A Brief Natural Gas Update (It's Thursday)

Posted by nate hagens on March 27, 2008 - 11:09am

Sometimes lost in headline discussions of oil production and prices is the sister story for natural gas. As might be expected, natural gas prices have mirrored the price change in oil, (though in the UK, they are currently approaching $15per mcf-a much higher increase than in North America). We have just been through (and still are in, from where I type this) one of the coldest winters in recent memory-consequently we have had dropped considerably from beginning storage levels. This morning the EIA announced a 36 bcf withdrawal of natural gas for the week ended Mar 21, in line with expectations, but capping a winter of 2nd largest withdrawals since 1995. Below the fold are a few graphical snapshots of the natural gas situation. TOD readers feel free to post any relevant natural gas links below.

Natural gas contract prices - daily for May 08 delivery (Click to enlarge)

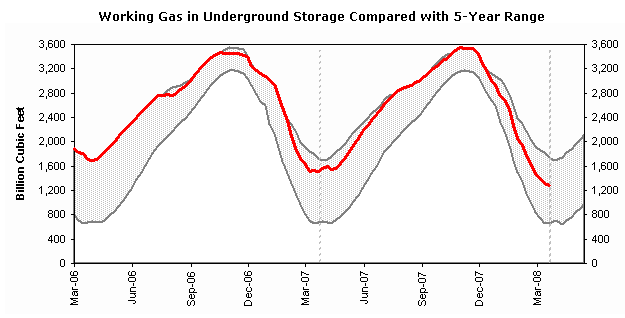

Thanks to 2 mild winters and a mild summer, the US Natural Gas storage situation started this winter season with record stocks. However, a cold winter has brought stocks much more in line with historical averages (note - these numbers are in absolute terms, not adjusted for demand or population growth).

Working gas in storage (underground) vs 5 year average (Source - EIA (Click to enlarge)

Through January end, we have undergone the steepest 12 month drop in global temperature on record - which led to more demand for natural gas for heating and electricity. (A primer on how much fossil fuels we use in USA for home heating, compared to our forest wood stocks can be found here)

10 Year temperature anomaly - UK Hadley Climate Research Unit Temperature(Click to enlarge)

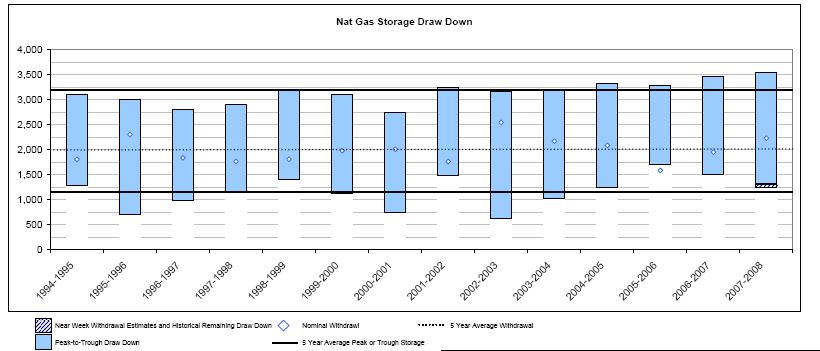

So we had the 2nd largest total withdrawals in last decade - equity research firm Johnson Rice graphed the drawdown like this:

Historic peak to trough drawdowns of US natural gas stocks- (Thanks to Johnson Rice equity research) (Click to enlarge)

So in sum, current storage is still above historic trough for this time of year - but only because we started with record gas in storage. This is all happening while electricity demand is near the top of the historic range for this time of year, after a February drop:

Historic electricity demand - Source- Johnson Rice (Click to enlarge)

As a brief aside, nuclear utilization (for electricity), due to maintenance and/or age of facility, etc. has shown a meaningful decline this month:

Historic nuclear utilization - Source- Johnson Rice (Click to enlarge)

When combined with an increasing speed of the treadmill for natural gas production in North America, and the fact that over 70% of energy inputs into oil production are natural gas, I expect we will have an interesting summer. I'll make sure and have my woodshed stacked come December 2008, just in case.

