| The Finance Round-Up: December 3rd 2007 | The Oil Drum: Canada | The Finance Round-Up: December 11th 2007 |

The Finance Round-Up: December 7th 2007

Posted by Stoneleigh on December 7, 2007 - 9:54am in The Oil Drum: Canada

The lackluster investment strategy of China Investment exposes a central flaw in the Chinese economy, its lack of a rational system of capital allocation. For more than a decade, Chinese state-owned companies have made losses, and have been propped up by the banking system. Since 2004, loss-making state owned companies have been joined by overbuilding municipalities, erecting white-elephant office blocks in attempts to turn themselves into the next Shanghai.

None of these losses have resulted in bankruptcy; instead the cash flow deficits have been covered by the Chinese banks. As a result, the Chinese banks have an enormous volume of bad loans -- $911 billion at May 2006, according to a later-withdrawn estimate by Ernst and Young, which must surely have ballooned to $1.2-1.3 trillion now.

That explains why China Investment is somewhat un-aggressive in its international investment strategy. China’s $1.4 trillion of reserves are in fact almost all required to prop up the banking system, when the inevitable liquidity crisis occurs. If the banks are to survive, China Investment will have to be followed by six more sovereign wealth funds of equal size, each of which will have to abandon its attempts to take over Exxon or Google and pour its money down domestic rat-holes.

A $1 trillion problem in subprime mortgages has caused even the US money market to seize up and has required frequent applications of sal volatile by the Fed. Since China’s economy is around one fifth the size of the United States’ the Chinese banking system’s bad debt problem is in real terms about five times that of the United States, about 40% of its Gross Domestic Product.

We have seen this movie before; the Japanese banking system’s bad debts after 1990 totaled around $1 trillion, about 30% of Japan’s GDP. The result was the bursting of the 1980s bubble and a period of little or no economic growth that lasted well over a decade.

China to adopt tight monetary policies in 2008: report

China has decided to adopt tight monetary policies next year, marking the first change in its stance in a decade, state media said Wednesday.

Prudent monetary polices have been in place for the past 10 years, Xinhua news agency reported, suggesting a profound change in Beijing's economic policies.

Credit 'Crunch' - or Credit Collapse?

Under normal circumstances, recessions can be temporarily alleviated and even turned into another boom by injecting more "credit" (debt) into the economy. This is done by lowering interest rates, and central banks have a number of ways of achieving that.

But when banks don't trust each other and stop loaning money to each other, that's when you have a real problem on your hands.

If they don't trust each other, you can bet that they trust their customers less. We are already seeing mortgage lending standards tightening up - and that is happening even though interest rates have been lowered 75 basis points since the credit crunch hit this past summer, and further significant rate cuts are expected.

This puts banks in a bind: They can't trust borrowers to pay their loans back as they did in the past, but making loans is the primary way for them to make money. The result: They end up making fewer loans. Fewer loans mean they make less money.

Fewer loans also mean that the rate at which credit (the money supply) grows begins to shrink.

When this gets to a point where not only the growth rate of credit shrinks, but where the total amount of outstanding credit shrinks, we have a full-blown credit contraction in the making - and the name we usually pin on credit contractions is "Deflation."

Banks Urge UK Clients To Stop Borrowing

Banks have asked top U.K. corporate clients not to draw on lending facilities to which they are entitled in order to preserve their balance sheets as they approach the financial year end.

The banks are urging some of their biggest clients not to draw on standby credit facilities as the sub-prime crisis and squeeze on interbank lending have affected banks' ability to fund themselves.

The problems started with the closure of the commercial paper market as a means of cheap funding for companies in the summer. Banks have to provide standby financing of up to 100% to backstop commercial paper programs. With banks struggling for their sources of financing through the interbank market, the drawdowns are having a direct effect on their balance sheets.

Several bankers have said Citigroup (C) is one of those most affected and that the bank was asking some clients not to use standby facilities, which are part of the normal relationship banking arrangements made between banks and companies.

UK rate cut opens up gulf with ECB

A gulf opened up between Europe’s two largest central banks on Thursday after the Bank of England responded to the global credit squeeze by cutting interest rates while the European Central Bank indicated another increase was still on the agenda.

The Bank of England cut its main interest rate by a quarter of a percentage point to 5.5%, reflecting its concern that the medium-term economic outlook had darkened in recent weeks. However, Jean-Claude Trichet, ECB president, said the ECB had not jettisoned plans to raise rates from the current 4% level, pointing to divisions among the governing council members and highlighting how far the ECB remained from considering a rate cut.

Lex says it is “too easy to paint BoE governor Mervyn King as Santa Claus and Jean-Claude Trichet as the miserly Scrooge”. The simple fact is that the UK’s housing and consumption fetish has to soften and the Bank needs to let this happen.

Market fears that Bank of England has 'lost control'

There were fears in the City last night that the Bank of England has lost control of monetary policy after expectations for money market borrowing costs rose - despite the Monetary Policy Committee cutting interest rates.

Experts warned that it was a sign that the credit crisis could escalate over the Christmas period, even though the Bank has now embarked on a major series of interest rate cuts for the first time in almost eight years.

It coincided with a chilling warning from the Organisation for Economic Co-operation and Development that the UK economy is heading for a major slowdown next year - and possibly a "significant slump" in house prices.

This month's short sterling futures, which indicate where the market expects the key benchmark interbank borrowing rate to be in two weeks' time, actually rose markedly after the Bank's decision - an almost unprecedented reaction. The pound also ended the day up slightly on its trade-weighted index - another highly unusual outcome on the day of an interest rate cut.

John Wraith of Royal Bank of Scotland said: "They haven't got the control over rates in the financial system that they ordinarily have.

"Historically, a 25-basis point change in Bank rate would lead to an almost identical change in Libor [the benchmark rate in the money market]. That hasn't happened."

‘Snooty’ bankers blamed for crisis

The “snooty” attitude of bankers and financiers who thought they were cleverer than everyone else is largely to blame for the global credit squeeze “disaster”, Germany’s finance minister has said....

....After talks with the Bundesbank and the financial regulator, the banks that rescued IKB said they would cover a further $520m of possible losses in addition to their €3.5bn ($5.1bn) rescue.

Mr Steinbrück was critical of the management of Sachsen LB and IKB. “It is clear that the management . . . didn’t have the right management expertise.” They had been unable to cope with the complexity of the products in which they were investing, he said. Crisis talks on IKB’s future took place on Thursday but Mr Steinbrück said taxpayers would not foot a rescue bill.

Moreover, America is not the only country with an economic problem. The housing bubble is turning out to be worldwide, with a major impact on England and much of Europe. The biggest economic losers include the emerging markets, especially China. Don't believe for one second those Wall Street touts selling the notion that the emerging markets have "decoupled" from the US economy and their growth will lead the world forward without the American consumer. That’s hogwash. Where do you think their trade surpluses and big sales gains (driving investment in plants and equipment) came from anyway? From the American consumer and MEW! Take $800 billion of easy spending away from the American consumer and you're going to see a lot of blow back in lost sales by the emerging market countries, including China.

'Decoupling' Debunked as U.S. Collapse Infects World

It turns out the U.S. economy matters after all.

The credit collapse and dollar decline that followed a surge in U.S. home foreclosures jeopardize expansions in the U.K., Canada and Germany, economists said. They also debunk "decoupling,'' an argument advanced by analysts at Goldman Sachs Group Inc. and Morgan Stanley that the world wouldn't suffer as it did during U.S. slowdowns in previous decades.

The Bank of England and Bank of Canada this week followed the Federal Reserve in cutting interest rates, and the European Central Bank lowered its growth forecast for next year. British policy makers reduced their benchmark rate yesterday, even after Governor Mervyn King expressed concern about inflation just two weeks earlier.

"Two thousand and eight will be the year of `recoupling','' said Peter Berezin, an economist at Goldman in New York, explaining his firm's about-face. "What began as a U.S.-specific shock is morphing into a global shock.''

