| The Finance Round-Up: December 7th 2007 | The Oil Drum: Canada | The Earth and Energy Round-Up: December 12th/15th 2007 |

The Finance Round-Up: December 11th 2007

Posted by ilargi on December 11, 2007 - 1:47am in The Oil Drum: Canada

Foreclosure Avoidance

A Society that is Psychologically Bent On Avoiding the Brutal Facts

Most will agree that as a society, we cannot spend our way into prosperity. In fact, many, even the most ardent bulls, will acknowledge that we have some serious issues to address in our current economy. From preliminary reports, this rate freeze will have a very minimal impact on the overall housing market.

Housing related stocks are up and with the prospect of further rate cuts, all seems well until you start facing the brutal reality of what is occurring.

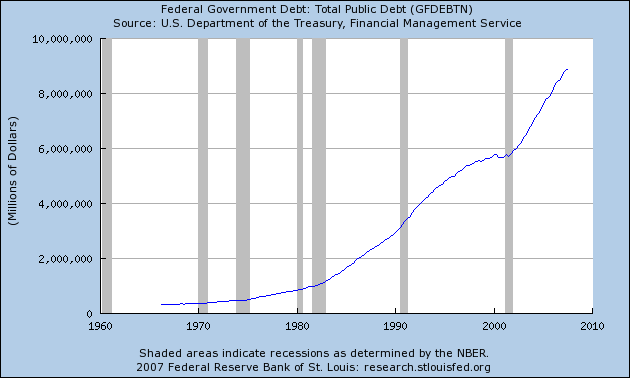

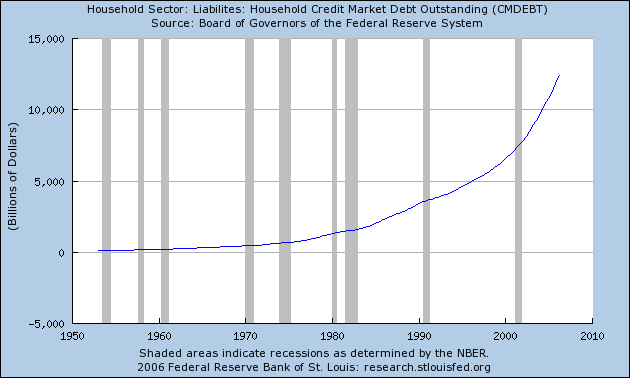

Click graphs to enlarge in new window

Decoupling dies as half the globe hits crunch

The seven pillars of global demand over the last year - measured by current account deficits - have been the United States ($793bn) (£388bn), Spain ($126bn), Britain ($87bn), Australian ($50bn) Italy ($48bn), Greece ($42bn), and Turkey ($34bn). Most are facing a housing bust. All are in trouble.

China cannot possibly step into the breach. Jahangir Aziz and Xiangming Li argue in a new IMF paper that China's economy is now so geared to the US and EU markets that a 1pc fall in external demand will lead to a 4.5pc slide in exports and 0.75pc fall in GDP.

Assumptions that it will weather a global shock are "likely to be wrong, perhaps dramatically."Note that Goldman Sachs, Morgan Stanley, and Lehman Brothers, have all begun to tear up the "decoupling" manual. - the pre-crunch script assuring us that the world could get along fine as the US buckled.

"What began as a U.S.-specific shock is morphing into a global shock," said Peter Berezin, a Goldman Sachs strategist. "There is a clear risk that some of the hot housing markets in Europe and some emerging markets will cool dramatically," he said.

Thomas Mayer, Europe economist for Deutsche Bank, said the European Central Bank must cut rates immediately, regardless of the lingering inflation threat."This could go beyond just a normal recession. It could turn into a real economy-wide crunch that we cannot stop," he said.

Four months after the global credit system suffered its August heart attack, nothing has been resolved. The US market for Asset Backed Commercial Paper (ABCP) shed another $23bn last week. The outstanding volume has fallen for 17 weeks in a row as lenders refuse to roll over loans, cutting off $393bn in funding since August.

For now, consensus has settled on the view that subprime losses will total $500bn, and crimp lending by $2 trillion as bank multiples kick into reverse. This assumes there are no more shoes to drop. Yet shoes are dangling precariously across the global credit system. We may soon have to add the terms HELOCs and 'monoline insurers' to our crunch lexicon.

S&P calls the death of the SIV

Standard & Poor’s has lost faith in SIVs.

On Friday, S&P cut the credit ratings on the capital notes all of the SIVs it rates, and said it did not expect the asset class to survive.It also put 18 SIVs on ratings watch negative, meaning downgrades are likely in the near future. In a strongly worded statement accompanying the downgrades - which saw some debt cut 10 notches to CCC from BBB - S&P opined:

The SIV as a type of vehicle is unlikely to persist and thus we formally assigned negative outlooks due to the issues in this sector

The downgrades reflect “the increased likelihood that capital investors in these vehicles will see actual losses materialize.”

Market prices for the structured finance and other types of assets in the SIV portfolios have been falling. [Moreover] funding options have been drying up as investor sentiment severely dampened demand for SIV liabilities

S&P analysts expect continued erosion in the net asset values of these vehicles, as well as a dearth of investor appetite for SIV debt, noting:

We cannot see investors returning to the market in sufficient numbers to reverse the funding problem

The ratings on junior debt of SocGen’s Premier Asset Collateralized Entity and Dresdner’s $22bn K2 were cut to junk. Premier’s senior debt is on watch for a possible downgrade, since it is close to breaching its capital adequacy test. S&P also downgraded the capital notes of three Citigroup SIVs - Five Finance, Sedna Finance and Zela Finance. And it gets better (or worse) - the unprecedented pressure on the asset class :

.. has resulted in the first defaults of senior debt in the structured commercial paper markets in its more than 20-year existence.

All of this comes after Moody’s said it had cut or was going to cut ratings for more than $100bn of SIV debt.

RIP.

Financial Taxidermy - Lessons in Being Stuffed

The fiscal irresponsibility of Central Banks is evident by the mountains of derivative paper that is starting to blow up. All of the newly created derivatives are simply transferring the "Day of Reckoning" into a later date in the future. Based upon examination of some 500 trillion plus dollars in derivatives, the hyperinflation of today is to try and keep the global economy functioning.

We live in an era where bank computers can add money to their currency with some "extra zeros" with the stroke of a finger, rather than with sweat, blood, and tears of the past where an ounce of gold represented so many dollars being eligible for existence in circulation.

The game going on is a game of musical chairs and when the music stops, there are only so many people who will find a seat.

UK: Millions paying off debts from last Christmas

More than four million people are still paying off their debts from last Christmas, it was disclosed yesterday.

Approaching one of the biggest shopping weekends of the year, figures showed that one in 10 adults - the equivalent of 4.4 million - had still not paid off their store and credit card bills from a year ago.

The disclosure sparked warnings from financial analysts that consumers risked intensifying Britain's personal debt crisis with another spending spree over the Christmas period.

Societe Generale Takes On $4.3 Billion of SIV Assets

Societe Generale SA, France's second-biggest bank by market value, will bail out its $4.3 billion structured investment vehicle after losses related to the collapse of the U.S. subprime-mortgage market.

Societe Generale will take on assets including $387 million of bonds backed by subprime mortgages, the Paris-based lender said in an e-mailed statement today.