(TODers please post any natural gas related data/links below.)

Contact

- Content: editors at theoildrum dot com

- Tech support: support at theoildrum dot com

License

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.

?

What i´m missing here? 36 bcf is nothing imo

?

total withdrawal for year was the focus - not this weeks number.(and, in truth, I saw nothing in the cupboard this am and was unaware of HOs coal post so put this together - I continue to believe nat gas will be the larger story in next 3 years)

About a year ago I insulated my 80 year old house and installed good replacement windows. My natural gas consumption has fallen from an average of 8.3 therms per day (Nov. 1 through Feb. 28/29) to 5.4 therms per day, a decrease of 35%.

Clearly we have more ethanol production year over year as well. Does anyone have any statistics on the increase in natural gas usage due to ethanol plants ? (I guess it would also be possible to calculate NG use for fertilizer and pesticides but much of that is sourced overseas now)

I just wanted to point out that while it may seem cold for january (from the same Hadley data), we've seen (globally) recent colder Januaries in 2000 and 1996 (how soon we forget).

Here is the plot of the January data from 1900 to 2008. I'm working on one for seasonal winter and I'll post it shortly. Compared to previous years it is a drop but it is still the 30th warmest january on record from 1900 to 2008.

Thanks - in the Johnson Rice graph I linked you can see that we ended 1996 and 2000 winters with about 750bcf left in storage - those were the lows of last 15 years. I just wonder what a bit of reduced production (e.g.5-8%) combined with cold winter might do.

Here is the Winter Temperature Anomaly since 1851 (corresponds to December, January, and February and the year corresponds to the January year value). The winter of 2008 works out as the 19th warmest on record since 1851 (the first complete winter on record).

The dataset from the GISS and NCDC show slightly different values from the Hadley data (but nearly identical trends) based upn how they validate and extend the data.

Watch and hear Schlesinger's comments on natural gas and more speaking at the

The National Academies Summit on America's Energy Future - The Geopolitical Context of America's Energy Future; Day 1, Part 3, March 13, 2008

He opens his speech with the following:

Thanks for that link.

You're very welcome. Later on, he points out that whether it's peak oil or "peak access to additional hydrocarbons," there is no getting out of the predicament we are in:

This chart is from the Canadian National Energy Board short term 2007 - 2009 NG deliverability report.

The Canadian government is predicting a fall in natural gas production because current prices are too low to support high drilling activity in Canada. This is going to make it difficult to refill those stocks. We can expect that stocks will fall until a price spike drives prices high enough to do more drilling.

NG in North America is not like world oil. Prices are only a thin margin above drilling costs. That is because industrial feed stock users are being destroyed (a 22% drop in NG demand from 1997 - 2005). Don't delay those insulation and home heating investments. The industries are buying home owners a brief price respite. It is coming to an end.

I have spoken with David Hughes who sits on the Canadian Gas Potential Committee. He confirms Leherrere's prediction for Canadian Gas. The pink line is total production (U=1900 in the key).

You can hear him discuss the situation here: http://globalpublicmedia.com/transcripts/827

Jon- this is the definition of a low energy gain, receding horizon, situation. Once nat gas prices increase, presumably drilling prices will also increase. Standing here today, market analysts will predict more production when we have higher prices but I'll bet dollars(err. Francs) to donuts that they are underestimating future costs that would accompany higher revenues.

Does the Canadian Energy Board forecast higher production after 2009?

The NEB just released a new outlook to 2030. Mr. Hughes stated that it went to press before they finished the 2007-2009 outlook, and so it is too optimistic (most data ends 2005 before the drilling activity took a steep drop). You can see the whole thing here:

http://www.nrcan.gc.ca/com/resoress/publications/peo/peo-eng.php

However, even this optimistic forecast shows natural gas production declining (but not nearly as much as Laherrere). And net exports drop over the whole period and Canada stops being a natural gas exporter by 2022. (pg 49). Clearly, this is not good for the USA. Canada is expected to start importing LNG to support further growth in NG use.

