TOD POLL: Where will crude oil close 1 year from now (12/31/2008)?

Posted by nate hagens on December 30, 2007 - 11:39am

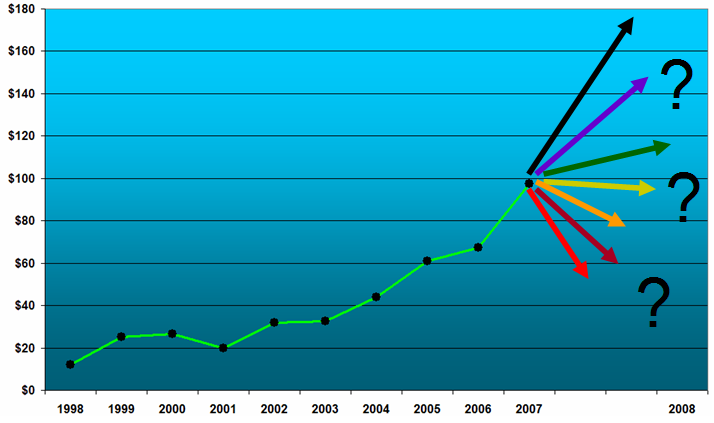

2007 witnessed a rally from $67 to $99 - we have one more day to kiss $100 on the price of front month crude - it may be close. Here is a POLL, open until Jan 1, where you can post your prediction for oils closing price for year end 2008. As previously discussed, sometimes the shape of the chart, chronological movement, and volatility can tell more of the underlying story than a closing price. Here we are asking just for the price, 12/31/2008.

Click to Enlarge

Here is the POLL. Here are the choices:

1) Below $50

2) $50-$65

3) $65-$80

4) $80-$95

5) $95-$110

6)$110-$130

7)$130-$180

8)Above $180

9)I have no freakin' idea. Futures distribution centers on $90, so thats more likely than anything else.

Discuss, debate, predict, and happy new year!

Contact

- Content: editors at theoildrum dot com

- Tech support: support at theoildrum dot com

License

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.

I think it's really difficult to make this prediction. On the one hand, increasing scarcity should push oil prices up. The declining US dollar also tends to inflate oil prices. A steep rise in oil prices seems like a no brainer.

However, the collapsing US economy could push oil prices down. Furthermore, the European and Asian economies could also follow the same path, because European and Asian central banks bought so much bad debt from the USA. We could be looking at at 1930s style worldwide depression. That should be bearish for oil prices.

But then again, it depends on how much the countries around the world are willing to crank up the printing presses in a desperate attempt to print their way out of a debt crisis. Look at some of the recent currency collapses we've seen: the 1994 Mexican peso crisis, the 1997 Asian financial crisis, and the 1999-2002 Argentina economic crisis. In these three cases, we saw currencies collapse, which inflated other prices (like oil and gold) if priced in pesos or Korean won, for example.

So, I hate to say it, but I just don't know what oil will cost a year from now. I can't even say if it will be more ore less than it is now. I hope that gold goes up, since I'm heavily invested in it, but I'm not even certain about that.

regards,

Oz

Ditto Oz, The variables seem to get greater each year. I think the printing presses will win out, however, and desperation to keep the status quo will push prices of everything much higher before depression reins in. I vote for over $150.

This is going to be a tough call. Economic slowdown in the US seems almost guaranteed. But supplies are so tight and geopolitical events so numerous I have to think it's going to stay fairly flat if not go up a little.

What Oz said, seasoned with a fear that we're due for one of the potential disasters itemized by shargash, puts me in the $130-$180 camp. Absent a disaster $90 sounds about right for recessionary 2008.

My guess is that we'll end the year with $150 oil. There will be more dollar depreciation. Right now, the only one's financing the US 600B current account deficit is central bankers. A good chunk of that is for oil and it isn't going away without a much lower dollar. There really isn't any resolution to this crisis without a lower dollar.

Add to that the idea that total liquids could be down again this year and you have an environment for higher prices worldwide not just in the dollar zone.

So, for me the instability in the US economy will serve to increase prices not decrease them. So, people walk away from their McMansion and default on their mortgage. They still have to drive to work. Sure, 25% unemployment a la the Great Depression would reduce crude demand a little but Ben Bernanke has stated that he is not going to allow that. One million USD in each home debtor's bank account and all problems are solved--to the detriment of dollar holders worldwide.

So, $150 would be my guess.

Can't tell if you're joking. How exactly will Bernanke transfer dollars into the average home owner's bank account? As the dollar drops in value 50%, my estimate would be the ave union member might get a 4% raise (published CPI)-non union members might be a nominal decrease (down more than 50% in real dollars).

I don't think it will work out that way. The problem is that as defaults start rippling through the financial system, the amount of economically effective money is going to decline. With fractional reserve, new lending means new money created---and hence defaults on loans means money is destroyed.

The central banks will attempt to counteract that effect, but they will not be able to fully do so because the private banks themselves will be unwilling to use their new reserves to lend since their own situations will be so dire.

I don't see gold going up in this environment.

Previous currency crises (Mexico, Argentina) occurred when debt was issued in different currency than the home currency, and with Argentina, they tried to keep a farcical currency peg.

This isn't likely to happen in the developed world: US banks made loans in USD, UK banks made loans in GBP and Euro banks in Euros.

I agree. This is going to be a tough year to make a guess. To many conflicting forces. I opened the link to say that, and everyone had beat me to it.

So I decided to use my amazing psychic gut! It works kind of like Socrates daemon.

http://en.wikipedia.org/wiki/Daemon_(mythology)

My gut says wild volatility with it plunging as low as 80 and as high as 130, but settling back to about 100.

So I guess my guess is: 5) $95-$110

I voted yesterday. Today I wanted to see what the totals are since then, but the poll won't let me look unless I vote again. Won't this skew the results?

It seems I remember there being discussions of 2008 seeing quite a bit of oil come on line compared to recent years. Also, the recession should be kicking in good by mid-year, and OPEC is supposedly picking up production.

All that is balanced by decline rates and growth in China, India and oil producing nations.

I voted for 80 - 95, or whatever it was, but I'd not be surprised by any range. Volatility should be the hallmark of peak, so anything goes.

Cheers

PS. Happy New Year! We just had ours here in East Asia.

Oz,

your comment reminds me so much of the following:

(From 'The Princess Bride', in case you hadn't guessed :-) )

Inconceivable!

AKH

From here:

http://financialsense.com/fsu/editorials/lalani/2007/1228.html

I think that is the best one-line summary I've seen yet for what to expect.

Energy is essential. McMansions are not.

I would have liked to have one more category in the poll. The $130 to $180 bucket is a bit broad, so you will pick up quite a few folks in it. I'm guessing around $150 at end of year (but that depends on so very many things). I'm expecting an average of $110, with perhaps a spike to near $200 and a dip to perhaps $75. LOTS of volatility.

#7 $130 to $180. Nice broad range. Since production has been flat in the face of growing demand for 3 years now, some thing has to give. Stocks are being drawn down, and the poor have already tightened their belts. Now the big guys get to bid against each other, and since we have outsourced most of our heavy industry, a US recession will not cut demand very much. After all, we need to feed those big screen TVs and our internet servers.

Like Oz, I'm all over the place on this one. I do think there will be a world-wide recession, but I don't think it will have a dramatic downward effect on oil prices, because the decline in consumption will be roughly the same as the decline in production caused by depletion. And if prices decline much from where they are, some of the more expensive production will come offline, and the capital investment needed to bring new production online will be delayed.

On the other hand, there are some possible events that could push prices very much higher than $130. Taken individually, none of them are likely to happen in 2008, but taken in the aggregate, I think there is a pretty good chance one or more will happen:

-- War in the Middle East (beyond what we have currently)

-- Civil war in an oil producing country

-- Pakistan losing one or more nukes

-- Natural disaster(s) in oil producing regions (e.g. bad hurricane season

-- Saudis admit (or cannot hide) that Gahwar is in decline

I think if I'm wrong, I'm likely to be wrong on the low side.

