| Countdown to $200 oil (10) - oil at $115!! | The Oil Drum: Europe | Italy like Ryanair: can it exist with oil over $ 100 per barrel? |

What Future for Coal in South Africa?

Posted by Doug Low on August 12, 2008 - 9:30am in The Oil Drum: Europe

This is a guest article by Jeremy Wakeford. Jeremy is an economist specializing in energy and sustainable development and is Research Director of ASPO South Africa.

South Africa has been in the news a lot recently because of its electricity supply problems throughout 2008. Most South African electricity comes from coal-fired power stations. Jeremy discusses the role of coal in South Africa's energy mix, long-term trends in production and consumption, and how underground coal gasification might help solve South Africa's energy problems.

Can and should our dependence continue?

South Africa’s energy economy is overwhelmingly dependent on coal. The fossil fuel provides nearly three quarters of total primary energy, supports almost 90 per cent of electricity generation, and provides feedstock for close to a third of the country’s liquid fuels via Sasol’s coal-to-liquids process. Coal is also used directly as a fuel by certain industries (e.g. steel production), and indirectly as feedstock for Sasol’s petrochemical products. In addition, roughly a third of the nation’s annual coal output is exported, generating an important source of foreign exchange earnings.

There are two major risks inherent in this heavy dependence on coal: one is the finite nature of its supply, and the other is its contribution to global warming. This article takes a broad look at some of the key issues concerning the outlook for coal in South Africa, including demand, supply, prices and environmental concerns. It concludes with a brief discussion of a promising development called underground coal gasification, which could potentially address both of these risks to some extent.

Demand for coal is growing

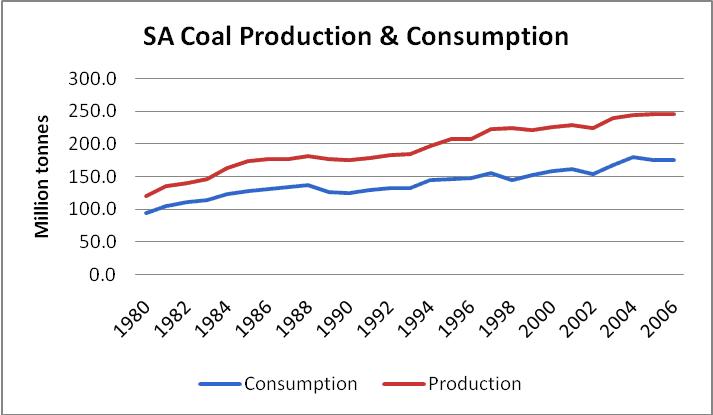

Production and consumption of coal in South Africa have grown reasonably steadily over the past two and a half decades, at average annual rates of 2.9% and 2.5%, respectively (see Figure 1). Consumption in 2006 is estimated by the US Energy Information Administration at 177 million metric tonnes (mt). The largest share of this, about 64%, was burned by Eskom in its power stations, with Sasol consuming another 24% and industry and small consumers accounting for the remainder. Eskom’s consumption of coal grew to 125 million tonnes in 2007.

Figure 1: Production and consumption of coal in South Africa

Source: US Energy Information Administration

This growth in coal use – especially by Eskom and Sasol – is expected to continue or even accelerate over the next few years. Eskom is in the process of returning to service three coal-fired power stations (Camden, Grootvlei and Komati) with a combined capacity of 3800 megawatts (MW). It has also begun construction of the new 4800 MW Medupi power station, whose first unit is due to begin generation in 2012, while a second plant called Project Bravo (5400 MW, scheduled to start generating power in 2013) was recently given the go-ahead. The combined consumption of these five power plants could raise Eskom’s coal use by over 50 mt (assuming they use the average amount of coal burned by existing power stations in 2007).

For its part, Sasol has announced that it is conducting feasibility studies for an expansion of its existing synfuels plant at Secunda by 20 per cent (or 30,000 barrels per day) and for the construction of a new plant (called Mafutha) with a capacity of 80,000 barrels per day. If both of these projects come on stream, they could raise the demand for coal by approximately 25 million tons a year (again extrapolating from past consumption patterns).