Decoupling is ``a good story, but it's not going to work going forward,'' Stephen Roach, chairman of Morgan Stanley in Asia, said in an interview in New Delhi on Dec. 2. His colleague, Stephen Jen, said in a report the previous week that because the possibility of a U.S. recession has increased, so has the chance that the rest of the world will falter.

Top CDO Classes May Lose 80 Percent, Barclays Says

U.S. mortgage assets in collateralized debt obligations have lost so much value that the top classes of the securities may be worth as little as 20 cents on the dollar in a liquidation, Barclays Plc analysts said in a report.

About 20 percent to 30 percent of principal would be covered for the ``super senior'' portions of mezzanine asset-backed bond CDOs, which mainly contain mortgage bonds and other CDOs initially assigned low investment-grade ratings, Barclays said in the report yesterday. The senior-most classes of CDOs containing highly rated asset-backed bonds would recoup 30 percent to 65 percent, it said.

Determining accurate prices for the collateral is hard to do, the New York-based analysts, Joseph Astorina, Elena Warshawsky and Wei-Ang Lee, said. ``We believe our methodology is analytically rigorous and represents a good jumping off point,'' they wrote.

Rabobank, Citigroup SIV sells almost half of assets

A structured investment vehicle (SIV) managed by Dutch bank Rabobank and Citigroup has sold almost half its assets, 4.5 billion euros ($6.6 billion), as the fund could not find sufficient refinancing, Rabobank said on Wednesday. "The market has dried up. It is all related to what is happening in the United States," a Rabobank spokesman said, confirming a report in Dutch daily Het Financieele Dagblad about the declining size of the fund, called Tango Finance.

The fund currently holds about 5.5 billion euros in assets, down from 10 billion euros in the summer, and could reduce its holdings further to reduce investment risks, the spokesman said. "Basically, what Tango is doing now is called unwinding," he said, adding that the market value of Tango's currently held assets is about 97 to 98 percent of their nominal value.

SIVs, off-balance sheet vehicles set up mainly by banks, issue a mixture of short-term senior debt and longer-term junior capital notes and invest the proceeds in long-term securities, mainly bank debt and asset-backed securities.

They have been hit by a double blow as their access to financing has dried up in the credit turmoil and the value of the securities they hold has fallen sharply.The spokesman declined to say whether Tango has been making losses or whether cooperatively-owned Rabobank would put the SIV's assets on its balance sheet if they could not be sold. He declined to say whether Citigroup, the largest bank in the United States, had invested in the fund.

Citi's Losses 'Greatly Exceeded' Profits for Subprime

Citigroup Inc., the biggest U.S. bank by assets, lost more money than it made from financial instruments based on U.S. subprime mortgages, a senior company executive said in a meeting at the British Parliament.

William Mills, chief executive officer of Citigroup's markets and banking division in Europe, said his bank had suffered ‘reputational damage'' from the fallout even though the New York-based company had made ‘adequate disclosures'' to customers who were trading subprime-related securities including collateralized debt obligations.

‘Our losses greatly exceeded the profits we made in this field over several years,'' Mills said at a hearing of the Treasury Committee today.

Bear Stearns faces new round of hedge fund claims

The first of a new round of investor claims was filed against Bear Stearns Cos. on Wednesday for its role in managing two mortgage hedge funds that collapsed earlier this year, securities lawyers said.

The claims, which will be submitted to the Financial Industry Regulatory Authority (FINRA) for arbitration, represent more legal challenges for Bear Stearns, which recorded losses this summer.The first of at least 11 new claims involves an unidentified Cayman Islands fund-of-hedge funds manager that lost $1 million in the Bear Stearns High Grade Structured Credit Strategies Enhanced Leverage (Overseas) Fund.

FINRA keeps the names of arbitration parties confidential. Lawyers for the fund declined to identify their client. Bear Stearns spokesman Russell Sherman declined to comment, saying he had not seen the complaint.Long considered one of the savviest bond traders on Wall Street, Bear Stearns suffered an embarrassing setback this summer as a rise in U.S. subprime mortgage defaults triggered a broader meltdown in mortgage-backed securities markets.

Credit risk to Canada remains: Bank of Canada

A Bank of Canada report says an unexpected shock in the already jittery global financial markets would have a profound effect on Canada's economy, possibly threatening the viability of some companies.

The central bank notes that while Canada has mostly weathered the continuing credit crunch crisis triggered by the U.S. subprime mortgage meltdown, it has not been immune. The risks of further damage to the economy remain real.

The conclusions are found in the bank's semi-annual Financial System Review and help explain the bank governors' decision Tuesday to cut interest rates in Canada by one-quarter of a percentage point.

The bank cited "global financial market difficulties," having "worsened since mid-October, and ... expected to persist for a longer period of time," as a key reason for its move, noting that tightening credit conditions and increased borrowing costs globally and in Canada.

CIBC warns of more subprime writedowns

Canadian Imperial Bank of Commerce posted higher fourth-quarter and full-year profits today, but warned of more subprime-related writedowns for its wholesale banking division, citing deteriorating conditions in the U.S. residential mortgage market.

Canada's fifth-largest bank said its fourth quarter profit rose to $884 million or $2.53 per diluted share, compared to year-ago earnings of $819 million or $2.32 per share.

Results for the quarter ended Oct. 31 were impacted by a slew of one-time items. Among them was an additional $463 million pre-tax writedown related to the falling value of its mortgage-backed securities, mostly offset by a $456 million gain related to Visa Inc.'s worldwide restructuring.

CIBC has already written down about 44 per cent of its $1.7 billion holdings of collaterized debt obligations and residential mortgage-backed securities and confirmed more markdowns are expected for the first quarter of fiscal 2008.

The Ontario government will join a growing parade of banks and private sector companies taking multimillion-dollar writedowns on commercial paper investments ravaged by a global liquidity crisis.

Ontario Finance Minister Dwight Duncan acknowledged in an interview yesterday that the government will be forced to write down the value of its investment in a class of short-term debt known as asset-backed commercial paper (ABCP)....

....Scott Blodgett, a spokesman in the Ministry of Finance, said the government has $719.5-million of ABCP on its books, accounting for less than 10 per cent of overall cash reserves exceeding $9-billion....

....Separately, Ontario Power Generation, the province's electricity utility, holds $103-million of third-party ABCP. OPG did not write down the value of the paper in the third quarter ended Sept. 30, but instead classified its holdings as "temporary" investments....

....The federal Auditor-General's office has said it plans to examine the Yukon government's decision to invest $36.5-million into the third-party ABCP, following weeks of pressure from opposition members.

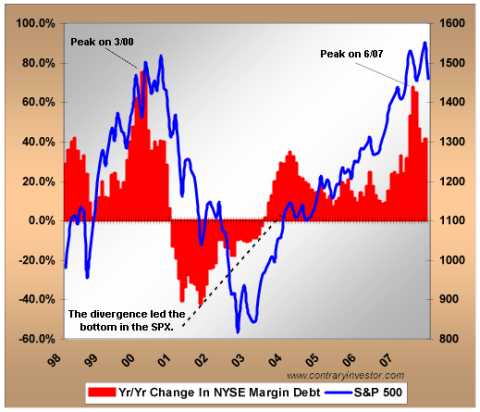

Unfortunately, and at least as of now, three discount rate cuts and two Fed Funds rate cuts have done little to nothing in terms of influencing the literal uninterrupted bleeding in asset backed commercial paper markets, the blowout of LIBOR spreads, swap spreads, and credit market spreads of all types. Maybe too simplistically, as we see it, the basic credit market problem of the moment is not liquidity, it's solvency and ongoing deterioration of collateral values underpinning mountains of in place leverage originally built on faulty forward collateral value growth assumptions. So will Funds rate cut numero tres most likely to be handed down this month be the silver bullet to change current credit market circumstances? Or will yet another rate cut ultimately prove as truly ineffective as the last two, heightening in investor perceptions the thought that the Fed is burning through precious monetary ammunition while completely missing the target?....

...Although we continue to believe that the credit markets are the key to financial market and real economic outcomes ahead, we want to have a quick look at the "other" credit market - margin debt - for potentially important messages that appear to us to be being overlooked at the moment.