#6 $110 - $130...oil prices seem to have dipped during the last quarter of last year and this year, due to mild winters and thus lower demand. So, looking into my crystal ball, I anticipate dollar depreciation and firm summer demand spiking oil up over $130 sometime during the year, then a seasonal dip down less than $130 by the end of the year.

$92.50 is my bet for this time next year, but we may see $120 before then.

Any particular reason for forecasting a closing price lower than today's? As stocks have been drawn down for two years (according to EIA numbers), if this continues the only way for prices is up. Unless there is significant new production, above depletion, or unless there is significant lowering of demand. If these factors are not spot on, in terms of moderating demand or increasing supply just enough, I can't see prices being roughly where they are now, except as a point on a wildly fluctuating curve.

Prices have risen 60% this year, when there hasn't been any really bad geopolitical news, though the US dollar has slumped somewhat. I can't imagine next year will be any more supportive of a stable oil price.

In terms of effects on people, I think only significant new production, that is, an increase over today's production of around 2 mbpd, would keep the world stumbing along as "normal". I don't expect that, but who knows?

2007 is ending on a price high and so I'm guessing 2008 may not. I think the price trend will stay intact but am simply guessing that the end of 2008 will see prices off highs reached during the year.

Well Euan, last time I won a bet I had a lot more hair and a lot less wasteline...

But 90- 110 seems fair. So 100.01 USD / bbl on 31/12/08

Why?

If the Western Industrial economies tank, the usual madness in the middle east will offset it, keeping prices high.

And of course Russia has learnt that a) high oil prices mean luxury goods and b) oil is a potent weapon.

I reckon on about 2 years of plateau pricing as western industrial economies try to cope and mitigate, cooling down, belt tightening,etc. But before the markets finally realise that Oil output cannot grow.

Then the shit hits the fan ultimately when we wonder where all the rich tourists are for the Olympics in 2012.

Mudlogger - I too suffer from expanding waistline syndrome. I can't wait for the 2012 Olympics. I suspect that infrastructure may be the first ever built on hot air power.

Have a good one Mudlogger!

You too Euan, have a good one.

best wishes to you and to all at TOD in 2008.

Decline in housing sector of economy plus high energy prices will sap spending power of the consumer and send US into severe recession by year's end.

Inflation of 8 to 10 percent will add to this straining of personal and business budgets to make recovery difficult for the next two years. As unemployment grows to around 8 percent or slightly higher, transportation fuel use will decline by the same percentage. This will cause oil use in the US to decline by at least 6 percent by year end (75% of oil is for transport in US). The balance of the world's developed economies will not feel as much pain, but they will not be growing much either. So world demand for oil will remain in balance (barely) with supply and price at year end will be below or near what it is now.

If a major political or military event occurs in the Mid East, price will be higher than now.

"as unemployment grows to around 8%" I got a thought on that I maybe wrong but there are already stories about illegals headed home from lack of jobs to cost of living increasing in the US with the weak dollar.And with a weak dollar less spending power for the money sent home.But as US citizens lose jobs TPTB will really crack down on illegals to open up jobs for US citizens.Along with a hostile view by those that employee illegals.

Please take a moment to review the Best of The Oil Drum Index and reply here with your favorite articles that I've missed.

http://www.inspiringgreenleadership.com/blog/aangel/oil-drum-best-index

Andre'

------------------------------------

Peak Oil, Climate Change and Business

Free, Bi-Weekly Executive Briefing

www.inspiringgreenleadership.com/peak-oil-climate-change-and-business

In current US$ the price will be down a lot as I believe the world econmy is going to turn down a lot this year and sooner too. Before that the price will shoot up. On the volatility poll I called for max 130 and low around 70. If it is only WTI on NYMEX then it will stay much higher in inflated dollars but the world wide justified price will drop.

Does anyone have the data (and a graph) relating price to cost of production. I can't recall where and when I last saw that but think it will be a more important issue when the global economy goes.

The only question in my mind is "exponential or asymtotic?".

Up. It will go up.

Ultimately you're probably right (that it will only go up), but a worldwide depression will lower prices and could lull us into thinking we don't have a problem.

A worldwide depression will also remove much of the cash that could be used for the transition.

Andre'

------------------------------------

Peak Oil, Climate Change and Business

Free, Bi-Weekly Executive Briefing

www.inspiringgreenleadership.com/peak-oil-climate-change-and-business

I expect a price increase of 25% by the end of 2008, but other measures are important. Oil will end the year at $125/bbl, 79 euros/bbl, 10bbl/gold oz. US headline inflation will have run at 18% from today to the end of next year.

I expect the coming year will be one of the most tumultuous we have experienced, and the following scenario is how I reached my conclusion on the price of oil. Sorry for the lack of links, but this is a compendium of thoughts found throughout TOD and Calculated Risk.

Oil begins 2008 at $100/bbl, 69 euros/bbl, 8.5bbl/gold oz. By mid-spring major banks, insurers, and lenders will race each other to bankruptcy. Gasoline will cost an average of $4.49 at the pump, and housing prices will have fallen an average of 22% around the country, 40% in California and Florida. Headline inflation will run at least 12% while the government claims core inflation is only 4.0%.

Durham, NC, will officially run out of water. Other municipalities throughout Alabama, Georgia, and the Carolinas will suffer similar fates. Fires will spread throughout the bone-dry forests and into the suburbs, and the firemen will have no water with which to fight. A mass migration will begin from the smoke-covered drought-stricken area to the rest of the country. Tent cities and soup kitchens will appear in open land from Florida to Maine and throughout the Mississippi River Valley, and local authorities will have difficulty coping with the load. FEMA and the military will be hard-pressed to provide rations and water for the refugees.

By mid-year the equity markets will have fallen 50%. Debt write-downs in the US at this point will total over $1.2 trillion, and credit will be mostly unavailable. The tech sector will see their orders dry up. The southern half of the country will continue to suffer through severe droughts, and dust bowl conditions will develop in New Mexico and the Texas panhandle.

In August the party conventions will select their candidates, but neither party will have a strong plank advocating direct action about the climate or energy crisis, focusing instead on impeachment issues, how to handle the situation in the Middle East, control of immigration, and most importantly what must be done to maintain the US good way of life. The Republican convention will be especially contentious, and the Social Conservatives may well join the Neo-Cons to form a hard-right coalition and splinter the party.

A category 5 hurricane will form in the Gulf of Mexico south of Houston and rip through the US oil and gas production fields in the Gulf. The eye will wrap around to head northeast across New Orleans and stall over Alabama and Georgia, ending the widespread drought with drenching rains that fill the reservoirs to over-flowing and flood the rivers throughout the South-East. Casualties will be low because 70% of the population have left the area.

Unemployment in the US will reach 7.5% in the fall, and the GDP growth will be negative. The rest of the world will suffer more and more of an economic downturn as US imports fall to 70% of their previous levels. Energy demand destruction around the world will take hold but not enough to match the drop in supplies, and the oil price will not drop. As food prices climb the number of starving people in the world will treble to 2.4 billion by the end of 2008.

After the Democrats win a landslide in the elections, the lame-duck President will order the withdrawal of troops from Iraq. Iraq's national government will divide itself into three regions, and those regions will begin to mobilize troops and weapons. The Saudis will send troops to Sunni-Land, and Iran will send troops to Basra and Shia-Land. The Kurds will ask Turkey and the US for protection in return for access to their oil, but the Saudis will move into the area and take both Turkey and the Kurds under their “wing.”

Oil will end the year at $125/bbl, 79 euros/bbl, 10bbl/gold oz. US headline inflation will have run at 18% year to year.

I surely hope I am wrong and am blowing smoke with no fire. But there are so many things that are near tipping points, and I just don't see the leadership available to address all these problems.

That's why I am keeping my footprint small and my profile low.

