| The Net Hubbert Curve: What Does It Mean? | The Oil Drum: Net Energy | What Does "Peak Oil” Mean to You? |

REVIEW: A Preliminary Investigation of Energy Return on Energy Investment for Global Oil and Gas Production

Posted by David Murphy on July 28, 2009 - 9:20am in The Oil Drum: Net Energy

This post reviews a paper by Nate Gagnon, Charles Hall and Lysle Brinker titled: “A Preliminary Investigation of Energy Return on Energy Investment for Global Oil and Gas Production,” published recently in the peer-reviewed journal Energies. The lead author was my colleague for two years at SUNY-ESF and the second author is currently my Ph.D. advisor and has published numerous guest posts here on The Oil Drum. See here for a list of previous posts relating to work by Dr. Charles Hall, and here to download a full-text PDF of this paper.

EROI of Global Oil and Gas Production

ABSTRACT: Economies are fueled by energy produced in excess of the amount required to drive the energy production process. Therefore any successful society’s energy resources must be both abundant and exploitable with a high ratio of energy return on energy invested (EROI). Unfortunately most of the data kept on costs of oil and gas operations are in monetary, not energy, terms. Fortunately we can convert monetary values into approximate energy values by deriving energy intensities for monetary transactions from those few nations that keep both sets of data. We provide a preliminary assessment of EROI for the world’s most important fuels, oil and gas, based on time series of global production and estimates of energy inputs derived from monetary expenditures for all publicly traded oil and gas companies and estimates of energy intensities of those expenditures. We estimate that EROI at the wellhead was roughly 26:1 in 1992, increased to 35:1 in 1999, and then decreased to 18:1 in 2006. These trends imply that global supplies of petroleum available to do economic work are considerably less than estimates of gross reserves and that EROI is declining over time and with increased annual drilling levels. Our global estimates of EROI have a pattern similar to, but somewhat higher than, the United States, which has better data on energy costs but a more depleted resource base.

As the title of this article indicates, the authors estimate the energy return on investment (EROI) for global oil and gas “production.” The first thing to note is that the calculation is actually for the EROI of global exploration, development, and production (commonly called E+P or “upstream”) – a much more comprehensive estimate than just production. They estimate that the EROI of global oil and gas E+P in 2006 was roughly 18:1 (above figure). To establish these estimates the authors rely on three datasets: a) the Energy and Information Administration (EIA), and b) the British equivalent of the EIA, and 3) John S. Herold, Inc., a privately managed database consisting of data on total "upstream" costs (i.e. all costs up to the point the oil comes out of the ground) of publicly traded energy firms around the world.

The crux of their analysis depends on the conversion of money numbers into energy numbers. Since global energy costs are not maintained in energy units, but in economic units only, they derived an energy intensity value for each dollar spent in the energy industry. These numbers, derived independently for the energy industries within the U.S. and England, were about the same: roughly 20 MJ per dollar for both countries in 2005. The energy intensity numbers were multiplied by the estimates of money spent to get rough estimates of energy cost of energy production.

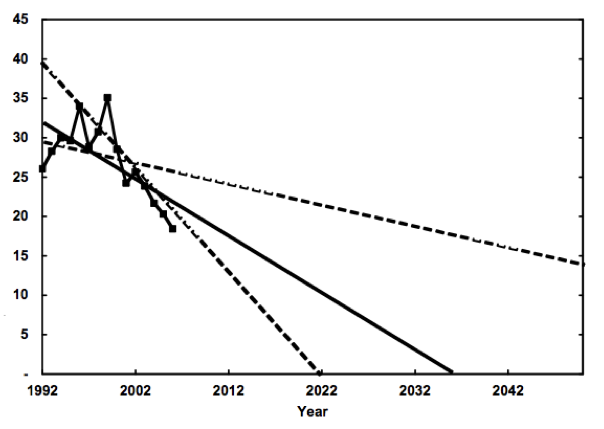

In addition to estimating the current upstream EROI of global oil and gas, they extrapolated three trends from their time-series estimates of EROI and show global EROI declining to 1:1 between either 2022 or sometime in the very distant future, with the best estimate being about three decades away. To do this, the authors forecast linearly the historic trend of global EROI, which is, as the authors acknowledge, a forecasting methodology fraught with problems. Nonetheless, the forecasts provide a thought-provoking view of what may happen if society continues along a "business as usual" path.

Linear extrapolations of historic EROI trends

The authors also attempt to answer the question “What are the reasons for the decline in EROI estimates, especially since 1999?” They offer two solutions: 1) technology is seemingly being outpaced by depletion, and/or 2) increasing the annual drilling rate decreases the drilling efficiency. The drilling intensity decreased during the early and mid 1990s when EROI was actually increasing, but has increased since 1999. This has led to a sharp decrease in drilling efficiency (barrels found/produced per well drilled). Their best guess is that both options are operational, a contention with which I am inclined to agree. Improved technology is increasingly used in E+P activities, including, of course, drilling. So the fact that the EROI of E+P has declined over the past 10 years indicates that easier-to-access resources, i.e. high EROI resources, are increasingly rare (if found at all), because even with increasing technology and drilling efforts, we are witnessing declining EROI.

Lastly, the authors address the major assumptions they have made while performing their analysis. This is a crucial step in most large numerical analyses and, unfortunately, one that is often overlooked. The assumptions are:

1) “changes in monetary expenditures indicate changes in energy expenditures.”

2) “energy intensities are the same the world over.”

3) “We assume a constant energy intensity in the US after 2002, and constant energy intensity in the UK prior to 1998 because there are no data available for those time periods.”

The second assumption is the most problematic from a scientific perspective because upstream costs vary widely from deep offshore, to tar sands, to shallow offshore, to onshore drilling. The application of energy intensity numbers, which are derived directly from cost data, from one area of the world to the rest of the world is potentially flawed. But in reality, this is a reflection of one of the conclusions the authors derive from their work, i.e. WE NEED MORE/BETTER DATA. The fact of the matter is that although the authors had access to three extensive data sets, two public and one private, they were still able to access data for only 40% of the world’s oil production. Furthermore, many of the data sets that are unavailable to public scrutiny are the most important, i.e. that from Saudi Arabia, Russia, Iran, and every other Nationalized Oil Company.

Some interesting quotes from the manuscript:

This [Herold] data base accounted for about 40% of the oil produced in the world in 2006.

What is clear in the Herold data base is that the amount of oil and gas produced per dollar spent between 1999 and 2006 shows a decline. In 1999 the industry produced about one tenth of a barrel of oil equivalent (boe) per 2005 dollar spent globally in exploration, development and production. By 2006 that number had declined to approximately 50%.