The rescue of Societe Generale's SIV follows similar actions by London-based HSBC Holdings Plc and Rabobank Groep NV in Utrecht, Netherlands, to limit losses from a potential fire sale of assets. The falling value of Societe Generale's Premier Asset Collateralized Entity Ltd., or PACE, pushed it close to having to name a trustee to protect senior debt holders, Standard & Poor's warned on Dec. 7.

"They jumped before they were pushed to avoid being forced to sell assets,'' said Nigel Myer, a credit analyst at Dresdner Kleinwort in London.

The bailouts by Societe Generale, HSBC and Rabobank further limit the role of the “SuperSIV'' fund set up by Citigroup Inc., Bank of America Corp. and JPMorgan Chase & Co. and sponsored by U.S. Treasury Secretary Henry Paulson.

Citigroup offloads assets from SIVs

Citigroup has slashed the size of its struggling off-balance-sheet investment funds by more than $15bn in two months through quiet side deals with some junior investors, according to people familiar with the business.

The news that the troubled US bank has been finding ways to offload assets from its structured investment vehicles (SIVs) without resorting to fire sales comes as Société Générale on Monday became the latest bank to announce a bail-out for its own $4.3bn vehicle. SocGen's decision follows similar moves by HSBC, Standard Chartered and Rabobank in the past fortnight.

The moves appear likely to reduce the demand for the so-called "super-SIV", conceived by Citigroup, Bank of America and JPMorgan with the backing of the US Treasury as a buyer of last resort for the industry that would prevent fire sales.

As Citi struggles to break free from the grip of its writedowns, and with capital levels hovering dangerously low, a takeover by a smaller banking rival is a distinct possibility, warn CreditSights.

In a gutsy - and perhaps mercurial - call, analysts at CreditSights say a takeover from JPMorgan isn’t unlikely, given the outlook for Citi. Otherwise, there’s also the threat of a breakup. At the very least, it’s a sluggish, troubled end to the decade for the world’s biggest bank - with the dividend remaining under threat for years to come.

It will take Citi three years to recoup losses on CDO writedowns, according to the report, and problems may get much, much worse. First and foremost, Citi is faced with further big capital hits from its seven ailing SIVs, between them with $66bn AUM. CreditSights think this will be the next test of strength for the bank. The M-LEC superfund-cum-stumbling block, then, is far more critical for Citi than previously given credit.

Secondly, CreditSights hint at further CDO writedowns in the offing. Indeed, with a definite sense that the super-senior CDO debt market is fast collapsing, Citi can expect more trouble. The bank has $45bn in super-senior CDO exposure. All in all, it amounts to a serious - potentially crippling - lead weight strung around Citi’s neck.

Our back of the envelope break-up valuation using a proxy of comparable companies P/E ratios applied to Citi’s major business units shows a potential 18-30 per cent upside from splitting up the company. In addition, our merger math indicates that a deal with JP Morgan Chase could be accretive when considering substantial potential cost saves. Unlike a deal with Bank of America, which would exceed the national deposit ceiling of 10 per cent, a JPMorgan Chase-Citi combination seems more doable, especially considering that much of JP Morgan’s senior leadership including CEO Dimon have extensive backgrounds at Citi. Further, Dimon has demonstrated a strong ability to integrate large bank deals, most recently being the JP Morgan-Bank One merger.

The Citi board meets on Monday and Tuesday to discuss the appointment of a new CEO.

Lloyds takes $410.6 million subprime hit

Lloyds TSB PLC said Monday that it was taking a $410.6 million hit from its exposure to the global credit crisis.

The writedown was higher than the $324.8 million (150 million pounds ) forecast, but analysts said that the bank, Britain's fifth largest, benefited from a strong retail banking business.

Lloyds said its retail operations employed tighter mortgage lending standards, while the firm has continued to grow its share of current accounts and seen "significantly improved deposits." The bank said it remained "firmly on track" to deliver a good performance in 2007.

"Whilst no bank has been immune from the recent turbulence, the relatively limited impact of the market dislocation on the group has been more than offset by the significant profit on the sales of noncore businesses," said Chief Executive Eric Daniels.

UBS writes down $10 bln, Singapore injects capital

UBS revealed a $10 billion writedown and an emergency injection of funds from Singapore and the Middle East, making it the biggest victim of the U.S. subprime crisis to date among major European banks.

Singapore is taking 9 percent of UBS in a deal that mirrors actions taken by U.S.-based Citigroup. Citi expects to write off between $8 billion and $11 billion and has secured funding from the Abu Dhabi Investment Authority.

"There must be a suspicion that it (UBS) feels a strong capital base is necessary just in case there is need for further write-downs," said Helvea analyst Peter Thorne.

The Singapore investment gives the Southeast Asian island-state 9 percent stake of UBS through its Government of Singapore Investment Corporation (GIC), another injection into a top western bank by a sovereign wealth fund along the lines of the Abu Dhabi Investment Authority's purchase of a $7.5 billion stake in Citigroup.

"It's a developing trend. Asian and Middle Eastern sovereign investors are cash rich and have a longer time horizon than the average market investor," said Omar Fall, analyst at ABN AMRO.

A further stake of about 1.5 percent goes to an unnamed Middle East investor, and the two investments raise 13 billion Swiss franc ($11.5 billion) of fresh capital. Oman's State General Reserve Fund denied suggestions that it was the investor in question.

UBS said it had not ruled out granting board seats to the new investors.

MBIA, Seeking to Raise Capital, Halted From Trading

MBIA Inc., the bond insurer seeking to raise capital to retain its AAA credit rating, was halted from New York Stock Exchange trading pending an announcement.

The Armonk, New York-based company's top credit rating is under scrutiny by ratings companies and MBIA said last week it may raise capital to keep its ranking. MBIA, down 59 percent this year, rose 14 cents to $30.14 today before trading stopped.

MBIA, whose credit rating stands behind $652 billion of state, municipal and structured finance bonds, said Dec. 6 that it's ``pursuing capital contingency plans.'' Losing the AAA credit rating would endanger MBIA's ability to guarantee debt, its main source of revenue.

MBIA (MBI) sent the hard-hit bond insurance stocks soaring Monday with news that it has lined up $1 billion in new capital from private equity firm Warburg Pincus. Warburg will buy $500 million in MBIA stock at $31 a share, a 3% premium to Friday’s close, and will backstop an offering of an added $500 million in stock to take place in the first quarter of 2008 - at what MBIA must hope will be higher prices. MBIA shares have lost 60% of their value over the past year.

Warburg will also get warrants to buy more stock at $40 a share, as well as the right to nominate two directors to the MBIA board. “The company’s high quality and liquid investment portfolio and the ‘pay-as-you-go’ nature of its insurance liabilities give it a strong liquidity profile,” Warburg Pincus honcho David Coulter said.

Housing Slump Pinches Almost Half of State Budgets, Report Says

The end of the U.S. housing boom is cutting into the revenue of nearly half of state governments as a slower economy crimps tax collections from New Jersey to California, according to a report by a state lawmakers group.

Officials in 24 states said the slower pace of home sales and declining prices are affecting their collections of sales, income and other taxes, a survey released today by the National Conference of State Legislatures shows. Of those, respondents in 18 states are concerned the trend may continue through the middle of 2008, three times as many as a year ago.

“Although revenue collections are hitting or exceeding expectations for the vast majority of states, a growing number report that collections are failing to keep pace with what forecasters had projected and what lawmakers had used to establish budgets,'' according to the report.

