| Canadian Gas - Decline Sets in. | The Oil Drum: Canada | The Energy and Environment Round-Up: October 21st 2007 |

The Finance Round-Up: October 17th 2007

Posted by Stoneleigh on October 19, 2007 - 8:59pm in The Oil Drum: Canada

A bailout of sorts appears to be underway for the Enron-esque off balance sheet financial conduits known as Structured Investment Vehicles (SIVs), similar to the on-going Canadian attempt to rescue frozen Asset-Backed Commercial Paper (ABCP). However, the US Treasury-supported use of Frankenstein finance to bail out the effects of past Frankenstein finance smacks of desperation rather than inspiring confidence.

Something had to be done to forestall a looming firesale of assets that none of the banks want marked to market, but 90 days may well be too long to wait when a crunch period is fast approaching, and $100 billion may not be enough. With problems emerging for both commercial real estate and consumer spending, as well as ARMs resetting, all on top of the SIV/ABCP deepfreeze, it's hardly surprising that this rescue plan has been described as "rearranging the deck chairs on the Titanic".

Heisenberg Uncertainty Theory Of Money

By observing or attempting to observe money you alter where it is and/or the velocity at which it is traveling depending on whether or not you are watching with one eye or two. One can either determine how much money there is, where it is at, or the velocity and direction at which it is moving but not all of them at the same time.

This is complicated by the fact that watching is an aggregate thing not an individual thing. Where money is and how fast it is traveling is influenced by everyone's attempt to watch it.

Too many people are watching Bernanke's helicopter drop right now which explains why money turns up in mysterious places like the pockets of those working for Goldman Sachs rather than blowing in the breezes or floating around in thin air as logic would dictate.

New! Master-Liquidity Enabler Conduit

S&L may yet be eclipsed. "The cost of the subprime crisis continues to mount on Wall Street. To date, the total stands at nearly $20 billion." (CNNMoney.com) Other estimates go far higher, dwarfing the S&L's $125 billion. "Ultimately, the total cost to ride out the storm would be more than any consortium of banks could afford." (USA Today)

The latest "Super-SIV" emergency financing scheme is an effort to enable the continuation of the credit binge. Some of the world's biggest banks plan to put about $100 billion in a fund that will be used to replace the investors who have stopped buying SIV-affiliated commercial paper.

"Details are still being worked out but the oversight committee of the three banks [Citigroup, J.P. Morgan and Bank of America] will set criteria for what the new fund, to be called the Master-Liquidity Enhancement Conduit, will buy." (Wall Street Journal)

If investors don't want the stuff, banks have to put it on their balance sheets and take the loss unless they can find another buyer, which it appears they intend to create.

Mary Shelley would be proud. Where did I leave my pitchfork?

This effort looks eerily similar to 1929, when the Rockefellers and William C. Durant pooled capital to buy large quantities of stocks to demonstrate their confidence in the markets to the public. The crash continued and the market lost $30 billion that week, ten times the annual budget of the federal government and more than the U.S. spent in World War I.

Total nominal Asset Backed Commercial Paper outstanding peaked on August 8 at $1.17 trillion. I used the word “nominal” intentionally, because the reported totals represent face value. Since that time we became aware that a significant portion of the paper coming due in July and August paid neither principal nor interest. The holders of the remainder were FORCED to roll it over. They had no choice.

That suggests that a significant portion of the remaining paper is worthless, or nearly so. There will be no interest payments, no return of capital. Holders who have bills coming due and were counting on the return of that cash now face a dilemma. Where will they get the cash to meet their obligations? Some may still be able to borrow in the market or, if they are depositary institutions, from central banks directly. Others will need to liquidate assets....

....The crunch in the ABCP market has now reached the point that many holders, including highly leveraged hedge funds, need to get their cash NOW. Otherwise they go poof, and the reverberations are likely to manifest themselves as waves of liquidation coursing through the financial markets.

Much of the dollar value being reported in money market funds and monetary aggregates consists of fictitious capital that has no value. We also know that a fragile daisy chain of obligations exists that, as with any giant Ponzi, must be funded by new players entering the market. Since the bad paper can’t be liquidated at a rate high enough to pay current obligations, once the Ponzi scheme begins to reverse, it becomes difficult to stop. Japan tried through the 1990s and even continues today, with only limited success.

Now the entire world faces the same problem. Unlike in the 1990s when the problem was mostly confined to Japan, bad commercial paper backed by bad collateralized debt obligations backed by bad mortgage debt, and soon to be proven bad credit card debt, has been spread throughout the world financial system by the Wall Street distribution centers.

In the 1990s Japan’s bad debt was concentrated in a few interlocking mega institutions which could be indefinitely propped by the BoJ. Today, with the bad debt so widely disseminated among countless thousands of banks, insurance companies, pension funds, and, most importantly, hedge funds, the potential for a chain reaction meltdown may be outside of the ability of the major central banks to keep from coming to fruition.

Banks And U.S. Treasury Discuss $100 Billion Support Fund

Leading U.S. banks have reportedly been meeting with U.S. Treasury officials about creating an up-to-$100-billion fund to stave off the danger that there could be a fire sale of shaky mortgage-backed securities, collateralized debt obligations and other distressed assets following the recent global credit crunch.

Such a fire sale could force big banks and hedge funds to write off or write down similar assets, setting off a second wave of the credit crunch that could flood into the broader economy.

Banks May Pool Billions to Avert Securities Sell-Off

While there are signs that the broader credit markets have begun to stabilize after the Federal Reserve lowered interest rates last month, a pocket of the commercial paper market remains under siege: structured investment vehicles, known as SIVs. The fear is that problems with these vehicles could infect the broader economy.

SIVs, which issue short-term notes to invest in longer-term securities with higher yields, are often organized by banks but are not actually owned or held by them. They are supposed to be financed through the issuance of commercial paper backed by pools of home loans and credit card debt, but the loss of confidence in the quality of subprime mortgage bonds has also tainted these securities.

Analysts say that investors have all but stopped buying SIV-affiliated commercial paper, and the worry is that the 30 or so SIVs will unload billions of dollars of mortgage-related assets all at once. That would put intense pressure on prices. As Wall Street firms and hedge funds mark value of similar investments they held to their new lower values, they face potentially huge hits to their profits.

Still, the impact on the biggest banks is even more severe. In times of crisis, they are committed — either legally or to maintain their reputations — to stepping in to buy those securities. Banks have already been buying significant amounts of commercial paper in recent weeks, even though they did not have to. But if they are forced to bring those assets onto their balance sheets, they might be less willing to lend to businesses and consumers. That could set off a credit crunch and thrust the economy into a recession.

The proposal being floated calls for the creation of a “Super-SIV,” or a SIV-like fund fully backed by several of the world’s biggest banks to provide emergency financing. The Super-SIV would issue short-term notes to finance the purchase of assets held by the SIVs affiliated with the banks, with the hope of reassuring investors.

SIVs forced into deleveraging as sector sees few signs of recovery

The short-term funding markets in the US and Europe might be starting to show signs of recovery but the sector that comprises one of their biggest groups of customers is still struggling to gain re-entry.

The structured investment vehicles (SIVs) that just three months ago represented a more-than-$400bn industry have been struggling to raise new short-term commercial paper since about mid-July, and consequently have been forced to sell assets - sometimes at firesale prices.

