The Coal Question, Revisited

Posted by Euan Mearns on December 15, 2010 - 10:20pm

This is a guest post by Professor Dave Rutledge (DaveR), of the California Institute of Technology (Caltech).

In the summer of 2007, Professor Kyle Saunders (Professor Goose) invited me to do a guest post for The Oil Drum. This post was "The Coal Question and Climate Change." In the post, Hubbert linearization was applied to make a regional analysis of world coal production. The estimate for long-term production, including both cumulative production and all future production, amounted to 724Gt. Many people, including Dave Summers (Heading Out) and Euan Mearns, made helpful critical comments on the post, particularly concerning British coal production. Overall, I was encouraged by the response. The Oil Drum is a great place to try out new ideas.

I now have a paper "Estimating Long-Term World Coal Production with Logit and Probit Transforms" that is in press at the International Journal of Coal Geology. People who are interested can download a pdf preprint at my web site. There is also an Excel workbook with the data for the paper at the site. The paper makes several changes from the original post. At that time, I did not have complete production data, and I was relying on cumulative production totals from reports by the BGR, the German resources agency. These turned out to be incomplete. However, over time, I was able to fill in the gaps in the production histories. Steve Mohr at the University of Newcastle in Australia gave wonderful help, and Nadia Lapusta, a Ukranian engineering professor at Caltech, located Russian language histories for the different Soviet republics. I was able to fill out the early American state production numbers from Harold Eavenson's 1942 book, The First Century and a Quarter of the American Coal Industry.

In addition, I became dissatisfied with Hubbert linearization. Hubbert linearization involves annual production directly, and this gives larger fluctuations in the estimates than an approach based on cumulative production. This is a particular problem for coal, which shows large production drops in strike years. Hubbert linearization assigns weak weight to the later years in the production cycle, and this means one often has to make a judgment call about throwing out a large number of the earlier points, because their influence is too strong. Also, Hubbert linearization is based on the logistic function, and a cumulative normal is a better fit for some regions. In the new paper, the logit transform is used to linearize the cumulative production history for the logistic fits and the probit transform for the cumulative normal fits. One way to understand how these linearizing transforms work is to think in terms of an exhaustion function, defined in the paper as the fraction of the long-term production that has already been produced. The exhaustion starts off at zero, and then monotonically increases, eventually reaching unity when the last mine shuts down. It has the same properties as a cumulative density function in statistics. From this perspective the probit transform is the inverse of the standard cumulative normal function, and the logit transform is the corresponding inverse function for the logistic distribution. The statistical quantity r2 (correlation coefficient squared) is maximized to find the long-term production estimate. This is a simple one-parameter fit, and it takes about one second in Excel. There are two regions where production is developing that do not give a maximum value for r2, South Asia and Latin America. For these regions, I used the reserves as an estimate for future production, even though the experience with the mature regions indicates that these numbers are likely to be too high.

Finally, in my original post, I had considered Montana as a separate region. Montana has enormous reserves, 68Gt at year-end 2008, but only modest annual production, 36Mt in 2009. I had used Montana's reserves as an estimate for its future production. After studying the USGS assessments for the area I came around to the view that this was not appropriate. The main production in Montana is from the Powder River Basin (PRB), and it appears that Wyoming drew much the better hand in the PRB. I believe that the differences in PRB production for Wyoming and Montana represent geology at least as much as any other factors. For more discussion, see "Potential for Coal-to-Liquids Conversion in the U.S.-Resource Base," by Gregory Croft and Tad Patzek, Natural Resources Research, volume 18, pp. 173-180. Montana does follow the same two-cycle pattern that other Western US production does, and I believe that Montana production is appropriately captured in a curve fit for the Western states.

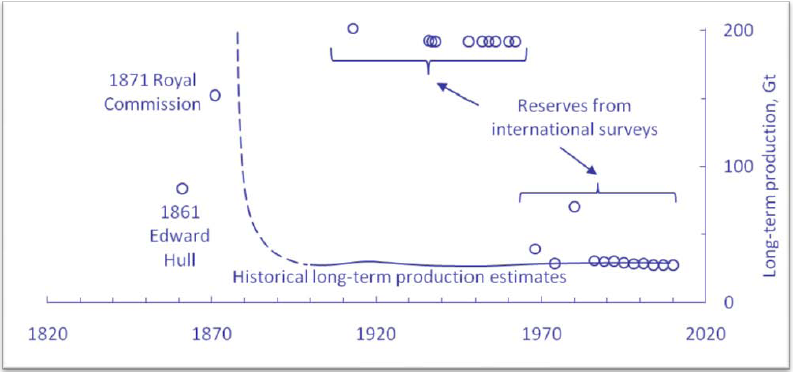

Recently, Dave Summers addressed the topic of future British coal production in his Oil Drum post, "Future Coal Supplies - More, Not Less!" The British production experience parallels that of the three other mature regions in my paper, Pennsylvania anthracite, France and Belgium, and Japan and South Korea. Production in each of these regions is less than 10% of the peak production. Also, in each region, the early reserves were much larger than the production that followed. On average, the early reserves plus contemporary cumulative production have been four times the current cumulative production. On the other hand, in each case, the curve fits gave appropriate estimates for the long-term production, by 1900 for the UK, Pennsylvania anthracite, and France and Belgium, and by 1950 for Japan and South Korea. This is shown in the figure for British production.

At the time of my original post, there were seven collieries with producing longwall faces in the UK. Since then, two have closed, Tower, and Welbeck. Five remain: Daw Mill, Hatfield, Kellingley, Maltby, and Thoresby. In addition, maintenance is being done on Harworth Colliery so that it could be brought back into production at some point. For comparison, William Ashworth's History of the British Coal Industry states that there were 803 producing faces in 1973. For completeness, it should be noted that there are also small underground mines that together contribute 1% of British underground production. In addition, there are surface mines. Surface mining in the UK started during the Second World War and peaked in 1991. The decline in surface production has been slower than for underground production, to the extent that by 2009 surface production was actually a third larger than underground production [3]. The largest coal company in Britain is UK Coal, which operates Daw Mill, Kellingley, Thoresby and Harworth. UK Coal's on-line financial reports indicate that its underground mining group has lost money ten years in a row, and that the company has debts of £250,000,000, twice its market capitalization. These mines are the last survivors out of thousands. As they run out of seams to work, they will close, one by one.

The new estimate for total world production, past and future, is 680Gt. This is 6% less than the earlier one in my original Oil Drum Post, primarily because the reserves for Montana no longer figure in the total. To get a feeling for the uncertainty, I check the stability of the estimate by making historical fits that use only the data available in an earlier year. The estimate for long-term production has varied in a range from 653-749Gt (14%) since 1995. I can make a comparison with Steve Mohr and Geoffrey Evans' [2] and Tad Patzek and Greg Croft's [3] recent estimates. Mohr and Evans use Hubbert linearization at the national level to get 702Gt, and Patzek and Croft use a multi-cycle analysis to get 630Gt. In addition, Patzek and Croft have possible contingencies of 70Gt for Siberia and 55Gt for Alaska. I view the three estimates as supporting each other, because they are calculated in different ways. My estimate is 58% of the current cumulative production plus current World Energy Council reserves, 1,163Gt. However, all the estimates for the long-term production, and the cumulative production plus reserves are completely different from what the IPCC (United Nations Intergovernmental Panel on Climate Change) assumes is available for production in its scenarios. The maximum cumulative production in an IPCC scenario through 2100 is about 3,500Gt. This actually understates the difference, because in this scenario, A1C AIM, production is still rising in 2100, implying substantial production after 2100.

The transform analysis also gives time parameters through a linear regression. These are expressed as the years of 10% and 90% exhaustion. The last region to reach 90% exhaustion is Russia, in 2101. For world production, the curve fits indicate 2070 as the 90% year. This gives a time frame for thinking about alternatives. The time parameters have an additional element of uncertainty compared with the estimates for long-term production, because in some regions there have been shocks that are associated with a change in the pace of production. The most important example was the collapse of the Soviet Union, when production in Russia and Eastern Europe slowed. For this reason, it would be appropriate to view the year 2070 as a current estimate, subject to future shocks.