It is important to note that the data we used in this analysis group oil and natural gas production together, since they are commonly produced from the same reservoirs. However, the effort required to pump oil out of the ground is generally much greater than that required to bring natural gas to the surface. We therefore expect that the true EROI of oil is somewhat lower than our results suggest, while that of conventional natural gas is higher.

REVIEW: A Preliminary Investigation of Energy Return on Energy Investment for Global Oil and Gas Production

PDF version

60 comments

REVIEW: A Preliminary Investigation of Energy Return on Energy Investment for Global Oil and Gas Production

PDF version

60 comments

Contact

- theoildrumeroi at gmail dot com

Personnel

Archives

- October 2010 (1)

- September 2010 (1)

- August 2010 (1)

- July 2010 (1)

- June 2010 (1)

- April 2010 (1)

- March 2010 (2)

- January 2010 (1)

- July 2009 (1)

- June 2009 (1)

- May 2009 (2)

- April 2009 (1)

- March 2009 (1)

- February 2009 (1)

- January 2009 (2)

- December 2008 (1)

- November 2008 (1)

License

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.

I applaud Dr. Hall's continuing (solo?) efforts at sussing out our biophysical energy balance sheet. His team has little real energy data to work with and I know how frustrating that can be - this work is monumentally important because it tells us how much/quickly we have to change the demand side.

I have numerous comments on this paper, in no particular order:

1)though I realize data is limited, I think it is potentially very misleading to use energy intensity (MJ per $) based on GDP to calculate energy costs. First of all, GDP is increasingly financial (40% of corporate profits this decade are from financial/insurance/real estate companies). So if there is a future downward revision of historical GDP (which I expect), your EROI numbers are going to be in % fashion overstated.

2)Using your method of MJ per $ ends up basically using oil price itself as explanatory variable. It ignores historical energy costs of energy infrastructure (drills, pipelines, etc.) and only looks at marginal costs. Ave oil price per year alone explains 82% of that years EROI (R^2). What if we eliminated all oil and gas infrastructure but retained the worlds oil fields/resources. What would be the energy from scratch needed to procure a 'new' 84 mbpd? THAT would be a true EROI -what you are portraying is a 'marginal EROI' and assuming no energy depreciation for built assets. A better way might be to amortize the emergy cost of oil infrastructure. Matt Simmons suggests our rig fleet is 90% in need of replacement - if true we are living on historical high energy gain more than we know...

3)It is true that when demand/economy drops that EROI goes up (because only the best/cheapest areas are drilled, on average). But this is misleading as well, because society cares about aggregate marginal energy gain, not EROI - we care about how much energy return we get from our available energy that is invested in the current time frame. So higher EROI on a smaller universe of properties might lead to smaller overall 'gain'.

We really need more people to join Dr. Halls effort in calculating biophysical costs. It is becoming more widely understood that the difference between 1 trillion dollars and 100 trillion dollars is merely paper, ink, and some unquantifiable deterioration in trust. The next logical and important question people should ask is: how much does it cost to procure and process the resources we want and need denominated in the resources themselves. It really goes beyond energy, though energy is the key.

I asked Dr. Hall what his thoughts were on Nate's comment. This was his response:

Nate, you make excellent points. We need the DOE and IEA economists to pull together the resources and get the best data available assembled. You'd hope by this time some of them would be looking more seriously at the physical systems problem with continually running up our economic overhead costs and running down our resource quality.

You're right to be cautious about using MJ per $ for the physical economy energy intensity. The financial system did indeed just go through a major inflation and deflation of misinformation about the physical world. The data I have is hopeful about the validity of the measure none the less. Maybe I'll get to update my curves and see if there's a new bump that would show whether that effect will turn up or not.