As credit dries up in U.S., concerns mount about recession

Credit flowing to American companies is drying up at a pace not seen in decades, threatening the creation of new jobs and the expansion of businesses, while intensifying worries that the economy may be headed for recession.

The combined value of two major sources of credit - outstanding commercial and industrial bank loans, and short-term loans known as commercial paper - peaked at about $3.3 trillion in August, according to data from the Federal Reserve. By mid-November, such credit was down to $3 trillion, a drop of nearly 9 percent.

Not once in the years since the Fed began tracking such numbers in 1973 have these arteries of finance constricted so rapidly. Smaller declines preceded three recessions going back to 1975....

....In recent years, much commercial lending was inspired by an upward spiral of enrichment: Banks made new loans, then swiftly sold them off for profit, using the proceeds to extend still more. But with much of the financial world spooked by the mortgage meltdown, buyers for commercial loans are scarce, removing a reason for banks to lend in the first place.

What loans are being extended are going primarily to companies with long-standing relationships with banks. Lenders are reluctant to bet their increasingly scarce capital on riskier, less-established companies in a time of economic anxiety. That leaves many companies - smaller firms in particular - scrambling to get hold of finance.

"Small businesses are just inherently more risky, and banks are going to be more conservative in protecting their assets," said Jody Keenan, who heads the board of the Association of Small Business Development Centers in Burke, Virginia. "We're starting to see a tightening already, particularly for very small companies. We're talking about real impacts in local communities."

Why it's likely economy is in a recession now

Last Thursday the government's Bureau of Economic Analysis reported that the GDP expanded by an astounding 4.9 percent annual rate in the third quarter. That was on top of a very healthy 3.8 percent expansion in the second quarter. Given those numbers you'd think that the economy was still expanding nicely. You'd also have to conclude that all the bankers, consumers, businessmen and government officials expressing concern about the economy are nuts.

Over the past few years I've explained repeatedly in this column how both the employment and inflation numbers released by the government are tweaked to look better than they really are. Today you'd have a difficult time finding anyone who believes either of those government statistics are accurate.

The GDP figure is getting like that.

Foreclosure gridlock threatens economy

“You’ve got this massive gridlock,” said Ira Rheingold, executive director of the National Association of Consumer Advocates, which represents attorneys who act on behalf of homeowners facing foreclosure. “People sort of think they need to do something, but no one knows what to do. You’ve got all these different parties involved. How do you bring them all together?”

Paulson acknowledged the difficulties in getting various players involved to agree on new guidelines.

"The company collecting your mortgage payment every month is most often doing that on behalf of those who own the mortgage," he said Monday. "And they are limited in decisions that they can make on behalf of those ultimate owners who are spread all over the world."

The gridlock starts with the borrower who has fallen behind — or knows that they’re about to once their monthly payments jump. Most of the mortgages written at the height of the lending boom were resold to other lenders or bundled in portfolios with hundreds of other loans, chopped up into securities and sold to investors. As a result, some borrowers are having trouble even identifying the right company to contact.

Bill Gross (PIMCO): The Shadow Knows

The woven tangled web of subprimes has claimed more than its share of victims in recent months. Homeowners by the hundreds of thousands, to be sure, but also those that created, packaged, insured, distributed, and ultimately bought what should have been labeled "junk mortgages," but which by a masterstroke of marketing genius were given a more respectable imprimatur.

"Skim milk masquerades as cream," warned Gilbert & Sullivan a century ago and sure enough, modern day subprimes packaged into financial conduits with noms de plume such as "SIVs" and "CDOs" pretended to be AAA rated cubes of butter. Financial institutions fell for the charade hook, line, and sinker and now we all suffer the consequences. Defaults are rising, the dollar’s sinking, and good Lord—even Google’s stock price is going down. Something must really be wrong here.

It is. What we are witnessing is essentially the breakdown of our modern day banking system, a complex of levered lending so hard to understand that Fed Chairman Ben Bernanke required a face-to-face refresher course from hedge fund managers in mid-August. My PIMCO colleague, Paul McCulley, has labeled it the "Shadow Banking System" because it has lain hidden for years—untouched by regulation—yet free to magically and mystically create and then package subprime mortgages into a host of three-letter conduits that only Wall Street wizards could explain.

It's Not 1929, but It's the Biggest Mess Since

We are only at the beginning of the financial world coming to its senses after the bursting of the biggest credit bubble the world has seen. Everyone seems to acknowledge now that there will be lots of mortgage foreclosures and that house prices will fall nationally for the first time since the Great Depression. Some lenders and hedge funds have failed, while some banks have taken painful write-offs and fired executives. There's even a growing recognition that a recession is over the horizon.

But let me assure you, you ain't seen nothing, yet.

What's important to understand is that, contrary to what you heard from President Bush yesterday, this isn't just a mortgage or housing crisis. The financial giants that originated, packaged, rated and insured all those subprime mortgages were the same ones, run by the same executives, with the same fee incentives, using the same financial technologies and risk-management systems, who originated, packaged, rated and insured home-equity loans, commercial real estate loans, credit card loans and loans to finance corporate buyouts.

It is highly unlikely that these organizations did a significantly better job with those other lines of business than they did with mortgages. But the extent of those misjudgments will be revealed only once the economy has slowed, as it surely will.

Straight Talk on the Mortgage Mess from an Insider

I’ve kept up an active dialog with Mark Hanson, a 20-year veteran of the mortgage industry, who has spent most of his career in the wholesale and correspondent residential arena — primarily on the West Coast. His current thoughts, which I urge you to read:

The Government and the market are trying to boil this down to a ’sub-prime’ thing, especially with all constant talk of ‘resets’. But sub-prime loans were only a small piece of the mortgage mess. And sub-prime loans are not the only ones with resets. What we are experiencing should be called ‘The Mortgage Meltdown’ because many different exotic loan types are imploding currently belonging to what lenders considered ‘qualified’ or ‘prime’ borrowers. This will continue to worsen over the next few of years. When ‘prime’ loans begin to explode to a degree large enough to catch national attention, the ratings agencies will jump on board and we will have ‘Round 2?. It is not that far away.

Since 2003, when lending first started becoming extremely lax, a small percentage of the loans were true sub-prime fixed or arms. But sub-prime is what is being focused upon to draw attention away from the fact the lenders and Wall Street banks made all loans too easy to attain for everyone. They can explain away the reason sub-prime loans are imploding due to the weakness of the borrower.

How will they explain foreclosures in wealthy cities across the nation involving borrowers with 750 scores when their loan adjusts higher or terms change overnight because they reached their maximum negative potential on a neg-am Pay Option ARM for instance?

Sub-prime aren’t the only kind of loans imploding. Second mortgages, hybrid intermediate-term ARMS, and the soon-to-be infamous Pay Option ARM are also feeling substantial pressure. The latter three loan types mostly were considered ‘prime’ so they are being overlooked, but will haunt the financial markets for years to come. Versions of these loans were made available to sub-prime borrowers of course, but the vast majority were considered ‘prime’ or Alt-A. The caveat is that the differentiation between Prime and ALT-A got smaller and smaller over the years until finally in late 2005/2006 there was virtually no difference in program type or rate.

Middle class and out of a home in Chicago

The home mortgage meltdown isn’t just gutting the poorer parts of town.

It’s beginning to hammer wealthy and middle class Chicago neighborhoods like Lincoln Park, Lincoln Square, Irving Park, Portage Park and Mt. Greenwood — all areas where home mortgage foreclosures have shot up by 100 percent or more from 2006 to 2007.

Data released Monday by the National Training and Information Center shows that in Lincoln Park there were 18 homes in foreclosure during the first six months of 2006 — but that number more than doubled to 37 for the first half of this year.

In terms of sheer numbers, poor neighborhoods still are feeling the worst pain. But percentage increase in mortgage defaults is climbing faster in middle class areas, according to the data.

Poverty stricken West Englewood, for example, had 348 foreclosures, or 111 per square mile — yet that was just a 58 percent increase over the previous year.But in middle class Portage Park, the heart of the Northwest Side Bungalow Belt, mortgage defaults jumped from 32 homes to 94, a whopping 193.8 percent.