References

[1] British coal production statistics are available at the web sites of the Coal Authority and the Department of Energy and Climate Change

[2] Mohr, S.H. and Evans, G.H., 2009, ìForecasting coal production until 2100, Fuel, Vol. 88, pp. 2059-2067.

[3] Patzek, T. and Croft, G., 2010, "A global coal production forecast with multi-Hubbert cycle analysis," Energy, Vol. 35, pp. 3109-3122.

Contact

- Content: editors at theoildrum dot com

- Tech support: support at theoildrum dot com

License

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.

Here's my basic problem with your argument: How can you know that the amount of extractable coal will not go up substantially at higher price points?

Take a doubling of the price of coal. How many coal fields become economically feasible to mine at double the price? Is there some way to get at that?

Hi FuturePundit,

Thanks for your comment. The Germans have done an interesting experiment in the Ruhr by subsidizing the production of bituminous coal to the level of four times the world price for decades. This is as close as we get in the real world to "technically recoverable coal." The production has been crashing at 8% per year (like British underground production), and will likely end in the next decade. Like the UK, Germany evaluated its Ruhr reserves as over 100Gt a hundred years ago. The total production will be around 10Gt.

In the post, I mentioned UK Coal's debt problems. In the paper, a calculation is done that indicates that the price UK Coal is getting now, inflation adjusted, is more than twice the 1859 price. Also, I became aware over the weekend that Powerfuel, the parent company for Hatfield Colliery, is in administration (roughly equivalent to bankruptcy proceedings in the US), and the mine is for sale. The mine is a hundred years old and has shut down twice before. It is working its last seam and needs £30,000,000 in improvements. Anyone interested?

Dave

The Germans have done an interesting experiment in the Ruhr by subsidizing the production of bituminous coal to the level of four times the world price for decades. This is as close as we get in the real world to "technically recoverable coal."

Of course that is pretty much like looking at a single coal or oil field and finding just how much coal or oil can be squeezed out of it at four times the current market price. The 'Ruhr experiment' would seem to show very little about how much resource becomes available (as the real price quadruples) in areas that are currently just too distant from markets to be producing economically now.

Any analysis of $12 a barrel oil in decades not so long past would not have vertically distant deep water oil making near the contribution to the supply that it now makes.

Just looked at your 'More,Not Less!' post so its obvious we agree on that point. Since I want to see your spreadsheet you've actually forced my hand and I'm finally downloading an Excel viewer, thanks ?- ) I was too cheap to actually put the excel on this machine.

Of course a huge amount, probably most, of the the world's northern coal is not even classified as a resource yet. That coal is merely a hypothetical resource. Its not hypothetical because it may or may not be in the ground but rather because it may or may not ever be economical to mine it. The size of the US hypothetical resource dwarfs the BP stated US resource size--I'm guessing the same is true for the other two huge countries that spill into the arctic, Russia and Canada.

See my post below for a map of the minimum ice extant in 2010--shipping lanes to the north's resources look to becoming a near term reality. I know you love coal but I sure hope we don't burn near what is out there.

I read "Estimating Long-Term World Coal Production with Logit and Probit Transforms" earlier and think the Logit and Probit transform approach is an advancement over Hubbert Linearization. It looks similar to what Sam Foucher did with the Hybrid Shock Model. Although no doubt better than HL, which both Rapier and I have shown dissatisfaction with, I would prefer that we think about depletion and a host of other problems through maximum entropy and related probability techniques.

So this is not at all a bash at Prof. Rutledge, but just a chance to announce that I have compiled most of my blog postings and edited them to fit into a manuscript format. Whether it will make it easier for "everyone" to follow my arguments, I kind of doubt it. But having the narrative formatted in math markup, captioned figures, full index, references, links, and footnotes should make it easier for people that are serious about the topic.

Should have the first draft out early January as a PDF.

To be published as a book?

For now just a big 2 volume PDF, over 700 pages. The first volume titled Decline and the second volume Renewal.

Congratulations for the this milestone Web. I look forward for it, though I doubt I'll be able to digest it timely.

And sorry for not being as helpful as I wish I could. Best.

Thanks. The hardest part is knowing when to stop.

Anecdotal evidence supports the view that we are within sight of Peak Coal. In the picturesque Hunter Valley of New South Wales wealthy business people have set up thoroughbred horse farms. Lately coal miners want to dig large pits right next door. Now even the business types are questioning the scramble for coal.

http://www.ozeform.com/Racing/News/101214/Miningindustrytoworkwithbreede...

Another telltale sign in Australia is that Chinese and Indian interests are buying coal mines. For now that coal goes into the system but perhaps later it could be direct export. The Australian government seems to have its head in the sand or perhaps coal dust. We are the OECD's biggest per capita CO2 emitter (~20t a year) and the biggest coal exporter (250-300 Mt a year) yet we lecture other countries at the climate conferences. To Peak Coal I say bring it on.

The one line message I get from this article would be this -

Three peer reviewed studies have concluded that total world coal production to 2100 will be 20% or less of the figure assumed by the IPCC.

see further my comment 6:18 am below.

The message you get from the article is erroneous. The B1 scenario for instance has coal productions that encompass the estimates from Dave, but he fails to mention that. IPCC has a wide range of scenarios, and makes no predictions about which the future will look most like! That is up to us to choose...

With the B2 scenario follows a calculated 2 centigrades increase in temperature 2100 compared to 2000.

Boof is right, kinda. The IPCC scenarios are demand led, and all based on the same large reserve figures. The B1 scenario is just one where due to socio-economic factors we choose not to use as much fossil fuel.

The peer reviewed studies aren't addressing the IPCC's demand led scenarios, they are addressing the common large reserve figure. The studies suggest this reserve figure (and the production rates it supports) is considerably less than the IPCC assume.

ok fair enough, I dont know the reserve estimate in B1.

BUT Boof assumed "production" (not reserves), so he takes in the wrong spirit from the main post in any case. B1 has coal production which is as Dave states from his analysis, less than 700 Gt.

Agreed. Unfortunately, Rutledge continues to tie his estimates to IPCC reports that are now based on science even further out of date. Kjell Aleklett continues to make the same error.

What both fail to acknowledge is what you cite above: they are scenarios, not predictions. Rutledge, at least, being a scientist, should have no problem understanding this except that he is not a climate scientist, but studies geology, if I recall.

He has at least chosen to merely mention the IPCC rather than go on at any length. I believe this to be a wise course of action on his part, for he leaves us to guess at his motivations and retain plausible deniability. However, we cannot let this pass without comment.

In addition to the error contained in mentioning but the worst case scenarios, thus creating the incorrect impression that the IPCC was somehow "wrong" and their conclusions improbable if not impossible, Rutledge fails to acknowledge that what the IPCC said three years ago is actually now 5 - 30 years old. The massive amount of research and significant new findings make any conclusions of the IPCC IV nearly irrelevant. If Rutledge wishes his work to be taken seriously, he must take a different approach to coal reserves and the IPCC.

Avoiding this problem is simple: 1. Use his estimates of coal reserves to analyze the full range of IPCC IV scenarios; 2. acknowledge research since 2005, such as http://climatechangepsychology.blogspot.com/2010/12/jar-dropping-tempera... and http://www.youtube.com/watch?v=_8WsIr7m-4w, for example.

The basic logic that we will reach 2C above pre-industrial with what is already in the pipeline, and that both sub-sea and tundra-based clathrates are already degassing at increasing rates should cause Rutledge and others to hedge their bets. The logic is simple: if the worst case scenario (melting clathrates, melting glaciers, melting Greenland, melting WAIS, massively reduced Arctic sea ice 40% reductions in plankton, ocean acidification, etc. ) is already being observed, and it is, then coal reserves are irrelevant because any additional emissions are much too dangerous to allow. In fact, more and more climate scientists are saying 3 and 4C is already inevitable. A finding that supports this is the one by Hansen, et al., that Greenland has previously melted at a 400 - 600 ppm range. That is, we are already in a range that can raise sea levels 7 meters.