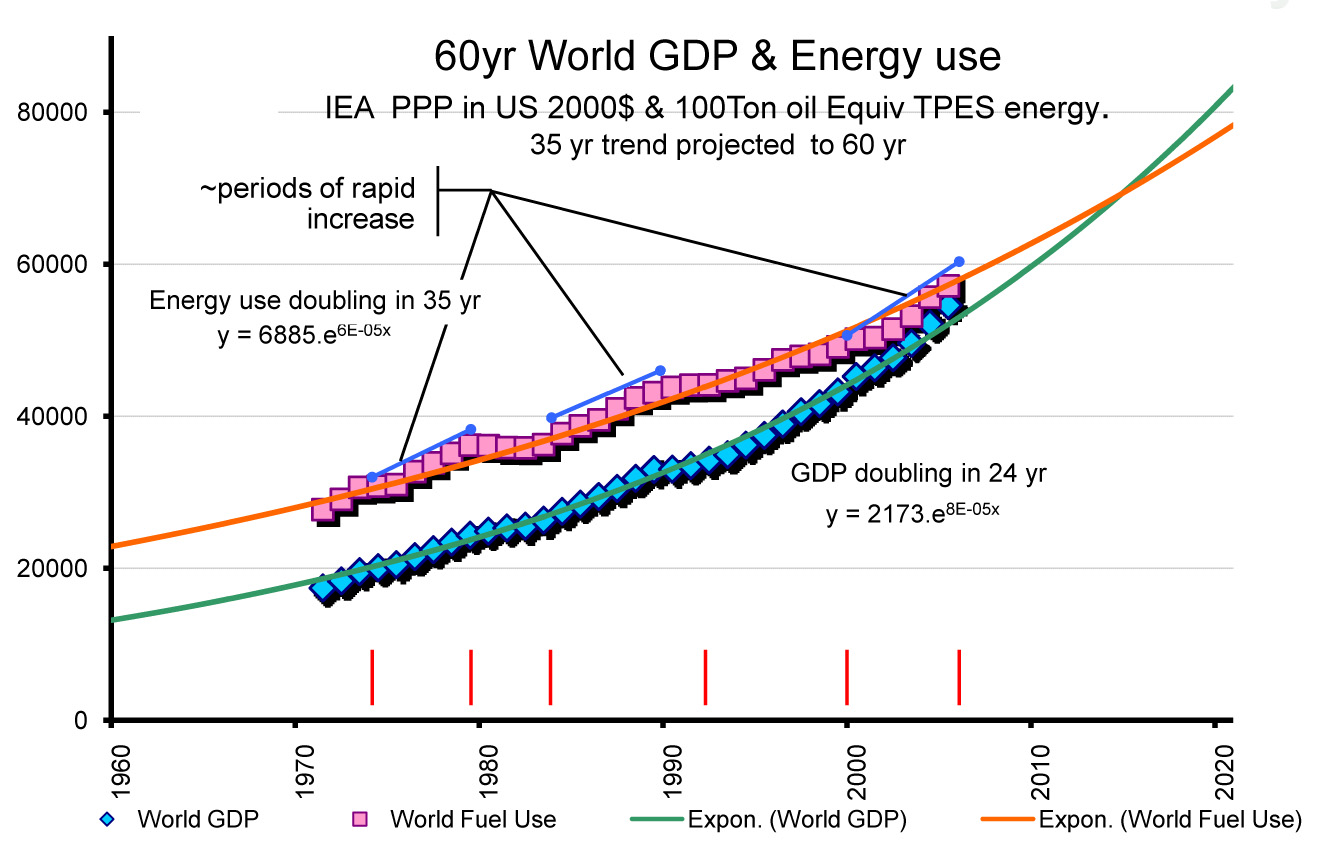

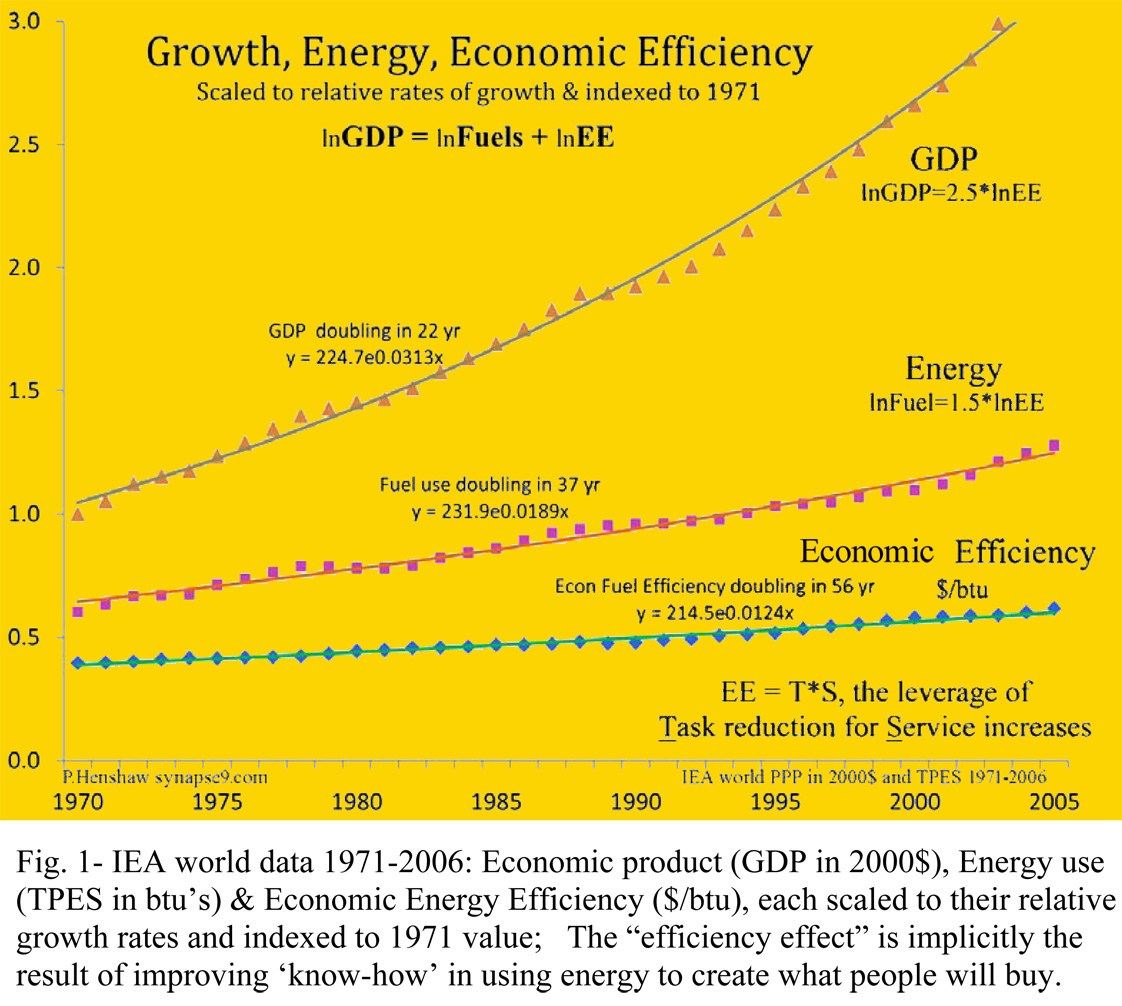

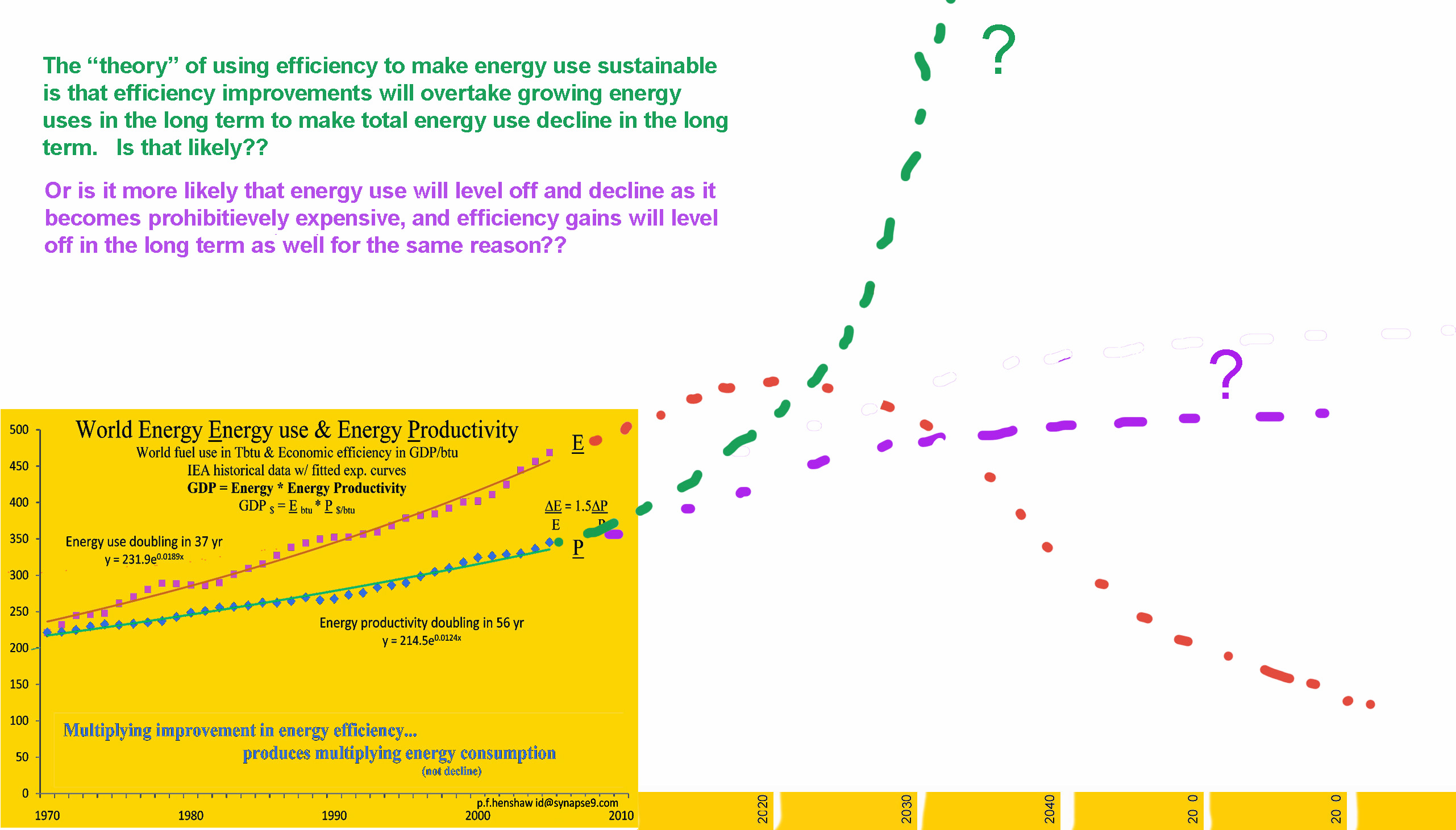

What I found in looking at the IEA's most detailed world product and fuel use accounts was miraculously smooth exponentials for both the world GDP and fuel consumption rates, and so for their ratio too. What I'm saying is that the fantastic money supply bubble of the past decade does not seem to appear in that as a distortion. The curves show methodically regular slow improvement in total economic efficiency. In my view you don't get regular exponential curves like that unless the growing system is acting as a whole, efficiently allocating its resources, and pushing steadily against its limits. So, I think it's possible that the economists actually succeeded in defining "real product" and the portion of economic activity that takes energy to produce, just maybe.

I labeled the periods of rapid energy use increase since the energy intensity curve (see www.synapse9.com/issues/World-eff_grow.pdf for it) show slowing improvement during the periods of rapid energy use increase and accelerating improvement in the periods of slowing energy use growth.

pfenshaw,

As oil and coal are replaced by nuclear and renewable mainly electric power we should see an addition reduction in energy intensity on a MJ basis. I know EIA uses a conversion factor to increase electric energy to a BOE basis, but there should be additional reductions in intensity because of the higher efficiency of electrical energy use, for example heat pumps and EV's.

The other factor will be improved efficiency with higher energy prices, as we had in 1979-85, and will probably have now, especially if oil prices remain high.

Neil,

Ah yes.... That's what *everyone* says is supposed to happen, that technology is *supposed* to be able to bend the economic efficiency trend to break the pattern. What is a popular presumption is not necessarily good science though. The people promoting efficiency as a solution omit the growth effect of efficiency gains that has the macro-economic rebound effect of increasing the uses of things faster than the efficiency of use increases... Also missing from that hopeful (self-promoting) idea is the historical fact that the systemization of the world economy has gone along with vigorous competition for improving efficiency all along. Efficiency improvement has never been neglected, but has instead been constantly pushing the limits of what was possible all along.

The economies have long been intensely competitive for efficiency, and it shows very clearly in the long term gradual improvement in efficiency, steadily, a bit slower rate than the equally smooth long term trend of increasing energy use. The reason for that seems to be that energy is such a very easily traded and substituted and valuable commodity. It's the universal resource, after all, serving for technology as money does for human choices. Globalization has always gone along with everyone's vigorous effort to beat the competition in delivering equal value for less cost, so squeezing out any inefficiencies people could find. That is the real reason money is such a very good whole system measure of energy use, well, if you understand the idea and check it out enough to feel comfortable with it.

