| The Bullroarer - Thursday 29th April 2010 | The Oil Drum: Australia/New Zealand | Resource Super Profits Tax |

Superannuation, Liebig factors, the housing bubble and a soft landing

Posted by Phil Hart on May 2, 2010 - 6:57am in The Oil Drum: Australia/New Zealand

This is a guest post by Cameron Leckie of ASPO Australia. (Superannuation is the term used in Australia for employer funded pension plans).

We are in a bind, a complex predicament of our own doing. We have designed a financial system that must grow or it will implode. Was the GFC the first of a series of tremors signalling the onset of that implosion? Can we prevent or delay the implosion? I think we can and I would like to propose one aspect of a plan that would use our superannuation in manner that might very well reduce the size and impact of future tremors on Australia and perhaps even prevent an implosion.

Before I do that however, let’s filter out the noise that surrounds our economy, examine some of the basic building blocks and consider its future direction. Fundamentally our society needs to be organised in such a way that our basic needs – food, shelter, health, education- are catered for with hope fully some spare capacity for the ‘nice to haves’. To date we have risen to this challenge by consuming more and more of everything, resulting in levels of economic activity that have consistently grown. Maintaining or increasing this level of economic activity relies upon there being sufficient inputs such as raw materials, energy and labour. This is where it becomes a little tricky. According to Justus von Liebig’s law of the minimum, growth is not controlled by the total resources available but by the scarcest resource or limiting factor (which I will call “Liebig factors”) in relation to the systems needs. Whilst Liebig developed this law after researching plant growth, it can equally be applied to economic systems.

According to Chris Clugston, 23 of 26 Non-renewable Natural Resources that form the basis of industrial civilisation are likely to experience permanent global supply shortfalls by the year 2030. This includes such key inputs as oil, phosphate rock and metals such as gold, tungsten and cadmium. Even if Clugston is wrong by half, the outcome is the same - growth and economic activity is set to decline and with it our capacity to meet our most basic needs.

Now let’s consider money. Whilst many, if not most people think of money as being wealth, it is not. Money is simply an instrument to make accessing real wealth easier. Real wealth lies in the value of the goods and services that are purchased. Because there are so many goods and services in advanced societies such as ours, we need a common standard to facilitate the transfer of goods and services and this is the role of money. Sometimes however, we don’t have enough money to purchase things that we want, such as a home. In this case we borrow money from someone on the agreement that we will repay both the principal and the interest.

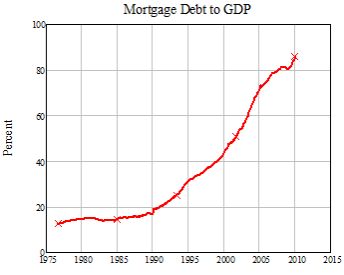

The term used to describe the situation where we owe someone something is debt and Australians along with just about everyone else seem to have fallen in love with debt. This willingness to take on debt coupled with the governments first home owners grant (or is that vendors grant?) as convincingly argued by Steve Keen, has resulted in the Australian real estate market remaining strong despite the GFC. The unfortunate consequence is that Australia’s Mortgage debt to GDP is still at historic highs.

Source: Steve Keen’s Debtwatch No 44

Steve Keen suggests a healthy mortgage debt to GDP ratio is between 25 – 50%.