Thus the domestic demand for coal could rise by 75 million tonnes or over 40% over the next decade. Only from about 2025 when the decommissioning of older coal-fired power plants begins could one expect consumption of coal to start falling (provided no further coal-fired plants are built). This raises an important question: for how long might South Africa’s coal reserves be able to sustain current and projected rates of consumption?

Can reserves sustain this growth?

The electricity crisis has already thrown a spotlight, so to speak, on the status of the country’s coal reserves: Eskom attributed a part of its electricity supply problems at the start of this year to difficulties it experienced in sourcing sufficient quantities of suitable grade coal. This prompted the Minister of Public Enterprises, Alec Erwin, to say that the government would if necessary intervene to ensure Eskom’s coal needs were met. Could this be an indication of moves towards resource nationalism, as are increasingly being observed across the globe in relation both to energy (especially oil) resources as well as food production? There is probably little immediate chance of this happening, for two reasons. First, Eskom uses low-grade coal while export-quality coal is high-grade and unsuitable for burning in existing power stations. Second, coal mining companies have long-term supply contracts to fulfil. Outright nationalisation of the coal industry would seem a remote possibility given the need for financial capital, management expertise, etc. possessed by the mining companies. However, it is still possible that growing domestic demand could at some point in the future come into conflict with exports.

According to BP’s Statistical Review of World Energy 2007, South Africa’s proved reserves of coal stood at 48,750 million tonnes at the end of 2006, representing 5.4% of the world total (the sixth largest national share). BP estimates a reserve to production ratio (i.e. the number of years production could be sustained at current rates) of 190 years. The Statistical Review defines proved reserves as “those quantities that geological and engineering information indicates with reasonable certainty can be recovered in the future from known deposits under existing economic and operating conditions.” This figure seems to be based on the 1987 Bredell report. However, the official government figure for reserves has been revised downward sharply to only 28.6 billion tonnes (South Africa Yearbook 2006/7), giving an R/P ratio of about 115 years.

David Rutledge, a Professor at the California Institute of Technology, has used the ‘Hubbert linearization’ method to estimate that there could be as little as 10 billion tonnes (Gt) of recoverable coal reserves remaining in Africa (most of which is in South Africa). If true, current production could be sustained for only about 40 years.

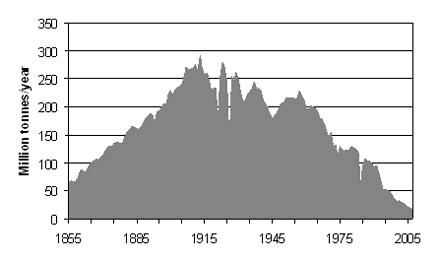

The R/P ratio is however of limited usefulness, for a couple of reasons. First, as mentioned already, the annual rate of consumption is expected to grow in the medium term, not remain constant. More fundamentally, production cannot maintain any particular rate indefinitely and then suddenly collapse to zero. Because coal is a finite resource, its production will of necessity reach a peak at some point and then decline gradually toward zero. This production profile, initially identified by the geophysicist M. King Hubbert in the case of US oil production, is clearly evident in the history of British coal output (see Figure 2).

Figure 2: British coal production

Source: Prof. Dave Rutledge: http://rutledge.caltech.edu/

The ‘Hubbert peak’ for South African coal production may still be a few decades away, depending on which estimate of ultimately recoverable reserves turns out to be most accurate. If Rutledge’s conservative reserve estimate is used as a base, and the rule of thumb applied that peak production occurs when roughly half the recoverable resource has been mined, then the peak could come by 2020 if production grows at historical averages (2.5%) until then.

Whatever the case, the economics of mining dictates that the most accessible reserves are mined first, so that the net energy return from the coal mining declines while the production costs rise over time (although the latter may be counteracted to an extent by technological improvements). To a degree this process is already in evidence, as costs are rising and the quality of mined coal is declining, according to statements made by Eskom officials.