SIVs use short-term debt fund investments in longer dated, higher yielding investments such as bonds backed by subprime mortgages. They have faced a double whammy of a freeze in funding and falls in the value of their holdings since the US subprime mortgage crisis sparked a broader liquidity squeeze.

The market was given a hard illustration of the pain that can be felt this week when it emerged that Axon Financial, a SIV linked with the US hedge fund TPG-Axon, had taken losses of $110m on sales of $3bn of its investments.

In total, the industry sold about $43bn of assets to meet repayments of maturing debt between early July and the end of September, according to data from Moody's, the ratings agency.

Enron, Subprime and the Derivative Disease

So far, many SIV sponsors have refused to realize losses on supposedly arm's length financing relationships with their captive conduits, hoping, against evidence to the contrary, that investor confidence in same will be restored. But as in the case of Enron, LTCM, Amaranth and now CFC, once market confidence is disturbed it is very difficult to regain. The derivative assembly line of originate, structure, sell has broken down.

Not only do we believe that the Treasury's effort to resuscitate the market for SIVs and other structured assets likely will fail, but we think Paulson already knows it will fail. We fully expect that the banks, insurers and broker-dealers involved in the asset-backed CP market obstruction will eventually forgo the fiction of SIV separateness and take these assets back "on balance sheet," creating a potentially crippling mark-to-market event. It is no secret that many conduits were rated according to the sponsor's ability to pay, not the collateral in the SIV, raising the same legal and operational risk issues for the banks as once caused Enron to collapse.

Super-Conduit or Super-Bailout Shell Game?

Can this financial engineering work? If the problem was only one of pure illiquidity and a generalized bank run then that solution may in principle work as you may resolve the double collective action problem. But the reality is different in this case as the assets of the SIVs are not only sound but illiquid assets. Many of these assets are toxic MBS, CDO tranches and other ABS assets of dubious quality; thus, there is a problem of credit or solvency on top of illiquidity.

This is the main reason why – unlike LTCM that held mostly illiquid but truly high quality assets – resolving the collective action problem is not enough to resolve the SIV mess. The proposed solution thus looks like a game of musical chairs that may not work. Indeed, if we assume that many of the assets held by the SIVs are of low quality, the attempt to avoid losses that would be incurred by selling these assets in secondary markets would not be possible.

It is true that impaired assets of poor quality may also suffer of illiquidity and thus their current market price would be even lower than the low fundamental price given their low credit quality. But putting such assets into a super-conduit would not resolve either the liquidity problem or the solvency/credit problem of these assets. Banks will have to accept that they bought lousy assets whose true value is now well below par – even leaving aside any current discount due to illiquidity – and that these losses cannot be fudged or eliminated by creating a super-SIV.

Banks Start Fund to Protect Credit Market

The conduit is expected to start operating in 90 days and will stay in place for a few years until it has disposed of the assets it buys, according to people familiar with the negotiations.

To maintain its credibility with investors from whom it would raising money, the conduit will not buy any bonds that are tied to mortgages made to people with spotty, or subprime, credit histories. Rather, it will buy debt with the highest ratings — AAA and AA — and debt that is backed by other mortgages, credit card receipts and other assets.

Each bank will put up an unspecified amount of its own capital into the fund, and other banks from around the world are expected to join the consortium in the coming weeks. The conduit will raise most of its money by selling commercial paper, which is a form of short-term debt like Treasury bills but is issued by banks, corporations and investment vehicles.

The conduit will pay market prices for the securities it buys. But it remains unclear how officials will determine the price of some bonds that have not been actively traded since August, because the difference between what buyers are willing to pay and what sellers want has widened significantly.

One analyst, Christian Stracke of the research firm CreditSights, said the effort appears to be an attempt to soothe tense investors in the debt market, rather than to provide substantive relief to the worst-hit mortgage securities. He noted that many of the banks participating in the fund had already been working on their own to ease problems at SIVs.

“For me, this is more of a P.R. blitz,” he said. The banks are “saying, it’s not just that we are doing this on an ad hoc, individual basis. Rather, we have a plan and consortium in cooperation with Treasury, which gives it a veneer of respectability.”

While Paulson and company should be embarrassed that their secretive meetings have resulted in such a toothless effort, the Treasury actually took the time yesterday to say that they are "pleased with the response by the private sector to enhance liquidity in the short term credit markets." Using the historical precedent of Long-Term, in 1998 then New York Fed boss, William McDonough, put the Fed's reputation and printing presses on the line when he gathered concerned parties into a room and said 'work this out!' Apparently the supposedly Street-savvy Paulson gathered everyone in a room and said 'try to sell some this toxic garbage to someone else!'

While the structure, investment scope, and overall purpose of the proposed MLEC could change, as it stands it looks like another desperate attempt by Wall Street institutions to share some of their pain with others. As the evidence continues to mount that the consolidation standards put in place following Enron have failed to end off balance sheet shenanigans, market participants await a real bailout from Paulson and/or Bernanke. Question is, will they have to wait 90-days?

Stocks Retreat Amid Bad Debt Worries

The concerns about banking came after Citigroup Inc., the biggest U.S. bank, reported that third-quarter results fell 57 percent. The company said it lost more than $3 billion in mortgage-backed security losses, leveraged debt write-downs and fixed-income trading losses.

The bank -- along with JPMorgan Chase & Co. and Bank of America Corp. -- announced the creation of a fund used to help revive the asset-backed commercial paper market. The fund will buy assets from structured investment vehicles, also known as SIVs, which buy corporate bonds and subprime mortgage debt. The bailout was orchestrated by the Treasury Department to avoid a fire sale in the market.

"It's a reminder that this problem never was entirely put to bed. There may be financial institutions out there than are in more trouble than we thought they were," said Aaron Gurwitz, co-head of portfolio strategy at Lehman Brothers Investment Management, referring to concerns about bad debt.

Paul Kasriel: MLEC - Trying to Turn a Sows Ear into a Silk Purse?

In recent months, investors' appetite for ABCP has all but evaporated due to concern about the credit quality of the assets, especially subprime mortgage-related paper backing the commercial paper (see chart below). With the inability to rollover their ABCP, some SIVs would either have to liquidate their assets or have their assets come onto the balance sheets of their affiliated financial institutions such as Citigroup. The liquidation of assets under current market conditions might entail sharp declines in the prices of these assets. This would put pressure on other institutions holding similar assets to mark down the value of these assets on their balance sheets. If the affiliated financial institution were to put its SIV's assets onto its balance sheet, these assets would then incur a charge against the institution's capital, which could constrain the institution's ability to engage in revenue-producing activities.

The idea of the MLEC is for it to purchase various high-quality assets from SIVs and to finance these purchases via MLEC-issued commercial paper. Although it is not entirely clear to me what guarantees would be provided by the MLEC's syndicate of financial institutions, presumably they would absorb some part of the losses the MLEC might incur. As some analysts have observed, it is not the high-quality assets of the SIVs that have impaired the credit quality of ABCP, but the questionable assets on their books such as subprime mortgage-related securities. To a skeptic, this MLEC might appear akin to re-arranging the deck chairs on the Titanic.

Big Banks Push $100 Billion Plan To Avert Crunch

The ultimate fear: If banks need to write down more assets or are forced to take assets onto their books, that could set off a broader credit crunch and hurt the economy. It could make it tough for homeowners and businesses to get loans. Efforts so far by central banks to alleviate the credit crunch that has been roiling markets since the summer haven't fully calmed investors, leading to the extraordinary move to bring together the banks.