In the past, the explanation that if the IPCC hasn't reported on it yet, it's not official, is erroneous and rejected outright. The IPCC simply collates the science done up to a given point in time and offers a consensus opinion on what may lie ahead, it does no science. The science is what it is and is not changed in any way via the IPCC reporting process.

That this new data seemingly does nothing to give pause to Rutledge and Aleklett is disturbing, to say the least. Rutledge, at least, is a scientist, after all.

I look forward to an explanation of Rutledge's thinking on ignoring climate science of the past five years and his focus on only one of several scenarios.

I encourage him strongly to contact Katey Walter Anthony or her colleagues involved in Arctic research if he wishes to maintain a balanced view of the relationship of carbon to climate:

Water and Environmental Research Center

525 Duckering Building

University of Alaska Fairbanks

Fairbanks, Alaska 99775

(907) 474-6095

(907) 474-6095

kmwalteranthony@alaska.edu

Happy digging.

pri-de,

"but studies geology"

Don't investigate much before you write, do you?

"for he leaves us to guess at his motivations and retain plausible deniability"

New to The Oil Drum? Stick around, you might learn some politeness.

Dave

But Cmon thats a completely dissatisfying answer. Ok the two sentences you choose two mention was the two weakest in the text above,

but they are not completely hostile neither. It is poor that you choose that easy way out, instead of explaining what you really want, Dave.

Where is the problem with the B scenarios or the new 3 w/m2 scenario?

Dave,

Please acknowledge in my post above that I reference your earlier work. No, I am not new to the oil drum. I've no doubt I read it more often than you and investigate all areas of the current crisis, save energy production explicitly, more thoroughly than you do.

I see no impolite comments above. Segeltemp has pointed out problems with your analysis, as have I. Your post here shows no evolution of your thoughts over what you produced in '07 and no evidence you have taken any critiques to heart.

So you're not a geologist. You also are not a climate scientist. My points must all be invalid, then.

Contact Katey. She has responded to my e-mails in the past, I'm sure she'll respond to yours. It is an important issue, and it is important that you, Kjell and others come to understand climate because you are, imo, grossly misinforming the public on this issue.

The logic is simple: the changes so far exceed worst case scenarios, but are occurring at CO2 levels far below those eventual levels. The A1 scenario is irrelevant. We are 90 years ahead of schedule.

Contact Katey.

DaveR,

You should actually address the issues raised, not add your own flame. Is the official Oildrum policy to ignore climate science. We are now hovering close to 400 ppm....and rapidly climbing.

Two comments on the state of UK Coal reserves and the financial health of UK Coal plc.

Some surface mine reserves in the UK have been or are proposed to be sterilised by Government action. The Governments of Scotland and Wales have already introduced a 500 metre buffer zone between areas of settlement and surface / opencast mine sites. When this proposal was made for Wales coal producers claimed that it would sterilise a significant proportion of known coal reserves:

" Members expressed there concerns that the 500 metre boundary proposed in the

consultation would lead to nearly two thirds of the coal reserves in Wales being

sterilised and that the remaining third had either been worked or was uneconomical.

Members said that the introduction of wind farms was also causing issues for the

sterilisation of coal reserves. Members felt that the impact of this sterilisation would

close the surface mining industry in Wales. Members noted that this was likely to

form a precedent which would be followed by England and Scotland."

(8th Meeting of the UK Coal Forum available @

http://webarchive.nationalarchives.gov.uk/+/http://www.berr.gov.uk/files... )

I do not have a reference to show what the impact of such a measure has been on Scottish coal reserves.

Now Andrew Bridgen MP has a Bill before Parliament to introduce similar legislation to cover England. First indications are that, if passed, this measure would reduce available English coal reserves by a further 200 - 500m tonnes of recoverable coal (see 'Visit to opencast sites test out buffer zone', The Journal 3/11/10 @

http://www.journallive.co.uk/north-east-news/todays-news/2010/11/03/visi...

As yet I have no information on what proportion of known English / UK reserves this represents.

In addition, as possibly the original author of the cumulative deficit being carried by UK Coal plc in 'UK Coal: An Alternative Report' and the update 'Briefing Note C1 'UK Coal's Financial Situation' avaible from http://www.leicestershirevillages.com/measham/minorca-protest.html, just to bring UK Coal's debt figures up to date its last Interim Financial Staetment, October 2010 indicated that the level of debt had risen to £265m (See http://miranda.hemscott.com/static/cms/2/4/2/6/binary/6893857063/1812145...)

Just to put the 200 - 500M tonnes estimate of England's recoverable coal (above) into perspective, because of rapidly declining home production, the UK, England with Scotland & Wales & N.Ireland, in recent years has imported as much as 50Mt a year for power generation and consumed up to 70Mt (albeit somewhat less than that since 2006). Coal's share of primary energy production in UK has declined from around 90% in 1950 to less than 20% since 1995.

Dave,

You may be aware of this already but I'll post it anyway

I've just come across some 'official' information on the state of UK Coal reserves as at 2006. Then, the statutory legal body with the responsibility to safeguard coal reserves and promote their utilisation (as well as other functions), The Coal Authority gave evidence to the Government's 2006 Energy Review.

In it they gave three definitions of how to define coal reserves, 'coal in place' , 'recoverable reserves' and 'operating reserves'

After reviewing changes made to assessing the UK Coal's reserves dating back to 1977 the evidence presented to the Government was that there were then 86m tonnes of recoverable coal in deep mines which would be exhausted by 2020 if no further investment occurred. if investment was undertaken then 159m tonnes of recoverable coal which on present trends would be exhausted by 2035. The total opencast / strip mine reserves were put at 909mt in 1993 in the evidence.

The information is downloadable from

http://www.coal.gov.uk/media/860AD/Response%20to%20Energy%20Review%20-%2...

The (UK)Coal Authority web site address is:

http://www.coal.gov.uk/

Hi Steve,

Thank you for the link, which shows how the thoughts on reserves have evolved over time.

Dave

Dave, thanks for your reply to my comments,

I can now update the information about UK Coal reserves and answer my own question about the proportion of UK surface Mine reserves that my be sterilised if Andrew Bridgens 500m Buffer Zone Bill is successful. Below is the latest assessment of UK Coal Resources by the Coal Authority dated 4th March 2010 (personal communication)

Deep Mines (all categories of reserves) 2,552m tonnes

Surface Mines (all catagories of reserves) 869m tonnes

Total 3442m tonnes

English Surface Mine reserves, according to this analysis, totalled 516m tonnes.

If correct, this means, according to the news story in the Journal above, that Andrew Bridgen's Bill could sterilise between 250 - 500m tonnes of the English Surface Mine Reserves, or between 48 and nearly 97% of such reserves!!

The Bill is due for it's second reading in the UK'a House of Commons on 11th February 2011. In light of these figures it will be interesting to see what happens.

Hi Steve,

Thank you for the link to your report about the UK Coal losses. I should have referenced it. My error.

Dave

"....The main production in Montana is from the Powder River Basin (PRB), and it appears that Wyoming drew much the better hand in the PRB. I believe that the differences in PRB production for Wyoming and Montana represent geology at least as much as any other factors."

One significant factor in Montana coal production is the lack of access to local rail lines. During the late 1970's through the mid 1980's several new rail lines were built in the Wyoming's Powder River Basin to access this coal, most notably the Gillette to Orin line of the Burlington Northern railroad. Later the Union Pacific railroad built a connector to the PRB. In contrast, the state of Montana has had many rail lines removed during the late 1970's and early 1980's. As example a mine at Klein, MT has to truck the coal about 50 miles to a rail head near Billings since the rail line through Klein was abandoned in 1981. The coal mine shut down, then reopenned after the state rebuilt the highway for heavier trucks to haul the coal.