So let’s take these two factors, debt and declining economic activity, and fast forward a couple of decades to see what the economy might look like. Let us assume that oil is the key Liebig factor. As per Liebig’s law, as the amount of oil available declines, the price will increase (relatively at least) as an indicator of scarcity. This will reduce the discretionary income available for activities such as travel and in turn increase unemployment in associated sectors. As unemployment increases, downwards pressure will be placed on wages, as the labour force rises in proportion to the jobs required to maintain a lower level of economic activity. Higher unemployment and lower wages will result in loan defaults and downwards pressure on asset prices. Indeed much of the long term debt on issue is unlikely to be re-paid once this process commences. The US housing market is a prime example where one quarter of mortgage holders are underwater and foreclosures continue at historically high levels. The availability of credit will decline as financial institutions realise that the ability for people to repay debt will fall as the level of economic activity contracts. Whilst we are likely to see periods of inflation and hyper-inflation in the transition to a shrinking economy, as governments attempt to keep the old system alive through methods such as quantitative easing, the overall trend, at least for assets such as real estate will be deflationary. In contrast inflation is likely to be the trend for commodities, particularly those commodities that become Liebig factors. It is the deflationary pressure on asset prices, particularly real estate that I will now consider.

Steve Keen argues that a property market crash is essential for positioning Australia for sustainable economic growth. This view in my opinion assumes there must be a day of reckoning in our economy and in particular the property market. But what if there was a course of action that allowed property debt to be reduced to manageable levels thus avoiding the property collapse and maybe even that of the financial system. This is arguably the most important predicament facing society today. The reason it is so important is that a zero-growth economy is incompatible with a debt based monetary system as eloquently explained by the University of Sussex’s Steve Sorrell. This situation is likely to be catastrophic in a contracting economy and thus timing becomes critical. Deflating the debt bubble must occur before Liebig factors take hold of the economy and we have few options with which to adapt. Enter your superannuation.

Most banks these days offer offset accounts for mortgages, where any balance effectively reduces the principal of the loan and hence interest payments. We should be able to use our superannuation in a similar fashion, with the option of using both our employee and employer benefits, where possible, as an offset to the mortgage balance. The advantages of this would be many. Firstly it would enable mortgage holders to pay off their mortgages far more rapidly, reducing the number of under water mortgages and foreclosures as Australia’s property bubble deflates, as it must in a contracting economy. Secondly, it would effectively increase the savings rate of Australia’s banks, reducing the requirement for international borrowing and limiting the requirement for banks to raise interest rates. It might also pave the way for a transition to 100% reserve requirements in our banking system. For mortgage holders, it would essentially provide a rate of return equivalent to the banks interest rate on their superannuation. In a contracting economy this would be a very good return indeed.

Of course there would need to be safeguards, such as ensuring that the mortgage holders continue paying their minimum repayments, lending criteria are maintained and perhaps only a certain percentage of a mortgage could be offset. As the economy shrinks and the credit/debt bubble deflates, house prices are likely to fall, probably significantly. With the lending of three of the big fours banks favouring home mortgage lending, this would place significant stress on Australia’s banks. This proposal would reduce the likelihood of bank collapses by keeping the number of foreclosures and the rate at which home prices fall at more manageable levels.

So what are the downsides to such a plan? Interestingly enough, both the capitalisation of shares on the ASX and the value of superannuation investments were just over $1 trillion as of June 2009. If a large percentage of mortgage holders withdrew the superannuation from other forms of investment, such as the share market, it would possibly trigger a collapse in equity prices. If the global economy contracts, this will probably happen anyway, the benefit here being that you the superannuation investor have an alternative choice. It could also result in a downsizing of the financial industry; however economic specialisation has a tendency to decline as societies reduce to lower levels of complexity, so the numbers of financial planners are likely to decline regardless of this proposal. It would also reduce bank profits, but at the same time reduce the risk of bank failures, arguably a price worth paying.

With the Governments review into superannuation due soon, perhaps it is an appropriate time to consider our superannuation as a tool to reduce the systemic risk to our financial system as we enter an era of limits and consequences.

Contact

- anz at theoildrum dot com

License

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.