What is implied by the strategy to use energy efficiency to achieve sustainability is that the future efficiency (=1/intensity) and the total energy use curves (shown below) will cross paths and efficiency improvement will accelerate so much faster that energy uses can continue to multiply as the total energy used declines, in the long term. Is that likely?? That's the scenario in the green dotted line projecting endless exponential improvement in efficiency... That's the scenario *everyone* is counting on to solve global warming and everything else.

Which future do you think is more likely?

"What is implied by the strategy to use energy efficiency to achieve sustainability is that the future efficiency (=1/intensity) and the total energy use curves (shown below) will cross paths and efficiency improvement will accelerate so much faster that energy uses can continue to multiply as the total energy used declines, in the long term. Is that likely??"

I have never implied what you are suggesting, just that energy efficiency will continue to increase at 1-2% per year. I expect energy use to increase( in terms of kWh not MJ) as more nuclear and renewable energy displaces FF.

The costs of these are based on the energy efficiency of the economy( energy/$GDP) so the capital costs will decline over time and renewable energy will become cheaper as FF become more expensive.

The two graphs you have are measuring totally different things and have different units so "crossing over " has no meaning. The per capita energy use has not increased in 30 years in the US but GDP/capita has and will continue to increase whatever the changes in total energy use or population in the future. I think population will stabilize and energy use continue to increase until we use 5-10% of wind and solar energy resources. That's a very long way off.

I see that Nate and I are sneaking in here before the article is posted, but I want to make a point as well. As far as I can tell, you are talking about only the energy to produce oil. It still needs to be refined. That will consume another 1/10th of the energy value of the barrel of oil (EROI of refining = 10/1). I know this number from my refinery days, but I have also provided a reference in the literature to back that up (I think it was to Nate). That 10/1 is also declining as we meet ever higher environmental standards in the refineries.

Robert, how does the increase in percentages of heavy sour crude factor into the amount of refining energy required?

Robert,

Dr. Hall and I have looked at this very issue and published a paper that makes an attempt at including "downstream" costs into EROI estimates. We found that once all of the downstream costs are included, that our energy sources must provide energy at an EROI of around 3:1 to maintain current society. See here for a full text PDF of this paper.

