 percent of the world’s total carbon dioxide emissions. China’s future development will have a major impact on the global economic, social, political, and ecological trajectories in the 21st century.

China depends on coal for 70 percent of the energy supply. If China’s coal production slows down dramatically and eventually declines in the coming years, China’s economic growth (and by implication global economic growth) will be severely constrained.

From 2000 to 2010, the Chinese economy expanded at an average annual rate of 10.4 percent and China’s coal production grew at an average annual rate of 8.9 percent. The economic growth rate was higher than the coal production growth rate only by 1.5 percentage points. However, after 2005, China’s energy efficiency improved rapidly. From 2005 to 2010, the economic growth rate accelerated to 11.1 percent and the coal production growth rate slowed down to 6.6 percent. The economic growth rate was higher than the coal production growth rate by 4.5 percentage points.

Taking the experience of 2005-2010 as a guide, this report generously assumes that China’s future economic growth rates will be coal production growth rates plus five percentage points. According to this report’s projection, China’s average annual growth rate of coal production will slow down to 3.8 percent for 2010-2020, 0.7 percent for 2020-2030, -2.3 percent for 2030-2040, and -4.6 percent for 2040-2050. Simple calculation suggests that China’s average annual economic growth rate could slow down to about 9 percent for 2010-2020, 6 percent for 2020-2030, 3 percent for 2030-2040, and 0 percent for 2040-2050. In other words, the Chinese economy will decelerate sharply after China’s coal production peaks and approach complete stagnation by the 2040s.

According to the BP Statistical Review of World Energy, at the end of 2010, world (excluding China) had 746.4 billion tons of coal reserves. However, out of the total coal reserves, 403.9 billion tons were sub-bituminous and lignite coal, that is, coal with low energy content and economic value. Only 342.6 billion tons were anthracite and bituminous coal of relatively high quality.

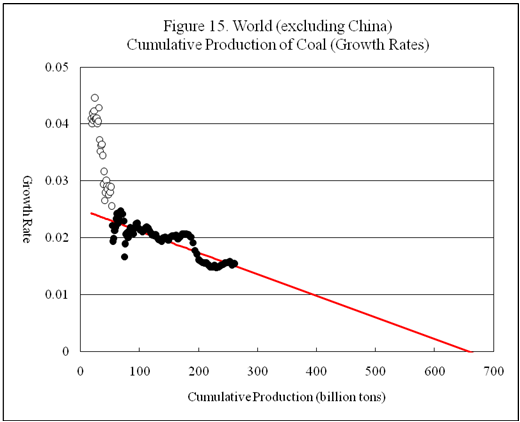

Figure 15 shows the historical growth rates of world (excluding China)’s cumulative production of coal. A long-term downward linear trend can be established based on the growth rates from 1931 to 2010 (regression R-square = 0.724). The world (excluding China)’s ultimately recoverable coal resources will be about 660 billion tons and the remaining recoverable coal resources will be about 400 billion tons. The predicted remaining recoverable coal resources roughly correspond to the anthracite and bituminous coal reserves reported by BP.

Figure 16 compares the world (excluding China)’s historical coal production and the projected coal production. The world (excluding China)’s coal production is projected to peak in 2027, with a production level of 4.1 billion tons.

Previous TOD articles on China Coal

China's coal bubble...and how it will deflate U.S. efforts to develop "clean coal"

The Chinese Coal Monster - running out of puff

References

BP. 2011. BP Statistical Review of World Energy 2011, http://www.bp.com/statisticalreview.

EIA. US Energy Information Administration. 2010. “Updated Capital Cost Estimates for Electricity Generation Plants,” November 2010.

____. 2011. “Short-Term Energy Outlook,” June 2011.

Heinberg, Richard. 2009. Blackout: Coal, Climate and the Last Energy Crisis. Gabriola Island, BC, Canada: New Society Publishers.

IEA. International Energy Agency. 2010. Key World Energy Statistics, http://www.iea.org.

Maddison, Angus. 2003. The World Economy: Historical Statistics. Paris: Organisation for Economic Co-operation and Development.

Rutledge, Dave. 2007. “Hubbert’s Peak, the Coal Question, and Climate Change,” Excel Workbook, originally available at: http://rutledge.caltech.edu (the dataset has been removed from the webpage).

Tao, Zaipu and Mingyu Li. 2007. “What Is the Limit of Chinese Coal Supplies – a STELLA Model of Hubbert Peak,” Energy Policy 35(6): 3145-3154.

WEC. World Energy Council. 2010. 2010 Survey of Energy Resources. London: World Energy Council.

World Bank. 2011. World Development Indicators.

Contact

- Content: editors at theoildrum dot com

- Tech support: support at theoildrum dot com

License

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.

Great article thanks. I think economic growth also follows logistic curve, meaning that, the peak happens around 10000-15000 $/capita and then slows down. So will the coal peaking affect economic growth or economic growth will reduce the need for coal(for the sake of more clean or nuclear resources) is a big question. So how will be the interaction between economic growth and coal production curves be?

I have been sceptical about previous Hubbert analyses of China's coal reserves. I still think there are too many unknowns to give even a round number estimate of the geological resource. However, this analysis is at least consistent with the evidence available.

My immediate reaction is to say thank God for peak oil and other limits to growth. If any society on the planet today could continue to expand coal production to the geological limits it is China. It has become a totalitarian state totally enslaved to the exponential economic growth model. If China did manage to dig coal to the geological limits it would guarantee climate change at a level which would certainly lead to massive human die-off as the carrying capacity of the planet would be drastically reduced, and also a massive species extinction event that will drastically impoverish the natural environment for the remainder of the lifetime of the human species.

However, I think a combination of peak oil, global economic collapse, and the rapid desertification of central China due to the early phases of climate change will lead to collapse of Chinese coal production before 2020. It may also lead to the overthrow of the Chinese state, but I have no way of knowing.

We are in the early stages of a major famine in East Africa. When the last one occurred , 25 years ago, the population density in the area was half of what it is now, and the world had plenty of spare grain and money to feed the hungry, once tghe logistics had been put in place. This time round, will we be so generous? Or will continue to throw Africans off their land to grow biofuels?

We have probably already put too much CO2 in the atmosphere to avoid massive environmental damage.

I like to think about this using Chaos Theory esp the way it is outlined by Taleb in his book The Black Swan, while it's foolish to put dates or even years on a coming energy crisis, the more we avoid it right now the more systemic risks get built up in the system, threatening to bring down everything whenever it collapses. I'd much rather have a series of mini crisis to avoid the larger one just around the corner.

The whole thing is becoming too complicated and dangerous with the Financial markets and Governments trying to manipulate energy markets and overdrawing reserves to keep things stable, overstating reserves to placate everyone doesn't help either, this doesn't resemble a free market anymore which can balance itself using demand and supply, it's a pack of cards kept together by using glue.

Not often mentioned are the emissions of sulfate due to burning coal without emission controls. The SO2 combines with water vapor, producing an aerosol which effects climate by increasing the albedo of the Earth. Burning coal also releases carbon black particles, as does open burning of biomass, which is thought to also impact climate. It's not unreasonable to link the cooling found in the climate record from the 1940's thru the 1970's to the emissions from US and European coal burning during the period. The rapid growth in the burning of coal by China is likely to have cooled the Earth this past decade, off setting the warming due to CO2.