Also of note, it is clear the NEB does not yet know about EROI because they forecast NG prices to drop and then remain flat over the whole 2010 to 2030. Nor do they seem to know that Japan is paying $19 per MMBTU today. Since prices are set on the margin it seems implausible for prices to drop and then remain low while importing LNG.

http://www.platts.com/Natural%20Gas/Resources/News%20Features/gasdiverge...

US NG Demand is 3x higher than the whole world market for LNG. Does that sound like a situation for falling prices? I admit being a naive engineer, but that sounds like higher prices to me.

Has anyone analyzed the potential for government subsidies supporting drilling? It's a national security matter, after all. And I doubt taxpayers would object to paying a bit more on April 15th for keeping the lights on and the house warm.

I keep telling people to reinsulate, even before anything about veggie gardens. Need/plan to take my own advice soon as well...

Unfortunately that just causes the NG to run out faster at a lower perceived cost. It is very popular with oil companies however.

Generally subsidies need to be on the insulation side for older buildings/homes and tough regulation on new buildings. There is no reason new buildings need to use much energy to heat and cool.

I have decided to voluntarily send an additional 10% of my income to the Government to support additional drilling for natural gas.

We keep the house cool in winters, warm in summers - however I am worried that my fellow Americans' multitude of commercial and residential spaces - shall not be sufficiently HOT in Winter and COLD in Summer.

I encourage all right thinking Americans and Canadians to do the same.

May the force be with you.

youre kidding right? they have no allocation mechanism to do that-plus they would need millions. Your gesture is noble but maladaptive

Yes I am kidding and was being sarcastic.

- I think that we use an excessive amount of fossil fuels & the oil drum has a nice quote - ...burning oil for fuel is like burning a Picasso for heat...

- The scale of American consumption is mind boggling (all 20 tcf annual NG burning is ultimately used for HVAC - even in manufacturing facilities

Jon, on the Laherrere plot it appears adding the predicted conventional and predicted unconventional should give the predicted marketed right? But they don't add up. Look at 2020. Each is 10 tcfa but marketed is like 17.5. Am I reading this incorrectly?

Hi Mark,

His U=1900 line contains both conventional and unconventional. The Red IEA forecast is not Laherrere's. (He likes to put a lot of plots on one graph, which makes them a touch difficult to read).

You can find the his whole paper (well worth the read) at ASPO France under documents. He also has a world wide look at LNG in a document with Nice in the title (It is in French, but understandable).

Ah. I skimmed too quickly.

Precision Drilling Trust is one of the largest natural gas drilling service "companies" in Canada. This was taken from the 2007 3rd quarter report:

There is a whole lot more to the story. The last year we had a severe drawdown from storage was the winter of 2002/3 which ended with about 730 Bcf in storage, and the NE on the edge of non delivery due to low pipeline pressure. Since then we have had a string of mild years, with low HDDs or CDDs or both. We have also increased storage caoacity from about 3200 Bcf to 3600 Bcf, and because of the mild weather have been able to reach essentially maximum storage every year. In 2006 we very nearly had more supply than we could store, and a small amount of supply was shut in. In 2007, with s little more capacity available we fell just short of the overfill point, mainly due to a decrease in both LNG and imports from Canada late in the year. USA production in 2007 was about back at the previous peak of 2002, due to growth in non conventional supply as shown in Laherreres chart. The growth in unconventional supply resulted from a huge increase in drilling during 2005/6/7, which cannot be continued due to lack of spare rig capacity. In fact drilling flattened, albeit at a high level in H2 2007.

For the 2008 injection season we can expect little to no increase in USA supply, some decline in Canadian supply (as shown above) and a decrease in LNG imports due to high demand/prices in ROW. To offset this problem we will likely have an increase in Hydro due to the huge western snow pack and precipitation, and maybe a mild summer if we are in the beginning of global cooling. For several years now we have not exceeded injection of 2100 Bcf. We are likely to end the withdrawal season with 1200 Bcf left in storage and maybe will start the next withdrawal season with no more than 3400 Bcf in storage vs a capacity of 3600 Bcf. Another withdrawal season like this one will bring storage below 1000 Bcf, and set the stage for a major crisis by March 2010.