The report is the second in as many weeks to show how the finances of state governments are being crimped as consumers pare their spending while home prices fall, Wall Street cuts back on credit, and fuel remains costly. Last week, a survey released by a governors group showed that states are curbing tax cuts, dipping into their reserves and increasing spending at a slower pace because of slowing revenue growth.

U.S. states receive about two-thirds of their revenue from sales and income taxes, which are tied closely to the pace of the economy. When revenue falls short of forecasts, states are typically forced to cut spending or raise taxes to balance their budgets.

Muddled Foreclosures: Whose Home is it Anyway?

As foreclosure cases clog the dockets of courts around the country, a variety of interesting details about the dealings of the mortgage industry have begun to come to light. One legality in particular has been the source of debate and delay in a growing number of foreclosure actions, centering around debt ownership and mortgage investment practices.

It seems that many foreclosure proceedings may not be the cut-and-dried cases that creditors expect when they take distressed homeowners to court, thanks to a complex web of mortgage note sales and investment that has been constructed in today's financial markets.

For about two decades now, most mortgage loans taken by consumers have been packaged or pooled for sale as securities investments. In many cases, mortgage notes are sold before the ink is dry on the paperwork, with the first sale of the debt arranged even before the loan has been officially closed.

With outstanding securitized mortgage debt reaching a figure of more than $6.5-trillion by the end of 2006, this practice has increased the liquidity in the market, providing a steady stream of funds for new loans to be made. However, it has also complicated matters, often making it difficult to determine who actually holds legal claim to the outstanding debt as loans are sold over and over again.

As with stocks in 2000-02, real estate wealth is wasting away. The drop isn't as fast or as severe, but it affects a far greater number of Americans. What Greenspan saw as the main advantage of a housing boom, i.e. wide participation, is its greatest shortcoming, as it turns into a bust. When stocks drop $100 the loss to 80% of Americans is just $9. But in the case of housing they lose $35 - four times as much.

The impact on the mood of the consumer, the so-called "wealth effect", is likewise severe - though with a significant delay, because house prices are not tied to a daily Dow Jones-type ticker. People have difficulty accepting that their own house is now worth significantly less. They too, are marking to model or, more accurately, marking to dream.

This is not lost on the Fed and the administration, both of whom are once more in thinly-veiled panic mode. They keep throwing up all kinds of misbegotten plans to save the day: the super-SIV, lifting lending restrictions to bank subs, encouraging Discount window borrowing, freezing ARM rates - BandAids, all. Perhaps they will try another tax cut soon?

The false prophets of wealth are finally seen for what they really are: pushers of debt and needless consumption. They preach that if debt is made cheaper, if the liquidity taps are opened wider, if we just borrow more, we us all shall be wealthy. But in a global financial system that is already awash in liquidity, what need have we of more? What is there left to speculate on margin, that is not already levered to the hilt? Nothing.

Black Swans and Endogenous Uncertainty

"There are many subtleties and twists in the story ... but the basic message, roughly speaking, is simple: The peculiar and exceptionally unstable organization of the critical state does indeed seem to be ubiquitous in our world. Researchers in the past few years have found its mathematical fingerprints in the workings of all the upheavals I've mentioned so far [earthquakes, eco-disasters, market crashes], as well as in the spreading of epidemics, the flaring of traffic jams, the patterns by which instructions trickle down from managers to workers in the office, and in many other things.

At the heart of our story, then, lies the discovery that networks of things of all kinds - atoms, molecules, species, people, and even ideas - have a marked tendency to organize themselves along similar lines. On the basis of this insight, scientists are finally beginning to fathom what lies behind tumultuous events of all sorts, and to see patterns at work where they have never seen them before."

[..]

Now, let's couple this idea with a few other concepts. First, economist Dr. Hyman Minsky points out that stability leads to instability. The more comfortable we get with a given condition or trend, the longer it will persist and then when the trend fails, the more dramatic the correction. The problem with long term macroeconomic stability is that it tends to produce unstable financial arrangements. If we believe that tomorrow and next year will be the same as last week and last year, we are more willing to add debt or postpone savings for current consumption. Thus, says Minsky, the longer the period of stability, the higher the potential risk for even greater instability when market participants must change their behavior.Relating this to our sandpile, the longer that a critical state builds up in an economy, or in other words, the more "fingers of instability" that are allowed to develop a connection to other fingers of instability, the greater the potential for a serious "avalanche."

A second related concept is from game theory. The Nash equilibrium (named after John Nash) is a kind of optimal strategy for games involving two or more players, whereby the players reach an outcome to mutual advantage. If there is a set of strategies for a game with the property that no player can benefit by changing his strategy while (if) the other players keep their strategies unchanged, then that set of strategies and the corresponding payoffs constitute a Nash equilibrium.

A Stable Disequilibrium

So we end up in a critical state of what Paul McCulley calls a "stable disequilibrium." We have "players" of this game from all over the world tied inextricably together in a vast dance through investment, debt, derivatives, trade, globalization, international business and finance. Each player works hard to maximize his own personal outcome and to reduce their exposure to "fingers of instability."But the longer we go, asserts Minsky, the more likely and violent an "avalanche" is. The more the fingers of instability can build. The more that state of stable disequilibrium can go critical on us.

Bank-Lending Drought May Continue Next Year, BIS Says

Investors expect the global credit squeeze to continue beyond the first quarter of 2008, according to the Bank for International Settlements.

Models using derivatives based on money-market rates signal "expectations of a persistent lack of liquidity and lasting concerns about counterparty risk,'' the BIS said in its latest quarterly survey. Basel, Switzerland-based BIS, formed in 1930, monitors financial markets and regulates banks.

"The bank liquidity crisis has become a more serious problem than subprime though both are correlated,'' said Aaron Low, a principal in Singapore at hedge fund Lumen Advisors LLC. “The banking confidence factor has affected a broader segment of the economy.''

When real-estate markets sour, owners of luxury homes and condos sometimes cling to a comforting theory, at least in the slump's early stages: Their properties are pretty much immune to a downturn, just as their own lives are immune to the daily economic tribulations of those sad and pitiful Janes and Joes forced to reside in those tacky $600,000 hovels out by the Interstate.

Alas, reality and theory don't always coincide.Consider Sarasota, Fla., a small city in which property values are king and which was one of the hottest of the hot spots in the U.S. real-estate bubble.

Hugging Southwest Florida's Gulf Coast, with a sparkling downtown facing a gorgeous bay, 35 miles of white-sand beaches, a wealth of museums, opera, ballet and theater, plus a well-heeled population of sophisticated retirees and second- and third-home owners, Sarasota thought the ride would never end.

Home prices jumped 150% from 2000 through 2005, according to the National Association of Realtors. Condos rose about 130% in the same span. And those figures, which also cover neighboring Bradenton and Venice, may understate the gains in Sarasota proper and its barrier islands, which boast a disproportionate share of the area's to-die-for properties.

But now prices are in something approaching a free-fall. The current readings say they're down 19% since the end of 2005 and 10% in the past year. Lots of residents who had considered selling their homes during the craziest of the craziness, but didn't, are wringing their hands.