Emissions by China and India have been shown to produce the Asian Brown Cloud, seen in photos HERE. Sulfate and black carbon emissions do not result in long term climate impacts, since the aerosols tend to rain out of the lower atmosphere rather rapidly. If China, India and the other developing nations begin to reduce their particulate emissions, the full impact of AGW can be expected to become apparent...

E. Swanson

CNN On the brown cloud:

http://www.youtube.com/watch?v=qYYK-2sDN4U

From the video:

> It lowers temperatures beneath: ground temperatures.

--- which reduces water evaporation

--- which makes for less rain

> It raises temperatures above

--- which may explain why mountain glaciers are melting so fast

> It is masking the effects of global warming at ground level.

> It would go away in two weeks if the sources turned off.

--- But the earth's average temperature would go up 1-2 degrees

1998 was the warmest year ever recorded at the time. And not only was it a warm year. It was also the record record; never before had the warmest-year-ever-record been broken that much. If climate did not change it would have been a freak year only, already forgotten. But since, it has kept heating up. Of the last 6 years, 3 have been about that warm or even. When something happens every second year, it is a normal thing. Record heat turned into daily average in just about a decade.

Now, if that is the trend when we have an asian brown cloud, then just guess what we would have without it.

Here, May set new records. June challenged 1998. The rains have broken, this month, but the pattern is not familiar. I don't like it.

NAOM

Keep in mind, when you say "ever recorded", you mean since 1978.

Unless there are new sources of emissions, emissions will be falling by mid century whatever the policy is. there simply isn't going to be that sort of polluting fuel to burn. As FF use falls what then will happen? I can see a surge in warming from this effect. My feeling is that once we pass the middle of this century we will see climate change on steroids as various effects and feedbacks start to kick in. I don't think the official guestimates are pessimistic enough and are not so because it is hard enough to get people to believe what is being said so they are being limited related to peoples' belief levels rather than what is more likely to happen.

NAOM

Here's another report from Reuters on the problem:

Asia pollution blamed for halt in warming: study

The source appears to be Kaufmann et al 2011 in the PNAS, "Reconciling anthropogenic climate change with observed temperature 1998–2008". HERE's a LINK from Anthony Watts blog...

E. Swanson

Watt's blog? Anthony Watts is a college dropout. Let's raise the standard here at TOD by not linking to dropouts' blogs, m'kay? Especially when the dropout is a nonscientist Denier.

By all means let's shoot the messenger, or more accurately poison the well.

Especially as the Pacific Northwest finally ends its latest spring ever, according to the local weather people. Latest was defined as latest day to first reach 60 F, and latest date to first reach 80. Multiple record lows in there too.

Crops are all running late as well, but the winter wheat crop is looking very good so far. But the apricots got hammered again :-(

Yes. Someone has to keep tabs on the nonsense that goes on on his site. I'm grateful that BD has agreed to take the job. Exposure to such stupidity and malice is bad for my mental health, and only serves to lower my already rock bottom opinion of our species.

I highly recommend this video to help flavor your view on coal as an energy_Saviour

Peak Coal: US Coal Supply Limits: Economic and Energy Constraints - Leslie Glustrom

Also in the rightside-window videos "Risks of Collapse: Dr. Joseph Tainter, Nicole Foss, David Korowicz" - here Nicole Foss impresses me big time with her answers to very tricky questions.

This report was produced by an anti-coal activist. Unfortunately, it suffers from wishful thinking - it grasps at straws like environmental challenges, and unexpected transportation and restoration costs.

The report gives about 2 paragraphs to the 150B tons of Illinois coal, noting only that it's high sulfur content makes it undesirable. It neglects to mention that sulfur can be scrubbed, but that the modest cost of doing so makes Illinois coal unable to compete with cheap Powder River coal - for the moment.

Gulp!

So that is less than 20 years for China and rest of World.

About enough time for two more doublings of China GDP; then it is decline 30 years from now?

That brings consequences, not least for China.

Other resource constraints? Oil? Food?

I am not sure how relevant the following is as comparison, except in world terms the scale now is so vastly bigger. By early 20thC USA had become world's largest producer of coal at over 350Mt/y, overtaking Britain which was approaching peak coal. Eventual peak coal in Britain was in 1913 at ~290Mt/y with population at ~42M (population increase was slowing rapidly by then, but was still drifting up, and not at any peak). Assuming China goes to 1.5 billion real peak population about 2030 and 5100Mt/y peak coal, then per capita coal will be about half that of Britain's in 1913. Unfair comparison because Britain was not electrified, was much less energy efficient, and was exporting perhaps as much as 1/3rd of coal production and purchasing about 2/3rd of food calories. There again, though, coal was sufficient for bulk commodity transport.

What happens to gearing of a vast global economy in the next decade or so seems beyond comprehension (to me).

How do you say, "The Greatest Shortcoming of the human race, is the inability to understand the exponential function", in Chinese?!

20 years is long enough for China to make the transition to nuclear energy.

As far as I can tell China is investing in every form of energy now. Yes they will have more nuclear in 20 years and more of every form of energy in 20 years. They are continuing to build a prototype thorium fueled molten salt reactor. They are applying the shotgun approach to energy. That is try everything and see what works.

If China is to transition to nuclear in 20 years, it seems like there are some obstacles.

(1) China today has many power outages, due to rolling blackouts related to inadequate supply of fuel (and perhaps other reasons). This situation isn't acceptable with nuclear plants. Too many power outages, and there are likely to be problems with the spent fuel pools. Spent fuel pools can be made to operate without electricity for a while, but after a while, the water in them evaporates/ boils off.

(2) There can't be a culture where bribery is completely expected (as seems to be the case today) because there are likely to have plants where shortcuts are taken, and the profit split with the government official who gave approval to the shortcut.

(3) Somehow, there needs to be a system of mining and transporting and processing uranium (or just reprocessing and transporting spent fuel) that does not depend on oil. Also roads need to be maintained, in order for transport to take place. Somehow, road maintenance needs to be done with very little/ no oil.

(4) Nuclear, as it is done today, requires large amounts of water for cooling. China has water shortages now. How will there be enough water for huge amounts of nuclear?

1) gravity feed source of water for the spent fuel pools. Volume of water needed is low.

2) this is an issue everywhere in the world. The rule of thumb for construction of the reservoirs that service New York City was 50% for graft and 50% for construction.

3) if need be China can mine with human labor, and transport with oxen over minimal roads

4) the need for water is not related to nuclear. It is EVERY electric generating turbine in the world needs a cold sink and a hot source. That is how heat engines work. The used cooling water can be used to irrigate corps it is just a little warm.

Energy will be harder to "make" in the future but nations will not roll over and die they will use the citizens in any way necessary to keep the nation running. Millions died in the building of the great wall of china if million need to die in mining they will.

" It is EVERY electric generating turbine in the world needs a cold sink and a hot source. "

You can dump heat to atmosphere if you need to. It's called a radiator. There is a cost in efficiency in the summer, not so much in the winter. The Dept of Ecology is down on cooling towers, so new construction is going to fin-fans and chillers in the process industries. Note that this is in a desert where water is a bit scarce and rather hard anyway, which is another consideration.

(1) - Power outages are primarily a grid management problem. Nuclear reactors should have grid priority, with other loads being shed to preserve capacity for nuclear plant campuses to back each other up (as well as on-site backup generators). Spent fuel should be moved to reprocessing plants to avoid buildups of spent fuel adjacent to individual reactors.

(2) - The propensity for bribery is somewhat offset by the occasional execution of managers and politicians for malfeasance (an approach that we might usefully adopt).