If we have a few weeks of hot summer, one or two temporary nuke outages and a cold winter next year, the crisis will be by March 2009. Peak NG for North America is almost certainly coming before peak oil. If you heat with NG I strongly advise purchase of long johns and sweaters. Murray

In a natural gas shortage, residential supply will be the last thing to go, not the first. The first thing to go will be the natural gas used to generate electricity. The reason is that cutting gas supply to homes creates too many fire hazards and other health risks. Once the gas is cut, all the pilot lights, gas burners, heaters, etc. go out. When you try to restart the gas through those lines, you can imagine the problems involved.

You are correct. But, in the UK at least, most gas central heating requires electricity to actually run anything more than a pilot light - so, no electricty means no heating since you can't consume the gas - unless (like me) you install a relatively small battery and inverter to run the pumps and lights during the electrical power cut.

In a shortage of gas (such as we probably can expect in the UK soon) IMO the domestic electrical power will become intermittent - deliberately - thus safely saving the gas that would have been burned in houses.

Expect the energy supply system to fail when it is under the most stress - either when it is very hot or very cold.

Warm clothing will be the order of the day if the power fails in the winter.

Perhaps the statement should be revised to say:

If you live in New England and heat with electricity I strongly advise purchase of long johns and sweaters.

This is because electricity generation in New England is highly dependent on natural gas, and as NASAguy says, natural gas used to generate electricity would be the first thing to go. Even that statement, however, is probably too alarmist. In the event of serious shortages, I believe electricity (and gas) for business and industry would be the first to go while trying to preserve electricity (and gas) for residences. Persistent price rises for both electricity and gas, meanwhile, will suppress long-term demand growth.

I would word it:

If you live in New England and heat with any device that requires electricity to run*, I strongly advise purchase of long johns, sweaters, and a wood stove.

*) that includes boilers/furnaces that run on oil or propane. Even some wood pellet stoves?

Also should add that, for now, electricity around here is no more expensive than oil or propane (per BTU), and does not require payment on delivery. Thus, in case of a cold snap, there will be some people using electric heat instead of their normal oil or propane devices, adding to the pressure on the grid and NG supplies.

Good point, which is why I'm thankful my gas-fired steam system requires absolutely zero electricity to run. The boiler's pilot light drives a 750 millivolt "powerpile" circuit which operates the gas valve. My heating contractor has told me that these 750 millivolt systems are not made any more.

I also have a wood stove insert, and even that uses an AC powered blower to provide forced convection. The stove will still provide heat, albeit much less efficiently, without electricity to run the blower.

In my area, suburban Boston, electricity costs over three times natural gas per BTU. I don't know how it compares with propane or heating oil. It (electricity) costs about $0.185 per kWh and gas is $1.71 per therm. Gas rocks; I'll be sorry to see it go.

California, too.

49% of our electricity comes from natural gas.

I would hope that rising prices would cut back both home heating and electric power usage of natural gas so that we don't lose all natural gas electric.

We really need to move away from direct use of fossil fuels for heating and instead use ground sink heat pumps and solar - plus a whole lot more insulation.

I have worked in several central heating plants and they were all designed to use NG or oil.

They would use NG all the time and only use oil if there was a shortage or low pressure on the NG supply.

We would always keep a full oil tank for such emergencies. I do not remember the tank size, but think it was about a million gallons.

For all the NG electricity power plants in North america, does anyone know if they are duel fuel with sizable oil capacity ??

Meanwhile pickens is advocating running cars on ng, low emissions/cost... great idea, but cars typically run for a decade, ng might not be so cheap in 2018. OTOH, he would do well if demand soars...

No one seems to be discussing the implications for electricity if natural gas prices increase too much.

Here in rural Iowa I have been using LP for a back up to my corn stove. With LP prices rising to the area of $2.00/gal or more retail, I am finding that electric heat is about the same price now. Plus I do not have to buy a full tank which can run $800.00 for 400 gals.. I know many heat with LP since natural gas is largely unavailable in the country.