In recent weeks, investors have grown concerned about the size of bank-affiliated funds that have invested huge sums in securities tied to shaky U.S. subprime mortgages and other assets. Citigroup, the world's biggest bank by market value, has drawn special scrutiny because it is the largest player in this market.

Citigroup has nearly $100 billion in seven affiliated structured investment vehicles, or SIVs. Globally, SIVs had $400 billion in assets as of Aug. 28, according to Moody's.

Such vehicles are formally independent of the banks that create them. They issue their own short-term debt, usually at relatively low interest rates reflecting their high credit rating. The vehicles use the money to buy higher-yielding longer-term assets such as securities tied to mortgages or receivables from midsize businesses seeking to raise cash.

Many SIVs had trouble rolling over their short-term debt in August because of concerns about the quality of their assets. That contributed to the broader seizing up of credit markets.

Rescue Readied By Banks Is Bet To Spur Market

The high-stakes plan to rescue banks from losses on mortgage securities amounts to a big bet that a consortium of financial giants -- at the prodding of the U.S. government -- can persuade investors to pour more money into the troubled credit market....

....According to people familiar with the matter, the Treasury hopes the plan, which could be announced as early as this morning, will jump-start demand for commercial paper, which froze up this summer amid the credit crunch that roiled global financial markets.

Companies depend on commercial paper to finance day-to-day expenses like payroll and rent. Some financial commercial paper -- known as asset-backed paper -- has been able to find buyers in recent weeks. But investors have remained skeptical of other types, including paper issued by certain bank-affiliated investment funds.

Super SIVs - A Fraudulent Attempt at Concealment

Don't Ask - Don't Sell

- Don't Ask what the asset is worth.

- Don't Sell or you will find out and not like the result.

Of course you can sell to the Master-Liquidity Enhancement Conduit at market prices, but market prices are not set by selling assets to yourself or by agreements to buy assets a back at a guaranteed price as Bear Stearns is doing.

Let's go back to the beginning. This problem was caused by loose monetary policy in conjunction with rules that allowed garbage to be kept off bank balance sheets. The proposed solution is another scheme to keep garbage off bank balance sheets. Logically the solution and the problem cannot be the same.

All indications are the Super-SIV bailout is nothing but a delay tactic that simply cannot work. Furthermore, there is another crisis waiting in the wings: commercial real estate. There is also a looming consumer led recession that is coming no matter what the Fed does. For those reasons, attempts to delay will only exacerbate the problem.

I do not know what the market will do on Monday. Perhaps this bailout will sent the market to new highs. Bulls certainly have been stomping as if the economic problems we face are temporary. Unfortunately the problems we face are not temporary. Structural economic problems run long and deep. Whatever final shape this bailout plan takes, it is doomed to fail over the long haul. A collapse in consumer spending and commercial real estate will seal the fate. Both are going to happen.

US Scheme to Rescue Banks from Bad Subprime Mortgage Debt

Susan Pulliam summed it up like this in the Oct 12 edition of The Wall Street Journal:

“Since the invention of the ticker tape 140 years ago, America has been able to boast of having the world's most transparent financial markets. The tape and its electronic descendants ensured that crystal-clear prices for stocks and many other securities were readily available to everyone, encouraging millions to entrust their money to the markets. These days, after a decade of frantic growth in mortgage-backed securities and other complex investments traded off exchanges, that clarity is gone. Large parts of American financial markets have become a hall of mirrors.”

“Hall of mirrors” is an understatement. The system is thoroughly opaque and crooked as a ram's horn. The market's new architecture, “structured finance”, is a dismal rip-off from start to finish. Consider the mentality of the hucksters who dreamed up “securitizing” subprime mortgages and selling them off as precious jewels in the secondary market. This was a blatant con-job. How can the liabilities of “borrowers with bad credit” be traded to foreign investors and pension funds like they were valuable assets? And where were the regulators while this scam was going on?

Isn't this sufficient evidence that the system is totally out of whack?

Wall Street avoids transparency like the plague. That is to be expected. But what about the government? It's the government's job to protect the investor and maintain the integrity of the system. Is that what Treasury Dept is doing or are they “LURING investors to buy debt issued by the rescue fund as part of the plan”? (quote from the Wall Street Journal)

“Luring”? Is that how Paulson sees it; like luring turkeys to the chopping block with a trail of bread crumbs?

The idea of protecting the little guy has never occurred to anyone in the Bush administration. Their job is to shift wealth from one class to the other via equity bubbles and government bailouts----anything that advances the corporate agenda.

Presently, the banks are sitting on $200 billion in non-performing mortgage-backed securities (MBSs) and collateralized debt obligations. (CDOs) They are also hold another $300 billion in collateralized loan obligations (CLOs) from mergers and acquisitions which stalled after the Bear Stearns meltdown. If the present bailout doesn't materialize, we're likely to see bank closures and a plummeting stock market.

Shouldn't the regulators have considered the probability of a crash before they allowed trillions of dollars of radioactive-bonds to flood the market when no one had any idea of their real value? Wouldn't that have been the prudent thing to do?

Now we know what they are worth. They're worth nothing. That's why the banks are running scared and refusing to put them up for auction. They'd rather sleaze them into a lofty-sounding superfund that masks their true value.

Bank of Montreal is considering whether to join forces with three U.S. banks who unveiled a last-minute rescue plan yesterday for the moribund commercial paper market....

....BMO is one of the biggest players in an arcane corner of the commercial paper market known as structured investment products, or SIVs. Banks set up these SIVs at arms-length, so they don't impact the corporate balance sheet, and then use them to issue paper to investors. The problem is that some of the assets held in these SIVs include mortgage-backed securities, which investors have come to regard like the plague since the recent meltdown in subprime lending....

...."This is a ridiculous waste of time. This asset class is dead - it has taken a bullet in the head, and you can't wind back the clock," said Christopher Whalen, managing director of Institutional Risk Analytics. "The notion you can just pretty this pig up and put lipstick on her for the fourth-quarter ... is hideous."

Banks 'Asleep At Switch'

Group blaming industry and watchdogs for ABCP crisis singles out Canada

The top international banking think-tank has slammed banks and regulators in Canada and elsewhere for the way they allowed the market for asset-backed securities to dry up this year.

"The industry has to recognize that we were at fault big time," said Philip Suttle, a director at the Institute for International Finance, a lobby group for more than 360 of the world's major banks, including the five biggest in Canada.

"A lot of us were asleep at the switch, both regulators and market participants," said Mr. Suttle, in an interview after the IIF submitted a letter expressing its concerns about the market to the International Monetary and Finance Committee -- a committee of the IMF that meets next week in Washington.

Mr. Suttle said the IIF's letter was concerned with the asset-backed securities market not just in Canada, but also in the United States, Australia and the United Kingdom. But the IIF noted that the Canadian market, in particular, was "different because the back-up facilities that the securities had in the Canadian market were less complete than [elsewhere.]"

The market for asset-backed securities -- typically 30-to-90-day notes backed by credit-card balances, car loans and mortgages, but also more complex assets -- ground to a standstill in the summer when some investors were spooked because some of the securities were linked to the troubled U.S. sub-prime-mortgage market.

Some observers have dubbed the securities market meltdown "a made-in-Canada crisis."