(3) - Gas, oil, coal to liquids, biofuels, etc., can supply the amount of liquid transportation fuels needed for uranium and thorium mining.

(4) - Seacoast plants can use seawater cooling. Higher temperature plants using liquid metals or salts as moderators can be more thermally efficient. China has a few major rivers and not much water would be lost to evaporation in a once-through cooling cycle. Losses to evaporation are greater when cooling towers are used.

Note: It also appears that climate change will increase precipitation in China, possibly due to the northern subtropical jet stream spending more time north of the Himalayas.

Given China's population and urge to be american, it will not be a transition to nuclear power, but adding nuclear power on top of what has already been built.

Excatly. China is not replacing anything, only expanding everything.

No, it will not work. This has never worked in history.

Diminishing returns = lower net energy = less complexity = collapse. You cannot replace high quality fuel with low quality fuel and survive.

This civilization cannot function on alternative (or nuclear) energy. Another one may emerge, but that will be completely different.

You cannot replace high quality fuel with low quality fuel and survive.

1) That's not true. Agriculture was much lower E-ROI than hunting and gathering. Coal replaced wood, but was considered greatly inferior to wood (a bit denser, but much, much dirtier and more difficult to work with).

2) nuclear and wind electricity is a very high quality fuel.

Try calculating how much crude oil China will need by then. Then calculate how may nuclear power plants it would take to replace that.

The numbers are numbing, as they say.

Try putting in a nuclear power station each week or so, like China was doing for coal-fired power a little while ago.

Try calculating (and I am not joking) the amount of cereal grain / soy needed if 1.3 billion plus persons eat an extra egg a week just now. Make that 4 more eggs a week, if GDP still has two more doublings to go. See Fred's nice dragon pic above.

PS I have an old calculation somewhere that says in energy terms 1 million barrels of oil a day is equivalent to 80 gigawatt nuclear stations. Not actually a fair comparison or calculation, but for sake of argument, say an extra 5Mb/day (see databrowser for last 15 - 20 years increase in oil consumption). Then that looks like 400 nuclear over 20 years, or one every 2 to 3 weeks.

The US uses 19mb per day. In 20 years it will need to substitute 12mb per day so one nuclear plant every week for the next 20 years. I guess this is one of the reasons Bill Gates is investing in a nuclear reactor company. Between US, China, India, EU, Brazil and others who want to escape poverty three reactors per week for the next 20 years. Lots of profit for someone. Yes if we had to build big pressure vessels like current high pressure water reactors there may not be enough material available in the world for this building mission. But using liquid salt or liquid metal at room pressure no pressure vessel is needed so they input materials are far far less. On the other hand I do not think there is enough uranium. But uranium may be like oil cheap uranium is in short supply but expensive uranium is likely much more abundant. I prefer thorium as a fuel, yes it is untested, the Chinese are building the test reactor currently. In five years we may have enough proof to build thorium fueled reactors going forward.

"may"

The US uses about 9M bpd to fuel it's 230M ICE light vehicles.

The same number of EVs would only need about 60 1.3GW nuclear power stations.

I do not expect the Chinese to follow a logistic curve for 10 years and then just sit back and enjoy their economic decline. Nor do i think that all of the remaining coal reserves are as easily accessible and extractable as the producing ones. China is already considering a cap on domestic production. A scenario of a more sustainable 4 billion tons production would be more likely (which would put their peak around 2015).

Also, just adding up coal tons does not take into account their energy content. One ton is not equal with another and it only seems fair to assume that most of the remaining reserves are of lower energy content.

There needs to be a good spread on return for investing in China vs. United States (or other home country). I mean, there is always a little risk premium for investing so far away. If China is hitting an inflection point on economic growth, it could change investors behavior long before 2027.

Oh, and what are the available net exports of coal from other countries? I know they import from Australia. Is that source peaking out yet?

Fresh from the energy databrowser: Australia exports approx. [edit] : 160 million tonnes oil equiv. per year in COAL. Increasing 4% per year.

Further China is exporting importing minucscule amounts compared to production and consumption internally.

Australia exports ~250,000,000 tonnes of coal a year. Probably a bit higher than your number suggests.

http://www.australiancoal.com.au/the-australian-coal-industry_coal-expor...

Ahh, you changed that. Most Aust exports go to Japan, followed by Sth Korea, China, India, Taiwan and Europe, the last four being around the same quantity.

Yeah luckily I was fast on the EDIT button. These small pesky errors of a few magnitudes... (corrected now).

China just does without what they can't afford.

Good thing they don't rely on industry.

China is exporting importing minucscule amounts compared to production and consumption internally.

China regulates the price of domestically-produced coal but they can't tell world markets what to charge; the coal imports into China are therefore prohibitively expensive.

So China buys very little imported coal and just does without power.

Although there is some very good work here, I find the projections 'Isolationist'. It does not take into consideration changes that could effect peak coal.

Clearly if we are at peak oil now and costs of mining greatly increase, then much of the resource will become uneconomic, with peak being reached much earlier.

This is a problem that we face in many areas, that despite clear evidence of the effect of higher energy costs as demonstrated in 2008, that no long term understanding exists of the constraints placed by energy reductions/price. BAU in the continued mining of Coal anywhere will not proceed in the manner envisioned, unless other parts of an economy are reduced to a greater extent.

It wouldn't take a very great proportion of the coal extracted by a mine to supply a CTL plant to provide all the liquid fuels necessary at a reasonable cost to enable the continued extraction of coal.

In many modern mines the bulk of the energy used for extraction on site is electricity. This can quiet easily be provided by coal.

Even the trains shipping the coal to the power station can be electrified.

My view is similar to yours. A limitation in oil supply causes the whole economy to contract, because everything is so networked. The result is that as oil supply contracts, so does the demand for coal and natural gas. It is basically a "Liebig's Law of the Minimum" issue.

Perhaps, if there were an easy/ cheap way of transitioning oil demand to electricity, the situation would be different. But there isn't, so oil shortages tend to lead to high prices which in turn lead to recession, debt defaults, and cutbacks in credit availability. All of these tend to lead to less demand for all kinds of products, including electricity.

You are beginning to win me over. Massive restructuring of big parts of society takes a long long time.

Once an economy develops a significant buildout of infrastructure (highrise towers, steel reinforced concrete freeway bridges, etc.) and significant penetration of autos and appliances, the scrap steel market begins to replace new steel demand and demand for coal drops.

http://www.worldcoal.org/resources/coal-statistics/coal-steel-statistics/

It seems reasonable to expect that China's rapid increases in uses of coal should level off and probably drop dramatically quite shortly, as their economy matures.

About 0.6 tonnes of coke are required to produce 1 tonne of steel. ... . China used 542 mm tonnes steel in 2007

That suggests about 330M tons of coal were used for steel production, or only about 10% of overall coal consumption, right?

I think it is possible to produce iron (the bulkiest component of steel), without using carbon to reduce the state (combine with the Oxygen that was in the iron oxide ore), i.e. if we had cheap renewable energy, and no coal (actually metallurgic coal, which is scarce high quality stuff), we could still produce iron.

You need carbon to reduce the oxygen. Iron in its natural state comes in the form of rust. Add carbon, turn on the het, and the oxygen pair upwith the carbon and the iron turns intoits pure form. Without coal you can always use char coal. But you need some formof carbon. I am a welder, if you know a process I have not heared about that goes around this, please enlighten me.