I'm now using electric space heaters as back up on days that are too warm to start the corn stove which is difficult to regulate in warm weather. If others figure this out, there may be a shift to electricity in the country.

I would expect a shift to electricity at some point if natural gas prices rise sufficiently. Electricity prices seem to be more stable at least around here. I understand some places have a whole regulatory process to adjusting electricity rates. This is a definite advantage over LP gas since its price seems to vary a lot and change much more often.

Hi x,

I'm not too thrilled with the prospect of using more electricity going forward, but over the past twelve years electricity rates locally have increased by 28 per cent -- less than the rate of inflation -- whereas home heating oil costs have tripled. And as previously noted, I'm paying $1.25 per litre/$4.70 per gallon for propane, so that's completely out of the running. In the next month or so, I'll be installing an electric water heater to further reduce my fuel oil consumption. I had hoped it would be a heat pump water heater but there were logistical hurdles that proved insurmountable, principally lack of space and restricted airflow.

Cheers,

Paul

isnt a large part of iowa's electricity currently natural gas generated ? it would seem that for the short term, electric rates would track ng, wind power may have an impact down the road.

As of 2006, Iowa's electricity generation was 76% coal-fired.

http://www.theoildrum.com/node/3744#comment-320940

It could be, although I thought most of their generation was coal-based. In any event, I'm in Atlantic Canada and our provincial utility is roughly 75% coal, with the balance being a mix of hydro, wind, tidal, oil and a small amount of natural gas (e.g., combined-cycle peaker plants). In two years time, NSP should have 300 MW of wind on-line, up from about 60 MW today so we seem to be moving in the right direction.

See: http://www.nspower.ca/about_nspi/in_the_news/2008/03202008.shtml and http://www.nspower.ca/about_nspi/in_the_news/2008/03172008.shtml

Additional tidal power and imports from the massive Lower Churhill Falls project could also be in the cards and I'm hoping this will allow us to get off coal altogether.

BTW, neighbouring New Brunswick should have 400 MW of wind up and running by 2010 and even tiny Prince Edward Island expects to have 200 MW in place by then, and their peak demand is just over 200 MW.

Cheers,

Paul

Chevron discovered an estimated 6 trillion cubic feet natural gas field in Vietnam:

http://www.iht.com/articles/ap/2008/03/26/business/AS-FIN-Vietnam-Chevro...

Six trillion cubic feet of natural gas is the BOE/barrel of oil equivalent of a billion barrels of oil in BTU's.

I know that an extra billion barrels of oil pushes peak oil back by only 6 days or so (1000 million barrels/75 million barrels/day )/2 = 6 days

Does anyone know how many days each trillion cubic feet of natural gas pushes of peak natural gas?

"hell no we wont go not to fight for texaco

EIA has also published the Natural Gas Year-In-Review 2007 this month, dunno if that's fresh off the PDF or not. Lotza inneresting factz - exports to Mexico down, LNG up, more pipeline capacity, rig count stabilizing, stocks high.

Nothing about that compressor station exploding in Kentucky - or was it Tennessee? They patch that up yet?

With respect to US natural gas production, the trend is not all that clear to me.

If we look at recent US production, it has actually increased a bit in the last two years:

Natural gas reserves have been growing fairly steadily:

The Year in Review tells about significant activity in building new pipeline. It is my understanding that some of the new tight gas and perhaps shale gas was shut in, because no pipelines were available. Now that pipelines have been built, this should help new production.

We know that there is a decline in conventional natural gas production, but exactly how that balances out with the increase in unconventional natural gas is not that clear to me.

Natural gas prices in the recent past have been low in relationship to oil prices. If the historical differential should hold, or even shift to a higher relativity for natural gas, than it seems like the higher price would encourage unconventional natural gas production. If there is a choice between higher natural gas prices and no electricity or no heat, it seems like we may choose higher natural gas prices.

There is a huge difference among oil, natural gas, and coal in price per BTU. If the natural gas price ever increases to near the oil price, it seems like a lot of otherwise uneconomic natural gas would become economic.

Nate, I've had my eye on NG after I read a post by Dave Cohen on TOD awhile ago. One plot I kept up with was the EOG resources plot showing the base decline rate increasing about 1% per year towards 33% recently. However, they stopped providing this on their website.