Here the worst of the crisis concerns a portion of the market known as non-bank sponsored asset-backed commercial paper (ABCP) -- worth about $40-billion -- which is still frozen, leaving some investors desperately trying to figure out how to get back their investments.

Montreal Accord deadline extended

Backers of the Montreal Accord have reached an agreement to extend until mid-December the deadline to restructure $40-billion of troubled asset backed commercial paper (ABCP).

The accord was due to expire Monday, but people familiar with the negotiations said dozens of banks and investors backing the pact expect to announce later Monday that they have agreed to a two-month extension. Sources said that banks and investors agreed to the extension this weekend after negotiators successfully convinced the half dozen sponsors and trustees of Canadian asset backed commercial paper to join the accord.

The support of the sponsors, which includes such companies as Toronto-based Coventree Inc., was a big breakthrough, sources said, because it gives participating banks short-term protection that sponsors will not trigger loans or liquidity agreements backing ABCP.

Frozen debt funds to start flowing

The investor committee seeking a solution, under lawyer Purdy Crawford, wants to exchange the unpopular short-term ABCP notes for longer-term bonds that will trade again freely. Investors who can hold on to longer bonds, including the Caisse de dépôt et placement du Québec, plan to do so, while companies that need more immediate access to cash can sell the bonds in the market.

As a first step, the committee expects to be able to announce the successful restructuring of Skeena Capital Trust, which has about $2.1-billion of asset-backed commercial paper out standing.

Investors will probably get a share of some of the roughly $300-million in cash that Skeena has, and the rest in new notes, with the exchange happening as soon as early November, sources said. They're also expected to get the interest that's built up in the two months since the paper was frozen.

"Skeena is the easiest one to do," said one person familiar with the situation who asked not to be identified. "They are getting close to being able to announce that one. It should create confidence in the process."

Skeena, set up 15 months ago by Toronto-based Dundee Securities, was designed like all of the trusts to buy income-generating assets such as mortgages, accounts receivable and derivatives. Skeena raised the money to make those purchases by selling lower-cost short-term debt to investors like money market funds and people looking for a place to park cash. The operator of the trust got to keep the difference between the high rates coming in and the lower rates going out.

U.S. fix similar to Montreal Proposal

News of the U.S. deal came the same day as an investors' committee overseeing the Montreal Proposal was expected to announce that it had been given more time to hammer out its rescue plan. At press time, Purdy Crawford, the chairman of the committee, declined to comment directly on the matter. "We're in good shape," he said in a telephone interview. Analysts said they expected Mr. Crawford will be given what he has asked for, but they said the fact that the answer has taken so long -- the 60-day standstill agreed to by signatories of the Montreal proposal when it was unveiled back in August officially ended last night -- is an indication of how difficult the job is proving.

The Montreal Proposal was unveiled by a group of major financial institutions, spearheaded by the Caisse de depot et placement du Quebec, believed to be the biggest holder of illiquid commercial paper, with as much as $20-billion of exposure. The Caisse and several banks in the proposal also played important roles through their links to ABCP sponsors. Under their rescue plan, the paper would be converted into longer-term debt with maturities linked to the underlying assets. Analysts such as Royal Bank's Andre-Philippe Hardy have criticized it, noting that investors end up shouldering the risk while leaving issuers and other players relatively unhurt.

The Canadian market for ABCP froze on Aug. 13 after investors stopped buying debt securities with exposure to U.S. subprime mortgages. Since then, investors have been unable to sell their paper. Holders include companies and funds from across the business spectrum.

There were at least four warning signs hovering over the the asset-backed market. They were complex products, the U.S. subprime meltdown had been telegraphed for years, there was lack of transparency, and in Canada we had the missing ratings agencies. For the sake of a few basis points, institutions and corporations -- including the Caisse de depot et placement du Quebec -- poured billions into what turned out to be problem vehicles.

The non-bank paper market was a private market in which buyers and sellers were sophisticated and knowledgeable. The failure here is not a regulatory failure, but a failure of self-discipline on the part of people who should know better. The public complaints of high-profile participants in the financial markets, along with those of corporate officers who should know better, only make them look foolish. If the most sophisticated of market players refuse to apply the the most basic buyer-beware principles, they deserve what they get.

Further Developments on the SIV Rescue Front

According to people familiar with the plan, though, the price of admission for SIVs will be high. SIVs will only be allowed to sell assets rated AA or better and likely will be unable to sell collateralized debt obligations -- pools of debt repackaged into slices with different levels of risk and return -- backed by subprime assets. In addition, the SIVs will have to pay a fee to the super conduit and accept a discount in the price of the securities they are selling. In return for that discount, the SIVs will receive notes in the "junior" layer in the conduit -- which will take the first hit if losses are incurred.

The restructuring of SIVs also raises the specter that certain SIV note holders may find themselves stuck with unexpected losses.

If you want a rescue program, you don't lard it up with fees beyond what is necessary for costs and risk assumption. In this case, that would mean market fees for any credit enhancement provided by third parties, plus a mechanism for recovery of costs (and we mean real costs) of establishing and running the entity. That means no debt placement fees, since the old SIV owners were capable of doing that for themselves.

If the spin is that this vehicle is being established to prevent a possible crisis, then it behooves the organizers to do so on a cost recovery basis. Anything else raises questions about the real motives (including are the fees yet another way to shore up Citigroup?).

Oh, but I forgot. Public spiritedness went out of fashion in the Paul Volcker era.

Paulson and Bernanke: Subprime is (not) contained

This is the scariest part. According to the New York Times, at a speech in New York last night Bernanke said, "I'd like to know what those damn things are worth. Until investors are confident in their evaluations, they are not going to be willing to fund these vehicles."....

....That's where Bernanke's exclamation comes into play. Nobody knows what those subprime mortgage backed securities (MBSs) are really worth. As I've posted before, they were sold on the basis of AAA credit ratings but now that the default rates on the mortgages are rising, it seems that none of the investors who bought the securities can estimate their future cash flows. And without that ability to value them -- one of the most fundamental concepts of finance -- the securities are essentially worthless.

Citizens For Financial Responsibility

There is rampant, outright fraud in our financial system. Through a number of schemes various institutions are sacrificing the markets’ integrity and financial strength while undermining the credibility of The United States as the world’s leading economy....

....Congress must act to ban all off-balance-sheet “conduits”, SIVs and similar schemes, and require that any and all liabilities be properly and completely reported both to regulators and shareholders. These vehicles create an intentionally-false view of firms’ financial condition. In effect, these vehicles serve to fraudulently manipulate a bank’s balance sheet by hiding debt. These are the same accounting tricks that were instrumental in Enron’s bankruptcy. Now, on the front page of the Wall Street Journal (October 13th) we learn that Secretary Paulson is actively involved in attempting to expand this deception!

At its most simple, the superconduit is a means by which a large collection of banks can keep “reasonable” pricing on some of their affiliated securities. And it is this pricing that is the key to the whole operation.

It’s obvious they won’t be priced at market rates because there’s not much of a market to begin with (and why the superconduit exists in the first place).

But where exactly do they get priced? To whose benefit? And by which standard?

Even without specifics, it’s clear that Citigroup has the most to gain from this operation. And it’s clearly bad if the balance sheet of the country’s largest bank were frozen for months on end as it poured money into contractual unwindings of SIV positions.