Don't they just burn whatever part of the oil barrel they can't sell? There's a lot of confusion on what EROI does or doesn't imply. Poor EROI means that ethanol or oil shales don't become much more profitable as the price of oil increases. But given the value of gasoline to our car crazy culture, oil can be pumped at negative EROI if the input energy is electricity or concentrating solar for heat or burning garbage or some other less desireable form of energy. Saying BAU can't exist without some minimum EROI is a fallacy. Not as long as there is a star 93 million miles away. Price of energy will go up, sure. Civilization collapse no.

Hi Robert,

If oil were a small part of the US energy mix (the way ethanol is today) then I would agree with you that we could survive oil going below unity EROI. But oil is 41% of our total energy supply. Nothing else is close to the size of oil. Not coal, or nat gas, or nuclear or any renewable.

So the question goes back to how fast renewables can scale. I am looking forward to Jeff Vail's next post on that subject.

Given it'll take decades to exhaust fossil fuels and France scaled nuclear up to 80% of their electric supply from nearly nothing in 25 years...

Jon,

While oil is >40% of energy in US( 42EJ out of 95EJ), we don't have to scale present nuclear and renewable(5EJ) to 47EJ, but enough to replace oil use. For cars and light trucks that would be replacing each gallon of gasoline and diesel ( 140MJ plus refining energy use and losses of 40MJ) with 5- 10kWh(18-36MJ) of electrical energy, or 4-8.5EJ.

If this is over a 20 year period this would require <0.4EJ/year or for nuclear and renewable energy to increase by 7% per year. It would seem possible for either nuclear or wind energy to scale at this rate and certainly possible for both together with smaller increases in hydro and solar to provide this amount of energy. A greater limitation may be replacing most ICE vehicles with EV in 20 years, again not an impossible task give average life of ICE vehicles.

If oil availability only declines by 50% in the next 20 years that gives a longer time for ICE vehicle replacement.

What are the consequences if these energy resources and EV's can only replace half of the oil declines? Gasoline rationing, much higher CAFE standards, and/or more ethanol not exactly the end of civilization as we know it.

Robert2734, do you think their is some RULE that says civilization can't collapse. If so you need to read Tainter's Collapse of Complex Civilizations. What is happening in the world today has happened before, its just that we found a different fuel for the rise of our complexity so we have more complexity than any civilization before us. Which leads to the famous maxim "The Bigger they are the Harder they Fall".

In the end it is not Peak Oil but Peak Everything - per wiki "In Tainter's view, while invasions, crop failures, disease or environmental degradation may be the apparent causes of societal collapse, the ultimate cause is diminishing returns on investments in social complexity (in contrast, Jared Diamond's 2004 book, Collapse: How Societies Choose to Fail or Succeed, focuses on environmental mismanagement as a cause of collapse). Finally, Tainter musters modern statistics to show that marginal returns on investments in energy, education and technological innovation are diminishing today. The globalised modern world is subject to many of the same stresses that brought older societies to ruin." http://en.wikipedia.org/wiki/Joseph_Tainter

Bah, Tainter, Diamond, Cassandra's of history as a mirror. Except it isn't a mirror.

Do you have a source for that Robert? The most recent data I've come across points to an EROEI of 5-6:1 for refining.

Great to see this topic gaining traction in the mainstream energy journals. I also understand and agree with the 'tweaks' Nate and Robert have suggested. Keep up the good work in this important area, Dr. Hall.

One main question:

- Does the EROEI trend need to be a straight line? Could it not also be a curve related to a function?

Since the easy to obtain fuel has been accessed first, couldn't the rate of additional energy needed to extract oil and gas increase once past the EROEI 'peak', the curve-fitting of which would more closely resemble an inverted parabolic curve (as one example)?

Will,

I also believe that a decline in EROI will have more of an exponential decline shape rather than a linear shape (i.e. resembling a Hubbert curve), as the high EROI sources (conventional oil) will be lost very quickly but numerous very low EROI sources (corn ethanol, tar sands, etc.) will persist for a while.

So if I understand you correctly, the oil/gas EROEI decline (different from production decline) could be exponential, while some low EROEI sources remain, leaving a 'tail'. This would seem to imply a sigmoid function (or the latter half of a logistics curve, as you mention).

If I understand the paper correctly, as we descend past an EROEI of 3:1, we would (incrementally) lose our ability to maintain BAU, though high prices before then would likely already have had some impact, so there may not be a sharp defining line.

Will,

Yes, that is more or less how "I" see the decline of EROI taking place - the question is which slope is correct? Slopes -1 and -0.5 imply markedly different energy futures for society.

The curves can also go up, which can be seen in the papers own data from 1992-2000 when EROEI goes from about 25-35.

Goes down then new technology or discoveries come along and the curves go up.

There are also multiple EROEI's being blended.

Also, the collapse scenarios do not consider shifts like nuclear power for commercial shipping.

About 9% of current oil is used for commercial shipping. There have been over 600 nuclear powered military ships. The US Navy is getting budget for nuclear support and troop transport ships and smaller ships. Indian navy started to go nuclear.

Nuclear shipping has economics that work as shown in the link.

http://nextbigfuture.com/2009/07/nuclear-power-for-commercial-shipping.html

http://nextbigfuture.com/2009/07/commercial-shipping-uses-9-of-world-oil...

Combined with new refining efficiency to make more gasoline and less bunker fuel

http://nextbigfuture.com/2009/07/rive-technology-working-to-increase-oil...

So Business As Usual can change but the direction it goes may not be the fireside/local/subsistence.

The trick is to determine if technology is increasing EROI or just lowering the rate of decline. Here we can see natural gas wells initial yearly production. And it is falling pretty steadily. As the number of shale gas wells grew, the downward trend slowed. However it did not reverse back up to 1995 levels. And there is tremendous resource usage in those long horizontal completions.

This chart of nat gas recovered per 1k feet of well drilled is still plummeting. So we might be getting the gas faster, but expending more steel and diesel to do that. It is hard to look at this chart and feel confident saying EROI is going up. (click for larger view)

http://nextbigfuture.com/2009/07/update-on-oilsands-bakken-bakken-three....

Multistage fracturing is lowering costs and increasing EROI where it is being applied.

Packers Plus's multistage fracturing drilling technology has opened up major new supply basins in Canada and the United States, potentially unlocking hundreds of trillions of cubic feet of new gas reserves in places like Horn River, Louisiana, Pennsylvania and even Quebec.