North American peak in NG and world peak in oil are occurring at about the same time. Unbelievable isn't it?

European peak gas is somewhere between 2007-2009, too. Scary. Peak Coal Imports in Europe, according to my estimation will be between 2007-2011.

Insteresting times, indeed.

I am recalling that well test I posted on drum beat a while back: http://www.scandoil.com/moxie-bm2/by_province/americans_onshore/usa/whit...

I ended up guessing 75 trillion cubic feet of gas from that if the Bakken play has 100 billion barrels of oil. So reserves might grow 30% or so, though it won't come out any faster than the oil I guess. Of course, it it exists, it might all be wasted on tar sands or ethanol.

Chris

Could anybody tell me how to find the price of North Sea natural gas on the Internet? thx

Euan cited this source when he was analyzing British natural gas costs. I notice the tables in the back give prices in pence per kWH.

http://www.berr.gov.uk/energy/statistics/publications/prices/index.html

and also price in Japan, and anywhere in the world

My understanding that Japan's natural gas is all imported LNG. A lot of LNG is priced based on long term contracts.

This is one subscription source that talks about Japan LNG.

http://energy.einnews.com/news/japan-natural-gas-prices

The EIA puts out some out-of-date annual natural gas price data by country (latest through 2006):

See heading "Natural Gas Prices for Selected Countries, Recent Years (U.S. Dollars per 10^7 Kilocalories)"

http://www.eia.doe.gov/emeu/international/gasprice.html

Saudi Desert's Gas Mirage?

Boast of Vast Reserves Faces

Growing Skepticism as Firms

Go Dry in the Empty Quarter

By GUY CHAZAN and NEIL KING JR.

March 25, 2008; Page B1

Saudi Arabia's boast that its southern desert region contains vast reserves of natural gas is facing growing skepticism, amid a string of exploration setbacks by international oil companies operating there.

The kingdom had hoped that gas in the Rub al Khali, a vast desert that translates into English as the Empty Quarter, would be a key source of fuel for its booming economy. If the region turns out to be as empty as its name implies, Saudi Arabia runs the risk of a gas-supply crunch within the next decade at today's rate of demand.

South Rub al Khali Co. so far has failed to hit large pockets of natural gas.

If that happens, and the kingdom has less gas than expected, it will be forced to divert more of the oil it produces for its own use, leaving less to fuel the rest of the world's cars, airliners and factories.

Pessimism about the Empty Quarter was fueled by French oil company Total SA's decision in January to quit a consortium exploring for gas in the region after it drilled its third dry well. "We don't see any way forward after [these] results," said Christophe de Margerie, Total's chief executive, in a recent interview.

Saudi Arabia has proven gas reserves of around 250 trillion cubic feet, according to British oil giant BP PLC, the world's fourth largest after Russia, Iran and Qatar. But most of that is caught up in producing oil fields, and not available for use. New discoveries have fallen far short of expectations. Meanwhile, the kingdom is seeing a huge increase in domestic demand for the fuel as a feedstock for everything from desalination plants to heavy industry and power generation.

Saudi Arabian Oil Co., the state-controlled oil giant known as Saudi Aramco, forecasts domestic gas demand will nearly triple by 2030 and is on a drive to boost the kingdom's reserves of nonassociated gas -- that is, gas from wells that don't contain any crude oil -- by 100 trillion cubic feet over the next ten years.

One of the world's largest deserts, the Rub al Khali is one of the most-inhospitable environments on earth: temperatures can reach 131 Fahrenheit. Former U.S. Secretary of Defense Caspar Weinberger once wrote that Rub al Khali "makes Death Valley look like a summer resort." But it has long been seen as the key to Saudi Arabia's gas-supply problems. The hope is that the region will add a significant fresh stream of natural gas by 2011.

Saudi Arabia has been off limits to foreigners for exploration, but five years ago it invited foreign investors to help it develop gas deposits in the Empty Quarter. That marked an evolutionary leap for Aramco, which has barred the big international operators from exploration work in the kingdom since the company was fully nationalized in 1980. The unraveling of these partnerships, should they fail to hit large pockets of gas, would be an embarrassment for a country that prides itself on being awash in hydrocarbons.