"You had a lot of upper-income people taking advantage of the low rate adjustable rate mortgages, interest only loans and other programs that were available in order to move up, to get an extra two or tree bedrooms," said Jeff Metcalf, president and CEO of Record Information Services, which provided much of the raw data used NTIC analysis.

The Mogambo Guru: The shock of a thousand trillion

In his own words, Mr Roubini said, "Losses due to subprime alone will be as high as $400 to $500 billion and this does not count losses due to near prime, prime mortgages, auto loans, credit cards, commercial real estate, leveraged loans, loans to the corporate system; if added all up losses could end up - in a US recession - as being as high as $1,000 billion or $1 trillion. The financial bloodbath thus has only started and a hard landing of the economy is clearly ahead of us."

A trillion? It used to be that a trillion was a lot of money, but my eyes opened when I saw the Opednews.com article by Sharon Kayser, titled, "Hey Buddy, Can You Spare $1,000 Trillion?"

Instantly, I knew that someone had erred! A thousand trillions? Hahaha! What a preposterous number!

So I was instantly on the phone to call Ms Kayser so I could tell her that there has been an error in the title, and then maybe, you know, she could drop a line to my boss and tell her what a nice guy I am and how firing me right before Christmas is so tacky, no matter how well-deserved, or maybe she could get me a job there with her or something.

So imagine my horror when I learned that there was no error! We are talking about a quadrillion freaking dollars! Instantly I knew that she was doing that on purpose to give me a heart attack!

Surge in Auto-Loan Delinquencies Is Latest Trouble for the Economy

First came housing loans and the subprime-mortgage crisis.

Now, signs of stress are creeping into another key consumer area: auto loans.Delinquencies in the auto-loan market are ticking up to their highest level in several years. Lenders are tightening terms in some cases, and interest rates have risen from the rock-bottom levels of a few years ago. About $575 billion in loans for new and used cars are made annually, according to the National Automotive Finance Association.

About 4.5% of auto loans made in 2006 to top-rated borrowers were at least 30 days delinquent as of the end of September, up from 2.9% the previous month, according to a Lehman Brothers survey of companies servicing these loans. That is the biggest one-month jump in at least eight years. Lehman says 12% of subprime borrowers, who have poorer credit records, were delinquent on their 2006 auto loans as of September. That is the highest level since 2002 and up from 11.1% the previous month.

"The numbers will get worse for auto loans," says Dan Castro of GSC Group, a New York firm that runs debt-related investment funds. "We're starting to see signs of rising losses, and delinquencies are creeping up."

I have already commented before on why an across-the-board (like in the Treasury/banks plan) rather than a case-by-case approach to sub-prime mortgage restructurings makes sense.

Moreover, the attempt to distinguish between those who are insolvent and would default anyhow (even after a freeze of the reset rate), those who can pay and don’t need debt relief and those who are illiquid but solvent (i.e. can likely keep on servicing their mortgages if the teaser rate is frozen for a while) also makes sense.

Of course, the Treasury plan may or may not provide enough relief to enough homeowners depending on how it is implemented. But its basic conceptual approach is sound.

Hmmm, Reggie Middleton, for one, doesn’t think so:

A few posts ago, I linked to Nouriel Roubini's blog, commenting on how I vibe with his strategic thinking. Well, he just posted a piece on the subprime plan that I completely disagree with. I had planned to stay away from this topic, but since I already implicitly endorsed him, I might as well clear the air. I have a lot of respect for his prescience and foresight in calling the real estate bust (because he agreed with me:-), but...

I thoroughly disagree with the good Doctor on this subprime thing. Most of my points have been covered by others in the comments on his blog and others, but a major one seems to be continuously missed by all, including our current administration -

This was never a subprime problem. It was a bad underwriting problem.

These defaults that you see in subprime, are now manifesting in Alt-A, prime and everything in between. Not just housing either - consumer finance, auto, boats, credit cards, you name it.

Hope Now Alliance: Not to be confused with Apocalypse Now Mortgages

Two of the major lenders in the talks are Washington Mutual and Countrywide Financial. Their stocks soared last week because of this plan. There is a reason that these companies are rubbing elbows with government officials. Where Fannie Mae and Freddie Mac have only about 15 percent exposure to California mortgages in their portfolios, Countrywide and WaMu have get this, 40 to 50 percent! This is according to a report issued by Goldman Sachs in October. Now think about that for a second.

California has been one of the last states to start showing actual declines in home prices. In fact, we only started seeing median decreases a few months ago in certain counties. These are horrible indicators for market predictions but these numbers are used in determining comparable sales and psychologically impact the overall market. Southern California is down as a whole, only 8 percent on a year on year basis. Now imagine how large this impact will be when we hit double digits in 2008? Fannie and Freddie have been MIA in California because $417,000 just doesn’t cut it here.

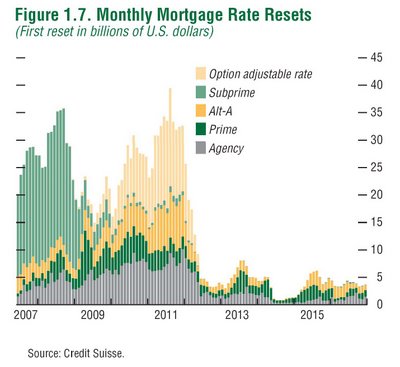

Remember all the talks about raising caps to $1 million? At least we can say that the Fed has shut up about such preposterous plans considering California is about 25 percent of the entire mortgage market and the reason Fannie and Freddie aren’t having it as bad as they should is because caps at least kept them in check to a certain extent. We are certainly in for a prolonged housing bear market. But thinking that sub prime is the main reason is naïve and flat out wrong. Take a look at the amount of Alt A and prime loans resetting next year:

Certainly with the chances of a recession increasing, many of these prime and Alt A borrowers will have a hard time making their payments. Will we allow these folks to freeze their rates? Why can’t we have the government step in and freeze rates for credit cards after their initial APR promotion is due? This is an apt comparison. We all know that 3.9 percent cannot last forever and expect 18 to 24 percent in the future.

U.S. mortgage foreclosures at record high: Mortgage Bankers

A record number of U.S. mortgages were somewhere in the foreclosure process in the third quarter, with 1.69% of all residential borrowers facing the loss of a home, the Mortgage Bankers Association said Thursday. The percentage of homes that entered foreclosure in the third quarter also hit a record at 0.78%, the trade group said.

Mortgage delinquencies, those loans with payments that were more than 30 days past due, shot up to a 21-year high at 5.59%, MBA's quarterly survey showed. Although all types of loans showed an increase in foreclosure starts in the third quarter, subprime adjustable-rate loans remained the biggest problem, accounting for 43% of all new foreclosures, even though they comprise just 6.8% of all loans outstanding, the MBA said.

The chill spreads to commercial real estate

The global credit crunch that took hold of financial markets in the summer is now taking the steam out of commercial real estate.

Office buildings, warehouses and shopping centers looked like a safer haven for big investors wary of falling prices for houses and condominiums. But now, the commercial side is feeling the pinch.

Even Southern California, which has been one of the country's favored markets for investment in recent years, has seen sales cool off and prices paid for business properties decline. Some owners are holding onto their buildings and waiting for the market to improve.

But with a falling stock market, a shrinking dollar and widespread concern about recession, real estate deals are getting dicier.

"The biggest issue on both sides -- seller and buyer -- is that no one wants to pay or sell at a bad price," said real estate analyst Raymond Torto. "They are all searching for 'the market.' "

Subprime bond losses to climb to 20 pct -analysts

Expected losses for troubled mortgages known as Alt-A loans are now more than double earlier forecasts and losses for subprime bonds originated in 2006 may climb to 20 percent or more, analysts said on Tuesday.

Moody's Investors Service on Tuesday raised its forecast for expected losses for U.S. mortgages known as "Alt-A" residential mortgage debt. Loss estimates for Alt-A bonds reviewed by Moody's increased by an average of 110 percent from initial expectations, with some loss estimates up by as much as 270 percent, Moody's said in a report.