Unless the coal can be shipped almost entirely by rail, some of the US coal deposits may not be economical to mine, especially given the high cost of trucking due to fuel price increases. Besides, most states do not want the burden of heavy coal trucks destroying the highways, as they cannot they afford repairs with tax revenue shortfalls. And certainly the coal mine companies cannot afford to build new highways. So the coal may very well remain in the ground forever at numerous places in the US.

It may come down to abandoned railways being rebuilt as in "trails to rails". Anyway, Kunstler and others think railroads will regain their significance as a serious mode of transport for passengers and cargo once the era of cheap energy is behind us. I think it will soon become apparent that ripping up railroads and building more highways as they did in the 80's and 90's was a bad move.

There's little question that freight will move from trucks to rail. OTOH, passengers will mostly move to EVs.

Local freight, between the intermodal yards and the shipping points will stay truck. There are too many origins/destinations for freight to go back to rail without a huge investment to build out local railroad tracks.

Maybe time to start thinking about alternatives. One of the issues would be that areas are built up and there is no room for a line while tunnels are expensive. If it is freight only how about suspended monorails above roads. Individual units with electric pick up. They could be semi-autonomous to route to different points. If people object to no man on board then take a hint from the future of the aeroplane and leave space for a man and a dog.

NAOM

I think that distribution of goods will become more efficient around two models.

On model is the parcel delivery model, where the customer orders over the web and one of the parcel delivery services optimizes transportation from the distribution center to the customer.

The other is the WalMart model, where the customer only drives to one store for all their shopping needs, and WalMart optimizes the transportation of a complete array of products to the store.

Between these, you can take a lot of truck miles out of retail distribution. You also achieve a lot of real estate and energy savings by getting rid of small inefficient retail establishments.

I agree. I really meant long-haul trucking.

Short haul trucking can electrify with little problem. Companies with large local delivery operations, like Staples, UPS and others, are moving to electric trucks (though they're still moving slowly):

"The trucks, which have a top speed of about 50 mph and can carry 16,000 pounds, cost about $30,000 more than a diesel, but Staples expects to recover that expense in 3.3 years because of the savings inherent in the electric models, Mr. Payette said."

http://online.wsj.com/article/SB1000142405274870458480457564477355257330...

I don't know where you live, but in Sweden rail takes 4% of cargo transport, and without massive investments, it is as high as it gets. Passenger transport is incrasing by the year, and we are already running the rail system at above maximum capacity. In Sweden,and most of Europe, rail will not carry most of the goods in the future. We don't have enough rail for that. I still maintain railroads are for moving people around.

1) in the US, the majority of freight goes by rail - the rail system is optimized for freight, and passengers take a distant 2nd priority. Freight capacity is fully utilized currently, but capacity could be expanded relatively easily by double tracking and adding more rolling stock.

2) in Europe, rail is aimed at passenger transport, and the majority of freight goes by truck - the rail system is optimized for passengers. A major barrier to expansion of rail freight is non-standardization of track, signals, etc.

According to Alan Drake (Alanfrombigeasy) there is a large potential for expansion of rail freight on the continent (France, Germany, Switzerland, etc). I'm not sure if he's addressed Sweden.

Large investments may be needed to expand rail, but you have to put those costs in perspective: how much will Europe spend on diesel for freight over the next 30 years? 2 Trillion Euros??

North America (the US, Canada, and Mexico) has an integrated freight railway system that carries almost half of the continent's freight. It is almost completely privately owned, and there are about 600 railway companies (although the seven Class I railways - five American and two Canadian - carry most of the freight), but they can interchange freight cars to get it freight anywhere in North America to anywhere else in North America.

There is a system of pooling freight cars that allows railways to borrow freight cars from other railways without asking for permission, and it is very effective in moving freight cars to where they are needed with no regard for who owns them. Many companies only own freight cars and have no locomotives or tracks of their own. They make money from the use of their freight cars. Other companies have locomotives and tracks, but not very many freight cars. They make money from moving freight cars for other companies.

One of the biggest advances has been the double-stacked container train, using intermodal containers to move cargo from the seaports to the destination cities, where they are loaded on trucks for final delivery. Clearances are sufficiently high in most of North America that they can put two containers on each railway car, and since the trains can have over 100 cars, they can move over 200 forty-foot (12 metre) containers per train. Often these containers are oversize (overlong and/or overhigh) because the clearances are large enough.

Using computerized scheduling they can move about 24 of these 200-container trains per hour in each direction over a single track, and if they double-track the line, they can move considerably more. In some places the railways are triple-tracked or quadruple tracked.

The only problem is that this system is incompatible with carrying passengers, so the freight railways do their best to discourage the use of passenger trains on their tracks. Their goal is to make money, not compete with the airlines.

That puts North American rail in a nutshell nicely RMG. I was aware the US and Canada linked freight rail seamlessly (US/Canada cooperation in general, is in my opinion, is unrivalled). I guess I should have known Mexico was part of the system as well, since some of the illegal traffic carried by rail does make the news from time to time.

Per chance do you have access to the numbers on cost per pound/mile of a double stacked container freight relative to that of a container freight being pulled as part of a semi tractor-trailer/s load? That would be instructive. To make it a truly comparable any extra handling and miles rail freight accrued relative to that of truck shipped freight would have to be accounted for but that might be just tad hard to work out.

On another subject of interest to us both:

I don't know if you had a chance to check out the 22 page paper, History of sea ice in the Arctic, published in Quaternary Science Reviews 29(2010)1757–1778 phil harris linked down the page. I'm about a quarter of the way through it (in the middle of "Types of paleoclimate archives and proxies for the sea-ice record," a thorough and balanced accounting). It is very much worth the effort.

Maybe, maybe not. There are exceptions, but many of the rails that got converted to trails were old and twisty, difficult or impossible to bring up to modern standards for curves and the like. (And those standards won't go away, because you can never backtrack on bureaucracy no matter how dire the circumstances - better to be "safe", even if it kills you.)

a ton of coal produces about 2.86 tones of CO2 according to this source

http://www.eia.doe.gov/cneaf/coal/quarterly/co2_article/co2.html

So the good news is that if Rutledge is correct, there will be

8 trillion tons of CO2 factored into the IPCC report that will not be generated.

This is about 240 years' worth, at current rates, if I have my math right. Our Choice says we produce 90 million tons per day

I've seen comments similar to yours fairly often throughout OilDrum, and even in this thread. I want to point out that the IPCC report isn't gospel - climate science is evolving, and the IPCC is a large group of diverse viewpoints, and subject to external pressure.

We really don't know what a safe level of atmospheric CO2 is. About a decade ago it was thought to be 450ppm, now James Hansen says its closer to 350ppm, which we have already exceeded. It's possible that there is already enough greenhouse gas in the air, combined with positive feedbacks, to completely melt the icecaps, and raise sea level by roughly 70 meters. We wouldn't know right away, because there is so much thermal mass in the air and ocean that the warming takes decades to centuries to arrive. In fact, the ice core records don't include a CO2 level as high as we have now, which suggests that we are way over the line.

If that is the case, even if future coal production has been vastly overestimated (which I don't have the knowledge to argue either way) we will still see catastrophic climate change. We'll just see it in the dark without any air conditioning.

I really think that this is very likely incorrect. We are likely to be as warm as the Eemian at present, and will almost certainly get warmer, however as Antartic and Greenland ice-cores span the Eemian we can be confident that such warming did not seriously impact the bulk of either ice-sheet. Antarctica is high and enclosed by the polar vortex so it's interior is largely isolated from the surrounding warming ocean. Although the West Antarctic Ice Sheet, being grounded below water, may be at risk; it'll take much more warming to melt the bulk of Antarctica. Greenland is at more risk, but again it's melt will probably take many centuries. That makes resultant sea level rise rather a slow process and hence likely to be manageable.

Regards this study.

What is interesting about this work on coal is that it does seem to me to cast more doubt on the highest IPCC scenarios. Although it should be borne in mind that these scenarios were drawn up from economic considerations, assuming that demand is the key driver. This and the other attempts to estimate resreves can be used to remove scenarios from reasonable consideration.