Citigroup Posts 57 Percent Drop in 3Q

Citigroup Inc. said Monday its third-quarter profit dropped 57 percent after the biggest U.S. bank took a hit of more than $3 billion in mortgage-backed security losses, leveraged debt write-downs, and fixed-income trading losses.

Chuck Prince can't seem to defuse the bomb of junk mortgages that's taking down Citigroup and bringing a piece of Wall Street with it. Despite efforts by the Citi chief to help set up a $100 billion pool for restoring the banking industry credit wipeout in the mortgage meltdown, Prince is making little headway in fixing his own bank's deeper woes.

Prince yesterday defended a steep 57 percent drop in third-quarter profits while sounding new alarms of more troubles ahead.

Investors bailed by the droves, causing Citigroup to drag down stocks across the board, with the Dow Jones industrial average losing 108.28 to close at 13,984.80.Shares of Citigroup tumbled 3.4 percent to $46.24, off $1.63 in busy trading at more than triple the usual daily volume. Citigroup said it lost $1.56 billion in mortgage-backed securities, more than it estimated two weeks ago. It blamed a new flood of homeowner defaults on mortgages in September. Citigroup also set aside more cash - $2.24 billion - for future losses on consumer loans.

Citigroup's trading chief shown the door

Citigroup, the biggest US bank, said its trading chief would leave after almost $US6 billion ($6.7 billion) of losses and bad-debt costs, and named the former Morgan Stanley executive Vikram Pandit to oversee trading, investment banking and alternative investments.

Thomas Maheras and a top fixed-income executive, Randy Barker, are leaving the New York-based company, its chief executive, Charles Prince, said.

Mr Pandit joined the bank as head of alternative investments earlier this year when it bought his hedge fund for $US800 million.

Mr Maheras and Mr Barker are the first casualties at Citigroup following its disclosure last week that profits fell 60 per cent in the third quarter because of losses tied to the collapse of the subprime mortgage market. Merrill Lynch, Bear Stearns and UBS have already announced high-level firings after being forced to book losses as a result of three months of credit turmoil.

Countrywide Mortgage Tricks Continue

The subprime mortgage malaise is quite multi-faceted. The borrowers are at fault for overextending themselves. The lenders are at fault for making loans that are a stretch. Realtors exacerbate the problem by artificially boosting prices. And the builders will keep building as long as they have access to construction loans.

Just when it seems that the mortgage madness is trying to work itself out, there was a surprise in the piles of mail this weekend: a 40-year mortgage offering from Countrywide Financial Corp. (NYSE:CFC). It seems that the lenders are still willing to play financial games to keep loaning money. Unfortunately this isn't really new at all. But it shows that at least this lender is willing to keep the games alive in overextending credit.

Say what you like about Mozilo, but you have to admire the art and the symmetry of that October bailout. He has this stuff down pat. Click here for a Historical Table of Mozilo's Bailout. Please remember that he has to bail with both hands because stock options are pouring in nearly as fast as he can bail.

For more on Countrywide Financial, please consider Countrywide Reaps What It Sowed, Countrywide Mortgage Restructure Free-For-All and Mad Dash For Cash.

Inquiring minds might also be interested that Countrywide was Sued by Workers Over Retirement Losses. However, when you are bailing as fast as Mozilo is (to the total tune of over $1 bln dollars over the years), why should he care?

German bank hit by subprime crisis slashes results, directors leave

German bank IKB said Tuesday it has drawn the "personal consequences" of its excessive exposure to the US market for high-risk home loans, with the departure of two directors and a retroactive slashing of its 2006/2007 results.

Markus Guthoff, a board member in charge of real-estate management, and Frank Braunsfeld, head of risk management, will leave the bank "effective immediately," a statement said.

IKB, which lends to small and medium sized businesses, was saved from bankruptcy in August when KfW bank, the government's financial arm, gave it a line of credit worth 8.1 billion euros and other German banks agreed to add another 3.5 billion if needed.

Questions arise about Goldman's blowout quarter

Goldman's stock has gained 13% since its earnings came out, as investors have bought into the notion that the bank is a cut above its peers and is able to weather, and even profit from, tough market conditions.

But that view could get revised, now that it can be seen in the numbers that a large proportion of its third quarter profits were 'unrealized' - i.e. paper gains, and not hard cash payments from fully closed out trades - and came from financial instruments that Goldman values largely according to its own estimates.

"The opaqueness of Goldman's balance sheet makes us immediately question how they made money in the quarter," says Charles Peabody, analyst with Portales Partners.

Experts Fear Repeat Of 1929 Economic Crash

"I think there are three big parallels between what happened in the 20's and what has been happening in Wall Street lately," Robert Kuttner told Moyers.

Kuttner is a veteran economic journalist and a former legislative assistant in congress.

"One is insiders with conflicts of interest that are not fully disclosed to the public generally, secondly - there's much too much borrowed money....particularly in the financially engineered parts of the economy....and third is the lack of transparency - regulators and the public don't get any kind of disclosure," added the former BusinessWeek writer.

Kuttner blamed an economy based on "asset bubbles" for the rising tension in the markets and said that, similarly to the 1920's, "engineered euphoria" and companies cooking the books had combined to endanger the safety of the economy.

Kuttner called for more transparency and slammed the Fed for recycling a vicious circle of cheapening the dollar to bail out Wall Street, inviting another round of speculative excess.

"The risk is that every time we repeat this cycle, we get bigger and riskier bubbles.

source:Federal Reserve Bank of St Louis

To more specifically quantify this, the accompanying table reveals the degree of money creation at an annualized rate. As of August 08th, MZM had a growth rate of 24.3%. Note that this was before the Fed's cut in the discount window rate, and prior to the global injection of liquidity by Central Bankers.Despite the increase in dollars, and the decrease in dollar value, the government maintains the fiction that we have a strong dollar policy.

Confidence between borrowers and lenders remains low while continuing new highs in Euro interbank rates indicates that liquidity has not returned. Longer term, the task of cutting back on risk, reducing debt levels and repairing balance sheets is only in the early stages. In addition, although many analysts believe that financial companies are writing off the kitchen sink in the current quarter, we’re not so sure this is the last of it. We remember too well that after the collapse of the dot-com bubble, technology companies took sequential writedowns despite assuring everyone that they were finished. Furthermore the housing industry will probably be reporting atrocious numbers over the next few months, and that could uncover even more financial companies with serious problems. Also remember that the people who are saying the crisis is over are mostly the same ones who never saw it coming in the first place.

Banks Earned $19 Billion From Overdraft Fees This Year

Kiplinger says that banks have already hauled in $19 billion this year in overdraft fees, and are quickly moving to amend policies that are attracting threats of regulation from the government.

Overdraft fees have morphed into a big money-maker for lenders, exceeding $19 billion this year -- up 85% from 2004. Banks charge as much as $35 for a check, ATM withdrawal or debit purchase when funds to cover them are lacking, even if it's a $2 cup of coffee that puts a customer into overdraft territory. The sharp increase in total fees is largely due to two factors: The increasing use of debit cards and the fact that many banks automatically enroll customers in overdraft programs without them knowing about it.

Banks say that they will start including more disclosure and "a requirement that consumers "opt-in," providing written consent that they want overdraft coverage and agree to the fees."

IMF issues a warning, but are the US and China listening?

Country A is borrowing a net $2 billion a day from the rest of the world — which seems odd to many, since it is not in obvious need. Country B is lending a net $1 billion a day to the rest of the world — which seems odd to many, since it has obvious needs around every corner.