Alt-A mortgages are made to borrowers with credit scores above subprime but who have other risky attributes, such as no proof of income or lack of an equity stake in the property. "Alt-A performance has not been very good," said Jonathan Polansky, a managing director at Moody's Investors Service, during a panel discussion at a bond conference on Tuesday.

For subprime bonds, losses for those underlying securities for collateralized debt obligations, or CDOs, are expected to be "well over 20 percent," said Kevin Kendra, managing director for structured credit at Derivative Fitch.

Caroline Baum: Paulson Goes to Washington, Loses Way

If you're like me, you've spent the last few days sorting through the sketchy outline of the U.S. Treasury's subprime rescue plan and mulling the potential impact. (Hey, I never said I was a swinger!)

We learned last week that Treasury Secretary Hank Paulson was working with the mortgage industry and major financial institutions to craft a plan to freeze introductory teaser rates on certain subprime mortgages that are due to reset higher, as specified by the original terms of the loan.Such a plan is easier said than done.

In the old days, a mortgage lender -- in many cases, your local banker -- had a relationship with the borrower. When a homeowner fell upon hard times, he and his banker would sit down to renegotiate the loan. It was in the interest of both the homeowner (he keeps the house) and the banker (he avoids costly foreclosure) to modify the loan terms.

Nowadays, subprime loans are bundled, sold, chopped up into pieces and packaged into collateralized debt obligations. The lender -- in this case, the owner of a CDO tranche -- has been replaced by a Cayman Islands hedge fund, a Florida municipality or a German bank. Their interests aren't necessarily aligned with those of the homeowner, not to mention one another.

PAULSON'S MORTGAGE LIFE-LINE MAY TURN INTO A NOOSE

Treasury Secretary Hank Paulson's new safety net to prevent a flood of home foreclosures could actually drown many hard-working homeowners who never missed a mortgage payment, experts say.

"This is not a silver bullet," Paulson said yesterday in a speech offering the first glimpse of his rescue project that's been making the rounds in Washington for weeks.

"This plan, in and of itself, is not going to deal with all of the problems associated with the housing market and bad lending practices," he said.

Paulson offered no specific criteria on which homeowners would get picked for a seat on the lifeboat, or who would be left adrift.But he did suggest that homeowners who have good credit and on-time payments might not be eligible for any relief from paying the hundreds of dollars in additional monthly payments when their reset mortgage rates balloon in the coming months.

Government, Industry Craft Plan to Slow Foreclosures

The plan, Paulson added, "does not, and will not, include spending taxpayer money on funding or subsidies for industry participants or homeowners."

Questions remain, though, about how many investors, who bought bonds backed by these mortgages and are spread out around the globe, will agree to change the terms of the loans.

Under the plan, borrowers will fall into four categories. Those who:

- Can afford their adjusted interest rate. They'll receive no assistance.

- Have been unable to make payments at their ARM's "teaser" rate. They will probably "become renters again."

- Can qualify for a refinance loan. Lenders should quickly get these borrowers into new loans.

- Have steady incomes and good payment histories and can afford the teaser rate but not the higher payments once their loan rate resets.

"We are focusing on this group," Paulson said. He didn't say how many homeowners might be saved. Interest rates for these borrowers could be frozen at the teaser rate for three to six years, according to some proposals on the table.

Before even debating the details of Henry Paulson’s new plan to prevent foreclosures, I think it would be logical to first ask the question:

What causes foreclosures?

Your gut instinct may tell you it is not being able to make the mortgage payments. Even though we have been inundated with media coverage about this (i.e. impact of rate resets on ARMs), the truth is:

This is NOT the primary reason for foreclosures at all.

The main driver of foreclosures is THE CHANGE IN REAL ESTATE PRICES.

Excerpt from Boston Globe article:

The recent spike in home foreclosures in Massachusetts is CAUSED BY FALLING HOME PRICES, AND NOT BY RISING MORTGAGE PAYMENTS, according to research released yesterday by the Federal Reserve Bank of Boston.

The contrarian report suggests the common understanding of the foreclosure crisis is somewhat mistaken. Unaffordable loans don’t cause foreclosures directly. Even as subprime lending became more common, even when people fell behind on mortgage payments - during the economic downturn in 2001, for example - foreclosures were rare because house prices continued to rise.

Housing price movement “PLAYS A DOMINANT ROLE IN GENERATING FORECLOSURES,” the report concluded.

One implication of the report is that current attempts by local and federal officials to help borrowers may be ineffective.

US Treasury Secretary Henry Paulson is negotiating a deal to freeze monthly mortgage payments on some subprime loans by delaying scheduled interest rate increases. Paulson reiterated yesterday the plan could be announced this week.

This proves that the Paulson plan is a phony PR stunt because it does not address the PRIMARY CAUSE of the foreclosure problem. Foreclosures are mostly driven by declining homeowner equity—especially NEGATIVE EQUITY.

Et tu Subprime? Why This Mortgage Proposal is Hot Air…As of Today

I’ve been digging deeper into the current Bush plan and if this doesn’t smack of political posturing with no meat, I really don’t know what does. Let us refresh your memories of what Mr. Bush said in August of this year:

President Bush said Thursday concern should be shown to those who’ve lost their homes but it’s not the federal government’s job to bail them out.

Today we get the following message from Bush:

“We should not bail out lenders, real estate speculators or those who made the reckless decision to buy a home they knew they could not afford,” he said today, adding there is no perfect solution. “The homeowners deserve our help. The steps I’ve outlined today are a sensible response to a serious challenge.”

And in the same breath they are offering a 5 year rate freeze. You shouldn’t jump to any quick conclusions like the market did today because a study by investment bank Barclays Capital found that of the 2 million subprime ARMs expected to reset from now until 2009 a mere 240,000 would be covered by this freeze. Keep in mind there was a lot of brouhaha when the FHASecure act was issued only a few months back and this program is expected to cover another 200,000 subprime borrowers. Not to be out done, the Democrats have come out with equally irresponsible proposals. Clinton is calling for a foreclosure moratorium.

Peter Schiff: The mother of all bad ideas

Without question, the Bush administration’s mortgage rescue plan will exacerbate, not alleviate, the problems in the housing market. As the plan will sharply reduce the ability of new buyers to make purchases, it really amounts to a stay of execution and not a pardon.

Although there are mountains of uncertainty as to how the plan will be structured and implemented, there is no question that as lenders factor in the added risk of having their contracts re-written or of being held liable for defaulting borrowers, lending standards for new loans will become increasingly severe (higher down payments, mortgage rates, and required Fico scores, lower loan to income ratios, and perhaps the death of adjustable rate loans altogether). The result will be additional downward pressure on home prices, despite the fact that in the short term fewer homes will be sold in foreclosure than what might have been without the rescue plan.

Most homes temporarily saved from foreclosure will continue to depreciate as new buyers fail to qualify for loans. As a result, lenders will be on the hook for more losses than had the foreclosures taken place sooner. Of course, as these chickens will likely come home to roost after the next election, that’s a trade-off incumbent politicians will happily make.

Compounding the problem is that subprime borrowers with frozen payments on loans that exceed the values of their homes will likely choose not to pay property taxes, condo or homeowners fees, or maintain the condition of their properties. Were these properties to be sold in foreclosure now, at least their new owners would have financial incentives to maintain the value of their investments. Upside-down subprime borrowers will have no incentive to throw money down a rat hole: why make additional payments on properties in which they have no equity and which they will likely lose to foreclosure anyway? When these homes do go into foreclosure, back taxes and other fees on dilapidated properties will inflict even greater losses on lenders.

Housing Slump's Third Year to Be 'Deepest' Since WWII

As the U.S. housing slump enters its third year, there is no sign of dawn in the darkness that is paralyzing home building, home buying and home lending.

Standard & Poor's 15-member Supercomposite Homebuilding Index tumbled 62 percent this year as of yesterday, the largest drop since the benchmark was started in 1995. The companies have lost about $35 billion of market value.