I still think that Kharecha/Hansen is the most useful paper in respect of fossil fuel depletion, using their coal phase-out scenario, at 330Gt Carbon emissions fro 2007 to 2050. Assuming a conservative 70% carbon content that's ~470Gt coal, well within the 680Gt coal found by Euan Mearns in the lead article. As K/H's scenarios b to e all implicitly assume this conservative emission of coal we can say that it's likely humanity can't push CO2 much above the region of 500ppm.

This back of envelope calculation does not include feedback-emission from the natural sources. However note that most of these sources are likely to be relatively slow (chronic, not catastrophic), excepting Arctic Permafrost emissions: Both changes in ocean CO2 uptake and Arctic CH4 clathrate destabilisation are rate-limited by ocean warming rates, and in the latter case sediment waming rates.

None of this can be used to argue that climate change is not a factor. However it seems to me that the worst case scenarios are looking less likely, which can only be considered good news.

This post and discussion is mainly about coal and how this links to IPCC emissions scenarios. Going off and discussing how these emissions scenarios may impact actual climate is off limits.

Then shouldn't he have not mentioned the IPCC at all?

Exactly. The only reason anyone cares about the IPCC scenarios is because of what they predict for future climate change. Its completely legitimate to discuss the effect of declining coal availability on projected future emission scenarios, but its equally valid to point to evidence that those scenarios may be wildly optimistic in their projected impacts. I posted links to two sources that suggest dangerous warming can occur at the CO2 levels we have in our air today. That post was deleted.

Thought police at work. Come on. Unreal and embarrassing.

If you want to discuss coal, then the article should be prefaced with something like the following:

"The following discussion concerning coal makes no claims about its effect on global warming."

Off limits. Gag. I thought the Oil Drum actually encouraged thinking. Apparently not.

Thanks for the interessting article.

One minor comment on German coal reserves. I've talked to some German coal miners of the Ruhr region recently and they stated that there are definitely large coal seams up to 6m thick in large numbers left and not yet mined because of different reasons (deep >2000m, no mines left in the regions of the seams - e.g. Saar, environmental restrictions, etc.).

So maybe this coal will never be mined, but there are definitly large amounts of coal left with significant positive EROEI, even in mature regions like Germany, but they are not mined because we are not China and do not bring up anything "at any price". The reason the price of the Germany coal is that high is not only geological (of course it is to some degree - 1800m deep mining etc.). But a German miner earns about $5000/month, a Chinese maybe around $500/month if he's lucky, environmental restrictions in a dence populated region like the Ruhr area in Germany are extrem etc.

This profile of Germany suggests that production has declined due to the closure of inefficient mines in the former East Germany; also hard coal is favored for imports of course, Poland being the largest supplier. Factoring in desperation and/or nationalism to these models would be apt, I think - a former industrialized nation suddenly suffering through brownouts will likely drop all these secondary concerns tout suite. Or perhaps react by building out cleaner energies, who knows? But much of these resources remain viable to extract, just not economical, and as long as economics dominates the game they remain in the ground.

Nice to have you around again Dave.

I calculate your Coal ultimate to be something around 480 Gtoe (I work with these units). Jean Laherrère, who also uses data from the BGR, is presently coming to a 700 Gtoe ultimate. The EWG assessed something between 600 and 650 Gtoe. BP reports available reserves of some 700 Gtoe.

The essential question is: what makes you prefer the ultimates provided by curve fitting methods over the reserve estimates?

Hi Luis,

Thanks for your comments. The view I take in the paper is that with respect to estimating long-term production, the curve fits and reserves are complementary. Reserves numbers are available early, and they provide a loose upper bound. Curve fits are unstable in the early years, but they have been more accurate than reserves once they stabilize.

Dave

Thanks very much for this Dave. When you first posted this assessment I was somewhat sceptical that such large amounts of coal would be left in the ground.

Since then I've come round to your analysis. the price of coal has increased substantially over the past 2-3 years to the point where now Nuclear Power is unequivocally the cheapest form of electricity production on the East Coast of China. The Chinese have responded and now propose 245 reactors by 2030 (from 11 in 2009). The number keeps going up. So all those deep seams look like being priced out of the market just like British Coal.

What you write is not correct: "However, all the estimates for the long-term production, and the cumulative production plus reserves are completely different from what the IPCC (United Nations Intergovernmental Panel on Climate Change) assumes is available for production in its scenarios."

Not "all":

You have missed for example scenario B1 which has C emissions of about 700 Gt (including coal, oil and gas, so coal is smaller than your estimate).(With that scenario a temperature rise of 2 degrees centigrade is calculated by 2100 compared to 2000, btw.). (See figure 10.26 in IPCC 4th report chapter 10).

Furthermore, keep in mind that the scenarios you criticize were constructed 10 years ago, and are being updated as we speak for the next assessment (see for instance "IPCC Workshop on New Emission Scenario

Laxenburg, Austria, 29 June - 1 July 2005" http://www.ipcc.ch/publications_and_data/publications_and_data_supportin...).

The scenarios are NOT predictions, but a purpose for the scenarios are also to be used as sensitivity studies for the models.

The evolution of scenarios is discussed to produce a class of "most probable" scenarios, that better can be used and understood by end-users. But that brings on a range of difficult questions too.

Id suggest you stop bashing on that particular A1 scenario - it is NOT a prediction.

All the IPCC scenarios assume the same large fossil fuel reserves, they just don't use them up. None of the scenarios become supply-side limited. This analysis doesn't bash any particular scenario, but the assumptions the whole SRES (and the new RCP) family sits on.

Well two things:

1) dont you agree it is slightly dishonest to make an analysis (main post) and say: "coal is less than literature, 700 Gt". then Dave compares that with one of the high end scenarios: "look thats ridiculous". If that aint bashing I dont know what. Why dont dave compare it with one of the lower sccenarios "look that scenario is same as my estimate"?

2) the new scenarios might still have too high reserves, but if the reserves are not used up we are getting to reality as TOD thinks it is, thats a fairly correct approach no? furthemore in http://cmip-pcmdi.llnl.gov/cmip5/docs/DraftRCPExtension_WhitePaper_26Jul...

there are discussions on "Inclusion of long‐term features not previously included in model comparison exercises, such as peak‐and‐decline behavior"

Note: PEAK and decline. I think it is fair to say that IPCC is working on getting fair scenarios out for the next report.

Hi Segaltamp,

Thank you for your comments.

For 1), I believe that Chris Vernon's response above is appropriate.

For 2), whether one prefers to use reserves or production curve fits to estimate long-term production, at least both the reserves based on seam maps and the production histories do connect to geology. The new IPCC scenarios (representative concentration pathways, or RCP's) are defined in terms of the radiative forcing in 2100 with three mitigation RCPs (2.6,4.5,and 6.0 W/m^2) and a fourth unconstrained scenario (8.5W/m^2). People who are interested in this can start with Jae Edmonds' presentation:

http://www7.nationalacademies.org/hdgc/Characteristics_Uses_and_Limits_o...

Edmonds states that the RCPs are "designed to yield radiative forcing values in 2100 that would give significantly difference [sic] climate outcomes."

This means that for the mitigation RCPs, the production numbers are effectively backed out from the assumed radiation forcing in 2100. The peak you mention is for the radiation forcing in RCP2.6. However, this peak is arrived at through climate policy rather than exhaustion. This makes the unconstrained RCP8.5 the appropriate one to compare with the results in my paper. RCP8.5 gobbles up a multiple of the reserves, just as the early high-end SRES scenarios do.

Dave

I am really interested in understanding what your problem with the RCP8,5 or 2.6 is.

I dont see why you have to point out that an IPCC scenario has a too large reserve. The model runs only care about the concentration of CO2 equivalents (roughly) in the atomsphere.

If there is a scenario 2.6 that corresponds to your production then all is well, no? You could state "that scenario, with this effect, is the one I personally predict is the most probable"? that is what the different scenarios are made for. Everybody should find one to his or her taste! and argue which one is the best path to follow.