For years, the International Monetary Fund, financial institutions and investors have been worrying about the sustainability (let alone the wisdom) of these flows. What will happen to the world if they stop? What will happen if they don't stop?

The IMF has been highlighting the risks for years. Its managing director, Rodrigo de Rato, has convened a joint study of current account imbalances to try to get the US, China, Japan, the Europeans and the oil exporters to act to reduce their imbalances: the US by reining in its budget deficit, China by making its exchange rate more flexible, Japan and Europe by increasing the pace of reform. But his success has been limited.

Now the IMF has broadened its attack with a new analysis which, in effect, warns China that its regime to hold its exchange rate below market value is likely to fail, and warns the US that unless it gets its fiscal house in order, it risks an even harder landing when the capital flows stop.

Homebuilders face soaring cancellation rates

Ever since the real estate market softened more than a year ago, builders around the country have been stuck with too many houses and too much land in part because jittery buyers have canceled contracts frantically. More recent problems in the mortgage industry added to builders' worries by making it difficult for buyers to qualify for financing and by fueling a rise in foreclosures. That has contributed to a glut of homes for sale.

In the Washington region, the cancellation rate for newly built homes shot up to 48 percent in July and August from 18 percent at the comparable time last year, according to the most recent data from Hanley Wood Market Intelligence, a real estate research firm. The most dramatic rise was among condominiums, where the cancellation rate jumped to nearly 124 percent from 13.5 percent a year earlier, which means there were more cancellations of previous sales than there were new sales.

Long Island foreclosures rise, and no one wants the houses

"The investors are not even buying the foreclosures" at auction, said Mineola real estate attorney Michele Messina, who represents lenders on foreclosed homes. "They're watching and waiting. If they're purchasing something at auction, two or three months down the road, those prices are dropping again."

In the last six weeks, Messina said, she has had two cases of prospective buyers walking away from down payments -- it's the first time in 22 years that anyone has done that in her experience, even when the funds required by lenders range from $5,000 to $10,000.

"They can get another home or another condo or town house for $20,000 or $30,000 less than what they entered into two months ago," she said. "Maybe the next property . . . was even better equipped, updated, newer kitchen, newer this, newer that, for $30,000 under the value that she already was in contract for. She's walking away from 10, but she made 20."

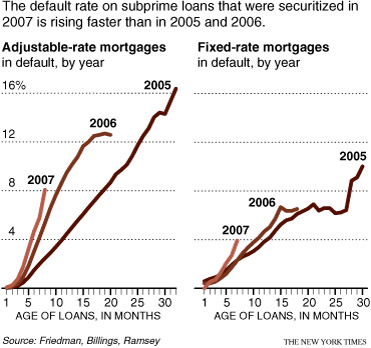

As Defaults Rise, Washington Worries

Borrowers who took out loans in the first six months of 2007 are falling behind on payments faster than homeowners who took out loans last year, according to a report by Friedman, Billings, Ramsey, an investment bank based in Arlington, Va. The data suggested that more Americans could lose their homes and that the housing market’s troubles might persist longer than many analysts have been predicting.The report’s author, Michael D. Youngblood, a portfolio manager and analyst at Friedman, Billings, Ramsey, said that most mortgage companies and banks had not tightened lending standards for borrowers with weak, or subprime, credit until July or August, even though early this year regulators, analysts and mortgage investors knew that the easy lending policies of 2005 and 2006 were producing high default rates.

“There are $10.6 trillion of mortgage loans outstanding in the U.S., and even if the brakes had been slammed, it was going to take a long time to slow this locomotive down,” said Mr. Youngblood, who has researched home lending for more than 20 years. “And I don’t see that the brakes were slammed on or that the engineer had a new track to follow. That track only now seems to be appearing.”

If your home price tanked, would you spend?

Consider that the trigger for all this - the unwinding of a decade-long housing boom - still has a way to go. Housing prices are only now beginning to retreat. The inventory of unsold homes, both new and existing, is still growing. And the tighter credit conditions will continue to make life more difficult for existing and prospective homeowners well into next year.

That suggests that the impact on house prices, and by association household wealth, isn't yet being fully felt. Likewise, housing starts and sales of existing homes are likely to continue to fall.

The Subprime Mentality: A Metaphor For the Whole U.S. Financial Market

First of all, the fallout from subprime lending will be bad enough as it stands. But the real problem is that “subprime” is a metaphor for the whole U.S. financial culture....

....Because subprime loans, by definition, are made to borrowers who are unqualified, lenders demand higher interest rates, which supposedly compensate for the risk. Except that they don’t, as best explained by George Soros in his theory of reflexivity. That’s because if a borrower who is already on financially shaky ground is charged an above market rate, the excess payment that such a borrower has to make means that s/he becomes an even greater risk than before. In short, the act of subprime lending itself creates the very problem it is supposed to solve. So the random people who could pay were in effect subsidizing the ones that couldn’t, because subprime lending was about finding someone stupid enough to borrow (on such terms), and honest and solvent enough to repay.

Grim Forecast for State Budgets

If the economy is booming, then why are so many states struggling with budget issues? Stateline.org takes a look at this issue in State budgets tenuous heading into '08

States awash in surpluses for the past two years are now treading water, with several desperately looking for lifelines to help them get out of budget trouble.A slumping housing market and skimpier sales tax collections are busting budgets from California to Florida at a time when national job growth is sluggish and consumer confidence is at a nearly two-year low.

“The forecast is looking pretty grim,” Sujit M. CanagaRetna, a state tax expert for the Council of State Governments, said. “The implications for states are serious.”

With an eye on Ottawa, Quebec tells the IMF to butt out

The notion of a single national securities regulator for Canada is turning into a politically charged issue with an international twist.

Quebec's Finance Minister accused the federal government yesterday of pressuring the International Monetary Fund to back Ottawa's campaign for a single, countrywide regulator.

Alluding to the coming release of an IMF study that recommends the creation of a single watchdog in Canada, Monique Jérôme-Forget said the only way to explain such "intervention" in the country's internal affairs is that Ottawa put pressure on the world body.

The "close ties between the [federal] finance ministry and the International Monetary Fund are certainly one of the reasons," she told a financial markets luncheon audience.

Global credit crunch may bite into Russia's loose lenders

Russia's oil-fuelled economic and market boom could face a hurdle not all that different from the one facing its old Cold War foe, the United States: A snap-back in its overstretched credit market.

Analysts said the global credit crunch, which has its roots in the U.S. mortgage sector, casts a cloud over an otherwise bullish investment picture in Russia, chiefly because of aggressive lending practices by the Russian banking community.

Their lending has injected billions into the Russian financial markets and helped fuel both investment and domestic consumption, but it has increasingly been financed by borrowings from foreign banks - leaving the entire Russian economy exposed if those foreign lines of credit dry up.

"Deposit growth hasn't kept up with the aspirations of their banks to lend," said Paul Biszko, senior emerging markets analyst at RBC Dominion Securities in Toronto. He noted that Russian banks' foreign debt has more than doubled since the start of 2006 to about $110-billion.