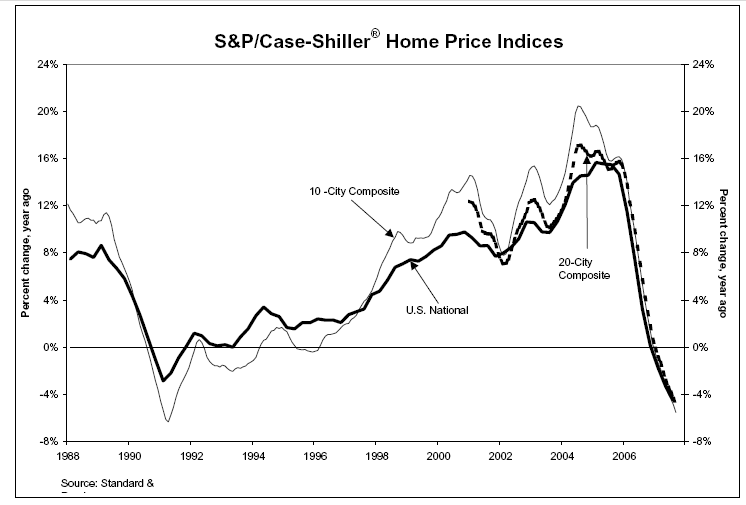

Shiller Home Price Index

Another Fantasyland Call From The NAR

Click to Enlarge in New Window

The chart above, depicting the annual returns of the U.S. National Home Price Index, the 10-City Composite, and the 20-City Composite shows all three still yielding negative returns as of September 2007. The quarterly S&P/Case-Shiller® U.S. National Home Price Index -- which covers all nine U.S. census divisions -- was down 1.7% from Q2 2007 and down 4.5% from Q3 2006.

“The declines in the national figure are notable for two reasons,” says Robert J. Shiller, Chief Economist at MacroMarkets LLC. “First, the 3rd quarter decline, at 1.7%, was the largest quarterly decline in the index’s 21-year history. And, second, the year-over-year decline posted its second consecutive record low at -4.5%.

To understand how understated the Shiller index is, ask anyone in Tampa or Miami who bought in 2005 or 2006 and are now looking to sell if they will take 10% less than they paid for it. I suspect most would be thanking their lucky stars for the chance.

Pending U.S. Home Sales Probably Fell in October to Record Low

The number of Americans signing contracts to buy previously owned homes probably fell in October to the lowest in at least six years, pointing to further weakness in housing.

The National Association of Realtors' index of pending home sales decreased 1 percent, according to the median estimate of 23 economists surveyed by Bloomberg News. The measure unexpectedly rose in September following the biggest back-to- back decline since record-keeping began, in 2001.

The jump in mortgage delinquencies and foreclosures has made it more difficult for some prospective buyers to get financing. Federal Reserve policy makers, who've said they are concerned the turmoil in credit markets will limit lending, are forecast to lower the benchmark interest rate tomorrow.

Freddie Mac tightens delinquent loan purchases

Freddie Mac, the second-largest U.S. home funding company, said on Monday it has adopted guidelines that may reduce the number of delinquent loans it purchases from mortgage pools, easing stress to its capital base.

The new rules expand criteria that must be met for buying loans in arrears out of its mortgage securities, the McLean, Virginia-based company said in a statement. The move is expected to cut the need for extra capital since the company's mortgage bond guarantee obligations require less backing than loans owned in portfolio.

Freddie Mac's policy shift comes after the company rattled investors last month with a $2 billion third-quarter loss, partly due to the purchase of $483 million in loans from its mortgage bonds, up from just $30 million in the period a year earlier. Many of these loans that were 120 days delinquent still "cure" or get paid off, making them good collateral for the bonds, said Sharon McHale, a Freddie Mac spokeswoman.

"We think this will better reflect the behavior of delinquent loans," she said. It will, at least initially, reduce the repurchases, she added.

Losing Control Of Monetary Policy

- The U.S. is on the precipice of its first consumer led recession since 1991.

- A wave of U.S. bank failures is coming.

- LIBOR rates are rising in the U.S. and UK smack in the face of interest rate reductions.

- The ECB continues with hawkish rhetoric.

- German businesses paid back more than they borrowed for the first time since the 1980s.

- Three-month Euribor rates are 93 basis points over ECB rates.

- One-month LIBOR rates are 74 basis points over the Fed Funds Rate.

The Fed's and BOE's easing actions simply are not working to restore faith in the credit markets. Credit conditions based on LIBOR are worse now than in the August and November stock market swoons. Banks remain reluctant to lend to one another in spite of central bank efforts to provide liquidity. Neither central bank appears to be in control of anything at the moment.

A few weeks ago, Abu Dhabi's Citigroup deal marked a historic event that I believe not many are truly grasping. It was this outside intervention that not only put a floor in the US financial system, but sent a very loud message, telling the United States that buyers were lurking and at the right price, would gladly step in.

You see, free markets are the lifeblood of this country. Our foundation is only as firm as the dreams, aspirations and ability of its people to pursue their ideas. A government intervention, when things go wrong, does hinder this. Yet the alternative today is that the free markets expand much farther than the US national borders, and if we remain truly free, we are at the world's mercy.

At present the US is a two part economy based on service and finance. As citizens we can proudly say that we have the smartest financial minds at work and have built the world's strongest financial system. However, those minds, those companies, and those practices are also for sale through the stock market. At the right price, and with enough money, this entire system is on the auction block and can be purchased by anyone.

While our current mortgage mess comes from the overbuilding from companies like Toll Brothers, Centex or Lennar, as well as lending practices from companies like Countrywide Financial, the result has spiraled into a credit crunch as well as a devaluation of major financial institutions such as a Citigroup, Bank of America, or a Wells Fargo. It is the intellectual property of these financial institutions that is extremely appealing to foreign countries seeking to evolve from their single export roots.

Ironically, at the same time that this intellectual property is for sale at an extreme discount, the purchasing power of foreign bidders has increased dramatically. In simple terms, it would be as if you not only go into a store that has marked everything half off, but to boot you also receive another 25% through a mail in rebate. Regardless of what may still be coming down the pike, or the financial unknowns hidden off balance sheets, at the right price, foreign countries have to be licking their chops at the opportunities that present themselves in the US stock market today.

Living the Diesel Shortages in China

The story goes something like this: Inflation is out of control at 6.5 per cent and prices of everything have at least doubled in the last year and a half. Wages remain almost stagnant with no upward rise to match the inflation rate. Five years ago, when China’s economic boom started, dreams were alive in the air: a new car, a new apartment and a better life filled with possessions if you came to the cities and worked real hard. That is exactly what happened, a flood of workers came to man the factories, build new skyscrapers, and fill offices by the hundreds of millions.

The carrot dangled in front of 1.3 billion people was simple: come, work and be rewarded. That was then, this is now. The dream is dying on the vine. A majority of Chinese citizens now realize that car ownership will not occur for them, same goes for the apartment. Property values are skyrocketing, from 2500 yuan for a square metre in 2003, to 10,000 yuan for a square metre in today’s high-rises.

With unfulfilled dreams of car and home ownership, average workers trudge through their days knowing that the basic necessities and a night out on the town is all they will get in life. With inflation running at 6.5 per cent now what little income there was is being eroded, and the dreams of nights out on weekends are starting to disappear. Doubling food prices are making the country tighten spending and more grumbling from the average person on the street.

It has been a culmination of lost dreams, minimal income, rising food prices and no end in sight of rising cost of daily life that made last month’s 10 per cent rise in fuel prices unpopular and added another nail to the coffin. Those that were able to afford cars within the last few years are now complaining about filling up the tank. Two years ago gasoline was 2.5 yuan per liter, now it sits at 5.8 yuan.