The models simply dont care about C (reserves) left in the ground.

Again your alarming that the reserves are too big has little practiacal effect, as long as all scenarios are considered "the same", and there are scenarios with a peak included.

I mean you seem to hang on that IPCC should state "exhaustion" rather than "climate policy". Sure IPCC might say that now that IEA has said that. But it is only wording. The CO2 in the atmosphere is what matters for the model, and the peak scenario is already in there. I dont see the problem.

The IPCC needs to be basing their scenarios on the most accurate production figures available otherwise the scenarios are actually useless to policy makers who may be tempted to make the wrong decisions. If a scenario exists wher peak coal, peak oil and peak gas are all represented as accurately as currently possible, the policy options for dealing with climate change as well as the hard ceiling on energy supplies may well yield a better policy response from what we are getting from governments at the moment.

Any climate change scientist who refuses to even consider new information on possible geological limits to CO2 emissions is being scientifically dishonest. Personally I feel this is an area that the IPCC needs to do much more work on and if necessary, use its position to force open OPECs books and every other country that would conceal its resource and reserve numbers for all hydrocarbons.

And for the record, it is not the concentration of CO2 that matters, it is the radiative forcing and its subsequent effects that policy makers need to manage.

There exists exactly scenarios that peak coal peak oil and peak gas are represented. "as accurately" is the hard part - you realize that too right?

Are you not overstating the power of the 15 person office of IPCC slightly "to force open OPECs books" - that is outside the realms of 10 researchers daily work, no? You know, IPCC has a defined mandate from UN: to collect climate relevant peer reviewed articles and analyze these... thats their job, nothing else.

Ofcourse it is the radiative forcing that matters (from CO2 and greenhouse gases and feedbacks (albedo aerosol and H20)). Excuse me for slightly simplifying for readability in my answer above. But surely you understood that too, right?

We agree about several things, thats the good part. I just would like you to quantify and source your statements above ("accurately" - how, by whom; "better policy response"; "refuses to even consider" - who do you mean and where have you read that; "needs to do much more work" - where have you read what they do currently and HOW do you want that to change - please detail otherwise pointless).

Segeltamp, your logic is correct. Reserves in the ground are not relevant to climate, only that produced and burned/not sequestered is. While the assumptions of the IPCC were based in reserves estimates and production estimates, theirs is not a document about economics. What ultimately matters to climate is only what is produced and burned.

What should concern Rutledge is that we are matching the highest estimates thus far and that the scenario you mention that matches his estimates is already far behind reality.

Euan has put this off-topic, tho, so final word, I expect.

The message from this post is that the global coal reserves, at the current economic price, are a lot lower than is widely expected.

The implications for this need to be considered in the context of the global primary energy supply. Coal, oil and NG between them are about 80% of that energy at present.

We all know about peak oil. Natural gas has not peaked, but an increasing part of the remaining reserves are either in locations remote from their markets, requiring expensive LNG transportation, or are shale gas which is more expensive to extract.

The combined effect is that the global energy supply is getting more expensive. That means in practice the ERoEI is declining. More and more resources need to be invested to sustain or increase the total energy supply. The energy production part of the economy is increasing at the expense of the rest of the economy. Sooner or later the increasde expense of extracting fossil energy cuts into and decreases the rest of the global economy, and so cuts energy demand (at that price). The world will have hit peak net energy. We may already be at that point.

Soon after that, we will hit global peak energy. Total global GDP will decline.

Of course, we should be investing in non-finite energy sources as fast as possible, because these tend to have large, up front capital costs, but see the recent post by Nate Hagens to understand why we are not doing this as fast as we should.

Nuclear power is a more complicated case. The current technology is based on a finite fuel supply. It has huge upfront capital costs and unquantifiable decommissioning costs. It is a high technology energy source which will be hard to sustain in a globally declining energy environment. There are huge logistic bottlenecks to its rapid expansion. It has contested environmental impacts and is a political impossibility in many countries.

At this moment, the general consensus is that we must No go about amession of 1000 GT of CO2 to avoid à 2C of temperature increase.

http://www.nature.com/nature/journal/v458/n7242/full/nature08017.html

https://regtransfers-sth-se.diino.com/download/f.thompson/migrated_data/...

http://www.pnas.org/content/106/38/16129.full

You coal reserve estimate are way above this limit. Also, this does not take account of oil and gaz, especially non convetional. Also, it does not matter much how fast these reserve are consummed. This will only delay to moment when the equilibrium temperature is reached by a few decades.

I don't think it's accurate to speak about economically recoverable reserves in vacuum. Yes, as the price of coal increases with demand, it becomes more economically feasible to extract a greater percentage of the world's known reserves.

On the other hand, what is that price point and what will such a price for coal do to the economic viability of other sources of energy? At some point, it becomes cheaper to use other fuels, such as natural gas, nuclear, or renewables, than it does to mine coal, drive up demand, and commit to a long-term higher price of energy.

All the arguments in favor of coal use and expanding coal use are economic in nature: this stuff is cheap. But to keep it cheap, we have to abandon hope of recovering much of the world's vast coal resources because recovery of those resources is more expensive. At those kinds of prices, coal starts to become much less attractive: it's bothersome to transport, difficult to extract, of inconsistent quality, and difficult to burn efficiently and cleanly. It's really a sub-optimal fuel.

High liquid fuel costs, high natural gas demand, and some economically viable coal-to-liquids process projects may change the calculus, particularly if some of the prototype technologies for in-situ coal gasification take off, but consider what other hydrocarbon projects are in the (pardon the pun) pipeline:

-Japan has recently undertake serious research into methane gas hydrate extraction. This may seem a long-shot technology, but that's what people said to Sony about digital imaging in the late '80s and what American engineers said to Toyota about hybrid drive technology in the 90s. The Japanese business sector has a history of sticking with these long-term R&D projects, so I wouldn't be surprised if we saw the first commercial gas hydrate extraction facility open up in the next 10 or 20 years. This would dramatically expand global gas reserves.

-Shale gas goes ever on. There are concerns about it's production ability and impacts, but I suspect these will prove to be more technological issues than geological and it certainly doesn't seem to affect the futures trade.

-Oil sand developments continue, with the total cost lowered by currently cheap natural gas. This may change in the future, but any attempts at CTL technologies would require even more massive thermal inputs.

-Coal is falling out of favor as the electrical generating fuel of choice in the US and an expansion of nuclear power, renewables, and a deployment of more efficient coal burning designs in the developing world has hedged future growth projections. This is as much an infrastructural issue as anything else: in the States, we're tearing down old coal boilers, with more to follow in the next decade or so, so our actual ability to utilize this fuel source in the future is diminished. Furthermore, it's just as likely that high electricity demand and high fuel prices will make other sources of generating electricity just as economically and politically attractive as coal.

-And what about oil shales? Sure, they're expensive to use, but we're talking about a future where energy is expensive enough to make reserves of coal which are currently totally uneconomical profitable. It takes just as much effort to strip mine shales as it does coal and the industry expects profitability at $95/bbl (higher with higher natural gas prices). This cost comes down as economies of scale are deployed. Either way, any future renewed interest in coal to liquids technology, as I believe would be the saving grace of the coal industry, would have to compete with unconventional petroleum production from tar sands and oil shales.

So there's a lot of economic considerations, infrastructural considerations, and we have to think about what future technologies currently under development may yield. In short, the point at which these currently unfeasible coal reserves are extractable may also be the point at which other technologies and sources may come online and how that would influence deployment of coal consuming technologies in the future.

Since coal is relatively expensive to ship overland, the rate at which mid-continetal reserves are consumed would seem to be related to the demand for electricity within a couple thousand kilometers of the reserves. This would be the case for Montana, Western China, Siberia, etc. Where large amounts of gas and oil are also available in the same vicinity, such as Siberia, it is likely that the reserves stay in the ground longer and are used less widely.

On the other hand, countries which have available coal reserves but limited other supplies of fossil fuel are likely to exploit them beyond the point that would be consistent with a "global" model of reserves and economic value through a variety of subsidies.