Archives

- November 2010 (2)

- October 2010 (5)

- September 2010 (4)

- August 2010 (8)

- July 2010 (2)

- June 2010 (2)

- May 2010 (6)

- April 2010 (7)

- March 2010 (12)

- February 2010 (11)

- January 2010 (7)

- December 2009 (10)

- November 2009 (6)

- October 2009 (7)

- September 2009 (10)

- August 2009 (10)

- July 2009 (3)

- June 2009 (14)

- May 2009 (10)

- April 2009 (15)

- March 2009 (16)

- February 2009 (16)

- January 2009 (15)

- December 2008 (15)

- November 2008 (23)

- October 2008 (25)

- September 2008 (24)

- August 2008 (30)

- July 2008 (44)

- June 2008 (38)

- May 2008 (48)

- April 2008 (43)

- March 2008 (29)

- February 2008 (32)

- January 2008 (30)

- December 2007 (26)

- November 2007 (32)

- October 2007 (11)

Great post Cameron. I diverge however a little bit on your defintion of wealth.

The value of those goods and services is subjective and context sensitive. Production of them however comes down to a decision by someone to spend energy to make them. The energy will only be spent to produce them if there is demand. Our society allocates money to people and organisations which entitles them to call on that energy in the form of the goods they desire. Some people of course make better decisions than others, and choos to be on the productive side while most choose to live mainly on the consumptive side. As more energy enters the system, more money can loaned inot existence by the people allocated that job which is the bankers. Energy of course can only do work when it is changing from one form to another so the ability of the economy to grow is directly linked to the amount of energy that can be accessed to do work. Real wealth, I would argue is the relative ability to be able to access larger energy supplies to do useful work, not how many products you may have in a warehouse , shop or stacked up in your garage. The bits of paper, shiny metal or e-digits we trade with eachother are simply the markers that represent an ability to call on the net energy available. The energy form doesn't really matter, it's about who has it and what can be done with it.

The problem I see with super being used for mortgage offsets is that it would encourage people to build even bigger houses and borrow even more money. Australians ahve been rather good at leveraging to the hilt to buy housing which is fundamentally a consumptive rather than productive purchase.

Where superannutation could be used effectively is to build better towns, complete with the public transport, commercial centres, education and public amenities rather than the patchy bits of small scale land development which just gives us incremental sprawl. A properly planned town can build higher density dwellings that are affordable (no more than 30% of average wage). Only big money can put in the necessary infrastructure for this and I can see big super funds playing that role. Economies of scale can be achieved and better ROI for super funds investing in New Urban towns becasue they can be built far more compactly than traditional sprawl. Companies like FKP, Lend Lease and Stockland are already doing this but catering only to the very weatlhy end of the market at he moment.

Good points Termoil,

You're right that Energy is the ultimate unit of exchange, but up until recently, Energy has been too cheap and too plentiful to have had the necessary "scarcity" factor.

eg. We still sell our Uranium energy exports for about half the value ($/GWh) of our coal exports at the moment... (I suspect this will change!)

And I'm now trying to figure out the Rudd govt's new "Resource Rent Super-Tax". I was listening to an analyst on the radio today saying that the main impact is on Oil and Gas producers (because the deductibility of existing State Royalty payments has an uneven effect on different producers). So is this really some type of inefficient Carbon Tax in disguise, now that the ETS is on ice for the foreseeable future?

;-)

At the very least the govt. seems to be cashing in on Peak Oil without admitting that there is a problem or doing anything constructive about it.

I'd like to see Superannuation money directed into building Renewables infrastructure, but there's faint hope of that if Canberra won't even contemplate that Business as Usual is under threat.

There is nothing stopping super funds investing in renewables right now. The problem is ROI doesn't stack up but I think that will change when state govts in particular work out that gross feed in tarrifs are an easier way to get private investment to build generating capacity. NSW is going with a GFT soon, not becuase they are all green and fuzzy all of a sudden but becasue the state is broke, cannot sell or open up the elctricity industry becasue of union disquiet, but need to build new capaicty quicksmart or continue to import peak power from Victoria at the same rate as the GFT anyway. If it stacks up financially over the long term investment period that super funds typically can look at, then there is no reason why super funds won't pile in pretty quickly and becasue bigger is always better, you will see new renewables investment vehicles popping up. Hey that gives me a great idea for my super fund....