Chinese citizens have put the equation together: Higher fuel prices = higher food prices. Based on the complaints I hear from my students about high prices, the central government would be asking for trouble with another fuel price hike. This puts the central government squarely in the center of a catch 22. If they raise fuel prices, refiners will produce more since they are not losing money, but civil disorder may occur. If they do nothing and the shortages will continue for the next six months, the manufacture and export sector will continue to slow down, slowing the entire economy.

Australian Home-Loan Approvals Unexpectedly Fall

Australia's home-loan approvals unexpectedly fell for a second month in October as interest rates at an 11-year high discouraged borrowing.

The number of loans granted to build or buy houses and apartments fell 0.7 percent to 62,509 from September, when they slipped a revised 2 percent, the Bureau of Statistics said in Sydney today. The median estimate of 21 economists surveyed by Bloomberg News was for a 1 percent increase.

Australia's central bank raised the benchmark interest rate by a quarter point last month, following a similar increase in August, to contain inflation. Higher lending rates, coupled with rising property prices, have pushed housing affordability to a record low, curbing demand for real estate.

"The housing market appears to be feeling the pinch from higher rates,'' said Matthew Johnson, senior economist at ICAP Australia Ltd. in Sydney. ``Given that the November increase has not yet been covered by the survey, I expect to see further weakness, possibly extending into 2008.''

Today's report "adds to the uncertainty over a further hike'' early next year, said Su-Lin Ong, fixed-income strategist at RBC Capital Markets in Sydney. ``This is the first back-to-back monthly decline in 12 months,'' and echoes declines that followed three rate increases last year. About 90 percent of mortgages are taken out on a so-called floating rate, which is tied to the central bank's benchmark.

2008 Existing Home Sales Forecasts

"Existing-home sales, after reaching the third highest total on record, 6.48 million in 2006, are forecast at 6.44 million in 2007 and 6.64 million next year." National Association of Realtors, Feb 2007.

Just thought I'd start with a little comic relief from Those Wacky NAR Forecasts! Compare to the current NAR forecast:

Existing-home sales are likely to total 5.67 million this year, the fifth highest on record, rising to 5.70 million in 2008, in contrast with 6.48 million in 2006. NAR, Dec 2007.

I think their forecasting model is broken.

Last December it was hard to find a Wall Street firm with a forecast under 6.0 million existing home sales in 2007. David Berson, then Chief Economist at Fannie Mae, forecast 2007 sales would be 5.925 million - and that was considered bearish. My forecast was for sales to "surprise to the downside, perhaps in the 5.6 to 5.8 million unit range."

Now we are starting to see forecasts for 2008. Back in August, Goldman Sachs forecast existing home sales would fall to 4.9 million in 2008. However, since then, Goldman has becoming even more bearish on housing.

Here is another forecast for 2008 via AP:

Patrick Newport, an economist at Global Insight, forecasts that home sales will drop from 5.66 million this year to 4.7 million in 2008

Calgary: Housing starts plunged in November

Housing starts in the Calgary Census Metropolitan Area plunged by more than 48 per cent in November compared with a year ago when they set a blistering record pace, according to data released today by the Canada Mortgage and Housing Corporation.

The CMHC said the overall drop consisted of a 76 per cent plunge in the multi-family sector and an 18.6 decline in single-family homes.

"Single-detached starts continued to be weaker while multi-family starts plunged this month after three consecutive months of high production," said Lai Sing Louie, senior market analyst in Calgary for the CMHC.

In particular, the Paulson plan is probably an attempt to take the wind out of Barney Frank’s sails. Mr. Frank, the Democratic chairman of the House Financial Services Committee, has sponsored legislation that would give judges in bankruptcy cases the ability to rewrite mortgage loan terms. But “Bankers Hope Bush Subprime Plan Will Scuttle House Bill,” as a headline in CongressDaily put it.

As Elizabeth Warren, the Harvard bankruptcy expert, puts it, “The administration’s subprime mortgage plan is the bank lobby’s dream.” Given the Bush record, that should come as no surprise.

This is supposed to help investors, because foreclosing on a house is expensive: there are big legal fees, and the house normally sells for less than the value of the mortgage. “Foreclosure is to no one’s benefit,” said Mr. Paulson in a White House interactive forum. “I’ve heard estimates that mortgage investors lose 40 to 50 percent on their investment if it goes into foreclosure.”

But won’t the borrowers gain, too? Not if the planners can help it. Relief is restricted to borrowers whose mortgage debt is at least 97 percent of the house’s value — which means that in many, perhaps most, cases those who get debt relief will be borrowers who owe more than their house is worth. These people would be nearly as well off in financial terms if they simply walked away.

No one's biting in 'buyer's market'

We're not supposed to have much of a sub-prime crisis here. So an ad for a real estate auction caught my eye. "In a buyer's market, YOU should be BUYING!!!" it said. Given all the anxiety about the housing market dragging down the nation, I figured I'd go look. If the stony-faced buyers gathered at the Radisson Hotel last Wednesday are any indicator, be glad that Peoria is supposedly doing well.

A real estate auction is where some landlords pick up new properties. Construction-savvy types seek fixer-uppers. Occasionally, a first-time buyer can find a bargain starter home.

At this particular auction, Cotten Auctions is selling 17 homes. Some are being sold out of estates. Some are being sold by people who don't want to use a real estate agent. A couple are the result of foreclosure.The soft-spoken auctioneer Joe Cotten takes half an hour to explain the way the process works in an almost professorial manner.

The first house on his slate has two bedrooms, hardwood floors, one bath and a concrete block garage out back. "How much? What will you give for it?" Cotten cajoles, and the sing-song begins. "How-much? How-much-will-you-give-for-it? One hundred thousand dollars? I see smiles. It's a buyer's market."

A grin flickers here and there, but that is the last of the frivolity. Even for a first-time buyer, even for a rental property, Cotten can't get a bid until he drops the price to $30,000. There is a brief flurry of activity. It stops at $48,000, which is less than the seller's minimum. No sale.

House Two has three bedrooms and one bath, a new roof, siding and windows. Bidding stops at $15,500. "You can make it up in six months rent!" Cotten pleads. No takers.

House Three has three to four bedrooms, a bath and a 2001 furnace. It rented for $525 a month. Bidding starts at $10,000.

No one bites. No bids at all.

Beware of more 'hidden' subprime losses

Report says Washington Mutual, Countrywide most vulnerable

The reality of Generally Accepted Accounting Principles, or GAAP, is that they give companies just enough rope to hang themselves and their investors, if they so please. Much of GAAP is so subjective that you could drive side-by-side snow plows through the gray areas.

That is something to keep in mind if, with the latest wave of write-offs, you believe it is time to start bargain hunting among the most beaten-down financial-services companies tied to the mortgage blowup. The time may very well be right, but a recent report by Gradient Analytics warns that financial-reporting practices of some of these companies yesterday and today could still come back to bite investors tomorrow.

Gradient, a Scottsdale, Ariz., research firm that caters to mutual funds and hedge funds, was early to spot accounting issues at Krispy Kreme Doughnuts Inc., Biovail Corp. and Children's Place Retail Stores Inc., among others, and their stocks subsequently tumbled.

"I think for a number of years they played games," Donn Vickrey, a former accounting professor who co-founded and is now editor-in-chief of Gradient, says about the financial-services companies.

By "playing games" he means a tendency during the mortgage boom "to report numbers that were artificially high." There were a variety of ways to do that, all of them completely legitimate and blessed by the gods of financial accounting rules otherwise known as the Financial Accounting Standards Board.