You don't need carbon to reduce iron oxide. Hydrogen will do just fine. The hydrogen can be electrolyzed from seawater, if natural gas isn't available.

Then there's recycled scrap. Most of the steel used in the USA is reclaimed from scrap (and when industries mature, essentially all of their steel can be recycled) ; all it takes is an electric furnace to re-melt it, and the electricity can come from anything.

"You don't need carbon to reduce iron oxide. Hydrogen will do just fine. "

But you still need limited amounts of carbon to get the correct carbon content. 1045 steel is 0.45% carbon. Cast iron is 1 to 2 % carbon. And so on.

On the other hand the L grades of stainless steel have as little carbon as they can get. By definition they contain no more than 0.03% carbon. The H grades, which are stronger at high temperatures, use as much as 0.1% carbon.

That is corect. We use the term "carbon steel" about certain qualities of steel. We also have a term "carbon equivalents". We use that to calculate how much the steel will be affected when we weldin it. But that is for desk welders (welding engineers). At the plant, I just make sure I have consumables that matches the steel, and weld on.

Isn't China importing enormous amounts of coal from Australia? Even if they ran out of their own coal, would they not merely continue to import coal?

No China receives only 1% of its yearly consumption from Australia. China produces still mainly its own coal.

It is an order of magnitude problem on importing coal. It would be hard to find enough available for export, and enough ships.

Also, I think there is a cost issue involved. China is already having a problem with the rising cost of coal, because if they were to raise consumer electricity prices, many of the citizens are already struggling with high loan payments on their condos, and would default on their loans. Imported coal is likely to be more expensive than domestic coal, because of the transport cost involved, and perhaps higher labor costs. With all of the coal China uses, it would seem like high coal prices could lead to some of the same recessionary issues we see here with high oil prices.

I agree hauling coal half way around the planet has to add cost. I would like to know how much it costs to transport a ton of coal from the US to China.

I agree raising energy costs will slow China down. We live in a global village like it or not so the pain of high cost energy will be shared globally. That may include shipping "cheap" coal from the US to China. Or all energy sources are fungible with enough effort so there is no such thing as cheap coal.

I do not understand who would be hurt if all Chinese mortgages were forgiven (or reset at 50 cents on the dollar). Who are the owners of Chinese mortgages?

Once oil gets too expensive to power bulk carriers like coal ships, you can always go back to coal powered shps. Then you will discover how much of your cargo you would need to burn just shipping it to China...

But, does it? The power required to push a ship scales as the third power of the speed. That means to energy needed per mile scales as the speed squared. Halve sailing speed, and fuel use is cut by three quarters! Slow sailing (plus other innovations, like adding wind power, via kites or sails can firther improve waterborne energy efficiency. Obviously at say half speed, you need twice as many ships, or half the volume of goods shipped. Clearly the cost of shipping will rise, but because of the speed/energy tradeoff, the increase should be relatively mild.

Also by increasing volume, you lower the cost/tonnage ratio. So the future holds giant floating transport islands moving about at glacier speed.

Not that far off that already

None of these solutions (CTL, giant ships, reduced speed, etc, etc. ) will work.

When net energy declines collapse is inevitable. In fact, it has already started.

Whatever the cargo, the shipper, i.e. the customer of the shipping line, has money tied up in the cargo, and the longer the duration of the trip, the more he pays in interest on that money. This slow-motion idea cannot be part of a business-as-usual future (in which 'time is money' ).

It could in a conveyor belt style shpping line. Say you move timber or ore from source to plant. If you have all the ships moving about constantly, it willmatter very little, other than salaries for the workers. But those cases are rare. Mostly you just ship one set of goods on one boat, and then, your comment is correct. Wich is most cases.

But on the other hand, we may see a future economy with 0% rent,intrest, inflation and economic growth, IE steady state economy. In wich case it will also not matter. But I doubt that scenario.

That is what is so impressive about SailDog's picture:

It's like a trail of ants!

Furtherdown the page:

SailDog on July 4, 2011

http://www.theoildrum.com/node/8064#comment-817598

If the conveyor runs faster, it can be sized narrower at less investment cost for the same transport capacity. That implies less debt service for the shipper who presumably would also be the 'owner' for such a special purpose facility.

But the discussion was about ocean shipping. I suppose one could put a conveyor type structure on a pontoon-bridge type structure that spans the Pacific from somewhere on the Pacific northwest coast to somewhere on China's eastern seaboard. I can't imagine prudent investors buying the bond issue for such a venture. ;-)

Even slow sailing is maybe a month. At 12% interest, financing adds 1% to the product cost. Expensive fuel&shipping doesn't end shipping, although some marginal products will probably drop out. Maybe its not true BAU, but to a Martian who had just arrived it would meet his expectations of the term.

Slow-motion financing worked fine in the clipper ship days. At the current 0.25% interest rates, I should think that the interest cost for a sailing ships longer journey would be pretty minor. And with fore & aft rigs and automated sail handling the crew should be much smaller than it was in the old days.

Your first point is doubtful: the largest fore-and-aft rigged ship ever built, the Thomas W. Lawson was barely controllable ("handled like a beached whale") and was lost with only two survivors from a crew of 18, just five years after launching. On the other hand, Alan Villiers described in one of his books a similar sized square-rigged barque (the Parma I think, launched the same year as the Thomas W Lawson) sailing to windward out of the Bay of Biscay in about 1932 with a crew of 18. He remarked how the outstanding performance of this vessel with a small crew was due to the use of the Jarvis brace winch, which partially automated sail handling over a century ago. The Parma holds the speed record for the Australia to England wheat trade under sail, 83 days from Port Victoria to Falmouth in 1933.

Fore-and-aft rig does not work well on large ocean-going ships largely because the booms become too large and are not controlled by running rigging as effectively as the yards on a square-rigger.

I think sailing ships will return, and they'll be square-rigged for crossing oceans. Fore-and-aft works well for smaller coastal vessels and we'll see them too.

Well, if you are going to do a modern square rigger, you might as well make it really modern, like this;

The Maltese Falcon , launched 2006. 88m long, does 20knots (23mph) under sail.

The sail system is the Dyna Rig, a very modern take on a square rig. All the sails are mechanically furled and unfurled - the whole rig can be controlled/operated by one person, without anyone having to go up onto the masts.

But, for cargo ships, the better way to go are the Skysails, which don;t need any masts at all, and "fly" up to 300m high, where there is lots of wind.

Paul,

I'm familiar with both the Maltese Falcon and Skysails.

The problem with Dyna Rig is its dependency on high technology which cannot be repaired with simple hand tools. Furthermore, it appears to be limited in the sail area it can deploy -- not a serious problem for a light displacement hull like your example, but a real problem for heavy vessels carrying a significant amount of cargo.

The barque Afghanistan, launched in 1888, has a rig typical of a large cargo vessel 120 years ago with no auxiliary power. It probably sailed close to as fast as the Maltese Falcon in a good breeze, but much faster in light winds because its rig catches more of the wind passing above the hull. This picture does not show the full sail area a vessel with this rig could set.

The problem with Skysails is that they have no windward ability at all. Both the square-riggers are shown sailing with the wind ahead of the beam.

Yes, skysails would only work as a supplement.

Fortunately, we won't really have to back to pure sailing ships.