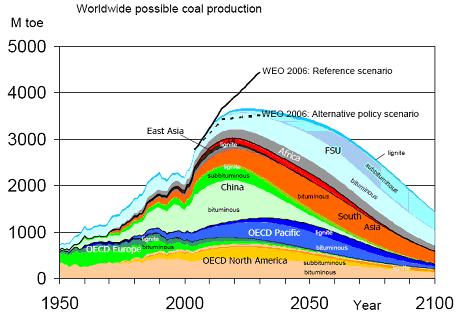

The global picture is similar. Several studies of global coal reserves published last year indicated that world reserves are likely to be much lower than has been commonly believed. One of these studies, by the German Energy Watch Group, forecasts that global coal production might reach its peak as early as 2025 (see Figure 3). Meanwhile, demand is growing rapidly in many developing countries, mostly notably in China (which has recorded growth of 12 percent per annum since 2001) and India.

Figure 3: Global coal production: history and forecast

Source: Energy Watch Group (2007)

Spiralling prices

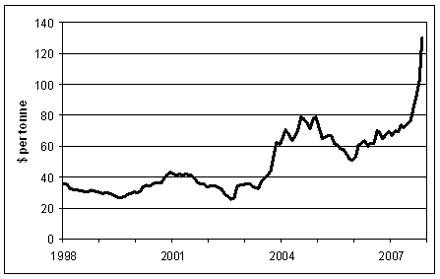

The surging demand in the face of short-term supply constraints has resulted in a dramatic rise in coal prices over the past few years (see Figure 4). The spot price of coal on the international market has risen from $100 to $300 per ton within the last year. A major reason is that China, by a large margin the world’s top producer and consumer of coal, recently became a net coal importer.

Figure 4: Northwest Europe steam coal marker price

Source: McCloskey Group

All this has been good news for South Africa’s coal exports. South Africa was the world’s fourth largest coal exporter in 2005, selling 65 million tonnes of high-grade coal to buyers in Western Europe (approximately a quarter of their coal imports) and East Asia. It was recently reported that India may source low-grade coal from South Africa to fuel new power stations.

Domestic coal prices are also on the rise. Eskom has cited a 30 per cent rise in the price of its key feedstock in the past year as one of the reasons it is seeking a 100 per cent increase in electricity tariffs over the next two years. The CEO of ArcelorMittal, the giant steel producer, recently stated that he expects the price of coking coal to rise between 150% and 200%. As long as demand remains strong, the spike in coal prices will not be a temporary anomaly.

Can our climate cope?

The scenario of demand growth – subject sooner or later to supply limitations and thereby forcing up prices – applies in a business-as-usual scenario. But from the climate change point of view, can we afford to burn all the coal that’s left? In parts of the developed world at least, there is a movement away from coal. In February 2007, NASA’s chief climate scientist James Hansen called for a moratorium on the construction of new coal-fired power plants unless they sequester the carbon emissions. Lester Brown, President of the Earth Policy Institute, recently noted that opposition is mounting to coal-fired electricity generation in the USA, where many State governments are placing moratoriums on the construction of new coal power plants. The European Union has embraced renewable energy and is at the forefront of efforts to reduce carbon emissions.

South Africa is a signatory to the Kyoto Protocol, but as an Annex I country currently has no obligation to reduce its greenhouse gas (GHG) emissions. However, this may change under a successor treaty to Kyoto, which is due to expire in 2012. Given the severity of climate change, a new protocol could be much more stringent, and could involve an international carbon trading system that would add a substantial premium to the price of fossil fuels. There is consequently a significant risk for South Africa that its carbon-intensity will undermine the international competitiveness of many of its exports (e.g. minerals, beneficiated metals and certain manufactured goods).

Thus far, although carbon capture and storage (CCS) has received a lot of attention, the development of economical technology could take years or even decades. Earlier this year the Bush administration cancelled federal funding for a consortium aiming to construct a demonstration coal-fired power station that sequesters its carbon dioxide emissions, on account of rising costs. Whether or not CCS will some day become technically viable in South Africa, it looks highly likely that carbon sequestration at existing plants would substantially increase the costs of coal-based electricity and/or liquid fuels.