Interesting.

More money into the housing market to delay the inevitable "Pop".

Then where would we be?

No pension.

Of course Wall St. will play fair with our pension funds. They always have.

Haven't they.

Souls of sober propriety.

If you believe that then boy have I got a deal for you. A very fast bicycle for sale.

If you passed a law allowing this, the Oz stock market would collapse immediately as millions rushed to withdraw money and pay off their vast mortgages. The nett effect would be a total destruction of most people's savings.

Agreed. Superannuation needs to be invested in productive capaicty not consumption.

I am in my early 30s, thus won't receive my superannuation for some decades to come. Based on where I think we are heading (a contracting economy), I don't believe that my superannuation will be worth that much, either in $$ terms/purchasing power by the time that I could access it, whereas it could be very useful in accelerating the rate at which I could get rid of my mortgage in the intervening period.

Maybe I didn't make it clear enough in the post, but in this proposal you would not be able to 'access' your superannuation, rather just invest it as an offset to your mortgage. Once the mortgage was paid off, or at any other time, you could switch it back to another investment option. In the transition I imagine that it will have a big impact on the ASX in the short-medium term, but over time this would level out. To minimise this impact criteria such as only allowing a certain percentage of the mortgage to be offset and perhaps a qualifying criteria in time (eg. have held mortgage for 2 years) may be required. The value of the ASX will in my view decline anyway over the long term, so the real impact is that we are bringing this date forward, but in doing so reducing the systemic risk to our financial system, and giving superannuation investors a broader choice as to how to invest. I know in my super fund, I don't think that any of the available options will do particularly well in a contracting economy.

You may have noted in the introductory paragraph I mentioned that this is 'part of a plan.' Another part of the plan, which some of the other comments suggest, is to build the infrastructure required in a shrinking economy with less energy available and provide the training necessary for all of those skillsets we will need (or have lost) as the economy changes.

Cameron Leckie

Cameron, you can always self manage your superannuation and there are many funds out there which give you a big say in what your super is invested in. Too many people take no responsibility for their super because it is percieved as being too distant in time and locked up. I only have a very small amount of super but I self manage it, which makes me far more interested in what it is doing and where it is invested. Consequently, I did rather well out of the GFC because I could act against the prevailing "expert opinion" who wailed loudly after the event that "nobody could have seen it it coming".

As a trustee I have an obligation to my older self to invest in the interests of that person. My present self has the capacity to pay for his own housing needs and if he doesn't like the price, he can make other arrangements. But my older self won't necessarily have that luxury. It doesn't necessarily stop me from investing in areas of mutual benefit to both of my selves, just as long as old self is not robbed by his younger persona.

Not wanting to shoot holes in your plan, but I have worked in real estate and mortgage broking long enough to know that the savings made from offsetting won't be used to pay down the mortgage any faster. The savings will be spent by most people (not necessarily yourself) on bigger houses, flasher cars, more OS holidays etc. Tnhsi would effectively be robbing older self of teh benefits and as you point out, most people don't beleive that super will be there and therefore want to gain the benefits now.

My advice if you are struggling under the weight of a huge mortgage is to sell you house and move to soemthing you can comfortably afford, be that a renter, a regional area or a caravan park. Then if you ahve surplus funds, save it in bank account unitl you have enough money to pay cash for the house you want. I know, I know.....much to radical an idea.

Thanks Termoil,

firstly, from the personal side I have downsized my home/mortgage, have significant equity in the home, am making significant additional repayments and am not too concerned personally about my ability to repay my mortgage in a period of time significantly less than the term of the loan. What I am concerned about however is the macro level issues that are discussed here regularly. In my view, the Aussie property market is likely to become a major issue sooner than the general impact of PO, although in the end many of these issues are of course related.