Large batteries could provide most of the remaining power needed, to be recharged at frequent port stops, as used to be done with coal (just as they picked up coal 60 years ago - that's why the US wanted the Philippines military bases, and why they're not needed in the oil era). Let's analyze li-ion batteries: assume 20MW engine power at a cruising speed a speed of 15 knots (17.25 mph) or 20MW auxiliary assistance to a higher speed, and a needed port-to-port range of 2,000 miles (a range that was considered extremely good in the era of coal ships - the average length of a full trip is about 4,500 miles (see chart 8 ). That's 116 hours of travel, and 2,310 MW hours needed. At 200whrs per kg, that's 11,594 metric tons. The Emma Maersk has a capacity of 172,990 metric tons, so we'd need about 7% of it's capacity (by weight) to add batteries.

So, li-ion would do. Now it would be more expensive than many alternatives that would be practical in a "captive" fleet like this - many high energy density, much less expensive batteries exist whose charging is very inconvenient, but could be swapped out in an application like this. These include Zinc-air, and others. It should be noted that research continues on batteries with much higher density still, as we see here and here, but existing batteries would suffice.

Refrigerated storage/transport could go via electric rail, which can certainly be low-CO2; refrigeration can always be made more efficient with better insulation; and there are "reefer" units that are "charged" on land, using grid power, that don't need any inputs from the ship during transit.

Hydrogen fuel cells: they can't compete with batteries in cars, but they'd work just fine in ships, where creation of a fleet fueling network would be far simpler, and where miniaturization of the fuel cell isn't essential. If batteries, the preferred solution for light surface vehicles, can't provide a complete solution, a hydrogen "range extender" would work quite well.

Hydrogen has more energy per unit mass than other fuels (61,100 BTUs per pound versus 20,900 BTUs per pound of gasoline), and fuel cells are perhaps 50% more efficient, so hydrogen would weigh less than 1/3 as much as diesel fuel.

Electricity storage using hydrogen will likely cost at least 2x as much as using batteries (due to inherent conversion inefficiency), but will still be much cheaper then current fuel prices. Fuel cells aren't especially heavy relative to this use: fuel cell mass 325 W/kg (FreedomCar goal) gives 32.5 MW = 100 metric tons, probably less than a 80MW diesel engine.

Hydrogen would have lower upfront costs versus batteries, and a lower weight penalty, but would have substantially higher operating costs. The optimal mix of batteries and hydrogen would depend on the relative future costs, but we can be confident that they would be affordable. Here's a forecast of affordability in the most difficult application, automotive.

Ird,

I agree that the Dyna Rig is a rather complicated system - but that is to be expected for a first attempt at a fully automated mechanical system - I am sure it could be improved upon.

The problem the square riggers had, is that you needed men up in the rigging to handle the sails - the average crew loss on a trip from US west coast to Europe, around the Horn, was two men. That would be simply unacceptable today, so any rigging system would have to be such that it can be completely handled from the deck, or better yet, from the bridge. Now, you don't have to go to the Dyna Rig to achieve on deck handling, but the fact that the DR achieved one man, from the bridge operation, is a big plus in both increasing safety and reducing crew size.

The appeal of the Skysails is that they can easily be added to any existing ship. The lack of upwind ability may result in these vessels favouring the tradewinds routes.

I am not really sold on the upwind ability being that big of a deal - but if it is, then surely the fore and aft rig is the better way to go. Like the square rig, we can do much better than a century ago.

Slowing the ships means reducing productivity. If the speed of a container ship is reduced by half, it means:

1. half the amount of cargo transported.

2. twice the amount of supplies for the crew.

3. profit reduced by 50%.

4. ship wears out after transporting half the amount of cargo.

5. there will be a glut of ships. If there is a shortage, then the price for transporting the goods will be high and the ship owner could afford expensive fuel to travel fast.

With profits plunging and a glut of container ships, ship owners will not purchase more ships. They will scrap their old ones giving a short-term boost to their quarterly business reports. Ship yards will go out of business. If ship owners could have increased profit by slowing down and purchasing more ships, then they would have used that strategy on the rising edge of peak oil.

When the container ships slow down, globalization is dying.

If the speed of a container ship is reduced by half

50% speed reduction isn't needed: 20% will reduce fuel consumption by half.

half the amount of cargo transported.

Don't forget downtime in port - it's not a straight ratio.

If ship owners could have increased profit by slowing down and purchasing more ships, then they would have used that strategy on the rising edge of peak oil.

Actually, they did in 2008 It worked pretty well.

Orders for new ships plummeted in 2008 coincident with the financial crisis and remain depressed.

China Applying the Pressure on South Korea and Japan in Shipbuilding, Metal Miner, October 18, 2010

Status and preview of shipbuilding orders in million TEU

That's what you would expect in a recession. Your first chart shows a clear boom and bust pattern.

From your second source:

"The annual growth rate of container traffic in the past 20 years averaged approx. 10 %. In the reporting year 2008, due to the flagging economy in the second half of the year, the rise was only some 5 %. For the current year, for the first time in the history of container traffic Clarkson is reckoning with a decrease of approx. 3 %. "

That looks like a classic business cycle.

Here's an interesting map. Note the relative size of that China-Russia deposit v.s. Australia, Germany, USA.

http://www.mapsofworld.com/business/industries/coal-energy/world-coal-de...

The thing that is strange is that with the apparent size of the coal deposits in Russia, they don't seem to use/produce very much. They are much more reliant on natural gas and oil. See Energy Export Databrowser data for Russian Federation.

I wonder if the reason wasn't that Russia had oil and gas available, and they were easier to use. Also, the coal was mostly way off in Siberia. Building railroads to get there, and getting people to move there, might have been a problem. Of course, it is hard to see that Mongolia would be a big improvement as a place to live. But it is close to China, and China needs the coal.

The "way off in Siberia" is the true culprit. To use those coal deposits takes loads and loads of infrastructure, and they don't have it pre installed. (Thank God for that). So they wont develop those fields until they find a buyer who is willing to pay for the coal, the tranport, and all those massive investments. Just now, the queue to the application office is very very short.

Don't forget, that map is a Mercator projection, which exaggerates areas in the far North. E.g. Greenland looks bigger than South America, and yet it's really about 2/3 the area of Argentina alone.

Where is Coal Found?, World Coal Association. The graph shows China's proven coal reserves under 50 billion tonnes (110 billion tons) which Minqi Li suggests greatly underestimates the URR.

A map showing the area where coal is located does not reveal the volume of coal nor the energy content of the coal which varies widely from lignite to anthracite. Mining and transporting coal from frigid, remote Siberia will not be easy. However, China does want a piece of Russian coal, China to Invest in Russian Coal Producing Market (Russia Briefing, Oct. 26, 2010):

The map gives a utterly false impression. The projection used is not iso area. On this map, Australia appears to be less than half the size of Greenland, but in fact Australia is 3.55x the area of Greenland.

But there might be coal in Greenland which might be available for export after the collapse of the world as we know it ;-)

Actually, there is coal in Greenland. It was mined at Qullissat on the northeast coast of Disko Island from 1924 to 1972. When I visited the area in 1972 I was told the mine was closing because a commission had found that it would be cheaper to pay the miners their full wages to do nothing and import the coal from Britain. The same coal seam (its outcrop is visible from the fjord) was mined by the crew of the Fox in 1858 to refuel after their winter trapped in sea ice, before sailing again for Lancaster Sound in the search for the Franklin Expedition.

I doubt if Greenland will ever be a coal exporter, but these deposits could again help some of the local population survive after imports cease.

Unless they have passed a penalty by death law on the consumption of fossil fuels by then? Would make a lot of sense to pass such a law when it is to late.