Sam Penny

the Prudent RVer

Worst case scenario - it would take several years to play out. Events seem to unfold in slow motion. I've been bugging friends about the subprime mess for at least a year.

Come on now, Sam. Don't hedge your bets. Tell us what you really think...

SubKommander Dred

...you forgot to add the bit where Superman comes and mends it all...

I'm not saying some of this stuff won't happen but I'm with the poster above, the timeframe is wrong.

5) $95-$110 (a battle between recessionary forces and dwindling supply: we are still in Phase1 of this so not a huge impact)

Nick.

I have a feeling this thread may get quite interesting, hehe.

EOY 2008? Front month close $130 to $140 I believe. We may well see that $140 by May or June. Refiners are about as tight as they can be on margins already, they will have to pass costs on, if for no other reason than to keep throughput at a level they can keep up with. Gas will probably be near $4/gallon I would think.

At the risk of being repetitive, I do not believe this is a refinery capacity problem, but one of supply.

Assuming the system holds together the rest of the year should be similar chart-wise to this year. Dip then Consolidation phase followed by return to highs near EOY.

An earmark of a tight resource situation is increased volitility. This is totally hidden by the headline chart, but nevertheless it should worsen as supply tightens further.

The only way I see to avert this is to have a bigger player have some problems and drastically curtail demand. So far only small players have dropped out of the demand side.

Of course if something happens like an excessive water carry-over in Ghawar that the Saudis can't hide then forget this low-ball estimate, lol.

I agree a U.S. slowdown seems more and more certain and should affect demand. But I don't think it will happen fast enough to hurt demand to the point where it will ease the crude price substantially. World demand vs. probable failure to keep ahead of production slippage should keep the pressure on price.

So many factors, assuming the big ones stay on their present course, the price will have to go up considerably to maintain balance.

Hmmm. How about exactly $100.00 for all US domestic oil, legislatively capped at that level after a fast rise towards $200, to discourage 'speculation' and 'keep gasoline affordable'. This is the sort of bonehead move which might pass for action in the USA, and it is supported by the fact that it would make all my call options worthless. Black market rates a good deal higher. Subsidies and tax breaks for oil exploration significant but too complicated for anyone but posters to this website to calculate actual price.

International exported oil increasingly price-irrelevant as buyer and seller trade more in geopolitical extortion/exchange of leverage than pure fiscal terms. Real terms increasingly kept secret.

I don't BELIEVE this, just goofin' around. we shall see.

I think you got it right. And after that, we'll start to use the Carter gas coupons that are currently sitting in the salt caverns in Kansas.

The dark green arrow. That is, 120 or a bit more, 130, which inches into the top category.

Producers will keep up their stuff, they like to be paid and reassure. The recession will hit the poor; demand destruction so-called will not occur. So barring wild movements in the month/weeks at end 2008, slowly rising price, set to continue. About 130 or a bit less or more.

$130-$180, based purely on how much oil has risen in a fairly quiet geopolitical and weather year (as regards oil production and processing). A 35% rise next year would be modest by this year's standards.

Could not agree more. I can recall just this year how we saw the floor go from $60, $70 to $80 and it now it appears to be pretty well stuck at $90.

IMO the only thing holding it back is the dreaded $100 psychological barrier as soon as we puncture — sometime in the next couple of months — that it's off to the races.

I wouldn't be a bit surprised to see $130-150 come mid May or June. People are waking up to the fact that we are at peak. Meaning we will be pricing for the first time at the margin. God forbid we start pricing oil for what it's worth. ;)

And don't get me going about demand destruction. If we aren't buying oil ChinaIndia will have no problem soaking up the extra barrels nevermind the fact that there is plenty of inelastic use here in the US.

those "couple of months" sure passed quickly ...

I have to say #9

A lot depends on what the U$S does and how the elections go.

"A lot depends on what the U$S does..."

This is a really good point as more and more countries and other entities are switching to the Euro, a collapse of the dollar is becoming a real threat. Probability of this is growing by the day. Oil in dollars would then go through the roof. How far are we from that ?

7)

I have no rational reason other then the news has been slowly bad for a long time and I "feel" it will get much worse very quickly

The US dollar is likely to fall in value at least 10%. Too many dollars in China and Japan to allow a precipitous fall, and the dollar has a good US, Canadian, and Iraqi oil asset backing. Paradoxically, the falling US dollar increases the value of the asset backing of the dollar. There is a fundemental asset value behind the dollar.

Q1, the "reef fish" of the financial markets flash this way and that as the US debt debacle is exposed to public view, and the adjusting dollar result in oil price adjusting to $US110.

Gold commences a rapid return to its longer term average of around 15 barrels of oil (about $US1500).

Q2, life goes on as normal, panic abates, oil prices fall to $90 +/-

Q3, Olympic mania, positive 'sentiment' regional fuel shortfalls in Eurasia (especially diesel), better 'other liquids supply', then, on historical precedent a hurricane in the Gulf of Mexico locking in a Mexican or US oil for anything from several weeks to several months.

Q4, Following the oil 'shut in' price peaks, Eurasian demand, Southeast Asian sweet hitting $120 due to demand/shipping costs, Saudi bilateral 'close-ins' with preferred partners with gold backed currencies (Russia, Germany, China starting) steep declines in Canterell production, Saudis drop production to 'milk' the price, USA decimated service sector drops consumption, USA manufacturers start to get legs, China manufacturing in dire straits and demand growth cut off at the knees, year ends around $US115.

Q1 2009 - genuine demand destruction across the globe due to recession and price, oil starts to slide toward $US85. (soon to be reversed).

Lorenzo

My guess is $110-$130 at y.e. '08.

We should note that Zimbabwe, for all the wrong reasons, has probably achieved Kyoto and way beyond in CO2 reduction already. Is this demand destruction?, or just a blip before a return to 'normality' in oil consumption when democracy returns to that troubled country?

But Zimbabwe's population is only 7m, so its effect on world oil consumption is minimal. My feeling is that high energy prices will permanently stifle its economy,as they will ultimately the economies all the poorer nations. I don't know how far this has yet to go, or how much demand loss this will cause.

OK, on 20 November WTI set a high of $99. Since then a floor has been established at $87, on 10 December. Today we have $96. Looking ahead to the end of 2008, in attempting to predict the price one must take into account the forecast demand growth.

http://www.cnbc.com/id/22256608

So for prices to fall below the current floor and stay down, all of this demand growth must be destroyed. And even OPEC who are worried about lower growth due to the poor "economic outlook" still see demand increasing 1.3mbpd.

There are 2 ways to lower the price. The first involves lower demand. Markedly increased unemployment, reducing driving and spending (and hence demand for goods) would lower the demand for gasoline and hence oil. How quickly can you see demand reducing due to this, and by how much during 2008? I can't really see a credit crunch induced recession getting that bad that fast to kill off all that forecast new demand, and then some of the existing demand, in order to get the price of oil down.

The other ways to lower the price is to increase supply well above demand. It seems to me that a key aspect controlling the price of oil is the amount of surplus supply available in the world. The bigger the supply overhang, the lower the price. Currently, surplus capacity appears to be minimal. Hence oil at $90+. It seems more likely to me that a hurricane/terrorist attack/infrastructure failure/you name it/ will occur, reducing supply and leading to higher prices in order to keep demand and supply in balance.

For oil prices to drop, supply must increase dramatically (unlikely), or else demand must decrease significantly, without the price of oil increasing to cause this(possible but less likely).

For oil prices to rise, supply problems occur (very possible), or demand growth occurs (still likely).

I just cannot see major oil demand destruction happening during 2008 without high oil prices being a major cause.

Watching the demand/supply/price dynamic of oil over the past few years has been fascinating. And I expect 2008 to be even more interesting, as the volatility that exemplifies peak oil continues. I am picking a end of 2008 price of $130 - $180. Only massive unemployment can take the price down significantly from where we are today, and I can't see that happening rapidly enough over the next 12 months for that to occur. And that is one prediction I do not want to be wrong about!