Mortgage meltdown

Interest rate 'freeze' - the real story is fraud

It sounds good: For five years, mortgage lenders will freeze interest rates on a limited number of "teaser" subprime loans. Other homeowners facing foreclosure will be offered assistance from the Federal Housing Administration.

But unfortunately, the "freeze" is just another fraud - and like the other bailout proposals, it has nothing to do with U.S. house prices, with "working families," keeping people in their homes or any of that nonsense.

The sole goal of the freeze is to prevent owners of mortgage-backed securities, many of them foreigners, from suing U.S. banks and forcing them to buy back worthless mortgage securities at face value - right now almost 10 times their market worth.

There are lots of people who would like to muzzle subpoena-happy New York Attorney General Andrew Cuomo to buy time and make this all go away. Cuomo is just inches from getting what he needs to start putting a lot of people in prison.

We are on the cusp of a mammoth financial crisis, and the Federal Reserve and the U.S. Treasury are trying to limit the liability of their banking friends under the guise of trying to help borrowers.

At stake is nothing short of the continued existence of the U.S. banking system.

Convoluted Mortgage Fraud Theories

A number of people have all emailed me with a sensational but preposterous "Mortgage Meltdown" article by Sean Olender about the interest rate freeze.

Yes there is "fraud everywhere" as the article suggests, and yes the freeze "has nothing to do with keeping people in their homes", and yes, "The problem isn't just subprime loans", and yes a "mortgage meltdown" is in process.

But the rest of the article is complete nonsense.

Class action suit spurs refunds of currency exchange fees

If you used your credit, ATM, or debit card for foreign transactions, you could be eligible for a refund of some of the currency exchange fees you paid, according to the proposed settlement of a class-action lawsuit brought against Visa, MasterCard, Diners Club, seven major banks, and affiliated companies. But you must file your request by May 30.

Under the proposal, payments would be available to anyone who used a Visa-, MasterCard- or Diners Club-branded credit, charge or debit/ATM to make foreign transactions while traveling abroad or over the Internet from Feb. 1, 1996 to Nov. 8, 2006. Covered transactions include purchases, cash advances, and cash withdrawals.

The refunds are expected to be at least $25, though they could be higher for individuals and corporations who actually can provide good estimates of their foreign transactions.

Sour state investments jolt local governments

The head of the agency that manages billions of dollars for the state dropped a bomb on his bosses in a mid-November meeting: About $2.28 billion in investments were going sour. Some of the investments, all of which had fallen below purchase guidelines, were in a fund where local governments and school boards stashed operating funds until they were needed.

Over the following two weeks, as word got out, Florida municipalities yanked $10 billion from the Local Government Investment Pool in a classic run-on-the-bank scenario. Only an emergency freeze on Nov. 29 stopped the stampede for the exits.

Last week, the executive director of the State Board of Administration, Coleman Stipanovich, resigned under pressure. The state hired BlackRock, a Wall Street investment management firm, to guide the state out of the mess by segregating the troubled investments into a separate fund and limiting withdrawals from the healthy fund while it works out the problems. And the problem is far from over: Alex Sink, the state's chief financial officer, who had pressed Stipanovich for the Nov. 14 finacial update that triggered the run, plans to ask auditors to probe what happened.

Local officials, scrambling to replace the missing cash with other funds, are wondering whether state laws were broken. Finger-pointing has begun, and some local elected officials are contemplating filing lawsuits to recover money they invested with the state.

It's unclear what losses the fund might ultimately face. 'There are so many unknowns, it's difficult to guess,'' said Christopher Stavrakos, BlackRock's co-head of cash portfolio management. ``It depends on the liquidity in the market. Right now, the market is obviously stressed and dislocated.''

Insolvency is here, and not just in the United States. The rise in LIBOR and the increasing speed of issuing new shares point to the high probability of insolvency throughout the world’s major financial institutions.

LIBOR is skyrocketing despite central bank easing, and debt markets have completely frozen over. Besides being reluctant to lend to businesses or each other, major financial institutions the world over are raising capital at alarming rates to survive something that might wipe out many of them.

First, Citigroup did it. Fannie then stepped up to the plate. Northern Rock is being nationalized. And now, the Swiss giant UBS AG is following suit.Ladies and gentlemen, this would be the third time that UBS has taken additional losses on their US investments. Turns out the b.s. never ends with these guys, as their losses far exceed what they reported. I think this will be the way the banks prefer to let out the bad news - in recurring increments. Get used to it. Goldman and JPMorgan haven’t reported any losses… yet. The first writedown will be the first installment in a long series of them.

Fitch, Moody's cut WaMu on mortgage exposures

Moody's Investors Service and Fitch Ratings on Monday cut their ratings on Washington Mutual Inc. after the savings and loan said it expects to report a net loss in the fourth quarter after recording non-cash write-downs.

WaMu also said it would slash its dividend, cut more than 3,000 jobs and announced a $2.5 billion capital infusion. Moody's said that it does not expect WaMu's profitability to recover until 2010.

Credit losses from WaMu's mortgage operations "will be noticeably higher than previously estimated," Moody's said in a statement.

Profit Slump Deepens Recession Worries

U.S. corporate profits are being hammered by the slowing economy and credit-market turmoil, intensifying concerns that the nation may be headed for recession.

Banks and other financial companies, which have taken huge write-downs on soured bets on subprime mortgages, have been among the most visible casualties. But businesses ranging from makers of artificial hips to surf-wear retailers to overnight-delivery services are also feeling the pinch.

If profits fall far enough, it could discourage capital spending and make companies less willing to hire or retain workers. A hiring slowdown could magnify the downturn and hasten a recession. That's bad news for wage earners as well as those who own stocks.

Weaker profits ultimately translate into lower stock prices, which could further erode the confidence of American consumers, who are already feeling less wealthy as fuel costs rise and their home values decline.

"The recession in reported earnings has already begun," says David Rosenberg, chief U.S. economist at Merrill Lynch & Co. "The underlying cause is a combination of painfully high energy prices and the general lack of pricing power in many businesses, which is starting to crimp margins."

Pundits tell us that the crisis that has reverberated in global markets since summer was sparked by overextended borrowers. Enticed by easy credit and soaring real estate values, consumers went on a spending spree and wracked up mountainous debt. Now good old-fashioned greed has given way to a huge financial hangover and we're paying the price. It's plausible, but dead wrong.

Sure, consumers went out and bought homes, cars and plasma TVs, but the problem was it wasn't enough debt. Not enough to satisfy investors that, in recent years, have gobbling up all kinds of debt by means of an innovation called asset-backed commercial paper. So the issuers of ABCP turned to complicated new products that few investors understood and that, when the credit crunch hit, behaved in ways that not even their makers predicted. As a result, $35-billion of ABCP may have lost a chunk of its value and Canada faces one of the biggest financial crises in recent history.

ABCP consists of short-term notes backed by bundles of credit card debt, car loans, mortgages and other cash flows. Introduced in Canada in the late 1980s, it caught on slowly. But as governments pulled back from debt issuance in the late 1990s, investors took a shine to ABCP. Between 1997 and 2000, the market grew to $60-billion from $10-billion. In fact, it became so popular that there soon wasn't enough debt to make all the ABCP that investors wanted to buy. Financial Post reporter John Greenwood tells the story of a middle man who was not only instrumental in creating but also in filling the demand for ABCP.

Shockwaves from the credit crisis — who are the victims, really?