Personnel

Archives

- December 2008 (1)

- October 2008 (1)

- July 2008 (2)

- June 2008 (2)

- May 2008 (6)

- January 2008 (2)

- December 2007 (8)

- November 2007 (9)

- October 2007 (11)

- September 2007 (14)

- August 2007 (14)

- July 2007 (10)

- June 2007 (9)

- May 2007 (11)

- April 2007 (9)

- March 2007 (11)

- February 2007 (11)

- January 2007 (11)

- December 2006 (12)

- November 2006 (16)

- October 2006 (13)

License

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.

Note the emphasized statement. September was the end of the current quarter. During the next quarter, ARM resets go up again. Then during the quarter after that ARM resets go up even further. It is not until April-June 2008 that ARM resets drop and even then they are still well above the current ARM reset rate right now which is what is triggering this mess in the first place. This credit crunch is only just beginning right now. And remember that Citigroup is just the first of many and also that Citigroup just underestimated their losses which they had to revise upwards. So when you look at that $2.24 billion future loss estimate, remember that so far Citigroup and every one of their peers has been consistently low on estimating future losses.

"The greatest shortcoming of the human race is our inability to understand the exponential function." -- Dr. Albert Bartlett

Into the Grey Zone

And where do you hide financially? FDIC insured. Gold? Ammo ;)

Buy an extra bottle of dishwashing soap, shampoo, and laundry detergent, a shopping cart of toilet paper and dish towels, an extra dozen cans of sliced peaches, chili, asparagus, beans, chicken soup, or whatever you usually buy. Your rate of return on canned goods will be above your rate of return on treasury notes.

No joke, stick a few thousand bucks worth of stuff in the closet. Lightbulbs, towels, whatever you bought last year that didn't need to be refrigerated.

No worries mate.

According to Little Ben Sunshine (Helicopter's Bean-Count Cousin):

Rest of Little Ben's NYTimes op ed piece, "The Gloomsayers Should Look Up" can be found here.

Silly puppy, buying food from the Mexican phone company.

Yeah, and there is also the self-reinforcing foreclosure cycle in the US whereby current foreclosures and short sales cause neighborhood home appraisals to drop, thus putting additional borrowers in an "upside down" situation where they owe more on the house than it is worth. The result is "jingle mail" where the keys are mailed back to the bank, who then forecloses.

Sometime in 2008, one can expect whole condominum projects to foreclose in Miami.

http://www.youtube.com/watch?v=QVFBojFJTZM

Here in AZ a few days ago on the news they had a whole development a bit outside of town where new houses started at 285K, They were auctioning them off with a reserve of 89K and only selling one in 10 if that.

The problem started when they loaned to those not capable of producing significant wealth through their work.

I followed a link here a few weeks back regarding the Florida condo market. The area being described had a historic appetite for about 1,000 units a year changing hands. There were 9,000 units, mostly unoccupied spec housing, currently on the market.

This has even happened here in the middle of nowhere. We have a little tourist town complex here made of Okoboji, West, Okoboji, Arnold's Park, Spirit Lake, Wahpeton, Egralharve, and Milford - about 6,000 full time residents set in the midst of 21.7 square miles of glacial lakes. Its cool, but its not all that. The far northeast corner in Spirit Lake where the city ends and the farmland begins has a six story condo tower overlooking a bit of East Lake Okoboji and some corn fields. There is a big sign on the side "Discount for first eight units sold". Judging from the parking lot there is someone there in the sales office and its otherwise unoccupied.

In addition the massive capital flight from anything connected to the US is beginning to show up in the data.

This is from August

http://www.telegraph.co.uk/money/main.jhtml?xml=/money/2007/10/16/bcnchi...

http://www.ft.com/cms/s/0/1ed4bb86-7bf8-11dc-be7e-0000779fd2ac.html?ncli...

How much room is there to further lower rates?

Considering that the last rate cut increased effective rates for the deadbeats, why not reverse the cut?

Why credit card debt is rising so fast, from the UK but it's the same deal

http://today.reuters.co.uk/misc/PrinterFriendlyPopup.aspx?type=personalF...

Maybe they should listen to some country western music instead of rap, "Got to know when to hold them, know when to fold them, know when to walk away, know when to run, ........"

At least in continental Europe the guilty parties at the banks, even though most likely they are dupes rather then instigators, get shown the door "effective immediately", here they get a bigger bonus instead of a ticket to the gray bar motel.

"know when to run..." is right Musashi, high tech's collapsing in the US and I'm only one of many casualties.

Now, the problem is, not only do I have more debt than I can expect to pay off in a lifetime, but if I get an aboveground job, all I earn will be taken away from me. (Think wage garnishment is limited? Taking all but say $150 or less a month of a worker's pay is common, almost routine.) So, I am living VERY cheap, will file my BK in a few months, between the disincentive to work and the lack of work around here, I'm just not doing a lot of economic activity.

Thus, while this huge ball of debt I owe is probably still out there being regarded as money, in a few more months it will be very evident that it's .... not there.

This is why the US isn't heading into another Great Depression but the Greatest Depression.

http://www.leap2020.eu/GEAB-N-18-Contents_a1000.html

I would like to remark positively on Nouriel Roubini’s 15th October post on Super-Conduit or Super-Bailout Shell Game?

http://www.rgemonitor.com/blog/roubini/

He is a uni prof so he makes his stuff understandable for the average guy.

“Without a video the people perish”-Is. 13:24

We are entering the Money / Energy transition (a term coined by Tom Robertson at listserve energyresources). This is when people will realize they can’t fuel their cars with dollar bills -- that money is meaningless and all that really matters is energy. Hubbert proposed an energy currency half a century ago so that people would understand how critical a role it plays in our survival, but it isn’t practical to carry tanks of gas around or bits of uranium in your pocket.

So we spent our energy foolishly, plundering and poisoning the planet for a blip-in-time of pleasure, and now the “Limits to Growth” boas of peak oil, climate change, and natural resource shortages are tightening around us.

I've written a short guide to Financial Monsters at http://www.culturechange.org/cms/index.php?option=com_content&task=view&...

about derivatives, leveraged debt, private equity and hedge fund shenanigans, the distribution of wealth, federal debt and obligations, public debt, Medicare/SSN, underfunded and underinsured pension funds, energy costs, job losses to offshoring, real estate, etc; dollar value dropping, hidden inflation in food, energy, and the M3 value; corporate psychopathy (i.e. "The Corporation: The Pathological Pursuit of Profit and Power"), massive illegal trade, Fannie Mae and Freddie Mac fraud, the Glass-Steagall Act no longer in effect, subprime, the real estate bubble, hurricane, fire and other insurance rates rising so high people aren't insured enough or at all in high risk areas, etc.

Above all we should be concerned about Taleb's "Black Swans", such as wars over the remaining energy resources, energy shocks, terrorists blowing up supertankers in the straits of Hormuz, a large earthquake in Tokyo or San Francisco, hurricanes in the Gulf, any sort of major disruption in global trade since we’re so dependent on “just-in-time” delivery, a revolution in an oil state (i.e. Saudia Arabia, Nigeria), the collapse of Mexico, a major nuclear disaster, etc.

Wall Street fears one of the above will lead to "The Great Unwind".

I think the monsters are already loose,and the panic we see in the banking/financial world is the first signs that its over...get the ready for the greater depression...What we may see in the "real"world in the next few months/years is the "firesale"Kunsler has been talking about...

Calories are fuel for humans and animals, BTUs are fuel for machines. Nothing else in our financial systems matters except as to how it relates to those two things. We used to have silver certificates and maybe next we'll see the treasury issuing a West Texas Intermediate certificate ... or maybe an SPR certificate.