Hello all TODers,

First of all I wish you all a Happy and a Safe 2008. Thank you all for your great contribution. I have been reading TOD religiously everyday for almost two years with amazement.

I have been waiting for oil to break $100 to make my first post but it hasn’t (yet). However, I do feel guilty of not contributing whilst reading information from TOD.

I do hope you find the following oil price forecast from the biggest (not necessary the brightest) brokers useful for further discussion. They are the latest forecasts:

2008 2009 2010

Credit Suisse $80 $75 $75

CitiGroup $80 $70 $70

Deutsche Bank $80 $75 $65

Goldman Sachs $80 $90 $80

Merrill Lynch $82 $70 $70

Morgan Stanley $80 $83 $85

UBS $74 $73 $76

These are all prices lower than today, and accounting for falling dollar in forward years, way lower.

Two or three of these investment houses are experiencing huge losses in SIV,derivatives, phoney money schemes. And I will guess few if any of the energy analysts at these outfits read the Oil Drum! But maybe they know something we don't.

At least they are all more realistic than the dart throwers at CERA (Daniel Yergin, Michael Lynch, etc.)

Welcome to TOD Mudbucket. All sorts of opinion here as you no doubt have seen. No matter what you say there will be someone disagree with you. Best accept that and move on.

I have seen the predictions from the august heights such as Citigroup. Have you noticed how prescient they were making all those subprime loans and creating the derivaities. Excellent reading of the sheep entrails if I do say so.

If you are reading TOD you at least think that we are going to have some difficulty concerning the price of pertoleum fuel. I doubt there are more than a percent or two of the readers who think supply/demand is suddely going turn around and prices of crude are going to drop 10 - 15 percent for the next 3 years.

Best Wishes for the New Year

Don't forget CERA's forecasts:

$100 Oil

http://www.theoildrum.com/node/3271

"World oil prices will drop to the low $60 range as long as the security premium in the world oil market does not rise," said Daniel Yergin, chairman of Cambridge Energy Research Associates.

Andre'

------------------------------------

Peak Oil, Climate Change and Business

Free, Bi-Weekly Executive Briefing

www.inspiringgreenleadership.com/peak-oil-climate-change-and-business

What does Yergin mean by "the security premium in the world oil market"?

Answer that and I suspect you'll know how he'll hedge on being wrong yet again.

The big banks just want to keep the system chugging along and their clients going hoo haah! You must know!

They are dependent on business as usual and cannot possibly change, their whole mindset, pointedly, as individuals, their own jobs and profits, are built on returns from resource extraction (indirectly to be sure, not detailed) so they talk the *talk.*

Many employees understand, realize what the real scene is - they are well placed to do so - but they have children and mortgages and figure they need to hold on till they are fired and the whole system falls apart.

After all, as an UBS employee said to me, if I can earn half a million in the next year, I can use that cash, etc. After that, like, duh, my son won’t get tennis lessons. *!!*

In the past year, I have seen 4 advisors from the UBS. 3 have been let go or fired, and the 4th calls me up to moan. He has ‘survivor guilt’ and sits in his cubicle..complete with security guards and leather chairs ;)

Hi Noizette,

Interesting post, as always.

re: "Many employees understand, realize what the real scene is - they are well placed to do so - but they have children and mortgages and figure they need to hold on till they are fired and the whole system falls apart."

What is going on?

Do they lack any sense of security in themselves, or ability to make moves or talk to (and/or confide in) anyone else?

Do they really believe they are doing well by their children?

"Survivor guilt" is tough. I know it best from my own childhood - but children are fundamentally trapped in their helpless position of being unable to protect others.

The point of growing up is to learn something different, isn't it? (?)

Agree that volatility is the name of the game in 2008! Which means the floor is open to wild speculation and that no matter how wild, there is a possibility that even extremes may be right.

Who would have thunk it, a 60% price range in 2007?

Reminds me of that guessing game used by charities where one estimates how many marbles or jelly beans are in a bottle. I'm feeling particularly lucky this year since I won such a contest just before Christmas.

I find I do better with such games if I throw out a number rather than pondering deep calculations about variables.

So, in the spirit of unscientific guesswork where all possibilities are open and no evidence is weighed, I'll up the ante and say, $200/barrel on 31st December 2008. A straightforward doubling.

And no, I don't want to bet on that. I could have very well said, $10/barrel, although I think that would mean one horrific depression with massive demand destruction. Even if things go belly up, I am anticipating price rises rather than falls.

Here ends my analysis.

Happy New Year!

We have our own betting pool going on at PO.com: The 2008 PO.com Oil Price Challenge. I'm for a low of $120 - reached on Jan 1! OMG WTF!

Price obtained by adding $100 to Yergin's old calls. Recycling, you know.

Things are bad. I predict they will become worse.

How about bets on how much Arctic sea ice there will be?

This one is a lot easier than the oil question: we know there is only 20% left, so it doe not really matter :) Ask the same question about Greenland...

I had a quick look at the Oil Price Challenge. When money is on the table it seems the speculation becomes far more conservative and less proned to risky highs and lows. Fair enough. One of the reasons I rarely gamble.

A few summers back, my wife and I were staying at an old farm house in rural Nova Scotia. We brought with us our house cat, a trusty mouser. One morning, a mouse ran from the cupboard and under the stove to escape capture. For two whole days our cat sat beside the stove fully awake and nary moving a whisker. Eventually the mouse made its move. It was a brilliant illustration of alertness and patience.

Watching PO unfold is a bit like that. One hears rumbles of movement, but nothing springs forth YET. Whether it is sea ice or clear signs of production or export decline with price spikes, I have an uneasy sense that someday the bottom will fall out.

Unlike our cat which knew what to do with the mouse, I'm not sure how I or anyone else will react once the evidence of PO comes to pass: not unlike Wile Coyote when he catches the Roadrunner. It's just that $200/barrel oil would not come as any great surprise to me.

I hope I'm wrong. $200/barrel oil would hurt the most vulnerable first. But I do see it as a real possibility, especially if Old Man Murphy of Murphy's Law fame (what can go wrong will go wrong at the worst possible moment) shows his hand.

There are just too many variables at work to see Murphy idle for much longer.

Cheers!

Dead center in #6, $120/barrel. Growing $40/barrel per year for the three or four years following. Since we seem to be providing reasoning...

I believe the price is set by exports, and that we'll be flat (at best) in exports over that period. $40/year is my estimate of the annual increase needed to keep demand at the current level in the face of increasing population and modest economic growth. I think we're overpriced right now, from a variety of causes, so use $80/barrel as the starting point. Reality is less regular than that, so say that I expect the actual price to fluctuate within about plus-or-minus $20 of that line.

6) 130-180 is a fair range for that time frame (post election, neglecting any wandering into WWIII)

For the rest of the year, key word is VOLATILITY. Average price for the year - around $100.

First quarter will be highly volatile, most due from economic unrest, and the balance due to demand shortfalls.

Still holding the $114(triple yergin) prediction for Jan 31(at 60% prob).

I put the QUAD yergin ($152) at a 75% probability for the year.

Things will likely calm for a bit at the beginning of 2Q08, with a short rest, and then a spike on Summer supplies in May and June.

Just like 2007 price may ease a bit (key word - 'may') over the summer, and expect demand to actually reduce (not - reduce expectation - actually be less)

After July, I expect some very weird manipulations as they start to prepare for the election ramp up.

After the election, win/lose/draw - we can expect some normality to resume in the markets and the world to end (just joking)...but a price spike is not out of the question.

BTW, as of Dec 20th(LI), we are essentially in a recession...will they actually call it in January...you figure...probably not.

110-130 with a range of 80-140+. I think we may also see a spike in Nat gas prices as well since there will be some fuel switching going on with high price of oil. I'd be very surprised if oil ever dips below 80 again barring a punishing, worldwide recession.

re prudentdriver

Good analysis. The one thing wrong is Saudi taking Turkey under its wing when it moves in to Kurdistan. Turkey is the dominant military power in the region. It has the biggest and by far the best army. They could march on Rydah if they wanted to, though they would probably be happy with occupying the oil producing regions of Iraq. Not the worst outcome.