The context for this proposal is a general acknowledgment that BAU is dead and buried, and that contraction rather than growth is the future. Whilst we will no doubt come to that view at some point, I don't see that occurring anytime soon. As a result the chances of implementing this plan are virtually zero. But when viewed in this context, I am sure that banks would rather this option as opposed to foreclosures/bank failures and that most home owners would not be irresponsible, although if implemented the way I propose, the only irresponsibility that could be exercised is that they might only make the minimum repayments.

Not having worked in real estate etc, do you see any other ways that we can manage the Aussie debt bubble when it goes pop (or hopefully preventing it from going pop)?

The only way I can see is to return to credit controls restricting banks from lending for consumer credit. Housing loans should never be more than 80% Loan to valuation ratio, car loans no more than 60%, and interest free deals should be totally banned. Credit card limits should only be allowed to the extent that you have money on deposit in the bank. Won't be popular of course but these are the sort of measures that Greeks are about to experience and we would be well advised to adopt them voluntarily so that we never have to be shackled with them by our foreign creditors.

The other thing that government should consider is changing the tax treatment of family homes. I think you could certainly introduce a tax on capital gain from sale of a house where the gain is well outside the CPI over the ownership period. To keep it simple, no other deductions or expenses should be taken into account, just the difference, with an appropriate rate then applied to that a amount, paid on settlement of the property. You could call it a deffered land tax and it could possibly be used to abolish stamp duty.

I believe that this measure, along with the credit restrictions above would go along way to reducing personal indebtedness. People hate paying tax they would rather sell for less, knowing that the buyer will get the benefit, rather than givng the profit to the government. It would also sharpen the minds of bank managers when they are calculating the quantum of realisable value of a persons collateral when considering lending them more money. Wouldn't be popular but economically responsible.

While I agree that all of the measures you suggest would reduce the level of indebtedness, the problem I see is time. My assessment is that we have no more than a couple of years to significantly reduce debt levels. If we haven't done so by then, we will be in the same position as the US is now re its housing market, with falling prices, rising defaults/foreclosures and at some point bank failures. To avoid this requires big responses soon.

I am not as pessimistic about Australia's position but the trend of ever eincreasing house prices with respect to average incomes is clearly unsustainable. However, we must remember that about half of Oz housing stock is not mortgaged and so the owners won't be affected at all by a price crash. They will just keep living in their homes. Many mortgages, like yours, are also very low compared to the book value, so a price crash of even 50% would still give your lenders plenty of collateral. It is the first home buyers who have leveraged nothing but their incomes and a fist full of government handouts into large oversized homes with all the trimmings that will be affected most. Losing their McMansions may be the best lesson that life ever teaches them, and will be the signal to the house building and development industry to build more appropriate product.

We also have some other econmic advantages that few other countries have. First is our low levels of public debt. We also have high interest rates that can be lowered pretty quickly again if necessary. We have a mining industry feeding the big gorilla in our neighbourhood that seems to ahve an insatiable appetite; we have a large fund of superannuation, as you have pointed out, which actually balances our private debt somewhat; we have an surplus of coal, gas and uranium which we can export (but no forever); and just for good measure, the drought seems to have broken this year which will boost ag production ( although I expect the long term trend to reassert itself in the nex few years). Our banks also haven't been as reckless as US and European banks. We started to see a bit of no and lo doc lending but it was choked off before it really made much impact and the lenders did require hefty deposits for thsoe types of loans.

So while I think we should be concerned with the culture of large personal debt being used to fund lifestyle, overall I think Australia is in better shape than some other countries. The stupid among us who have borrowed too much money and spent it on consumption deserve to be reigned in and I think Mr Market will take care of that. In many ways we actually need the crash to happen in the next few years to give us all a wake up call about learning sustainable living practices.

Not sure if this has a bearing on your argument... but the extension of Liebigs Law of the Minimum is that the "organism" that survives is the one that out competes others for the limiting "factor", or otherwise uses it most "efficiently"... so long as other factors do not become limiting.