The outlook is bleak with new home sales projected to fall 13 percent in 2008, according to estimates from the National Association of Realtors in Chicago, even as interest rates drop. Losses at Fannie Mae and Freddie Mac, the two biggest U.S. providers of mortgage financing, may restrict the availability of home loans, and chief executive officers at D.R. Horton Inc. and Centex Corp. expect another tough year.

``This looks like it's going to be the deepest correction of any housing correction since World War II, and the question really is, `What's the duration, how long will it be?''' Centex CEO Timothy Eller said at a JPMorgan Chase & Co. conference in Las Vegas on Nov. 27.

House prices seen falling 30 pct

Housing markets from Punta Gorda, Florida, to Stockton, California, will crash and suffer price drops of more than 30 percent before the housing crisis is over, a report from Moody's Economy.com said on Thursday.

On a national level, the housing market recession will continue through early 2009, said the report, co-authored by Mark Zandi, chief economist, and Celia Chen, director of housing economics.

The report paints a worsening picture of the hard-hit housing sector, which is in the midst of its worst downturn since World War II.

While activity will stabilize in 2009, it will not be until 2010 before a measurable improvement in sales, construction and pricing will emerge, the report said.

House prices are forecast to fall 13 percent from their peak through early 2009. After accounting for incentives home sellers are offering buyers, effective declines peak-to-trough will total well over 15 percent, the report said.

Morgan Stanley: Report sees years of losses ahead

Even a quick Christmas fix aimed at cooling down the foreclosure crisis won't help the housing industry's deeper ills for years to come, experts say.

A barrage of grim reports yesterday raised fears of an unprecedented wipeout of home prices over the next three years, erasing as much as 30 percent of a home's value in many areas.

That bleak assessment from Morgan Stanley and Moody's Investors Service hit just as another report warned that even good credit risks are suddenly turning delinquent on their payments, dragging down mortgage banking's healthiest chunk of business. The Mortgage Bankers Association says it's alarmed by the surprising jump in third-quarter delinquencies on prime loans held by the most credit-worthy owners.

Morgan Stanley said the ongoing collapse of junk mortgage paper, combined with a decline in available credit, has plunged the US real-estate industry into "a very different environment on the heels of market events that could force a housing recession like none ever imagined or experienced."

"History has never seen such extended periods of house-price declines," it added.

Three Systemic Risks to Watch For

I was asked recently, “What’s the next shoe to drop?”

At the risk of being indecisive, I believe there are three large systemic risks out there that have yet to be fully appreciated by the market.

The first is home equity credit. Beyond the alarming 16.5% 60 day delinquency statistic reported by Moody’s last week on home equity credit nationwide at the end of June, there is the question of collateral coverage. Generally speaking, home equity loans represent a junior mortgage. In the old days, home equity loans were obtainable for just some portion of the appreciation of home values, but in this credit cycle, home equity lines provided credit up to 110% of a home’s value at peak valuation.

Given the deflation in home values, I believe that many home equity loans today represent at best partially secured credit, if not unsecured credit. To my knowledge, few home equity lines were either underwritten or priced with this in mind. As a result, I believe that home equity loan losses will far exceed even the most current pessimistic forecasts.

The second risk area I see is municipal credit. Beyond the now well-reported Ambac and MBIA solvency issues, and the State STIF fund, SIV problems are looming a large property tax shortfall. Whether it is a function of home borrowers’ inability to pay or borrowers’ ability to pay lower taxes due to successful assessment appeals (lower property tax payments due to lower home values), I believe local and state municipalities are in for a very hard time. And without serious, immediate cuts in services, municipal debt ratings are likely to fall (and if AMBAC and MBIA fail, fall hard).

The final risk I see is derivative counterparty risk. Or put differently, how financial institutions can be both right and wrong at the same time. Underlying our financial system today are trillions of dollars of over the counter swaps covering everything from future of interest rates to the future of GMAC debt - where money is owed to one counterparty from another based on what happens in the future.

MBIA and Ambac's Capital in Doubt

It took a while but Moody's is finally coming to the realization that MBIA and Ambac capital is in doubt.

MBIA Inc. had the biggest drop in more than 20 years in New York Stock Exchange trading after Moody's Investors Service said the biggest bond insurer is "somewhat likely" to face a shortage of capital that threatens its AAA credit rating.

"The guarantor is at greater risk of exhibiting a capital shortfall than previously communicated," New York-based Moody's said. "We now consider this somewhat likely."

Mish: "Somewhat likely" is certainly a strange way of putting it. I suspect "nearly guaranteed" is closer to the truth.

The loss of MBIA's top ranking would cast doubt over the ratings of $652 billion of state, municipal and structured finance bonds that the company guarantees. MBIA is among at least eight bond insurers seeking to ward off potential credit-rating downgrades by Moody's, Fitch Ratings and Standard & Poor's. The insurers guarantee $2.4 trillion of debt and downgrades could cause losses of $200 billion, according to Bloomberg data.

Mish: The entire idea that junk Municipal Bonds can carry an AAA rating based on "guarantees" is now in question. The implications of an across the board downgrade of municipal bonds is very serious.

Please note that California Forgoes Insurance On Municipal Bonds. If MBIA and Ambac attempt to raise prices for guarantees, more states like California will simply refuse to pay. This makes it unlikely that insurance hikes are the way out for the insurers.

Florida Says Unfreezing Fund Would Spark 'Fire Sale'

Florida schools and towns with money frozen in a state-run investment account are unlikely to get their cash back tomorrow, when officials meet to discuss a crisis prompted by withdrawals that drained almost half of the fund's $27 billion in assets, a policy officer said.

``If we reopen the window without limitations on Tuesday, and we see behavior like we've seen up to now, there's simply no way to meet that demand without having a fire sale on assets,'' said James Francis, senior policy officer for the State Board of Administration, manager of the Local Government Investment Pool....

....Florida counties and schools pulled out $13 billion in assets last month after learning the pool, described by state officials as a money-market fund, held $1.5 billion of downgraded and defaulted debt tainted by the subprime mortgage market collapse. The crisis shows the far-ranging effects of the housing slump, as complex investments once sold as high-yielding havens are now backed by collateral investors don't want.

Florida Just First to Face National Run on the Bank

Florida officials are going to meet today [Dec 4] to talk about the crisis in the state's Local Government Investment Pool. I don't know what they are going to talk about, but I know what they had better decide.

The investment pool, which contained $27 billion this summer, now has $14 billion, the result of withdrawals by municipalities with keenly developed senses of self- preservation. On Nov. 29 the board told the remaining participants they couldn't withdraw any more money from the pool.

The pool, which is where most of the state's municipalities put their money when they are not using it, owns $1.5 billion in securities that have been downgraded or defaulted as a result of the subprime market collapse.

In freezing the pool, Coleman Stipanovich, executive director of the board, said, ``If we don't do something quickly, we're not going to have an investment pool.''

The state stopped the clock.

The same clock is ticking for every state in the country where school districts and cities and towns put their faith in someone else, usually at the county or state level, to manage their money. This means, I think, most of them.

Moody's May Cut Ratings on $105 Billion of SIVs

Moody's Investors Service is preparing the biggest credit rating cuts since subprime mortgages contaminated the bond market, foreshadowing losses for investments that pay Florida teachers and money market funds.

Moody's may lower ratings on $105 billion of debt sold by structured investment vehicles after the average net asset values of SIVs sponsored by firms including New York-based Citigroup Inc. declined to 55 percent from 71 percent a month ago, Moody's said in a statement Nov. 30. The assets were valued at 102 percent in June.

``The assets that SIVs hold are continuing to decline in value,'' said Ira Jersey, an interest-rate strategist in New York at Credit Suisse Group, Switzerland's second-biggest bank by assets. ``As they do that it's creating more problems for the holders.''

'Super Fund' for SIVs, Hoped for $100 Billion, May Be Half the Size

The three banks assembling a "super fund" aimed at helping to ease the global credit crunch are scaling back its size due to a lack of interest from financial firms that are supposed to benefit from the plan, according to people familiar with the matter.

Originally envisioned as a $100 billion fund that would buy assets from the struggling investment vehicles, the fund may now wind up being about half that size, these people said.