After contemplating my navel for a few hours:

Oil is currently at 8 barrels per ounce of gold (the only true currency). Both oil and gold are subject to massive derivative trading volumes, so neither is trading at their "market discovery" price. (Since many traders do not take delivery, less physical is needed to satisfy the market).

Predicting the price then means predicting the continued success and motives of the future traders (which includes the central bankers not trading with a profit motive).

1. I think 2008 is the year in which gold breaks loose, and trades towards $2000 ounce, implying an oil price of >$200.00 per barrel, but...

2. Oil, despite massive demand destruction, stops being fungible (in the sense that you can not buy it on the free market).

My predictions:

1. Oil price ceases to have any meaning since it is not freely traded any more

2. Gasoline prices are allowed to find their true level - say $5.00 per gallon at the end of 2008

3. Diesel is rationed at $4.00 per gallon, if you can get it.

Francois.

I have long been navel gazing what I should do with my tiny saving. A gold coin I purchased in the spring has made me over 200 dollars now, which is pretty good considering my investment goal is to make up for inflation.

Trouble is, if one puts ones money in gold, then when very bad things start to happen, in the worst case scenario, you can have a hard time using gold to buy anything. Many times in history the selling and even possession of gold was restricted or banned by the government in order to protect the 'economy'.

Right.

Take care of essentials first - only excess wealth to gold!

Francois

Hi Francois,

Could you possibly elaborate on the reasons for:

"2. Oil, despite massive demand destruction, stops being fungible (in the sense that you can not buy it on the free market)."

A topic which was discussed here some time ago.

Still, wondering what your thinking is and why you see this happening in 2008, as opposed to, say 2012 or something.

5) $95-$110

A quick look didn't find anybody below 4... well, this is tod, after all.

3, and OPEC imo will be cutting production to hold this price sometime this year. Recessions are always deflationary... even in the seventies, when oil never fell y/y, oil price did not rise much when recessions were biting... so, with avg price in 2007 around 72, I pick 75 for end 08.

your stratergy is similar to mine (averaging '07). decline in the giants may be made up for with reduced demand (r-word or conservation). i dont hold much hope for additional "net" production in '08. i really wanted to pick 4) but when i did, i felt a tightness in the groin.

China added 8.5M net new cars this year, far more than the US, and this will be above 10M next year. This alone will add

1M barrels a day to Chinese consumption each year - so they have to bid up prices in USDs to force others out. They can speed up the currency appreciation to keep local prices from getting out of hand. My bet is that the US F150 truck owner with an Option Arm mortgage and 29% APR credit cards gets squeezed in 2008, to make room for 3 Chinese business owners with new Brilliance sedans, paid for with cash.

For my very first post:

Somebody linked yesterday to a story about GWB's Crawford ranch being off the grid. I can't find the original post but the link was wrong. Although the house is eco-friendly, it's still connected to the grid:

http://www.grist.org/advice/ask/2003/10/15/umbra-ranch/

Interesting link.

I don't think I would want to eat any of the vegetables coming from the Bush family garden as it is watered with filtered toilet discharge water.

Welcome to TOD. Good to have you on board, offGridInVT.

I didn't know that GWB's Texas Ranch was touted as "off-the-grid", but such speculation very well could have appeared somewhere, sometime back in the TOD blog. I remember reading before, here or elsewhere I can't remember now, how the Crawford ranch was noted for green self-sufficiency.

The article you quote states,... snip "How can this man, whose administration has gutted environmental protection as though it were a trout, care enough to recycle toilet water in his home? Who knows..." I suspect he does know how precarious the energy situation and environmental equilibrium is for the U.S.A. I would be more worried (and I don't have much faith in GWB's ability to do right) if he was showing signs of being absolutely clueless. As my family says, "It is better to be a half-wit than witless."

"In the land of the blind, the one-eyed man is king." Except in this case, in the land where Paris Hilton is newsworthy, the neo-cons look positively intelligent. (Being an outsider from the Great American Republic, this is what really worries me!)

This is a tough one Nate,

As many of the other readers here, I think there will be a lot of conflicting drivers to the oil price next year. For 2007 it seems like the annual arithmetic average will be around $75/bbl (even if it is close to $100/bbl) at year end.

A back of the envelope estimate some time ago came out with approximately ZERO economical growth in the world economy if oil prices gained more than $30/bbl year on year (assuming oil prices pulled other energy prices with it).

It looks like the US economy is headed for a recession, but on the other hand this may not impact growth in Chindia.

The oil price will certainly be subject to much more volatility the coming year, and could be all over the span during 2008 (could even make Yergin’s prediction for $38/bbl spot on …for some tiny time and make Mike Lynch correct for perhaps more than……….30 seconds during 2008), but I voted for the range $95 - $110/bbl at year end 2008 based on what I think will happen within the economy and how much price increases the global economy can take year on year.

IT’S THE SUPPRIME, CDO, SIV,RMB, LBO, ARM, BOR/OIS spreads, that makes this such a hard call.

Regards and a Happy New (volatile oil price) Year to all TOD contributors and commenters,

NGM2

My guess is $150. I don't have data on oil, but do on gold and silver which generally move with oil and against the US dollar; I my statistical analysis shows gold at $1,200 and silver at $30 at the end of 2008.

Hi,

$111

Happy New Year to everyone!

Dave

What makes this expecially hard is that we'll be right in the middle of an elections cycle and it's impossible to know what the folks in our beloved Congress will be doing to save us, but probably not much.

$145 if world events are similar to 2k7, $250 minimum if the ME stops playing nice and starts throwing fiery rocks at each other.

The Big Players have been pleasantly surprised that $90+ oil hasn't caused major hand-wringing, they intend to find out how high it can go, it's all extra unexpected billions to build up infrastructure at home.

Remember the attitude of the oil companies to our predicament:

'F**k 'em, let 'em freeze in the dark'.

8) of course :)

I think we are going to see surprising significant declines in production in th US, Mexico and Canada and the North Sea, along with production problems in Venezuela and Iran. Along with extreme volatility in Iraq and Pakistan. Also this is Bush's last chance to start a war with Iran. Next I'm betting on accelerated declines starting to become obvious by the end of the year outside of the "high tech producers". By September or October I expect serious questions about KSA capacity and at least on terrorist incident or unrest in the Emirates or KSA itself.

Finally we are due for at least one or two decent hurricanes in the gulf next year.

On the financial side I actually expect things to hold together longer than most people would imagine and although problems in banking will continue to spill over into a slowing economy I expect the brunt of the recession to really start near the end of 2008. This is a big train wreck but we can expect the central banks and China ( Olympics ) to dance till the bitter end.

So given all the above I really think we will see peak oil awareness go mainstream by the end of 2008 at the latest and in a sense the gloves come off as countries are emboldened to position themselves for a world short on oil.

On the price size I actually expect most of the price increases near the end of the year after august potentially over 200 plus including a weakening dollar. Before August we will probably be in the 90-130 range.

In 2009 economic/political/military issues makes it difficult to guess since little oil will probably not be freely traded with most exports tied into extensive coop agreements. So pricing may be high but the comprehensive agreements probably make it difficult to understand the real prices. This will be a sort of power down protocol but I doubt it will be fair. Europe for example will be forced to take a military stance and probably will fence with the Chinese in Africa. If the US has not invaded Iran it may target Venezuela along with a increasing action in Mexico.

The only reason we are not in Venezuela now is I suspect the plan was to start a war with Iran use that to restart the draft then expand later into Venezuela if the seriously reduce exports to the US. Also I think the US was hoping that Venezuela Chinese exports would increase thus in effect killing two birds with one stone once we decide to invade.