Two birds with one stone?

More promisingly, Eskom and Sasol are currently working jointly to develop an alternative technology for extracting the energy from coal, called underground coal gasification (UCG). This is a process whereby coal is ignited in situ underground, fed through a borehole by air or oxygen and yielding a synthetic gas (syngas). The syngas can be used for electricity generation, for the production of synthetic liquid fuels or for industrial uses (e.g. manufacture of petrochemicals). In addition to this flexibililty, several other advantages are claimed for UCG. First, otherwise uneconomical resources can be utilised; Eskom estimates that an additional 45 billion tons of coal could be exploited through UCG. Second, there is no need for traditional mining and associated health and safety risks for miners. Third, indications from a pilot UCG project in Australia indicate that the process has a much lower environmental impact (in terms of groundwater contamination, land degradation and subsidence, and greenhouse gas emissions) than conventional mining.

Eskom already has a small pilot UCG plant in operation at its Majuba power station in Mpumalanga, generating 100 kilowatts of electricity. So far, Eskom is optimistic that the costs will compare favourably with those of conventional coal mining and power generation. One must pose the question, however, as to why UCG has not been commercialised before in South Africa (and other countries such as the United States), given that the technique has been used since the 1950s in the former Soviet Union.

Conclusion: watch this space

Let us attempt a quick summary of the coal situation. In the first place, coal’s future in South Africa is perhaps not as certain as was commonly believed, at least until recently. Second, the risks of continuing heavy dependence on coal are becoming clearer: including security of energy and electricity supply, as well as climate change and associated financial risks related to carbon pricing. Third, the international price of coal looks set to continue to rise in the foreseeable future – whether from resource constraints or climate protection - so that the long era of cheap coal seems likely to be over for good. Fourth, underground coal gasification may provide a partial solution to all of these challenges in South Africa by substantially extending the amount of economically recoverable coal reserves while also limiting the environmental damage. The development of UCG will no doubt garner close scrutiny over the next few years, and not just in this country.

But this prospect should not allow a renewed complacency to set in regarding coal dependence. From a long-term perspective it arguably still makes sense for the country to diversify its energy sources by investing in renewable energy technologies and industries as ultimately these will be needed, have proven environmental benefits, and are becoming increasingly cost competitive with fossil fuels.

Jeremy Wakeford

This article was first published in the May 2008 edition of the magazine Energy Forecast

Personnel

Editors

Contributors

Peak Oil Primers

Archives

- November 2010 (3)

- October 2010 (6)

- September 2010 (4)

- August 2010 (7)

- July 2010 (6)

- June 2010 (7)

- May 2010 (2)

- April 2010 (8)

- March 2010 (4)

- February 2010 (6)

- January 2010 (3)

- December 2009 (5)

- November 2009 (8)

- October 2009 (12)

- September 2009 (6)

- August 2009 (5)

- July 2009 (11)

- June 2009 (8)

- May 2009 (16)

- April 2009 (10)

- March 2009 (7)

- February 2009 (10)

- January 2009 (15)

- December 2008 (9)

- November 2008 (9)

- October 2008 (9)

- September 2008 (13)

- August 2008 (10)

- July 2008 (14)

- June 2008 (23)

- May 2008 (16)

- April 2008 (12)

- March 2008 (16)

- February 2008 (9)

- January 2008 (13)

- December 2007 (13)

- November 2007 (16)

- October 2007 (22)

- September 2007 (8)

- August 2007 (9)

- July 2007 (16)

- June 2007 (8)

- May 2007 (7)

- April 2007 (7)

- March 2007 (10)

- February 2007 (10)

- January 2007 (12)

- December 2006 (9)

- November 2006 (15)

- October 2006 (4)

- September 2006 (5)

- August 2006 (5)

- July 2006 (9)

- June 2006 (5)

- May 2006 (10)

- April 2006 (9)

- March 2006 (13)

Vital Trivia

License

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.