Lastly, if Peak Oil seriously jeopardizes the welfare of the economically well off, the think tanks will be funded to reevaluate their conclusions, public opinion will be reconditioned, and environmental concerns will go out the window.

Nations that have access to coal will use it, while others will depend on imports of gas or nuclear fuel.

How did you treat Utah coal reserves?

http://geology.utah.gov/online/c/c-93/gsekcoal.htm

The economics of mining Utah's coal depends partially on the size of each deposit and its proximity to a rail line. If the coal bed has 10 million tons, but is 100 miles from a rail line, the added cost ship by truck is $5 to $10 per ton, counting infrastructure cost of highways. So, is this coal competitive with other coal close to rail lines? Probably not.

My prediction is that a lot of the coal that is not near a currently operating rail line may never be mined as the cost of diesel fuel heads higher and likewise the infrastructure cost to build upgrade highways or build new rail lines heads higher too. As FF prices escalate so does the cost for steel, concrete, and equipment operations to build infrastructure. Law of receding horizons will make some coal uneconomical forever.

Hi Merrill,

Utah's production shows a two-cycle pattern like most of the western states, and it is included in the Western US region in the analysis.

The Kaiparowits Plateau is part of the Grand Staircase-Escalante National Monument, created by President Clinton, and that coal cannot be legally mined. I believe that it should not be included in the EI reserves for Utah, which are currently 2.7Gt.

Dave

It will not be mined while we have money to import oil and until natural gas supplies are depleted, but it will be mined before people will freeze in the dark. Same thing with Alaskan coal.

sad but very likely true, but if we ever start really going after those huge northern coal deposits (that have only been mapped in the most cursory manner to date) the freezing part may not be relevant on much of the planet's surface. Most of the scenarios that put peak coal in the near term assume some other energy sources stepping up cheaply as oil prices and electrical demand skyrocket in tandem--lets hope those are the correct assumptions.

Of course the peak coal predictions based on just not enough capital left in the demolished world economy to develop those northern coal resources assume the opposite, that nothing cheap comes on line and the modern world as we know it comes to a crashing halt.

One thing looks certain shipping lanes to the much less frozen north are going to be a lot larger and open a lot more of the year. Four of the last four years have had the lowest minimum ice extant on satellite record, 2007 having the least ice followed by, 2008, 2010, 2009--I know that modern satellite only goes back to 1979, but as the ice recedes some significant sediment core surveys should give us far better insight into the last million years or so of the arctic ice cycle.

Dave,

I just wanted to congratulate you on providing the Excel spreadsheet along with your results. I expect a large amount of effort went into compiling the historical numbers and making them freely available is a huge stride toward a more 'Open Source Science'.

If scientific results are supposed to be reproducible, scientific papers should always be accompanied by the data and software from which the results are generated. David's inclusion of an Excel spreadsheet is so remarkable because it so rarely occurs.

Thanks for setting a good example,

Jon

Absolutely.

add my thanks for your comment.

(proprietary science is a contradiction in terms, IMHO)

phil

The problem that I have with this analysis is to do with the distinction between known resources and reserves. We are in (or rapidly coming to, depending on who you believe credible) a period where crude oil is going to be perpetually over $100 a barrel, because of the costs for production at the margin needed to meet global demand. The demand for domestically based alternate fuels will thus rise.

At present coal is still one of those products (Germany being an exception to the almost global rule) that it is the cheapest producer that gains the market, and that there are still many deposits where all you need do is scrape the dirt from the top and buy a bigger shovel and then, provided you can provide transport the coal, it costs very little (about $10 a ton) to produce. Even within those constraints we have the example of Botswana who, until recently had 1 power station, 1 mine, and 1 mining machine - all that was needed in a country that bought most of its electricity from South Africa. The reserves of the country were therefore considered to be very small. Then South Africa decided it needed its power for itself, and the feed to Botswana is being cut off. Suddenly there are coal mines being developed and reserve estimates continue to climb. And the Chinese are helping, since this could be another source for future supplies and so the reserve base is climbing (up to 200 billion tonnes ).

Even in the UK the need to meet future energy needs (as opposed to goals) are causing the government to have a bit of a rethink on their coal-fired power plans.

Coal's biggest competitor at the moment is natural gas, and the plentiful cheap supply of this to power plants is restricting and confining the coal market. However there is a production cost and ability to gas from shale, that Art Berman has written about, that will, over time likely reduce the volumes that are available at a competitive price, relative to the price and availability of coal for power stations. At which time coal supply will require the conversion of more of what is now only a resource, back into a reserve.

Hi HO,

Thank you for your comment. The current range for the historical fits since 1995 is 653-749Gt (14%). We can accommodate Botswana.

Dave

Well yes but there is a whole lot of Africa that might be in the same boat as Botswana.

It is interesting that the EIA, writing in this week's TWIP, has shown that the crude reserves in the US increased by 9%, and natural gas by 11%, primarily as a result of the increase in price. The world is already learning that governments can't legislate technology (vide cellulosic ethanol), although it might take a long while for some governments to learn that lesson.

In the meanwhile, with your indulgence, I have posted a somewhat longer reply on Bit Tooth.

Hi Dave,

Thank you for the link.

Dave

Here are some of my thoughts:

First, why ask how much coal we have? Don't we want to reduce or eliminate coal because of climate change?

Yes, we do. For better or worse, however, it's important to be realistic about the availability of coal. If we're not running out of it, we have to make a conscious decision to eliminate it, not rely on geological limits. Also, it's good to know whether or not we'll face energy shortages due to coal scarcity. If not, we have more options - if we face an emergency, we will have the option of using coal. Of course, that may be expensive and difficult to do without excessive CO2, but options are usually good to have. In that vein, we should note that if we have coal to spare it's actually easier to sequester CO2 - sequestration consumes a fair amount of energy, and if things are tight it will be much harder to pay for something whose necessity isn't obvious to all .

So, do we face limits on our coal production, as a practical matter?

No. Coal is unlike oil - we have enormous reserves, we know where they are, and in many cases there is no significant increasing marginal cost to their extraction, except for temporary costs of expansion.

Do higher energy prices raise the costs of extracting fossil fuels?

It depends on the individual case. Coal has a high E-ROI. For instance from a recent survey by Heinberg ( from http://www.theoildrum.com/node/4061 ): "Consider the case of Massey Energy Company, the nation’s fourth-largest coal company, which annually produces 40 million tons of coal using about 40 million gallons of diesel fuel—about a gallon per ton" .

That's a very high E-ROI: a gallon of diesel is about 140K BTU's, and a ton of coal is very roughly 20M (see http://www.uwsp.edu/CNR/wcee/keep/Mod1/Whatis/energyresourcetables.htm ), so that's an E-ROI about 140:1! Now, diesel costs very roughly 10x as much per BTU (reflecting it's scarcity premium), so the cost ratio isn't quite as favorable, but it's still well above 10:1. So, the price of diesel rises by $1 (roughly 25%), and the cost of coal rises by $1, or very, very roughly 2% - not a big deal. Also, we should note that coal mining (and transportation) is often electric even now (especially underground), and that it's pretty amenable to further electrification - in other words, coal mining can power itself using a small fraction of it's production.

Will higher coal prices make a substantially larger fraction of the coal available for extraction?

Yes, but only slightly higher prices are needed. Here's what Heinberg has to say: "if Montana and Illinois can resolve their production blockages, or the nation becomes so desperate for energy supplies that environmental concerns are simply swept away, then the peak will come somewhat later, while the decline will be longer, slower, and probably far dirtier.". The Montana "production blockages" he talks about are relatively trivial, and Illinois doesn't really have them. The pollution he refers to is CO2 and sulfur - the sulfur costs about 2 cents/KWH to scrub, and the CO2 might cost out at $80/ton of CO2, which IIRC would add about $30/ton of coal, should we choose to internalize this cost.

Illinois coal simply couldn't compete with Powder River coal with a 2 cent premium for sulfur scrubbing - it's as simple as that. UK and German coal became a bit more expensive, and they couldn't compete with cheap oil.