Three years ago, Packers could insert a half-dozen or so "stages" into a single well. As horizontal wells got longer, that number has grown to 22, and Themig says new advancements will allow virtually "unlimited" stages in a single well. That, in turn, has resulted in an order-of-magnitude higher production for a basic well that costs only about twice as much to drill.

The average conventional gas well in Western Canada produces about 250,000 cubic feet of gas a day. EnCana Corp. CEO Randy Eresman said in releasing the company's second-quarter results this week that its latest Horn River wells that use the multistage technology are coming on at initial rates of up to 11 million cubic feet per day.

Brigham Exploration Company reports continuing reductions in drilling and completion costs. The company is now using up to 24 stages in long laterals. The Strobeck 27-34 in Mountrail County, North Dakota flowed 1,788 bbl/day of crude oil and 1.2 million cubic feet/day of natural gas. The well, completed in the Three Forks, had 18 effective fracture stages. The well also confirmed core results from the Anderson 28-33 which showed that both the upper Three Forks and the middle Bakken were oil saturated. Completed well cost was $3.9 million, 33% less than similar wells drilled in 2008.

Suncor expects its [oilsand] capital costs to decline by as much as 20 per cent from the peak of 2008, but oilsand growth is far lower until prices go back up.

Kelso, of Whiting Petroleum, said his company's drilling activity shows that Three Forks-Sanish likely is a separate formation. He said core samples taken from the Bakken and Three Forks show more hydrocarbons in the latter. Three-Forks Sanish could double the amount of oil in the Bakken area.

Hi Will,

Graphing costs we get increases that could be exponential (click for larger view).

I put in trend lines both ways for Canadian natural gas so they could be compared. The linear fit looks better for natural gas, but clearly oil (graphed in the main article) is not behaving the same way.

Along the bottom are two lines, one at an EROI of 5 and the other at an EROI of 2.5. Somewhere between those values it will take as much energy to produce, transport, and use the energy as we get out of the energy and the natural gas will no longer be an energy source.

Even with an exponential decline, it does not take that long to cross the minimum boundary.

So we're really about ten years past "real" peak. And Hirsch said we need twenty years to prepare for peak. So we're about thirty years behind schedule.

Great.

By the way, does this analysis include tar sands, etc, or just conventional oil?

I'd like to jump in at this point.

It seems to me that the EROI function is composed of two components: one technological which increases energy returns with a decreasing marginal return (similar to an inverted 'learning curve') the other physical due to the greater energy required as resources are depleted.

Combining these two components leads to the peaking EROI function that Hall et al proposed in their fantastic "Energy and Resource Quality: The Ecology of the Economic Process" This does not tell us whether or not the depletion component is linearly or exponentially decreasing, but overall the EROI function seems to decrease non linearly.

Another factor that is seldom recognised is the difference in capital/fuel requirements between non-renewable and renewable resources. Oil and other fossil fuels require little physical capital but fuel to operate - that's fine it's what they produce. Renewables are capital intensive and that capital has to flow through the rest of the economy first. That could cause big problems for the economy in a transition away from fossil fuels.

I've been producing some models around this and will share results as I have them.

Mik

Mik,

While renewable energy is capital intensive, the economy as a whole has a much lower energy intensity (6-7MJ/$GDP) compared with the oil and gas industry (20MJ/$expenditure). The energy used in manufacturing say wind turbines( based on Vestas CO2 disclosures) is a small part of the embedded capital cost, most is from the energy used by the economy(profit, labor, financing).

Furthermore nuclear and renewables such as wind and solar produce kWh's which have a much lower energy losses during distribution to end consumers, and a higher energy value than the MJ content of NG or coal used to generate electricity.

For these reasons for renewable energy we need to know the energy saved on energy invested, for example a wind turbine producing 1,000kWh will have 3,600 MJ energy content, but save burning 10,000MJ of coal or 7,200MJ of NG.

Regarding up-front investment, it seems like it varies.

I think with oil it depends on whether you are producing oil from wells that have already been drilled, or from new wells. With respect to new wells, it depends on whether all of the E+P is ahead of you, or if the wells are simply infill wells to offset depletion.

With natural gas, ramping up production can be done by drilling a lot of new wells, and doing a lot of fracing. The problem is that this is not really sufficient in order for the natural gas to really be useful. It seems as though to really be useful, the system really needs a whole lot of new infrastructure--pipelines, storage, and users for the gas produced--either new furnaces using natural gas or cars using natural gas. We have already seen what happens to price when more natural gas is produced than the system can handle.

With wind turbines, it is not just the wind turbines that are needed, but the transmission line upgrades, and probably energy storage. If energy storage isn't possible, then one needs some other approach for handling variability.

So I don't think the model is quite as simple as non-renewable / renewable.

30 years "behind schedule" only accounts for the technology transition problem, as if energy sources were "plug and play" and there was general infrastructure problem, like where we built the cities and how we sprawled the suburbs, and how we centered all our government and financial institutions around ever more rapid expanding use of cheap energy,... and things.

If you think of steering things, say like in canoeing or skiing, where the only really safe turn is the one you start at the very earliest possible time, we might well have needed to start the turn toward sustainability about 100 years ago, and have now probably lost control of much of what is now about to happen as a result.

pfhenshaw,

You may be overestimating the infrastructure problem as well as the technology transition problem.

Replacing ICE vehicles with EV's, is really a "plug and play" situation. We have the electrical fueling infrastructure in place, the off-peak capacity, transition fuels( coal and NG) until new "conventional technology"( nuclear and wind) is built.

We don't have to invest in new factories to produce EV cars, or new rail lines or new roads. We would require new investments in energy production, but we are investing in oil and gas now. We have to invest in building new vehicles but we are doing this anyway replacing in 15-40 years almost all ICE vehicles.

What if you no longer have asphalt as a low cost by-product of the fuel we use? What will roads get made of then? What if the cost of travel goes up as competition for limited resources restricts energy use to all but essential business uses, and we only get our exceptionally wasteful systems to survive by stripping them to the bone? What if you still need exponentially growing energy use to maintain basic economic stability in a growth driven competitive world?

Sure, it's hard to predict a lot of things, mainly proving how hard it is to imagine what could happen. For example, global warming is assumed to be the last big problem that nature will throw at us as we continually multiply our impacts and rest control of ever more of the planet's energy and resource flows for our purposes.

I have a good imagination, but not a good enough one to compete with people who count on "proof of concept" by failure to imagination what could go wrong. That is actually what we are all mostly doing with sustainability planning, really. I prefer to rely on certainties rather than on "wobbly predictions". One can be quite certain, for example, that pushing any system to change scale repeatedly will exceed the functional bounds of its parts, whether I know what the parts are or not. Not acknowledging that has left us in a jam.