The problem with using Hubbert peak analyses to predict the future with coal is that the assumption that only traditional coal mining methods will be used in future doesn't stand up too well to close examination:-

http://www.coal.gov.uk/resources/cleanercoaltechnologies/ucgintro.cfm

Hi ES,

My guess is that UCG would be treated like coal-bed methane in statistics, and would show up as natural gas production, rather than coal production. The situation is somewhat like Canadian oil sands, which are strip mined but count as oil production. The output would naturally be included in the Hubbert linearization for natural gas for Uzbekistan, according to your link.

Dave

Can you tell me where the largest mines for coal are in South Africa. A map or just general area would be fine.

Jeremy,

Has South Africa any strategy to replace Coal's role of baseload electricity generation? And in Transport? What fraction of South Africa's transport systems are reliant on Coal? Is there any strategy to replace Coal's transport synfuels?

From this distant view, I'd say that replacing Coal under the current environment of constrained Gas and Oil markets will be hard in the least.

A few remarks:

In the 80s Eskom had its own coal mines, so it could manage its own supply. Apparently this isn't so any more. Maybe not a very smart decision to cut off one's own supply chain...

I think the main issue in South Africas electricity supply are the extremely low consumer prices. As far as I remember they were at 1 cent per kWh before they doubled to 2 ct/kWh (compare: average in Germany: 20 ct/kWh or 30 US-ct/kWh). Thus, energy providers are far from being motivated to invest in more capacity, which would produce anything but losses for them. It is just like in the socialist countries where people had sort of a flat rate on energy, so nobody cared about energy efficiency. As for South Africa I remember some people even left their air conditioning on when they were on holidays.

Of course it will be very hard for the government to wean the people from the good old cheap rates - people are already now protesting against rising petrol prices. But sooner or later there won't be any choice as the resources as such become more expensive to dig up.

I have the impression that South African coal may peak quite soon:

There were very large deposits exploitable from open pit mines, but the shallow ones are almost dug up, and the deeper ones have to be extracted from underground mines. This is especially difficult with the geological conditions in SA, where the occurrence basalt dykes may obstruct the production process. Here, underground coal gasification sounds like a good solution. But as far as I know this technology is still in an experimental stage, and all former projects trying to use it were discontinued. So if UGC will ever work it will probably take quite a while until it will bring a considerable contribution to energy supply, and this will be probably post-peak.

Furthermore I don't see that UGC will have a better carbon balance - and adding the cost of CSS it will be very doubtful if coal power plants will be profitable at all - certainly not at a price of 2 cent per kWh!

Could you expand on the difficult geologic conditions? The basalt dikes you mention, do these cross cut the coal seams?

Yes, they do. If you are lucky you can localize them with a magnetometer (20 years ago I did this walking through the bushveld, now this is also done with helicopters). If you miss one you may be out for a bad surprise. Whereas in an opencast mine you just blast the whole stuff and pick the coal out, in an underground mine a dyke may provide a much darker outlook: A 2007 study for the EU "COAL OF THE FUTURE" has a few more details (currently offline):

"In southern African mines the coal seams are heavily intruded by Jurassic dolerites dykes and sills. These either burn the coal or cut through it and due to their hardness and possible seam displacements, which makes mine planning difficult.

The presence of these intrusives is the main reason why so few long wall or short wall mining methods are used in South Africa."

This makes mine planning even more complex than they are already: Unlike the regular (although folded) coal seams we are used in Europe the South African seams I have seen were much more irregular due to a different deposition history. It was quite hard for me to keep the track and I was impressed of the local geology team who managed it regularly.

If one used UCG long enough, wouldn't that undermine the surface and eventually cause subsidence? With a regular mine, they leave pillars behind to support the surface - with an underground fire like this, it is haphazard and you wouldn't have a good way of doing that.

I suppose that would mean that the surface underneath the mine is essentially unusable for many purposes.