The same general rule applies to US, UK and European coal: only under Business As Usual is coal declining. I discussed this at length with David, and I thought we came reasonably close to some kind of agreement on this. If there are serious energy shortages, the old reserve numbers will apply, for better or worse.

So, would a doubling in coal prices substantially increase recoverable coal reserves?

Yes. Now, "recoverable" is tricky: the normal distinction used by the USGS is "economically recoverable" - that includes economic assumptions, and Illinois coal (and much other coal in the world), at a slightly higher cost as discussed above, is currently uneconomic. But, that's under Business As Usual - if we have a true energy scarcity, Illinois coal will very, very quickly become economic.

What about the "Law of Receding Horizons"?

That applies only to low E-ROI sources of energy. Coal is high E-ROI, unlike Canadian bitumen (tar sands) or Colorado kerogen (oil shale). I would note that the importance of this "law" has been enormously exaggerated, as it's confused with temporary capex issues and scarcity premia, which are allocating temporarily scarce capital resources.

More coal gets extracted from the ground each year as measured in tons, but hasn't the quality declined so much that net energy content is lower now than 10 years ago?

Powder River coal is lower energy density (sub-bituminous), but it's sufficiently cheaper to mine that the difference doesn't matter. Again, this is a purely economic shift from Illinois coal, which is higher energy density (bituminous). This shift has caused endless confusion to analysts unfamiliar with the coal industry (OTOH, people inside the industry understand this).

Aren't coal prices rising?

In many cases, this is due to the temporary costs of expansion. Oil & gas are much more expensive per BTU due to a scarcity premium, and so demand has increased for coal. Most coal is on long-term contract, not on the higher spot market (unlike oil). But it's important to be clear that in many places, like the US, the long-term marginal cost of extraction isn't really increasing, as it is for oil.

Is Coal-to-Liquids (CTL) feasible?

Yes, but projects tend to be large and expensive, and would be CO2 intensive. That means that investors would like federal loan guarantees, but that such guarantees are unlikely. Nevertheless, CTL is cost-effective even with fairly high carbon taxes, with oil prices at anything like the current level , and projects are slowly moving ahead . The best path would be CTL with CO2 sequestration - this would deserve guarantees.

Is oil-shale feasible?

With oil over $100/barrel, the answer is almost certainly yes. There's something like a $50T incentive there for exploitation, and somebody is going to make something work. In that way its similar to the Bakken basin, which may have 400B barrels of true oil, though only 4B is economically recoverable right now.

Kerogen has the advantage of not needing hydrogenation (which is needed for both tar-sands and CTL), which requires expensive natural gas or a combination of added energy and water (also a significant cost).

On the other hand Green River kerogen (mis-named oil shale) is low density, and a pain to dispose of after burning (it expands). That's why even low-value coal is more attractive for burning (which is what the Estonians do with it). That's also why retort conversion to oil (the conventional method) is unattractive, and why Shell is considering in-situ conversion instead.

Further, kerogen requires a lot of energy to upgrade - the Shell process looks very much like a very slow, inconvenient method of converting electricity to oil (kind've like ethanol, except ethanol mostly uses natural gas). All in all, it seems inevitable to me, but not cheaply or at large volumes any time soon.

I wouldn't reject it, as it is extremely valuable to have diversity in energy supply, but it would be much better to concentrate on electrifying our vehicles ASAP. In other words, we can't let it distract us from the main and best solutions available to us, which are, unfortunately, inconvenient for oil & gas and car companies.

Perhaps most importantly, kerogen burns quite nicely. If we were to run out of coal, we could certainly burn kerogen, and we certainly would before we let the lights go out.

Your entire post leaves out the transport cost for coal and therefore diminishes most of your arguement about coal costs.

Did you know that between 50 to 60% of the cost of western coal (PRB) used by eastern utilities to meet emission requirements is for transport by rail or truck/rail combination? And as fossil fuel cost rise, so will the cost of this transport, making coal even higher priced.

The railroad, which transport about 90% of the western mined coal, have tremendous power to increase prices for their services and I don't see this portion of delivered cost for coal going down relative to the mine3d price.

Outside of building mine mouth power plants and new HV transmission lines for trillions of dollars, I don't see the high railroad cost aspect being avoided.

You're right, I didn't address this question directly (for a discussion of oil inputs for coal mining, see the section titled "Do higher energy prices raise the costs of extracting fossil fuels?").

A $100/bbl increase in the cost of oil would increase the cost of transporting a ton of coal by $100/bbl x 1bbl/42 gal x 2 gal/ton* = $4.8/ton. That's a 2.5% increase in the cost of electricity, which means that railroads will be easily be able to out-bid other potential users, like trucks.

Coal transportation by rail can also be converted in a relatively straightforward manner to use electricity instead of diesel, meaning that reduced oil supplies are highly unlikely to have a significant direct impact on the ability of the US to transport coal.

We're going to have to make a conscious decision to eliminate coal - it's not going to run out, and make the decision for us.

*Rail transportation is about 440 ton-miles/gallon on average, and coal is at minimum 500 tm/gallon. Coal trains are probably even more fuel efficient, because the ratio of load to tare weight is greater than most other rail freight (particularly intermodal). 600 tm/g might be a good estimate. Low-sulfur coal in the US travels roughly 1,000 miles before being used (high sulfur coal travels much less). Dividing these tells us that transporting US coal requires roughly 2 gal/ton.

Did you know that between 50 to 60% of the cost of western coal (PRB) used by eastern utilities to meet emission requirements is for transport by rail or truck/rail combination? And as fossil fuel cost rise, so will the cost of this transport, making coal even higher priced.

That's because the cost of western coal (PRB) at the minemouth is incredibly low, less than $20 per ton.

Electricity in the US is about $0.10/kWh, and US coal generates about 2,000kWh/ton. That gives a retail price of electricity of $200 per ton of coal used, so a cost of $10/ton for coal represents only 5% of the overall retail price.

".... Low-sulfur coal in the US travels roughly 1,000 miles before being used (high sulfur coal travels much less). Dividing these tells us that transporting US coal requires roughly 2 gal/ton. "

Nick, your calculation is off by a factor of at least 2. The coal train may run 1000 miles to the power plant, but then returns empty, so the train makes a 2000 mile round trip for each load. That fuel use would be more like 4 gallons per ton.

Because coal trains wear out the track structure much faster than passenger trains and intermodal (container) trains, the cost per mile to operate such is the highest of any type of train. As railroad maintenance and operating cost increase, coal traffic will get a larger share of these costs. I know what rail industry cost drivers are as I worked for Burlington Northern and Santa Fe railways in the years prior to their merger. The successor company, BNSF Railroad, is the largest coal hauling RR in the western hemisphere.

We might need more data.

We don't have coal-specific fuel consumption data; we don't know what % of coal trains must return empty ("dead-head"); we don't know exactly how much consumption declines when a train is empty.

Fuel consumption is driven by 1) acceleration and climbing; 2) drive-train friction; 3) wheel friction; 4) wind friction. 1 and 3 will rise (and fall) with weight, but not the others. If coal trains wear out the track structure much faster than intermodal (container) trains, then they must weigh much more, and be substantially more efficient on average. Conversely, dead-head trains would consume less fuel, but the decline won't be 100%.

If the industry stat is 440m/g, we can assume that coal gets at least 600 miles/gallon one way (1.52 gallons per 1k miles). The empty train might use 50% as much the industry average for fuel on the dead-head leg (or, in effect, 880m/g, or 1.14 g/kmile). 1.52 + 1.14 = 2.65 gallons for the 2,000 mile roundtrip.

The 440m/g industry stat must include dead-heading: IIRC coal is roughly 1/3 all US train traffic, and it's not the only freight with this problem, so the above calc (which allocates this overhead cost only to coal) is conservative.

Because coal trains wear out the track structure much faster than passenger trains and intermodal (container) trains, the cost per mile to operate such is the highest of any type of train.