What if you no longer have asphalt as a low cost by-product of the fuel we use? What will roads get made of then?

As far as I remember all express-ways and interstates are made of concrete, that's the case in Australia, UK, Canada.

What if the cost of travel goes up as competition for limited resources restricts energy use to all but essential business uses, and we only get our exceptionally wasteful systems to survive by stripping them to the bone?

The cost of travel is probably going to rise, it's cheaper now than in any time in the past, not a big issue as long as the cost of transport by rail and sea is very low. Costs go down with size and volume of goods transported.

Why would energy use be restricted? We are not running out of energy, just FF energy.

So change all the 'just in time' deliveries by planes with ship- and railtransport, right ?

Here's the reddit & digg links for this post (we appreciate your helping us spread our work around, both in this post and any of our other work...):

http://www.reddit.com/r/Economics/comments/95bg4/review_a_preliminary_in...

http://www.reddit.com/r/energy/comments/95bfm/review_a_preliminary_inves...

http://www.reddit.com/r/environment/comments/95bfo/review_a_preliminary_...

http://www.reddit.com/r/science/comments/95bfv/review_a_preliminary_inve...

http://www.reddit.com/r/collapse/comments/95bg0/review_a_preliminary_inv...

Find us on twitter:

http://twitter.com/theoildrum

http://friendfeed.com/theoildrum

Find us on facebook and linkedin as well:

http://www.facebook.com/group.php?gid=14778313964

http://www.linkedin.com/groups?gid=138274&trk=hb_side_g

Thanks again. Feel free to submit things yourself using the share this button on our articles as well to places like stumbleupon or other link farms yourself--we appreciate it!

There seems to be considerable enthusiasm in some circles for drilling of the coasts of Virginia, Northern California, and in other locations where there may be little oil or gas. What is the EROEI of a dry hole? I recall a bizarre situation during the 70's when stripper wells were subsidized in the US to the extent that monetary return trumped EROEI

Stripper wells still get very favorable tax treatment, but the Obama administration would like to change that.

If oil production were reduced because of such a tax change, it seems like the EROI calculation would change as well. Production used in the calculation would go down (upper limit 20%), but the investment numbers would remain essentially unchanged, implying a lower EROI.

All of these calculations are so long-term, it is hard for me to understand what should be matched against which other numbers.

David (et al) thanks very much for this. My main comment is related to time scales and flow scales. It is significant, I think, that the EROI peak (1999) more or less matches the $/bbl nadir (1998). By 1998, KSA was in great pain, having cut production so much to support price, they had to borrow money from UAE to keep their country running. What followed was the mega mergers and essentially the decimation of the global oil industry - but out of the ashes....

Main points in relation to time scale is that up to 20 years or more can pass between exploration expenditure and field development. Costs (financial and energy) can be spread over decades. The 1999 EROI high coincides with the N Sea peak - the fruit of 30 years investment reaching a peak and then going into decline.

On similar theme, the EROI distribution is VERY HEAVILY skewed. I'd guess that EROI on Ghawar is over 1000 - and that accounts for 5% of global production. And so there is likely to be a very large difference between the mean and the median EROI or the mode. It follows that linear fits to the data are likely inappropriate. When the very high EROI, very high flow rate oil from KSA starts to decline, the mean EROI will move rapidly towards median or mode where it will then stabilise. I think Will Stewart's chart describes this quite well.

That is a good point. Some readers may not remember that oil was at its relative lowest point about 1998 in terms of price. This is a chart from one of Euan's post's showing oil and other energy prices as a percent of GDP.

This is another chart, from one of Dave Murphy's posts, showing oil alone as a percent of GDP, and its inflation adjusted price.

'What is wrong with this picture'?

How can EROEI possibly go negative?

Eo/Ei=EROEI so as Ei--> infinity, EROEI goes to zero.

Somebody is laughing, I'm sure.

Hello Majorian,

If one narrowly restricts the ERoEI discussion boundaries to strictly math concepts or definitions: you are right--the math ratio ERoEI can't be less than zero.

But in the larger concept or bigger boundary of Life: negative ERoEI regularly leads to starvation. Imagine an old, half-blind, arthritic cheetah that can no longer reap a strongly positive ERoEI from it's earlier high-speed sprint for harvesting gazelles. It has to now chase much smaller/slower african game. If the old cheetah is mostly unsuccessful in attaining a positive ERoEI on this smaller prey: the cheetah is merely delaying the final day of reckoning as it is only burning off its fat and muscle energies faster than it can harvest, digest, and restock [a negative ERoEI].

The same applies to humans: I remember reading somewhere that celery [although tasty] takes more energy to chew and digest than the calories contained within the celery [again a negative ERoEI].

I picture the miles and miles of MRC horizontals, plus the ever expanding networks of rusting pipelines and other FF-infrastructure, as our increasing global energy reliance on 'aging steel celery'. This ongoing change to our 'FF diet' will lead to much starvation or worse, IMO.

If memory serves David Pimentel wrote about the negative energy output of celery and similar luxury foods during the 1970's. Dieting is easy - if one enjoys such foods.

That was a fallacy due to a mix-up of energy units - when a diet refers to calories it is in fact referring to kilocalories.

Celery is definitely a net positive energy supply, even if you grow it yourself. However, I still hate celery!

Do you have a link supporting your claim that celery provides a positive energy balance. Incidently having been a physics major before going to medical school, I am aware of the calorie kilocalorie convention. It is well established. I don't recall ever hearing anyone claim to be on a 1000 kilocalorie diet.

RalfW is correct. There are food calories and real calories.

As I mentioned I an aware of the historical and current use of the word Calorie. Is this necessarily relevant to celery? I met Pimentel at an energy meeting in Washington DC and briefly discussed my memory of this very issue from the time I first became aware of his work. He had politely responded to a snail mail question. I am still looking for the specific antique reference and the correspondence, thus far without success.

http://en.wikipedia.org/wiki/Calorie

use a source other than oil itself.

I presume you were trying to reply to Robert2734 above, and his comment about it being theoretically OK for oil to have a negative EROI.

It's worse than that, Gail.

This is from a stated PEER-REVIEWED published SCIENTIFIC article and they show a negative EROEI.

I should like to see the derivation of negative EROEI.

Jon Friese showed an exponential decline curve with asymptote of zero in which I assume manifests his embarrasment over the article diagram(you can get it from the Excel 'growth' function) which is on everybody's computer.