This is definitely not correct. The German deposits start at the Cologne area (now depleted) and reach up to the North Sea and furher (100 km wide, ~300 till ~500 m thick). At the high of Hamburg they are ~5000 m deep, but they are existing and contain enormous amounts of coal. I don't see this well known deposit in the map! This does not mean the deposit is economic exploitable, but it exists. Also it maybe the case that the reason that there are nearly no depoits in South- America and Africa may be because of the lack of survey targeting coal there...

China is importing coal from Australia and the US. There are huge US reserves that can keep China going for another 30 years after their own 30 years. So a total of 60 good years ahead for China.

No, the US produces a billion tons per year, and China needs 3 billions per year. You are thinking that the perhaps 500 million tons that the USA MIGHT in a crisis sell and export to China is gonna make a difference?

In 30 years from now how much do you think we are gonna be able to dig up still worldwide? Just askin.

Alaska probably has between 2 and 5 Trillion tons of coal. Canada also has huge amounts of coal.

Please provide a link to back this up. The total USA URR for coal is just barely a fraction of this.

Alaska has 2-5 trillion tons of coal, and very likely has at least 200 billion which are "technically recoverable" (a 200 year supply for the US). And, yet, it's not being used at all right now, because it's significantly more expensive than lower-48 coal. David Rutledge agrees: http://www.theoildrum.com/node/6700/674664

"A few years ago, estimates of Alaska's coal resources placed them at approximately 130 billion tons. Now, largely because of better knowledge about the coal beneath the North Slope and the offshore area beyond, the estimates range from 1,860 billion to 5,000 billion tons.

This, of course, is a huge energy resource if it could all be recovered for use. Full recovery is unlikely because much of the coal is deeply buried, of not the best quality or is at locations where transportation is lacking.

In estimating what portion of an identified coal resource is recoverable, experts considering reserves elsewhere in the United States pick figures ranging from one percent to over twenty percent. And that percentage generally is applied only to known resources, not those which are hypothesized to exist on the basis of surface outcrops or sparse drilling information. Nor does the percentage apply to resources speculated to exist, such as off Alaska's northern coast, on the basis of even less information. The 1,850 billion to 5,000 billion ton estimate for Alaska includes these hypothesized or speculated resources.

But suppose Alaska really does have a coal resource amounting to the lower figure, 1,850 billion tons, and suppose that 10% of it is recoverable. That means Alaska could recover 185 billion tons."

http://www.gi.alaska.edu/ScienceForum/ASF4/492.html

-----------------------------

http://www.groundtruthtrekking.org/Graphics/Small/HowMuchCoal-01.png

There's more coal in the arctic than we previously believed.

Prior to the last couple decades, the last time Alaska's arctic was assessed for coal by the USGS was in a study in 1967. At this time, the majority of the assessment was made by searching for coal outcrops on the surface. In the intervening decades a large number of oil shafts, boreholes, exploration shafts, etc. have been sunk throughout the North Slope and have basically all struck coal. The 2005 USGS assessment of the presence of up to 3.5 trillion tons of coal in the North Slope is based on a mapping of these sites, many of which are widely seperated. This coal is definitely present, but the sparse mapping data causes it all to be classified as hypothetical resource. With further exploration, some of this coal could be reclassified as identified resource, and then potentially added to the reserve base."

Both the above are from this article which does a decent job of laying out the Alaskan coal picture. http://www.groundtruthtrekking.org/WildResource/Issues/HowMuchCoal.html

Here's my link: EIA estimates there are 261 billion short tons of U.S. recoverable coal reserves, about 54% of the Demonstrated Reserve Base. http://www.eia.gov/energyexplained/index.cfm?page=coal_reserves

Historical trends in American coal production and a possible future outlook page 11

http://www.tsl.uu.se/uhdsg/Publications/USA_Coal.pdf

Again, the report gives about 2 paragraphs to the 150B tons of Illinois coal, noting only that it's high sulfur content makes it undesirable. It neglects to mention that sulfur can be scrubbed, but that the modest cost of doing so makes Illinois coal unable to compete with cheap Powder River coal - for the moment.

This kind of basic mistake gets repeated endlessly. You can't use Hubbert analysis for coal.

With peak oil either here or soon coming to a threater near you, US coal exports will rapidly fall to zero - China has zero chance to import coal from any outside country when PO strikes.

The US currently produces only 1 gigaton per year of coal it has 238 gigatons in reserves. It owes China somewhere from 1 trillion dollars to 3.5 trillion dollars (never clear it varies article by article). The annual trade deficit is about 1 gigton of coal per year. Will we refuse to sell coal to China even though we are running a trade deficit with them? US coal production can be increased. We can make the Chinese pay for the development costs if they want the coal. I am sure they would be happy to provide all the mine workers and the train workers and the port workers.

http://www.nytimes.com/2010/04/08/business/global/08rail.html

I hear they're also offering to provide the financing.

Much of the US cellphone infrastructure is owned by Saudi Arabia so why not have trains owned by China.

No - 238 Gtons of various quality and unknown cost of extraction.

USA might increase production a little. How much of the 1 billion tons per year will USA ever export? Not much is MY guess.

Even if China owes the USA. This has been the case the last 10 years - the situation aint gonna change before a major change of BAU. And when BAU is dead all bets are off. or is this what you mean?

The ramping up of production even with Chinese help will take decades, in the scenario you propose.

My argument is - there is noone to help China get 3 billion tons of coal per year except war, end of BAU or China itself.

China has 20 years to ramp up US coal production. That is longer than they took to ramp up their domestic production.

Looking at that map I posted, there's a LOT more coal in Russia's Siberia than in the US. A few rail lines or even HVDC transmission should do it.

Mongolia also has heaps of coal. Seams even break out of the surface and most is easily strip mined. Most of it goes to China - in effect Mongolias reserves, which are huge in themselves, should be added to China's.

I was in the Gobi desert last week and took this pic of trucks moving coal to China. And endless stream of trucks 24/7, each holding around 80 tons. And that was only for one border crossing (Gants Mod).

http://www.flickr.com/photos/saildog0907/5901013408/

According to EIA, Mongolia produced 13 million short tons of coal in 2010 and the reserves at the end of 2008 were about 2.8 billion short tons. These are small numbers compared to China. It would be interesting to see how Mongolia's coal production and reserves change in the future.

OK in this particular framing of the question you win ;)

Sure China has enough coal, for the current population and its living standards for another 20 years.

Lets leave the interconnected questions of increasing demands of standards and perceived freedom aside, as well

as food quality and pollution problems during the next 20 years in Asia, shall we...

Sincerely you made me reflect on these issues, thanks,

Segeltamp

Thank everyone for your excellent comments.

For those who are interested in the interactions between peak coal, peak oil, and peak GDP etc, please note that this is only a small part of a much bigger informal report on global peak energy and the limits to growth. The full report can found at: www.econ.utah.edu/~mli

Below is an abstract of the report:

World oil production will peak before 2020; world coal production will peak before 2030; and world natural gas production will peak around 2040. World total energy supply will peak in the mid-2030s. As rising energy efficiency fails to offset declining energy supply, gross world output peaks around 2050 and declines over the second half of the 21st century. While the carbon dioxide emissions from fossil fuels consumption are projected to peak before 2030, the cumulative carbon dioxide emissions over the century imply a long-term global warming of 3.5-7 degrees Celsius, with potentially catastrophic consequences for the humanity.