UCG is especially advantageous for very thin coal seams, which are too thin to be accessed by men and/or machines, which means relatively little subsidence. Furthermore the coal generally is going deeper and in great depths the subsidence is widely dispersed, which helps to avoid surface damages. Maybe material can be blown in from above ground. Or parts of the coal is left unburndet (perhaps unintentionally, as it is not so easy to keep it burning regularly).

But as I wrote all is still in an experimental stadium.

Guys, the electricity crisis in South Africa has nothing to do with coal and everything to do with politics.

Eskom fired most of their competent white engineers and technicians and replaced them with blacks who were mostly clueless. Now their whole infrastructure is in desperate need of repair and there's no one to do it.

Recently they also got rid of most of their white contractors, who had supplied coal cheaply and reliably and hired new black contractors, most of whom had no freight delivery experience whatsoever (eg. one guy who got a $10M/year contract through Eskom's affirmative action policies was an estate agent) This had predictable results and when Eskom scrambled to get coal from their old white contractors, they found that the coal is now in long term export contracts to China.

Here's a good primer.

It's a bit too politically correct, but it does mention the important bits.

The global coal situation is worrisome both short term for the atmosphere and long term for those not pursuing alternatives. India needs to import higher grade coking coal and China is hinting at looming shortages. It's interesting that South Africa is bringing coal plant out of retirement as was done after the gas pipeline explosion in Western Australia. De-mothballing old coal plant may be cheaper and safer politically than building new plant, albeit lower emitting. Those newer plants that may get approved include supercritical steam, dried lignite and combined cycle coal gasification; the trick seems to be to assure gullible politicians they are 'capture ready'.

I'm not that confident that UCG is a winner as opposed to coal seam methane. The CO2 rich gas has low heating value and there are problems with groundwater and leakage. It seems highly unlikely that the CO2 could be economically scrubbed, cooled and re-injected into a different part of the same coal basin.

I recall a recent mention of carbon taxes in South Africa. While both US Presidential candidates and the Australian government are committed to cap-and-trade in practice I think existing coal users will get off lightly. The tough talk may put off coal-to-liquids projects in which Sasol seems to be a key technical advisor. Putting it all together on a global scale I think we will make excuses for increased coal burning for another decade then the real crisis will begin.

True. I don't think developing countries will sign up to restrictions on their emissions if it has a negative impact on their development, and if they do they will not attempt to abide by them.

Jeremy,

One small remark: The picture for the price of coal is in nominal dollars I guess? Better to use inflation corrected dollars.

Further, since it is european coal, maybe putting it in euro's (or DM before 1999) would be better. I think it will change the conclusions a bit.

For instance: The world big currencies are not floating freely. The dollar and the euro are (more or less), but the Yen is not and the Yuan is definitely not.

So if the price rises for China because they keep their Yuan artificially low wrt the dollar (which is declining wrt the euro because of a sustained very large trade deficit), then that's a result of the currency manipulation of the Chinese. Not because the market is pricing coal more expensive. Basically the Chinese are subsidizing the US (and Europe etc) at the expense of their own people. They choose jobs, not wealth.

The price of coal in dollars is only interesting if this coal is exported in large volumes to dollar countries.

Well, just my 2c's

Hi ex pats,

Most of ESCOM's problems are absolutely political myopia.

Now the problem compounds. I used to fly a magnetometer and a scintillometer around SA looking for Uranium. I think we found quite a lot of it.

If common sense prevailed in SA they would realize that Nuclear is the only sustainable long term power system functional at this moment.

Olduvai is a worse risk than Nuclear as a long term prognosis, so they should try to get to it quite quickly, and save all their coal for SASOL, and transportation needs

One draw back is that with their Black empowerment they have no chance of creating enough local engineers and technicians in time to relieve themselves of the Coal usage, to try to retread the white guys in this field will find that they are too few and too old.

No country in Africa has yet "made it". Ghana, had the best chance of all in 1962 and failed. Zimbabwe probably inherrited the second best country with a chance and it is failing miserably.

SA has a mammoth task ahead of it. Bringing 40 million deprived Tribal people up to speed is mind boggling, probably impossible in the time available. (Psych 301 once mooted that it took 4 generations to bring immigrants up to speed)