A trio of large financial firms -- Citigroup Inc., Bank of America Corp. and J.P. Morgan Chase & Co. -- have been working since September to find a way to provide liquidity for off-balance-sheet entities, known as structured investment vehicles. The SIVS, which issue short-term debt to buy other, higher-yielding assets, have been hurt by the credit crunch that has left buyers for the debt on the sidelines due to concerns about exposure to subprime-mortgage securities.

People familiar with the banks' plans say they are proceeding with the fund despite the smaller size. The banks, which have informally been seeking participation from other financial institutions, expect to start a formal syndication process within the next several days.

Hillary Clinton and George Bush: Two of a Kind

With Hillary's Letter to Treasury Secretary Henry Paulson calling for Immediate Action to End Foreclosure Crisis she proves she is no better than George Bush.

Here is the paragraph in question:

I will consider legislation that enables lenders to convert unworkable mortgages into stable, affordable loans without the permission of investors. Protection from lawsuits will remove the obstacle that keeps lenders, servicers and others from turning mortgages that were designed to fail into mortgages families can afford. Right now, servicers who process monthly loan payments and interface with homeowners have flexibility to modify loans. However, they are reluctant to fully exercise this discretion in part because they fear investor lawsuits. Investors who own the securities into which the mortgages have been packaged may assert that they are harmed when servicers help at-risk borrowers. Protection from lawsuits could enable the servicers to help homeowners avoid foreclosures, help investors avoid the losses they would otherwise suffer, and help the economy.

Her entire proposal is complete nonsense but the above is downright scary. Bush ignores the constitution from the oval office and Hillary obviously has no regard for constitutional issues either. Hillary Clinton has just proven she would be no better than President Bush.

This should be a wakeup call for America and I hope it is. The country cannot stand four more years of Bush in the White House and that is exactly what we will have if she is elected.

It's time to get behind the one and only candidate who stands behind the constitution. That person is Ron Paul.

Wall Street firms subpoenaed by N.Y.: report

Prosecutors seeking information on debt tied to high-risk mortgages

Several Wall Street firms have been subpoenaed by New York state prosecutors seeking information related to the packaging and selling of debt linked to risky mortgages, according to a published report Wednesday.The office of New York Attorney General Andrew Cuomo has sent subpoenas to request information from several Wall Street firms, including Merrill Lynch & Co. , Bear Stearns Cos. and Deutsche Bank AG, The Wall Street Journal reported, citing people familiar with the matter.

Prosecutors in a broader investigation of the mortgage business are looking into how well the banks examined the quality of mortgages before packaging them into products sold to investors, the report said. The probe also focuses on how the debt was pooled into securities, including banks' arrangements with credit-rating firms, the newspaper reported.

Fed May Couple Cut With Measures to Increase Credit

Federal Reserve officials, who are forecast to lower their main interest rate next week, are signaling that they are looking for additional ways to increase credit to companies and consumers.

The Fed may lower the discount rate -- what it charges banks for short-term direct loans -- by a quarter-point more than the benchmark rate after Vice Chairman Donald Kohn and San Francisco Fed President Janet Yellen publicly expressed frustration that previous rate cuts haven't encouraged banks to lend to one another.

Such a move would narrow the gap between the two rates -- normally 1 percentage point -- to a quarter-point. Economists said that may spur lending by easing the stigma of borrowing at the discount rate, letting firms claim they are taking advantage of a better deal.

"The Fed has to re-liquefy the markets to reduce the risk of a financial accident,'' said Lou Crandall, who used to work at the New York Fed and is now chief economist at Wrightson ICAP LLC, a Jersey City, New Jersey-based research firm that focuses on government

An Irrelevant Fed: Thimbles of Water in a Forest Fire

Last week, investors made a great deal about an $8 billion 43-day repo that the Fed initiated. While this was reported as an extraordinary measure to stabilize the financial markets, the fact is that the Fed regularly enters a long-dated repo every year, just before the holidays, in order to accommodate a moderate increase in the demand for currency (in 1999, the amount was massive because of year-2000 fears, and was quickly reabsorbed after the new year). The $8 billion repo the Fed entered last week amounts to roughly $25 per American in extra cash to carry around the malls. To frame this as some sort of extraordinary effort to stabilize the banking system is absurd.

Again, the problem with the U.S. financial system here is not liquidity, but the solvency of mortgage loans and securitized debt. The Fed's actions are not likely to have material impact on this.

Federal Reserve: Home equity falls in 3Q

The amount of equity homeowners hold in their homes slipped in the third quarter to the lowest level on record, just above 50 percent, according to a report from the Federal Reserve Thursday.

In its quarterly U.S. Flow of Funds Accounts, the central bank reported that homeowners' percentage of equity dipped to 50.4 percent from 51.1 percent from the previous quarter. On average, housing is Americans' single largest asset.

Economists expect this figure, equal to the percentage of a home's market value minus mortgage-related debt, to tumble even further as falling home prices eat into equity. It could easily drop below 50 percent by the end of next year, some experts say, marking the first time homeowners will owe more than they own since the Fed started recording the data in 1945.

The Bubble Economy, the Dollar, or Both?

For too long, our economy has relied on the expansion of credit at the expense of real productive achievement. Additionally, government edicts and monetary policy have distorted the market process to such a degree that a free market economy certainly is not what we have at this point. They may try to fool you into thinking that one exists, but the reality is the economy has been "shepherded" to the point where laissez-faire might as well be a French pastry. To put it plainly, the risk that imprudent government action has added to the equation has grown into an 8,000 pound untrained gorilla sitting in your living room.

When it is all said and done, Bernanke will be powerless to stop the forces that have built up over 30, 50, even 100 years -- directly at odds with what should encompass the spirit of his job. It's inevitable. You can't brush economic reality under the rug forever.

Indeed, we appear to have reached a critical turning point; where we go from here is anyone's guess.

The question we should all ponder right now is this: Which will take the greatest hit on the chin? The economy or the dollar.Or both?

What's with all the gloom about the U.S. economy? The problem is that we have two problems. One is that the economy is slouching toward recession or, at best, slow growth. It's the consequence of falling house prices, higher energy prices, flagging consumers and shrinking profits.

The other is that the market for credit, the lifeblood of a modern economy, isn't functioning well. That problem is amplifying the pain caused by the first.

Just a few weeks ago, a lot of folks were arguing that the worst was behind us. Housing was still ailing. But after a big wallop, markets for credit seemed to be moving toward normalcy. The Federal Reserve ended its Oct. 31 meeting declaring that the "upside risks to inflation roughly balance the downside risks to growth." If Fed officials truly believed that then, they no longer do. They'll likely cut interest rates again on Tuesday.

Only the most optimistic observers expect the U.S. economy to rebound quickly from its fourth-quarter slump. The argument now is between those forecasters who expect growth to be so slow in early 2008 that the unemployment rate climbs a little, and those who see a recession in which it climbs more. In ordinary times, this would be unpleasant, but not so frightening. The Fed knows how to treat this condition: cut interest rates.

Sure, it's tough to get the timing right. And administering the remedy is more complicated with the dollar drooping and inflation returning to the Fed's agenda for the first time in years. Still, this is a familiar disease. Although the Fed has not and cannot abolish the business cycle, the U.S. has suffered from recession only 16 months in the past 25 years. (In the quarter-century before that, there were 64 months of recession.)

But these aren't ordinary times.

You Go First: Update on Various Hail Mary Schemes to Put a Bid Under Fictitious Capital

Open call to the Winter Watch community. In an attempt to get discussion properly focused again I have what I consider to be the most important question of the day. First, foreign central banks (FCB) completely passed on new custodial holdings in the latest week. It came in at zero change, marking six straight weeks of inactivity.

In the Fed´s H.4.1 report footnotes you will see the term ¨federal agency¨and $808.3 billion listed. The vast majority of these were purchased during the last three years at the peak of the housing Bubble. The question is, what is this entry exactly? Is the term federal agency accurate or misleading, and to what degree? How good is the collateral behind these holdings.

How many foreclosures and non performing mortgages do central banks hold? Do FCBs hold only mortgages issued by housing agencies, or have they been caught in the bogus AAA rated mortgage backed securities snare? Do they in fact also hold a shitload of severely marked down securities? I suspect this is the case and in spades.