As the credit crisis deepens, at least one big question has been answered, says the FT’s Tony Jackson in his Monday column. “We now have abundant evidence that the crisis is affecting the real economy. So we need to switch our attention from the travails of the banks and look instead at their customers.” Which of them are getting hit?, he asks.

The benign response comes from the global economics team at Merrill Lynch. Granted, they say, US mortgage borrowers are suffering and their UK counterparts will be shortly. But in the eurozone, consumers are less heavily indebted. And credit creation in the eurozone, on the latest October figures, is still showing strong double-digit growth.

Hence the fact that the European Central Bank did not cut interest rates last week. It saw no need.

Asia, meanwhile, is awash with savings, and so is unaffected. And across the world, corporate balance sheets are strong and governments are under no particular pressure to borrow. So by a process of elimination, the victims of the crisis are Anglo-Saxon consumers.

- = stock is going no where, its pure junk let me look at something else.

- = lucky break, it's going to definitely crash.

- = what it's still going up earnings are not so good people are definitely getting carried away its going to pull back and crash.

- = ahh see I knew it was going to crash, thank God I did not buy. (Mistake the mass mindset misses the main point here. Yes it pulled back, but look where the pull back ended miles away from its first break out. A losers mind can only see the picture for what it is not, by replacing it with a picture from his or her imagination. Since they live in a losing sphere they focus on the negative aspects but not on the positive aspects).

- = what happened here this stock was supposed to crash how the hell did it get here. Perhaps I should have bought I could have made a lot of money; this looks like a sure thing. So only halfway through stage 5 will the mass mindset decide it's safe to venture out. Now this person finally musters the courage to buy. Vow it actually went up, great I making money.

- = this stock is going to go to the moon let me tell all my friends about it; it looks like a sure thing.

- = what happened it pulled back ahh I am not going to fall for this like I fell for it last time (look at number 4). Time to buy more; buy on the dip that's it.

- = I knew it, its going up and I made more money, wish I had bought more. Next time I will invest more on the pull back. (Notice the loser's mindset does not bother to take time to notice that the stock did not put in a new high. All that matters is that it went up).

- = it's going down again, time to really load up I don't want to lose this opportunity. Earnings are great so it must be a good time to buy some more.

- = first dose of bad news and the stock takes a big hit, okay this is just temporary it's going to go back up. (Blind faith (a huge mistake), one of the main ingredients of a losing mindset). Let me buy more and average down.

- = maybe I should sell now things don't look good, but you know what let me just hold for a bit longer maybe things will change. Yeah things have to change look how fast this stock went up and it has pulled back so much. The worst is over it has to go up.

- = this stock is dead I have to get out; it's not going anywhere (this is when the stocks start to bottom. The secret programmed desire to lose syndrome has completed its mission. Trader is in state of extreme distress and shell-shocked). I am never going to look at this stock again I knew it was garbage why did I ever buy it in the first place.

- = Slow base formations and the possible start of new up trend and the worst part is that this trader is out.

Personnel

Archives

- December 2008 (1)

- October 2008 (1)

- July 2008 (2)

- June 2008 (2)

- May 2008 (6)

- January 2008 (2)

- December 2007 (8)

- November 2007 (9)

- October 2007 (11)

- September 2007 (14)

- August 2007 (14)

- July 2007 (10)

- June 2007 (9)

- May 2007 (11)

- April 2007 (9)

- March 2007 (11)

- February 2007 (11)

- January 2007 (11)

- December 2006 (12)

- November 2006 (16)

- October 2006 (13)

License

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.

Another good posting of articles. Thanks for the time and effort to compile these. It's nice to have this balance of information as it relates to PO and all the other happenings of our quickly changing and intersting world in which we live. John

Wow!!!!!!

Any other time in history and a round-up of zinger headlines like that would signal financial collapse.

Not in "The new reality" of today.

I am begining to think that TPTB have a firm hand on things and can draw this out for a very long time.

The slow squeeze that leanan keeps suggesting.

I am so glad I sold out at the top earlier in the year thanks to you two and westexas.

In the mean time we are having a record year here at Soup Shop (think starbucks only a cup of nutrition instead of sugar & cafeen).

I've explained earlier that I don't think it's up to us to dispense advice; we compile news. That said, I'm glad that you did what you did, since it certainly won't hurt. Is that diplomatic and neutral enough? I also urge people to follow the example. The picture gets worse fast, as you will see in Friday 14th's upcoming Round Up. In the Dec 7 one, k-man noted what he did, and that all seemed very reasonable to me.

Offering good nutrition for good prices might be one of the few fields that remain standing. Still, how many can afford it, is hard to say.

Looks like HOPE NOW is working as designed. LOL. Scroll halfway down to where someone called the number.

Muddled Foreclosures: Whose Home is it Anyway?

Hi Uncle Ilargi, Thanks for the articles and about the above one, I thought I was thinking silly thoughts again, when I wondered how they would be able to figure out who held the mortgage for foreclosure, but I guess life is as silly as my thoughts. No wonder we are in trouble.

Also have brought a Canadian Christmas %toy% for us kiddies on the site, maybe you will tell us, Uncle dear, if you think there is good play value in it?:)

Thanks for the great round up of stories. I especially liked 'Architects of ABCP'. Seldom do we get a glimpse behind the curtain at the people pulling the strings and using financial lingo to confound even those with many years experience in the the field. I believe it was in August that Ben Bernanke had to have a face to face sit down with some of these 'financial specialists' so that he would have a clear understanding of exactly what they had created. Judging from the rate cuts mandated by the Fed in the face of a falling dollar I think that meeting might have frightened Ben...But, to be fair, Ben took the job when Greenspan knew the jig was up and got out...In time to write a book defending 'Greenspanisim' and ahead of the debacle ahead. Sort of like saying excuse me after stepping on anothers foot but before the other realizes that their shoe shine is gone. All Ben has to do now is save Wall St from itself once again, while destroying the savings, retirements, state mutual funds, et al, of all the people that are out here trying to make a living and put their kids through school. Here is hoping Attorney Gen of NY, Cuomo, puts at least a token number of these rascals in the crossbar hotel for a while.

Soup,I will be surprised and pleased beyond words IF[big if]they wire it together for another years.That means one more year to be a energetic squirrel.

Hello Ilargi,

Thxs for this compendium of finance info--much appreciated.

I still believe commodities or real assets is where its at in the years to come--my so-called biosolar mission-critical investing theme, at every scale, from bicycles on up to investing in NPK and solar power and wind turbine manufacturers.

If I was the Saudi King: I would be directing my finance ministers to forget buying dogs like CitiBank, but buying 'hen' control of POT and FSLR--then sending the 'eggs' back home to make KSA survivable without FFs. They could then export much FFs to really leverage their wealth. IMO, Biosolar-MPP is better than FF-MPP when the Hubbert downslope ride begins.

Of course, Canada would be better off to nationalize POT and the oilsands, plus any other vital resources to protect their future generations, and maximize their own biosolar-MPP. My feeble two cents.

Bob Shaw in Phx,Az Are Humans Smarter than Yeast?

Well, we've decriminalized pot. I suppose we'd have to legalize it before we nationalized it.

;-)

What ho Totoneila,

future generations? whazzat?

also MPP, whazzat too, some sort of POT

BTW, I agree with you about Potash long term but in between, if one has the time and stomach (which I don't), I think a lot of wealth redistribution could be had on the volatility that we are in store for. (had thoughts about dumping yesterday before Bernanke but dithered, oh well:)

Ian Gordon The Long Wave analyst writes that we are now entering the full force of the Kondratieff winter, and that a devastating depression worse than the great depression is unavoidable.