In 2010-2011 I expect this to start breaking down as parties renege on their parts of the agreements resulting in at least some open warfare. Also expect free trade to break down with high tariffs on Chinese goods if this does not happen earlier in 2009. The Chinese will be the bogey man of the post peak world.

More than 2008 but the point was I see a set of conditions being met at some point in the future that will permanently transition us into a very tense post peak future. 2008 will I believe be the transition year. But for the most part I don't think the problems will hit till near the end of the year so I'm not 100% doomer :)

Memmel: I wouldn't hold my breath waiting for a trade war with China. They are handing a whole lot of money to Wall Street (and that's just what the MSM has told us about).

Well once the recession turns into a depression and gasoline is still expensive the game will change. Note I don't expect to happen until after the status quo is disrupted and the world backs away from world trade. This return to high import taxes is in my opinion pretty much unavoidable.

Also this probably means the US dollar will be replaced at least inside the US. Most people say fiat currencies are not backed by anything but they are in my opinion backed by the faith that debts denominated in those currencies will be paid back in the same currency with reasonable inflation expectations. Thus widespread debt defaults seem to me at least to effectively destroy a fiat currency.

The greatest power the US has now is to default on the US dollar and when it becomes necessary to exercise this power the US will.

I guess I just don't feel that this game will be played forever with the gloves on so to speak. And China for a whole host of reasons is a easy target.

I think by 2010-2011 the concept of a "local" American/North American Union only currency will be very viable.

I just don't see how a fiat currency can survive when the creators of the currency only have debt in that currency they cannot pay and all their creditors hold the cash.

I mean at that point your either hyperinflate default etc but the currency itself is toast.

These concepts come from simply expanding ELP out to the national and international scale. The most critical factors in the next 5-10 years will be restarting local and regional then national economies. I think you will be surprised how fast a lot of fiat currencies and international trade will be unraveled and destroyed during the process. What survives will be critical trade and this will probably be subject to military political control sort of a return to the 1800's.

China at least as it exists today really has little to offer a world turning its back on globalization and the rest of the world needs the resources to rebuild local economies.

The real problem is China did not build itself up for the Chinese people they have really not benefited from the recent growth. China basically followed Reagonomics and the trickle down theory. It gutted America and it will gut China. What are Chines factories worth if no one will sell them steel except at inflated prices ? And they pay outrageous export taxes ?

The bottom line is we don't need global trade for wage arbitration once the western middle classes collapse.

We will have plenty of poor people local willing to work for meager wages.

And don't underestimate the need for a scapegoat over the coming years.

Certainly when is a big question but I don't see that whats going to transpire is all that difficult to figure out.

ELP must happen for better or worse.

If there was to be an attack on Saudi facilities which say dropped production by maybe a couple million barrels/day would that not help hide evidence of any actual physical decline in Saudi fields for some time?

Ok there would be a massive immediate surge in oil prices if this occurred but clearly the price increases wouldn't be blamed on peak oil.

Just wondering.

Hmmm, you've predicted all the nastiest things to happen right before the elections. Did you consider that when you wrote this?

I don't know where the oil price will be, but I want to vote this chart the absolute most honest chart posted on TOD this year...

http://www.theoildrum.com/files/crude_2008_poll.PNG

O.K., so it wasn't as artistic and mathematically challenging as many of the masterpieces of chart making we see on TOD, and it had to be very easy to make, but I am grading on HONESTY! This is the chart to use as a guide!

Prepare for all the scenarios shown as best as possible and you should be o.k.! :-)

HAPPY NEW YEAR EVERYONE!

RC

Heres my vote.

Most of the analysis here on TOD is focused on the supply side, which indeed is going to have problems going forward, (and eventually serious problems). But the other half of the 'price predicting equation' is demand. I think we are in for a period of enormous volatility in financial and commodity markets as the early skirmishes of the battle between a financial and a biophysical economy get underway. At the date of Peak Oil, which we may or may not yet be, we are still producing more oil on the planet than ever before (though on a 'net' basis this may not be true). This means that any serious demand change due to lack of money or 'credit' could trump the variables that have resulted in greater depletion and higher prices thus far - plus there are some megaprojects coming online next year. But at some point, there will be a paradigm shift when the 'hoarding' behavior begins, which might coincide with watering out of some of the larger wells, and geopolitical conflict. I most certainly believe the rules of the second half of oil will be dramatically different than the first, where economists plotted out next years production and could be reasonably certain they'd be within a couple %. This certainty will become a thing of the past. But these things will not likely occur in 2008...

As Matt Simmons showed a graph once, (which I can't find), we are in for a period of higher highs and higher lows - 2008 will a period of higher lows due to the global OECD economy moving into steep recession. I think we could see $120-$140 in the first quarter, but will have a whiff of deflation later in the year due to economic contraction. Since oil is still priced at the marginal barrel, and in my opinion, the futures market does not give balanced view of future dearth or surplus, we will overshoot on the downside, kissing $65 again before closing the year at $75, down 25% from here.

I am more sure of volatility than I am sure of direction, though I certainly lean towards a lower number in 2008, unless the dollar really sells off. 2009 and beyond though I expect much higher crude prices. Unlike some on this board, I don't believe we will ever see $300,400+ per barrel, as that would be so disruptive to the just in time system we have in place that normal market mechanisms will be superceded by state control and rationing of energy. Given the economic situation, this may be some years in coming.

I am rooting for higher prices in perpetuity because other than education, which seems to work only once established, price signals are all that people respond to. I hope that wind, solar, tidal, wave, geothermal, and other 'interest' paying energy sources are continually pursued even if fossil fuels take a short term drop in nominal pricing.

Stay tuned.

hmmmmmmmmm...........

My personal guess for 2008 would be of a severe slowdown( not a clear ressesion). The Fed will continue to bow to wallstreet and the white house by aggresively cutting rates and plowing piles of new cash through the discount window. there may be even more co-operation between world bankers to avert slowdown.

this will stoke demand for oil while devalueing the dollar by at least 15%-20% against the euro. by summer $4 gas will seem 'normal' and $3.50 would be seen as a bargain.

CPI will be setting at 5%, with real inflation at 8%-12%. This will cause ben bernake to come to his senses (I hope) oil will be at $130-$150 by mid-summer.

Then the real slowdown will start in ernest without fed intervention with stagflation being part of everyones vocabulary again, along with the misery index.

The second half of the year will be touch and go. The credit markets will seize (again) and the feds hands will be tied(china and eu will probably threaten to dump dollars if we continue injecting liquidity). if mexicos feilds continue to dry up then even with demand destruction oil will hang out at between $130-$150 per barrel.

the only other senario I see is if fed stops intervention now then the ressesion becomes full blown by summer. the latest rate cuts will work through the system and $130-$150 with $4-$5 per gallon of gas by summer anyhow.

after summer there may be a momentary glut as demand pulls back. possibly dropping oil below$90 toward $70 later as the world economy slows as well. But again if mexico or saudis or anouther major producer exports drop off then $150 per barrel could be reached in weeks if not days.

either way 2009 will bring more price stability as more mega projects are brought on-line and the world economy reels from a severe downturn.

but this is just a guess.

Nate why do you think a recession in 2008 ? I think at best towards the end of 2008. Although we are aware of the current problems almost all of them are related to debt. Its a banking crisis. We are still a long way from having sane lending even as this crisis trundles forward. Also a lot of the problems are related to illiquid assets such as real estate. It takes six months to process a home through foreclosure and banks for whatever reason are allowed to hide losses for unreasonable periods of time. And the central banks are working hard to keep things from unraveling. Also direct intervention in the stock markets is not impossible. I'm not saying we won't enter a recession but I'm now wondering how fast this will play out. We have a lot of reason to believe that the central banks can keep plugging holes in the dike for a while.