Either you know the hell you are talking about or you don't.

.. Either you can figure out what the hell they are trying to express, or you can't. Or you just don't.

an EROEI of less than 1:1 or 1/1 sure counts as 'negative' to me in all it's implications, even if it's not a 'Negative Number' mathmatically.

It's negative because you're losing your investment.

What if you need the oil to run big ag and are willing to use electrical energy produced by solar at a EROEI<1 because you like to eat.

It basically makes oil a energy carrier but it also gives you the form of energy that you need to survive. The sun isn't going away. Consider the energy difference as a cost. I guess the point is that all energy forms are not equal in their application or usefulness. Oil is definitely a very versatile form of energy and worth "paying" extra costs to get.

Don't get scope locked on the math it is only a modeling tool to help make real world decisions.

Yes, you can logically make that conclusion Porge but that is very unlikely to happen. Agricultural companies like AIG and Cargill are not in the oil business. They have to buy their oil. The oil companies are not going to produce oil at a loss, not for very long anyway. What you must look at, and indeed what every company looks at, whether they deal in agriculture or oil, is ROI not EROEI. And ROI can very definitely go negative. You can lose money.

So for your case to become fact, the oil companies would have to produce oil, getting their energy from mostly other sources like wind or solar. Then they would have to mark this oil up higher than their cost to produce it. Then the agricultural companies would have to pay dearly for that oil and in turn mark their food products up high enough to cover that cost.

Somehow I just don’t see that happening. However if it ever did then food prices would have to be enormously high. Our diet would change dramatically and most people would probably starve.

Ron P.

Enormously high or subsidized by the gubmint printing press.

We are talking about food here.

You absolutely will lose money but some things just should not be analyzed in terms of money.

The value of "money" is relative to the environment that surrounds it. Quality of life is the goal.

Porge,

You may have the upper hand debateing Darwinian today,which imo is not something that happens very often.

We could (somebody,it doesn't really matter who) manufacture synthetic diesel and gasoline and "eat " the energy losses if necessary in order to farm with our existing equipment.If the price goes high enough,coal,natural gas,or even wind or nuclear electricity could be used to make this necessary amount of fuel.

And even if diesel were twenty bucks per gallon,it would not run up the price of food nearly so much as one would assume because the farmer gets only a small portion of the food dollar,and liquid fuel is only a portion of his energy costs-the farm energy costs include lots of electricity and embedded energy such as is used to manufacture fertilizer and tractors ,etc.,plus a lot of electricity,mostly generated with coal,and a lot of natural gas,used to dry crops etc.

And while the farmers total energy costs are high,they are again only a portion of the farmers total costs.

Twenty dollar a gallon diesel and gasoline would undoubtedly bring the world economy to it's knees overnight,but if we could somehow run the rest of the economy without these fuels,we could easily feed our selves with food grown with negative eroei ENGINE fuel at these prices for farmers and delivery trucks.

This would of course assume that fertilizer,steel,etc,are manufactured with coal or natural gas or other energy sources at more reasonable prices.

But I believe like Darwinian that such an outcome is unlikely.

It will be easier and quicker to build or retrofit trucks and tractors to run on(propane) lp gas,which can so far as I know,be seperated fron natural gas in suffucient quantities to supply a good part of the amount needed to farm,and I am under the impression that it is not that hard to manufacture fron crude or ng,although at an energy loss of course.

( natural gas itself is not useful as a MOBILE engine fuel,as it has to be supercooled to liquefy it and get enough into a tank to drive very far.There does not appear to be any workable solution to this problem at this time.)

Furthermore Scania manufactures a very good diesel engine that runs on 95 percent ethanol and 5 percent ordinary diesel,which is very fuel efficient.And ethanol fueled spark ignition engines will suffice for farming purposes if necessary,although the ethanol path is imo another high road to hell.

(Refitting existing diesels to run on ethanol is not really a solution-a new one wouldn't cost much more and probably less.Refitting older gasoline tractors to run on high ethanol fuel mixes can be done but I have no cost data,as the only ones I have heard about have been back yard tinkering jobs.They will run,but thats all I can say for sure.)

I recently talked to a Scania man on the phone who told me the engines cannot be marketed in the US because they will not pass the emissions tests but that the Europeans have necessarily made the pragmatic decision to use the engines and make up the pollution excesses by tightening up elsewhere.

He was not knowledgeable concerning the price of these engines,being an American dealer,but his impression is that they run about twenty percent more than the conventional engine and last just about as long.

And of course trains and electrically powered trucks can pick up part of the load,etc,plus localization will do away with a lot of shipping.

C2H5OH + 3O2-------> 2CO2 + 3H2O..........what emission problem????

Too much carbon dioxide? Certainly not too much water since we could use all we can get in the environmental water cycle.

I don't get it.

Never mind. I looked into it.

Nothing is perfect stoichiometrically. Lot more to it than I thought due to imperfect combustion. Doh!

The problem has to do with nitrogen oxides rather than co2.

If they are willing to license it ,Mercedes has an ammonia injection system in production that takes care of that problem nicely.

Also I must correct my above comment about ng not being a satisfactory mobile engine fuel.The very high pressure tanks necessary are getting cheaper all the time,and ng vehicles are now cost effective for fleet use.My info was past it's expiration date.

Both Scania and Volvo has multiple engines that can run on different fuels and anyone of them can be series produced quickly. Ethanol, DME, methanol, biogas, LPG, LNG, RME, you find the fuel and there will soon be an engine that can burn it. Volvo has been more agressive in their developments then Scania but they are also larger.

Scania even have a producer gas truck engine in their archives. It were developed with state funding during the cold war to be used if there would be a long term interruptions in the oil imports to Sweden. It do not comply to modern exhaust standards and the engine it were based on is no longer in production but given a couple of years it could be produced in volume.

Yes, it's a secret technique of scientists who know better to describe things non-sensically just because they feel they are not confused by what the non-sensical description means (like describing progressive change as linear). The default presumption for all accumulaltive development curves should be that they fit a sequence of regular progressions, with reorganizatin of the system producing them during the transitions. The real effect, that the scientists that draw straight lines for the beginnings and endings of developmental processes is that they miss all the questions about how the shape of the most likely true curve points to the true behavior of the system doing it.

For example, if you understood that the random fluctuation in a curve *is above and below the mean of the physical continuity* of the underlying process... you would draw the implied continuity as a line connecting the midpoints of he fluctuatins and see if that made more sense in terms of describing the underlying process.

It should look like the blue with Excel 'growth' function not the pink 'trend' function.