His advice(and others to) is to invest only in goldbullion and goldminingstocks.

There are a lot of articles about this global economic mess in english language. Very weird is the fact, that here in Sweden the ongoing collapse seems to go unnoticed. Everything seems normal, and they only write a little about the US housingproblems, as if it won´t effect us.

The housing collapse are spreading to Europe now. Downturns have started in Spain, GB, and France as i have read sofar.

Here in Sweden the condo prices in Stockholm topped out this summer, and prices are down about 10% now. The downturn will soon spread through the country.

I really believe we are very soon in for a global housingcollapse and a depression. I wonder about how much oil demand would be effected in a devastating depression. Could it give us some years of respite before we have shortages of gasoline?

Hi Swede, I am always glad to get a wake up call from you, just checked a gold basket (fund) which looks good at this point to get into . Are you looking at that other gold, Potash?

About shortages of gasoline, haven't you bought yourself an electric chainsaw yet?! (anyway a gas one uses very little petrol ) As far as gas for cars, where do you think you will go? Disco died a long time ago and unless you are into S&M or ultra-violence the streets will not be for the likes of thee or me:)

Here is something from Lao Tze somewhat on this point:

Hi CR

I am 100% in goldbullion and goldstocks(can´t loose much there). Potash?? what´s that?

As for gasoline, i need it for my floatplane. Other transportation needs i can manage with electrical bike during summertime. During winter time a little gasoline could be needed for my car until i have bought an EV.

100% gold, now with that in the pockets you will keep your feet on the ground and whistling a merry tune, but Swede, Swede, one can't chop wood with a float plane .... loose too many fingers that way and then you have all that wet wood and that's not a practical way to carry water IMO:)

What's Potash ? It is the golden substance that puts muscle to the rutabaga, clear sight to the carrot and tells the woodman to spare this tree. If you don't believe me ask totoneila.

Now that is one fine chap for the "yoicks , yoiks , tallyho me lads, follow that potash critter down it's Saskabush hole".

OK, now i know what potash is. Never heard of it before. Here in Sweden you get salt from the supermercado.

BTW i have electrical woodchoppers. But i usually buy the firewood cheap already chopped and delivered home. We have a group of mentally undeveloped guys here who does the job in the communitys supervision, so that they have some meaningful work to do.

Fertilizer.

CR,

The Bushman and the Hillabeast suspended the law of gravity and have a theory that the Kondratieff winter will be offset by global warming.

Hi musashi,

Don't you mean Global Smarming? Lot of that going round, did you see our Minister of the Environment, Baird, in Bali smarming all over global warming! He for sure has been playing kiss kiss with Bushman. Don't know if Hillabeast is in on that as well but if you find out that's a 'for sure', next year, let us know and we'll put an extra ice cube on the barbie for ya.

For those unfamiliar with Kondratieff long cycles try here (a little out of date) or here or here or here (PDF warning).

Click to Enlarge in New Window

Here's Mish's take on it from 2005:

I may write an article about this at some point.

That's SOO Funny. I just posted this on TOD Without even seeing this post On CTOD.

http://www.theoildrum.com/node/3365#comment-276564

This morning I read again about it, and I printed off the Color picture of the graph. (Don't have the URL of the pdf right now)

But I said it was "Dec. 20th 11pm and one hour till Winter Starts.

Deflation (of money supply) is coming. Price inflation on things like Energy, Food. (live chickens, Seeds, etc).

Also just read something bizarre on waves movements.

http://www.financialsense.com/fsu/editorials/2007/1211.html

Sent it to a financial friend I have and he stunned me by saying he's been studying it for a few years now.

Anyway Kondratieff is a subject that SHOULD get some play right now.

UrbanSurvival.com is even doing a Kondratieff thing this morning. 12/13

http://www.urbansurvival.com/week.htm

Thanks again for the work in collecting these stories. looks ugly going forward.

deflation/inflation

Is there a way for the fed to "print money" and "dump it from helicopters" via bailing out the banks?

It all must be accounted for on the books somehow.

If not I see deflation.

As I've noted before, my bear-of-little-brain view is that so much capital/credit is about to disappear through the breakdown in markets such as SIVs, CDOs and ABCP, as well as the general derivatives markets, that I simply don't see how central banks could print enough money, even if that were their goal.

People, to me, seem to accept a little too blindly that central banks will do all to save markets. If that were so, why would they have created the mayhem we're now in?

In Canada, the ABCP issue is still being worked on. I think there's another deadline coming up in a few days. But Skeena, remarkably, got its money out somehow.

Or did they?

Globe and Mail

And so with the markets finally reacting the way that they should to huge losses in the capital markets and the resulting credit tightening what does the Fed do?

They along with a few other central banks are going to pump massive amounts of liquidity into the system via "auction loans".

http://www.forbes.com/markets/feeds/afx/2007/12/12/afx4430096.html

The markets love it of course....just throw more cheap money at that problem. As long as we can keep the banks and consumers borrowing, we'll push off the inevitable just a little longer. Let the good times roll. The world has gone mad.

They are LOANS and are only available for bid to depositories for 30 days. If the sh*t paper defaults the foreign central banks eat the sandwich.

Reminds me of the old saying. "Life is like a sh*t sandwich. The more bread you have, the less sh*t you have to eat"

Maybe it puts some funds out there, but what happens if the funds are bid up to or above LIBOR out of desperation?

The goldilocks are running around beating their drums like the Eveready bunny, but they are just trying to suck a buck out of the sheep with market fluctuations.

"Black Swans and Endogenous Uncertainty" is a particularly good piece.

Indeed, the first half of it describes, in large part, how the complex world works: not just finances, but complex systems from human beliefs to the collapse of ecosystems. There's some deep stuff there, I recommend it.

Self-organizing criticality is all around us and we're part of it.

Nice to see it raised in this context.

I don't know, but I think Clive might just have hit it on the head. I mentioned the parallel to the movie "Payback" and Mel Gibson driving down an alley and hitting a car head on. ON PURPOSE. (you must see the movie to understand why).

See the sections I mean at the bottom.

Think about the last 10 years or so, Think how things unfolded.

NO WAY BACK - the horrible US economic morass

Clive Maund

I'm a realist too, not a Doom Monger.

http://www.321gold.com/editorials/maund/maund121307.html

CrystalRadio

Are you awake now? For me on the other side of the globe it is time to go to bed.

Happy New Year and Merry Christmas

God Jul och Gott Nytt År

HI Swede,

As much as ever I am and as convoluted as well.

I see by the 2:24 on your clock that you must have found a disco after all :) I will be in bed in 6 hrs by 9:00. I am not getting older (too old for that already) just practicing up for Olduvai.

BTW, where did you get that Festive 'Ar' with the decoration, neat.

A Merry Christmas to you too, I wish I could say that to you in my mother's tongue, Russian, but in that all I can manage is 'bread' and 'salt' and also I'm afraid my keyboard would have some sort of revolution if tried.

Happy New Year.

Веселое рождество и С Новым годом

Greetings Comrade musashiovich,

Great!! and the same of course to you. Now all I want for Christmas is to know how to write: 'There is always a Joker in the deck':)

Goldman chief’s pay set to hit $70m

Reading about all these wonderful "profits" being made by Goldman Sachs and the great bonuses being given to its employees somewhat loses its gloss after a peak at the article below

How fund managers make you pay for their mistakes