If you look at the Great Depression the economy was on borrowed time from the 1926 Florida housing crash. The market did not crash till 1929. Taking 2007 as the first year of crash puts a deep recession in 2010. I think we are already in a mild recession thats deepening. But we still have a ways to go before this really gets rolling. We are probably at the beginning of the Greatest Depression and it simply takes time for this thing to pick up. Also since the financial world is so screwed up for example housing prices in California need to drop by 50% just to become sane much less cheap as in a real recession. And we have more games we can play now.

I'm not saying we won't continue down through 2008 but we are coming of a massive bubble and headed for the deepest depression we are still a long way from anything close to normal. I just think its going to take time for all this to unfold.

Memmel,

I wholeheartedly agree except that the crash started in 2006. 2007 was the year bankers could no longer hide the problem and the wheels came off(credit crunches) the housing market.

I'd put the severe part of the recession at late 2008 at soonest with 2009 being 1929 all over again. the only benifit being demand for oil will drop off just as new resources/ technologies come online.

I guess it's all a matter of how long the fed can continue delaying the inevitable and making it worse. I just don't see our lenders around the world (china, japan, EU) continueing to put up with it.

Well memmel, personally I think the 'banking crisis' is nothing more than a symptom of the energy crisis. If there was some way in the world to totally avoid further energy problems, there would be ways to chopper right out of the bank situation. Especially given that so many of the big players are totally immersed in the system.

Look at what is going on, Citi throws a couple billion at Countrywide, knowing full well they have liquidity problems of their own they will shortly have to own up to. Not 2 months later, yup, they take a big write down, then another month later announce $7 billion of foreign capital investment. Phew, that was close, lol.

I can only imagine what total Citi write-downs might be by the time they are out of the woods. Meanwhile their stock in Countrywide has done nothing but lost them money and refuses to show signs of an upturn. So much for that gambit for now.

This is just one little sign of course but it does indicate how willing the big players are to work with one another to avoid total catastrophe. Given stability in oil they could probably work it out.

But turn the wayback machine back to Summer 2005. The peak of the housing boom was reached and the peak/reversal just happens to coincide with the summer crude peak.

Coincidence? I don't believe in them in situations like this...

Sure, I agree fully that the banking situation was ripe for disaster and has been for quite some time. It took an oil spike to trigger though, in the context of a multi year bull run, both in production and price.

I don't think we'll ever see sub-$75 again, a very firm chart floor has been put in. Even getting back down below $80 at this point would be very short-lived probably. I didn't think we'd be quite this high this fast, so much for that. Just an Extreme bullish indicator.

The behind the scenes diplomatic scurrying around to help aid deliveries has to be a sight to behold at this point. It's all there in the price to see. Every barrel is being bid for at this point.

I agree with you that it's probably only getting worse next year. Too bad about those pesky userers, er bankers, getting it in the shorts, hehe.

I agree that the two will become closely tied. We have not yet had a oil emergency and given all thats going on I can't see us making it through 2008 with out a event that will effect oil output. Esp given global warming and hurricanes. Basically in watching that the storms are forming like crazy its just the tops are being ripped off by high altitude winds. We have been lucky.

But going back to the S&L crises the banks can cook the books until they are forced into insolvency that the advantage of creating money out of thin air. The problem is they can't easily make new loans with so many bad loans and deprecated collateral on the books. The game seems to be to try and meter out the bad news with a series of writedowns.

This can go on for a while. But the REAL economy has to start heading south near the end of 2008 and this will force the bankers hand.

The real problems for them is not profit loss but revenue when their revenue stream dries up as the real economy slows they can no longer play games with the books. And they will by the end of 2008 have to start unloading all the REO's.

I think they will try and hold prices through the spring and early summer but by fall they will have no choice but to capitulate and slash prices. Once they finally reach a price point that starts selling they will be forced to revalue their assets. So the BIG write downs are actually first second quarter of 2009.

This is when bank lending for business is dead and only then do we see weak businesses fail as the defaults.

The role oil plays is huge see above right when the financial are on the ropes the consumer will be gutted by high oil prices sending car purchases into and abyss and consumer spending down the tubes. Christmas 2008 will be the worst since the great depression.

But in the summer we have a safety valve because the historic driving season will turn anemic as gas approach 4-5 dollars a gallon. So we will see demand destruction during this discretionary season. Think of it as the lull before the storm. If gas prices drop it will pick up so we have a tug of war between discretionary driving and oil prices. For a lot of consumers it will be the last summer fling. Others will be busy moving out of their repossessed home. I think summer 2008 will be repo season instead of buying season as people use the time to move out of their homes.

UHAUL and the like should have a fantastic summer so I rate them a strong buy.

I'm assuming we get a build in oil inventory in the early spring so we should actually go above average and this will take months to draw down. If we hit summer with below average oil inventory then no problem gas is 5 bucks a gallon and people cut back. So you see how we can balance peak oil monetary issues etc etc into the late summer and fall.

Now because of my assertion of a technical effect I think that oil production in the US and GOM etc will drop steeply first half of next year but this won't begin to effect inventories till mid summer. By fall assuming one external event we go to the moon in effect on prices probably touching 200 a barrel or more.

Fast forward into the winter with the recession finally in full swing and we have some price drop back down to lows of 120-150 range.

In 2009 its a tag team between economic problems and depletion. At this point high gas prices might actually be the least of our problems. What a lot of people are not realizing is we should have at least one major car manufacture bankrupt at this point and a number of oil refiners close to bankruptcy as they have excess capacity.

The majors will be forced to downgrade reserves sending stock prices lower even though oil is expensive.

West Texas's Iron triangle will be breaking apart in 2009.

Trade wars will erupt etc etc.

And finally and don't forget a lot of state and local goverments will be going bankrupt at this point. Understanding this issue is what keeps me from moving now.

I lot of "cool" places will have dysfunctional police and fire departments. I'm eying Oregon but I really think the governments their will get hammered and hosed from all this.

They are similar to California. I want to see who is fsck'd.

So I plan to buy my retreat fall 2009 :)

Or move in with mom and dad :(

I have often agreed with almost all of what you post memmel. We seem to things in similar ways.

One little difference this time however. Timing...

3 years ago I didn't think there was a way in hades that production could stay this high this long. I stand corrected, lol. At that point it had been easy to see how screwed up the housing market was becoming for some time. The triad of unscrupulous lenders, ditto real estate agents and home builders put the screws to buyers that should have given more thought to the biggest purchase in their lives.

It created a huge surplus of homes that were unheatable as soon as energy prices ticked up even a little. All it took was a little surge in oil to trigger the entire house of cards into collapse.

Began July/August 2005. It was quite interesting to watch the whole thing unfold as MSM and vested interests denied the underlying problem with more and more creative rationalizations.

It has held up as well as it has for a couple of reasons imo- 1; Oil has remained, uhm, affordable for the bulk of the developed world, so far, and this fact has given the big boys time to try to unwind positions and 2; support the market while doing so, escaping with as much of their wealth intact as possible.

It is my belief that it will be possible for the big boys to support the market somewhat long enough to largely escape to safer financial havens. As long as oil remains available in sufficient quantities and at prices that won't make it unobtainable for the masses.

We're only quibling about a year or two here imo. Next year is going to be interesting no matter what probably. But I have been thinking recently that it will hold together through next year, much the way it did this year.

Gas will probably have to hit $4 in May or so but watch the refiners as they desperately dance the number around to balance throughput at a manageable level without killing the golden goose (consumer).

Yes, the economy should show more signs of slowing, but I just think it takes more time for things to break apart. The big boys have seen this coming, some for a looong time, others not so long maybe, but surely they ALL do by now. They are playing defense in a big way, and still have cards to play (or moves to make on the Chess board).

The new Prez won't be inaugurated until early 09. As long as oil production can stumble along near this level, I expect the current admin to stay their present course. The day after the inauguration the new Prez will be taken aside and brought up to date on things he/she probably never expected to be going on. Expect some waffling on positions soon after, lol.

Yes, next year a major home builder or three will BK, one of the big banks or two ditto. But the King has been Castled into a position that is safe, for now. It will take some time for the next round of maneuvering to weaken his position further.