In other words, given my current assessments, we are likely to both reach the limits to growth-peak world GDP by the mid-century and potentially suffer from the worst climate consequences for centuries to come under the projected natural depletion of fossil fuels.

Another finding of this report is that coal will overtake oil to become the world's largest source of energy after 2020 and will remain to be the world's largest energy resource until about 2040. This is very different from the projections made by mainstream energy institutions (such as IEA, EIA, BP), which typically predict oil or natural gas will be the largest energy source in the coming decades.

About the possible cooling effect of China's coal consumption. I'm not an expert on it. But my understanding is that while some aerosols have cooling effects, aerosols such as black carbon have warming effect. Also, in the long run, as fossil fuels become depleted, aerosols in the atmosphere will decline rapidly, but long-lived greenhouse gases (CO2, CH4, N2O, etc) will stay, with the full warming effect exposed.

Liminqi,

The photo from Saildog above is one of the exact reasons why I think that peak coal will come much sooner. When oil becomes to expensive to run the trucks, CTL plants will begin to happen, yet the funds to build these will dry up, plus the liquids created will be too valuable to just move coal.

Building railroads to move the coal will become prohibitively expensive with only rare oil to do it. The metals needed will also become in short supply as the available energy to move and form them contracts.

A simple underestimation of the effect of peak oil and depletion will change future scenario predictions greatly.

In my report, it suggests world peak oil in 2016. So we'll see how it plays out when peak oil does happen and how it affects peak coal. But the above projections would tell us what the existing evidence suggests.

Yet there is plenty of evidence that it has already peaked, including from the IEA. Fatih Birol claims it has already happened in 2006.

http://www.abc.net.au/catalyst/stories/3201781.htm

As global net exports have clearly already peaked, I'm sure it would change your timeline when taken into consideration.

Can you post where you get 2016 for peak oil please? (OK I went through the entire main article) I hope you are aware that both the EIA and IEA have been downgrading future oil production projections over the last 10 years.

Analyses of C&C are useful for the purpose of evaluating PO forecasts, but ultimately liquid fuels are what matter, and liquid fuel hasn't peaked even when you take E-ROI and net BTUs into account.

Thank you for this valuable report. It highlights the challenges we face. In my opinion it makes the critical nature of energy policy clear.

A few comments:

Using BP's renewable numbers (electricity + biofuel liquids) neglects certain potentially non-trivial renewables used to provide industrial process heat and residential heat. This is chiefly wood waste, firewood, and solar thermal.

Natural gas power plants differ markedly in type (Brayton cycle, Rankine cycle, and combined cycle), and different types exhibit markedly different capital costs, fuel efficiency, and capacity factors.

Capacity factor and cost trends for wind and solar are not static at the average U.S. levels of 2009.

Biofuel potential differs markedly by feedstock and process.

The assumed GDP/BTU trend is critical. The technical possibilities are markedly higher, in my engineering opinion.

Whether black Carbon (BC) is net warming or cooling is not well determined. BC over high albedo areas, such as the arctic warms, but it is not clear about most other areas. The tendency of aerosols to provide CCN (cloud condensation nuclei) complicates things greatly. Generally more CCN mean more (and whiter) clouds, which has a cooling effect. The aerosol/cloud effect is referred to as the indirect aerosol effect, and its magnitude is still not well known.

Generally, I would expect that over time, China will burn coal more cleanly (although digging into lower quality reserves makes this more difficult), so I expect peak aerosol will come before peak coal.

Completely enjoyed your paper. Nice to see a broad perspective. Nice to see mention of storage after the first 10% of intermittent solar electric generation.

You point out for 20% renewables by 2050 we need to build 220 GW of renewables per year. We are nowhere near this value.

Great phrase "natural depletion of fossil fuels". So far there is no projection that shows renewables replacing fossil fuels before they are depleted naturally.

That assumes: A:No renewable production other than electricity and liquid biofuels. B)25% capacity factor for future construction of world renewable electricity production.

In the U.S. non-electricity, non-biofuel renewables were roughly 28% in 2008 (process heat from wood and waste without electricity generation, firewood, and solar water heaters, etc.).

China installed roughly 30GW of solar water heaters in 2009.

Global production of new solar panels and wind turbines was together about 50 GW in 2010. Sustainable annual growth for these is conservatively 20% for the next 10-20 years. By 2020 global production of new solar panels/wind turbines will easily be 6.2 times the 2010 production rate, i.e. 300 GW annual new panels/turbines. This is really not that difficult. It requires some energy inputs but the EROEI for both wind turbines and solar panels are good enough (energy payback in 1-3 years) where these have sufficient wind and sun. The trick is to install sufficient energy storage and grid-stabilizing features to handle higher penetrations of non-dispatchable power. These technologies are ready for use, they just need a business model and willing investors.

You have made no mention of population growth or per capita numbers. I see that the discussion is valid without it but I still would feel better with at least a nod to the quality of life of humans (me, mine, you, yours, etc.)

Good luck with that, as far as China is concerned...and the rest of the world is not much better! Humans don't get it but they will. I suspect sooner than later. Yes, we are about to hit a wall with peak resources and we will suffer the impact of global climate change. However local ecosystems are being degraded at ever accelerating rates everywhere around the world.

http://planetark.org/wen/62519

A fisherman rows a boat in the algae-filled Chaohu Lake in Hefei, Anhui province July 3, 2011.

http://planetark.org/images/wefull/62519.jpg

That one picture alone is worth 7 billion words, and every single one of those words is F@CK!

I highly doubt that China, or anywhere in the world for that matter, will be habitable at all, long enough to build all those power plants...

So Long and Thanks For all the Fish from The HitchHiker's Guide to the Galaxy.

http://www.youtube.com/watch?v=ojydNb3Lrrs

The last time my brother was on business in China, the sky was green during the stay.

China is not even remotely survivable.

Merely the last great industrial power.

Its not clear to me what that picture signifies. I can remember being on lake Wissota (famous for being mentioned in the Titanic movie) just after the fall thermocline overturning. It looked almost that bad, but was a natural cycle, and the fish seemed to do just fine. To know whether it is bad, I think requires a chemical analysis. I hear acidified lakes look great, the water is wonderfully clear.

Oh, come on! And CO2 is good for plants...

http://www.china.org.cn/photos/2010-06/24/content_20336407.htm

It also helps if one has at least a basic concept of what eutrophication means and why algal blooms occur in the first place. Algal blooms generally indicate something out of balance in the aquatic ecosystem, often caused by excess nutrients from things such as agricultural waste runoff.

The human nose is a rather sophisticated chemical analysis instrument even if some human brains refuse to accept the results... I hear gilded turds look like pure gold too!

Dr. Li,

I've started reviewing your full report. I'll start giving you some feedback immediately, and add as I go.

In this study, nuclear electricity, hydro electricity, and other renewable electricity are all measured by their electrical energy content (not “thermal equivalents”). They are all converted into oil equivalents based on the following conversion ratio: 1 million tons of oil equivalent = 11.63 terawatt-hours (billion kilowatt-hours).

This is highly unrealistic. You really, really do have to use “thermal equivalents” in order to have your calculations mean anything.

This is the equivalent of assuming about 10.5 kWhs per liter of fuel. An electrical vehicle uses about .2kWh per kilometer. The average vehicle in the US uses about .1 liters per km. That means that an EV uses .2kWh to do the work of .1 liters of fuel, for a conversion of about 2kWh per liter of fuel.