Saudi officials are confident there will be big finds. "There is still reason for optimism," said one. "We don't know what the success will be but the geologists are still hopeful."

One former senior Aramco official, however, remains skeptical. "If there was a lot of gas there, we would have been exploring it ourselves," said Sadad al-Husseini, former head of exploration and production, who retired in 2004. He spent several years overseeing gas exploration in the Empty Quarter in the early 1970s. "It is just unfortunate that so much money has been spent to confirm what we knew already," he said. The companies declined to divulge costs.

Mr. Husseini is among a growing contingent within Saudi Arabia that believes that the kingdom's whole gas strategy is misguided. With signs mounting that the kingdom overestimated its available gas supplies, Mr. Husseini said, "the consequence is that we need to go back to the strategy we had before, which is to make better use of oil, to be more efficient, and to be more gradual in our industrialization."

Total was a partner in one of four international consortia created to drill in the Empty Quarter. The company it formed along with Aramco and Royal Dutch Shell PLC -- the South Rub al Khali Co., or SRAK -- was awarded the largest concession, an area the size of Kansas. But the results have been disappointing. "We see the ingredients of a hydrocarbon system," says Malcolm Brinded, Shell's head of exploration and production. "We just haven't found them all together in the same place."

With Total gone, Shell will now have to shoulder more of SRAK's exploration costs. But it says it will stay the course. Shell Chief Executive Jeroen van der Veer recalls an incident in the 1930s when the company was asked to take part in an international consortium exploring for oil in Saudi Arabia. A famous telex, still in Shell's archives, declined the offer, saying there was no oil in the kingdom. "I don't like to make the same mistake based on three wells in an area fives times as big as the Netherlands," Mr. van der Veer says. None of the other foreign companies working in the Empty Quarter have found gas in commercial quantities either.

There has been some good news. Luksar, a joint venture of Aramco and Russian producer OAO Lukoil, last year reported discovering some hydrocarbons at one of its wells. Sino Saudi Gas, which brings together Aramco and Sinopec International Petroleum Exploration & Production Corp., also announced initial gas flow from one of its wells, though it's too early to say how much gas is there. EniRepsa, a consortium of Italy's Eni SpA, Spain's Repsol-YPF and Aramco, has found nothing substantial.

"They've only scratched the surface in terms of the search for gas," says Iain Brown, a Middle East expert at oil-and-gas consultancy Wood Mackenzie. "There's a long way to go before the potential for gas has been fully evaluated."

But as the failures build up, so are the costs of drilling each well, which has shot up to around $70 million, up from the $30-$50 million projected in initial budgets, according to industry observers. Rigs also are scarce, and wells on some blocks are taking longer than expected to drill.

From the start, the ventures had relatively low rates of return; the companies have to sell any gas they find to Aramco at 75 cents a million British thermal units, minus a fee for transportation of around 15 cents a MMBtu.

Conditions on the ground are tough, too. South Rub al Khali had to build its own airstrip so workers could be evacuated in an emergency. Drinking water must be brought in from the nearest town 190 miles away. Sandstorms mean workers have to wear respirators.

Analysts say the Rub al Khali might not even be the best place to be looking for gas in Saudi Arabia, and that the Saudi Aramco Reserve Area in the east of the kingdom -- a province off limits to foreign companies -- has by far the most-promising acreage that covers an area that is a little larger than North Dakota.

Yet companies still leapt at the chance of working in the Empty Quarter, hoping for a rare foot in the door in Saudi Arabia's oil-and-gas exploration sector and an in with Aramco. But Total's Mr. de Margerie says there was no point in staying in SRAK just to keep on the right side of Aramco. "You have to be pragmatic," he says. "If you start to do things to please, your company will be dead."

Saudi Desert’s Gas Mirage?

Just provide an excerpt, not the entire article.

Will do going forward. Thanks for pointing that out.

Rgds

WeekendPeak