So far only a few pawns and minor pieces have been exchanged. Plenty of pieces still on the board. I would call this early mid-game.

Thanks, Relayer,

Interesting.

re: "...to largely escape to safer financial havens."

What might those be?

And then...what?

Good morning and Happy New year Aniya!

Not being highly educated on international monetary affairs leaves me poorly equipped to answer that first one, hehe. I had thought the traditional haven of gold would surge earlier than it has. Other precious metals with more industrial uses have done much better, probably some of those moves are positioning.

It seems to me that a decent percentage of the repositioning has been into privatizing businesses. There has been a marked upswing of private capital moving into this arena. When TSHTF it will leave the new owners in control of actual assets instead of paper money that may very well inflate into worthlessness anyway. It has the advantage also of enabling big leverage with the houses money to gain this asset ownership. Payments towards use of such money should become increasing irrelevant also as inflation kicks in.

And of course this line of reasoning helps settle a discussion issue- Stagflation or Inflation? Well gee, which way do you think it goes when you see how much of our money has been used by the big boys in an asset grab? Yea, inflation looks like a pretty darn safe bet, eh?

Accounts in Switzerland, Caymans, etc? What currency would you store it in? Actually, the case could be made for developed countries currencies having a better shot at surviving the coming storm better than any other, it would

be a crap-shoot picking a storage currency for me. Far more learned people than myself suggest gold coins, even get specific on which ones. So far I have stuck with equities in energy related areas. I can be very mobile that way, up to a point anyway.

And then what? Wow, even up to this point it's all speculation. But... I doubt that the hard crash boys are going to be very pleased. The lords up on top of the food chain can not afford to totally ignore the masses imo. If they do their support structure disappears and they end up actually having to do some work just in order to survive, lol. I'm sure that just wouldn't do.

One thing that is for sure- they will use this to their best advantage, sigh. I just hope that the strategies of the rich and famous leave room for a comfortable existence for some of us proles.

This whole thing is just fascinating to ponder. My poor ruminations have been improved considerably by crawling the web and I consider this site a priority and visit it as often as time allows.

Thank you all very, very much for all the insight into a situation which remains shrouded in the fog of war...

Have you Castled yet Aniya?

Happy New Year!

And Nate if I say things might be better then you predict By God you better listen :)

I still believe oil is going much higher over time - Ive lightened up on my futures position. And in fact, Im starting to focus more on 'real' goods and knowledge than the market, though this is going to be a long transition (for me....;)

Like a lot of posters I am up in air the about closing price 2008. I'm really waiting for Kunstler to post his 2008 prediction. He was pretty close on most of his predictions for 2007.

One thing most of the posts seem to overlook is that as the Oil producing countries rake in the wealth of tightening supplies and their own economies grow they will need to hold back more production for domestic use which will tighten even more world supplies.

I am expecting some pretty wild swings this year as oil supplies tighten prices go up and economic growth then slows, followed by falling oil prices and economies start to recover and the cycle repeating itself over and over.

A stab in the dark $150 at the end of 2008 (assuming the bottom hasn't fallen out of everything).

I read TOD frequently though this is my first post.

It's tough (& getting tougher every year), but this time I'm putting my vote in for 4). My guess is about $US85, with events moving somewhat more slowly than the doomers are predicting. And here's why:

1. Recession in US will bring about demand destruction, mainly through reduction in commercial activity (fewer goods criss-crossing the country, fewer commercial vehicles running around town). The recession in the US won't start out real bad, but it will just keep getting worse. The Fed will have interest rates back down to 1% by year end.

2. Europe & Japan will slow down, but not get into a deep recession. European interest rates will be cut, but not as drastically as in the US. Japan will keep them on hold and abandon plans to raise them.

3. Recent price rises will continue to price low-value uses of oil out of the market. Henry Groppe says that China & many other Third World countries still use a lot of fuel oil:

http://globalpublicmedia.com/transcripts/2891

Demand destruction in this area is what has caused price rises to stay rational while we are at a plateau in production & it still has a way to run. I don't buy Groppe's line on Saudi Arabia, though. The water line on Ghawar just keeps shifting. I think he's a victim of the very phenomenon he describes the IEA as having - if he calls them liars, they cut off his data & he loses his living.

4. China & India will not go into recession. There's an increasing amount of domestic demand being built into their economies, but there's also another factor entering the equation. In the past, recessions caused a greater than proportionate drop in imports, as the productive capacity of the local economy was all that was needed for most sectors. Now, production is increasingly globalised. Businesses will react to falling demand & (especially) profits by cutting costs - and the obvious way to cut costs is to outsource manufacturing to China & IT to India. This will mean that the impact on the US economy will be felt almost entirely in the domestic sector. That's the reason I say above that the US recession will keep getting worse.

5. The Fed won't give up on interest rates & resort to printing money until '09, so the drop in the $US will be kept reasonable till then. There will be no recovery of the US manufacturing sector based on lower currency values, since the Chinese currency won't be revalued far against the greenback - and that sort of thing works over a lot longer time-frame than the 12 months we're talking about, anyway.

6. The Chinese currency won't be significanly revalued until a Democrat is in the White House (i.e. after the relevant time-frame). The Dems are more anti-Chinese than the Republicans and will decide their China policy is more important than the phoney War "on" Terror. Since the Chinese regime are looking for an edge, not a stoush, they'll give ground on the exchange rate if they're pushed hard. The US China policy will backfire, though, setting off inflation, even in the midst of recession.

7. Apparently a lot of mega-projects are scheduled to come on line in '08. This will also keep a lid on prices for a while. The real action won't start till '09 or '10, when depletion can't be covered up and there are bugger-all mega-projects in the pipeline.

8. Meanwhile, down here in Australia, the boom will continue, since "dig stuff out of the ground & ship it to China" will still look like a winning strategy in 12 months time. Probably 24 & maybe even 36.

9. My price prediction is based on no major negative geo-political events occurring. The US won't attack Iran - the bombing threats are just a Plan B & sound-effects to back up the diplomacy. Talking has got Uncle Sam further with North Korea & Libya than shock & awe has with Iraq, so Condi has neutralised Cheney. The two most likely negative events are a Turkish invasion of Iraqi Kurdistan (as distinct from the present limited raids) and an Islamic revolution in Pakistan. I'd put both of them at less than 10% probability, at least for '08. Islamic revolution in Saudi Arabia will follow the complete watering out of Ghawar, which won't be in '08.

Hi Ablokeimet,

An interesting and significant point, about US manufacturing.

re: "Now, production is increasingly globalised. Businesses will react to falling demand & (especially) profits by cutting costs - and the obvious way to cut costs is to outsource manufacturing to China & IT to India. This will mean that the impact on the US economy will be felt almost entirely in the domestic sector. That's the reason I say above that the US recession will keep getting worse."

So, a hypothetical business will...continue to outsource...even though, the underlying problem is really... the beginning of FF decline.

I wonder if this business would make different choices if "it" knew?

Yet, how many of the multi-nationals "know", do you suppose?

Taken together w. your next point:

"There will be no recovery of the US manufacturing sector based on lower currency values,"

This is sad, sad (for the US, anyway). Because, to quote memmel, ELP has to happen...will it (resuming a somewhat localized production) ever really happen, or will the whole thing just simply collapse?

re: "The US China policy will backfire, though, setting off inflation, even in the midst of recession."

Could you possibly expand on this and explain further?

Aniya's asked a couple of questions, so here are my replies:

1. Business choices with foreknowledge. Unfortunately, businesses will still go for outsourcing & cost-cutting, even if they see it will only aggravate the recession. It's because of the difference between micro-economics & macro-economics. Cutting costs makes sense for an individual firm (i.e. on the micro level), but the aggregate outcome (i.e. on the macro level) makes no sense at all. The problem is that a single firm can't affect the decisions of other firms, so the greatest pain for businesses will be felt by those who don't cut costs to the same extent as their competitors.