Let me put that another way: replacing the 9M bpd of oil used in the US for personal transportation would only require about 100GW of generation, not the roughly 525GW your conversion would suggest. Your conversion suggests that the US would have to more than double it's generation just to replace 50% of it's fuel consumption, when in fact it would only have to increase it by about 23%!

-----------------------------------------------------

Table 1 is inaccurate. Unfortunately, the EIA is not a good source for information about wind power: In the US capital costs are $2/W including transmission, not 2.4, and the capacity factor for new wind power is 30%-35%, not 25%. Capital costs for new coal are significantly higher than $2.8/W - closer to $5.

The result: new wind power capacity is roughly about 7 cents per kWh, about the same as new coal. Only natural gas is cheaper than wind at the moment. Wind power costs have been falling consistently, and will continue to do so.

Wind power is the logical candidate for the bulk of future low-carbon generation. In particular, using current solar power costs presents a highly unrealistic picture.

------------------------------------------------------

The world currently has a total installed electricity generating capacity of about 5,000 giga-watts with an average capacity utilization rate of about 50 percent.

This appears a bit high. This suggests an average generation of about 2.5TW - as you note on page 17, average generation is about 2.1TW. If total installed electricity generating capacity is really at about 5,000 giga-watts then the average capacity utilization rate is about 42 percent.

------------------------------------------------------

In the long run, renewable energies are limited by the physical availability of land and various nonrenewable mineral resources.

This is not realistic, as applied to wind power. Wind power may need to be spaced over a large area, but it does not consume that area - turbines only occupy about .5% of that land. The US could generate it's entire 440GW from farmland, while farming would continue peacefully between the turbines.

-------------------------------------------------------

Solar and wind are intermittent energy resources. Given the existing electric grids, wind and solar electricity can penetrate up to 20 percent of the installed electricity generating capacity or 10 percent of the actual electricity production without causing serious problems. Beyond these limits, further increase in solar and wind electricity will have to require large-scale storage of electricity (Lightfoot and Green 2002).

This is unrealistic. Large scale storage is an extremely expensive solution to intermittency. Better solutions that are both practical and cost-effective include Demand Side Management; geographical dispersion; overbuilding; and backup by inexpensive, rarely used biomass.

--------------------------------------------------------

The manufacturing of the solar and wind equipment consumes massive amounts of nonrenewable mineral resources (Prieto 2008).

This may apply to solar, if highly conservative assumptions are made. Wind power does not consume "massive" amounts of mineral resources.

--------------------------------------------------------

If half of the total energy demand can be met from electricity and the rest has to be from biofuels

This is entirely arbitrary. If electrical vehicles are used, only a very small percentage of total energy demand would need to come from liquid fuels. Further, the assumption that liquid fuels can only come from biomass is inaccurate - it can be synthesized from seawater, atmospheric carbon and electricity. Granted, that would be fairly expensive, perhaps $2.50 per liter, but if it were a small percentage of energy consumption that wouldn't matter.

--------------------------------------------------------

for the projected increase in renewable energy to be materialized, the world needs to build in average 220 giga-watts of renewable power plants a year from 2010 to 2050.

Again, this is roughly 3-5 times too high, because of the incorrect conversion of electricity to oil-equivalents.

In the 1890s the Times of London predicted that by 1950 every street in the city would be covered 9-feet-deep in horse manure.

This prediction illustrates the folly of extrapolating into the future based solely on technology known today. This was pointed out by MIT chemistry Prof. Dan Nocera in connection with the MIT Energy Initiative.

Yes, I recall that back in 1975, the use of electricity in the US was growing at 7% a year, a trend which, if continued for 25 years to 2000, would have required the building of an additional 4.5 times the existing generation capacity. That translates into something like the building of 1000 nukes by 2000. We ended the century with 104, as I recall.

Edit for better analogy:

Darned the exponentials, lets put the peddle to the metal and fly full speed ahead, that's not a peak up ahead, that's a plateau (and we know where that ends)...

E. Swanson

When this was filmed, we were going to the moon.

2001 opening scene

http://www.youtube.com/watch?v=ML1OZCHixR0

Which part of the movie are we closer to now,

The monkeys or the space ship?

Countdown starts for NASA's last shuttle launch:

http://www.reuters.com/article/2011/07/05/us-space-shuttle-countdown-idU...

Will there be wars over coal, too?

This comment assumes that there is a techno-fix to China's problem. Bruce Sterling has a variation: "The future is already here. It's just unevenly distributed." In London's case the future was the internal combustion engine; in China's it's ... it's ...

The main techno-fix for China's problem appears to be nuclear power. And China is exploiting it: by 2020 it expects nuclear to provide a whole 6% of its electricity, up from 1% currently (Wikipedia). Perhaps by 2027 we can expect 12%. To this we can add another few percent from hydro, wind, and solar. So the Chinese will be able to keep essential services going after the coal runs out.

A bigger future lies in the declining income elasticity of coal use, down from over 1 in 1990-2005 to 0.6 in 2005-2010 (6.6% increase in coal use for 11.1% increase in GDP, according to Prof. Li above). If China can drive its income elasticity of coal use down to 0 (or even negative), it may not have a coal problem.

China is getting deeper into water issues by the year. Do not expect any long term energy boosts from hydro power in that nation. Droughs and hydro power is a sorry marriage.

To the best of my knowledge, The Times never predicted any such thing. It's a myth.

The Richard Heinberg article http://www.theoildrum.com/node/6434 tips 2015 not 2027 as the year for China peak coal. I wonder if this author has dismissed some factors in favour of the early date. I would add that reduced oil supply could impact coal demand. As the West slows down there will be less purchasing power to import goods from China.

There is already some disquiet in Australia about Chinese companies (in reality government agencies) buying up prime farmland to dig for coal. In a couple a days an announcement will be made on the carbon tax to start July 2012. If the rate is set at $20 per tonne of CO2 then in effect thermal black coal becomes $50 a tonne more expensive. That's since a tonne of coal becomes about 2.5 tonnes of CO2 in the smokestack. $50 is a lot on top of a spot price of perhaps $150.

I think Blind Freddy can predict that Australian coal users will ask why they should pay carbon tax on the same coal that is exported tax free to China. That includes both thermal coal used in power generation and coking coal used in steel making. Sunday's announcement will include some kind of cash compensation for trade exposed industries like steel mills and aluminium smelters using coal fired electricity. My suggestion is make everybody pay carbon tax. Since the tax is supposed to be revenue neutral the Chinese govt can ask for a refund of the carbon tax paid on Australian imported coal. The money should go to Chinese green programs however.

I agree there is likely to be quite some argument about domestic coal users paying the tax, when exports don;t, and now even oil users won't. The carbon tax is not taxing the one thing that needs to be taxed most - oil!

Interesting concept about charging China (or any other buyer of Aust coal) the tax and then refunding it. Seems kinda redundant, but going along with, how could you enforce that China uses it for renewable projects? The only recourse if they don't is to stop refunding the tax, in which case they just buy coal elsewhere - a $50 premium gives lots of room for competitors.

I don;t think the Aust gov is willing to do anything that would risk China walking away from Aust coal (and iron ore).

The $50/ton of coal adds about 2c/kWh, which compared to typical residential rates in Australia of 20-24c, is almost noise. Might be good for Tassie though.

Incidentally, if you look at wood as a fuel source, one (dry) ton of wood is equivalent to about 0.75tons of coal, so the carbon tax differential means a ton of wood as fuel saves about $37.50 of carbon tax - wonder if that might be enough make some places burn woodchips for power instead of exporting them for pulp?