And even if these are all virtually GSE agency securities, how many have been damaged by measures such as allowing second lien or piggyback mortgages to be used against them? Do FCBs hold primary mortgages with delinquent second mortgages? Do they even know if the seconds are delinquent? How involved directly have FCBs been with purchases of agency backed non traditional loans such as HELOCs?

Spare me the "shock" about credit card rates

Usurious credit card fees are back in the news with feigned shock and outrage about interest rate increases that consumers are getting hit with. Credit companies were testifying before the Homeland Security and Governmental Affairs Investigations Subcommittee on their interest rate practices. This has been a big set up and is what was meant to happen.

Back in 2005, Frontline aired "Secret History of the Credit Card. The current usury by credit companies was set up in 1996:

There is no federal limit on the interest rate a credit card company can charge.

If you've ever looked at the return address on your statement, you may notice your credit card issuer is located in a state such as South Dakota or Delaware. That's because these are the states that have either weak or no "usury laws" meaning there is no cap on the interest rate that is charged.

The federal government once had national usury laws that set a cap on the amount of interest that could be charged on a loan. But after the Great Depression, it repealed them and some states put no new usury laws in place. That's why Citibank, the issuer of MasterCard, moved to South Dakota, which has no cap on interest rates.

Credit Card Practices Denounced

With Americans weighed down by some $900 billion in credit card debt -- an average $2,200 per household -- practices of the very profitable industry have been ripe for scrutiny by the Democrat-controlled Congress. They have also grabbed the attention of the Federal Reserve, which plans to require credit-card issuers to give customers at least 45 days' notice before raising interest rates and to provide clearer information on fees.

At a hearing Tuesday, Levin's subcommittee, which has been investigating the industry, planned to look at how credit-card issuers raise consumers' rates, to as high as 30 percent, when their so-called FICO credit scores decline -- even if they've paid credit card bills regularly and promptly. In many cases, consumers have little notice of the increased rate, which are automatically triggered by declines in FICO scores for reasons left unexplained, the subcommittee found.

In some cases, just opening another account, such as a department store credit card, could trigger the downgrade in credit score....

....Industry critics say it's another example of abusive, confusing credit card practices that can push consumers deeper into debt.

Subprime Crisis Not Seen Changing Accounting Rules

As banks reel from massive U.S. subprime losses, some experts argue that creating transparency in the market would be more effective at restoring public confidence than changing accounting rules.

"The regulator's tools for the most part are disclosure," Roel Campos, former U.S. Securities and Exchange Commissioner (SEC), said at the International Federation of Accountants' World Accountancy Forum in New York on Tuesday.

"I don't know that it is appropriate to expect regulation, regulators, and standard setters to essentially prevent the next restructuring or subprime mortgages," he said in response to a question from Financial Accounting Standards Board Chairman Robert Herz.

"Maybe there is a different way of thinking about the risks in the system and how to govern the financial system," Herz told the forum. "I don't know where the balance is, but we're somehow not getting it right."

Various financial services started implementing higher fees and interest rate hikes. Somewhere along the line, the "universal default" policies came into play. These policies allow a creditor to move a customer to a maximum interest rate for late payment on any reported bill - even if the payments to that creditor have never been late. As this practice started kicking in, consumer bankruptcies started rising.

Personnel

Archives

- December 2008 (1)

- October 2008 (1)

- July 2008 (2)

- June 2008 (2)

- May 2008 (6)

- January 2008 (2)

- December 2007 (8)

- November 2007 (9)

- October 2007 (11)

- September 2007 (14)

- August 2007 (14)

- July 2007 (10)

- June 2007 (9)

- May 2007 (11)

- April 2007 (9)

- March 2007 (11)

- February 2007 (11)

- January 2007 (11)

- December 2006 (12)

- November 2006 (16)

- October 2006 (13)

License

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.

Stoneleigh

Here are two that should be included;

Shortages, Inflation and Withering Credit: What's in Store for the First Half of 2008

At SeekingAlpha

http://seekingalpha.com/article/56302-shortages-inflation-and-withering-...

And

THE ECONOMY'S LAST HURRAH

by Richard Benson

http://www.financialsense.com/editorials/benson/2007/1206.html

BOTH are well worth the reads

John

Thanks John,

We have a truckload of stuff still on file, waiting to be included. It'll be sort of a Rolling Round-Up today. Do check back, we'd suggest.

Yeah, here's another goodie:

Senate passes fix for alternative tax

They "fixed" the problem by giving another unfunded tax cut which will be "paid for" with more borrowing.

By the way, Stoneleigh, great job with these financial round-ups. Don't know how you do it, but keep it coming.

best regards,

Oz

Don't know if I should, but I'm posting this anyway. I just read this post on Nouriel Roubini's blog. I am posting it because it is a GREAT boil down of Peak Oil meets Financial realities.

I am seeing more and more Peak Oil people(or finanical people who have learned about Peak Oil) posting on Financial Blogs in the last 3-6 months.

If this is out of line, just delete it Stone.

John

I shortened it to an excerpt and formatted the links in html.

Thanks, I think what he is pointing out is VERY important.

Classical Economists/Financial Analysts, etc Have NO MODELS for what we are starting to experience.

The Down side of Hubbert's Peak is a WHOLE new ball game of economic theory.

I have changed my reading habits to first discern whether the finanical writer knows about Peak Oil, and Depletion.

Or are their "Cycles" and expectations based "Unlimited" supply so that supply/demand theories work.

If the writer is clueless about PO, and is already pessimistic, I multiply/factor in an increased severity to it.

I think I know what you mean. A while back I swapped some emails with Martin Wolf the FT's erudite and respected chief economics commentator.

Essentially, the "discussion" came to an end when it became clear that he had no idea of the importance of energy in economics.

Since then, I have been skipping his articles that are about energy or economic growth.

I still read the good ones, But like I said, I factor in a magnitude more of "Badness" so to speak knowing what I know of PO, Water Shortages, Soil, and Infrastructure decrepidness...

We are at the point in time when OUR graphs of Peak Oil decline meets the Graphs of Business Cycles...

NOTHING will work the same, or as expected.

It is, quoting from my Unwritten Book, The End Of *MORE.

Economics is just the new theology of the new religion. It works within its own artificial world, but, when reality intrudes, its tenets will seem as ridiculous as those of theologians past.

Of course their economic models won't work and eventually they will see that their god has forsaken them. The poor wretches will then have to face the masses and tell them why their faith will not save them and to see to themselves and kin the best they can.

Eventually a new "Enlightenment" will happen, hopefully, it will promote the natural over the artificial and wipe out the last vestiges of the original "Enlightenment", which brought us to the verge of extinction.

People won't make the same mistake twice, this time they'll burn the monasteries too :)

These sub prime leeches are the biggest dumbazzes ever. They keep enabling the Wall Street mafia.

They are celebrating the bailout dancing in the streets and buying 20" spinner wheels for their Escalades, but in reality it is a sucker trap and they would be much better off walking away from their houses.

They haven't figured out that anyone with 3% or more equity doesn't qualify.

The senior tranches in the CDO's lose also as delaying foreclosures just forces the auctions into a even more depressed market.

They are doing anything at all to provide whatever liquidity they can to the banks, it is an act of sheer desperation. No one with an IQ higher then room temperature is going to leave any funds in US banks.

Instead of cutting the cancer out early, they are talking aspirin and shining people on.

musashi: you graciously referenced our musical parody takes on some of these issues a few weeks ago ("THE DOLLAR AND ITS DIVING"; "BEARISH"). New pieces that might be of interest: "DEPRESSING" (about the subprime mess etc.); "MALAY RIDE" (about holiday shopping in the global economy in the subprime mess). Thank you, and happy holidays.

Thanks for the links, I had forgotten about the site.

Good to get a chuckle in between the news, eh?

Happy holidays.

Hi Musashi,

I am feeling particularly in a very 'conspiratorial theory mood' this morning and something you said the other day about the ( mafia bosses?) having nothing on 'these guys' has triggered it.