The Mexican collapse black swan is already flapping its wings - Cantarell production collapsing which kills the government's revenues, and remittance from guest workers here collapsing due to the ARM scam unwinding. Mexico could stand either of those stresses ... but not both. The PEMEX bombings seem like a cause some days and merely a symptom of the troubles on others.

The only terror organization that is going to blow up anything in or around the Straight of Hormuz is the Bush administration. How much longer until 1/20/2009?

We're working on trying to stop the action.

http://www.prosefights.org/nmlegal/balderas/balderas#balderas2

There seems to be two aspects to the unwinding of structured finance - the quality (or lack thereof) of the assets, and the leverage used by the bag holders. If memory serves, Long Term Capital was leveraged 90:1, an absurdity made possible by the high quality of the underlying assets. The Bear's hedge fund that imploded a few months ago was leveraged around 30:1. Mentioned earlier in this thread, TPG-Axon took a loss of $110 million on the sale of $3 billion of its investments. This is only a 3.7% haircut; one would have lost more owning the DJIA last week, unpleasant but not the end of the world. Unleveraged this result is hardly a disaster; leveraged up the gazoo would be another story.

After Reg Q was abandoned, on a mark-to-market basis is was obvious virtually the whole US S&L industry was bankrupt. Ditto for the Japanese banking system in the 1990s. The BOJ created a fund to buy "lesser quality" loans at par, stuffed them in a drawer, and the banks avoided a huge hit to their balance sheets, albeit the Japanese stock market declined by over 80% from the peak in 1989 and real estate values did about the same, yet Japan remains the world's second biggest economy today. The "assets" backing SIVs may be landfill quality, but they are not worthless. What is freaking the market out is the clearing value of this paper, but at some price there will be buyers. As purely a hypothetical, say the SIV paper is worth 25% less than par. Given the amount outstanding, the hit would be $250B, a big number but not the end of Western Civilization - half the cost of the Iraq war to date. Returning to leverage, if some hedge fund is running 30:1 and takes a 25% hit it's lights out. Couldn't happen to a nicer group of folks. The most bearish thing I've seen in recent weeks was the announcement of the $100 (or is it $200?) billion bailout fund for SIVs: I had hoped that with the announcement of Q3 earnings by the banks they would have done a mark-to-market of their assets, the damage could be assessed, and the decks cleared. By establishing this fund it became obvious the banks are still playing peek-a-boos with their balance sheets, lowering investor confidence, and impacting the fear-greed game known as the stock market. My hunch is some one will start a secondary market in SIV paper since it's worth more than zero, the market for this trash will clear (buyers will meet sellers), leaving in its wake a lot of bag holders now wiser, if poorer.

On housing, my guess: House prices went from 2.8x average (or median, forget which) income from the late 70s, 80s and most of the 90s to 3.8x. A return to baseline is a 25% haircut - assuming flat incomes, true for most in the good old USA. Then again, there is replacement cost of the housing stock - with the money supply growing 24% a dollar might not get you what it did in the past.

These bubbles and financial shenanigans are in part due to the maldistribution of income in the United States. Income and wealth have become so concentrated at the top that those who control it have a hard time finding suitable investments. In their greed to amass even more wealth they are forced to lend to those nearer the bottom who can not really afford to borrow, but do out of desperation and the myths propagated by those running the show at the top. If income and wealth were more equally distributed there would be less pressure to lend and less pressure to borrow IMO. The obvious solution is to increase taxes on the wealthy to relieve some of the pressure to lend. Couple this with some social programs like national health care which would take some pressure to borrow from those at the bottom.

That's called socialism, which also have severe problems of inequity and corruption, as we have seen in the former USSR. The whole of our way of life, including this economy, is based on freedom and the ability to amass wealth and ownership. Take that right away, and it becomes a previlage instead, and democracy disapears.

Maybe there is no ultimate solution to how a civilzation should work. Maybe economies have lifespans and the only way to reset the wealth is for it to evaporate and have to start over.

Richard Wakefield

London, Ont.

No one is ahead of their time, just the rest of humanity is slow to catch on.

"That's socialism" Well, that's no way to rubbish a sensible argument. The failure of CDO's will act as a tax on the wealthy with no decent result. Europe is doing well with free healthcare thankyou very much, nothing wrong with a bit of socialism. In reality, there is no manichean solution, it is all about recognising the complex tappestry of competing requirements and both prioritising and compromising. Universal healthcare has more than a taxing benefit, those who are healthy can be productive, so are more able to generate wealth and are more able to borrow from the wealthy, so socialism in that sense is not a radical distruction of the system as we know it, in the way that occurs with communism. The previous poster was talking about a progressive mixed economy based on an uneasy concoction of economic rationality and humanist ethics. The sooner the US realises that it is stupid to leave poor people to die or be inactive and unfulfilled from lack of healthcare in the most wealthy country in the world the better.

"Nobody needs to go anywhere else. We are all, if we only knew it, already there." (Aldous Huxley "Island" 1962, p38)

I'm not saying no social programs, I'm against ripping off people's wealth for the sake of playing Robin Hood.

And as a Canadian I can assure you there is no such thing as free healthcare. In Ontartio it takes up 45% of provincial bugdets, and is still under funded so much that they had to raise our income taxes by $900 a year to help pay for it. Wait times for surgery are months if not a year or more, so much that some people are willing to pay to go to the US to have it done so their lives can be saved. So this "free healthcare" is not the miricle you make it out to be.

Richard Wakefield

London, Ont.

No one is ahead of their time, just the rest of humanity is slow to catch on.

You know, if the best you're suggesting is a replay of the dozen-year long Japanese depression, people will be jumping out of windows even if the country will survive.

Maybe that's why these guys didn't explain that they had history on their side.

Congrats and thanks for a thorough report.

Surely this is essentially the same as Nick Leeson opening another '88888' account?

When all the electronic money is either spent or lost, just open another account.

I watched the story of 'Rogue Trader' last week, telling the story of the collapse of Barings Bank.

There are so many parallels..

http://en.wikipedia.org/wiki/Nick_Leeson

http://en.wikipedia.org/wiki/Barings_Bank

There are indeed many parallels with Barings, but also with Enron, Worldcom etc.

Financial engineering (usually just leverage by another name) is not a good thing. It may carry individuals, companies and whole economies to the highest heights, but there's always a huge price to pay because of the underlying Ponzi dynamic. The excesses of this boom are far larger than any any other, hence we should expect the pain of the bust to be similarly extreme.

I spoke today to a woman in Okoboji, Iowa. She was a very well kept fifty something and as we talked I mentioned I'd just moved back to the area. She asked "What brought you back?" I replied "Have you been looking at the housing market? It looks like we're going to have an instant replay of the Great Depression." Living in this area and at her age means her parents were young adults for the Great Depression.

She blanched and then asked what I would do if I had a property on which I was "under water", pay it off or ... and she couldn't finish the question. Then it all came spilling out. She'd purchased a rapidly appreciating lot in Florida, sight unseen about six months ago. She put it on the market when things started to tumble and the best offer she has received is 20% of what she owes on it. I comforted her, TOD style, but that did nothing to reduce her fear.

"Well ... at least I can pay it off and live there when I'm old."

"How far above sea level is it?"

"I don't know ..." [again the blanch appears]

"Take a look around the internet. The arctic icepack collapsed this summer and the Greenland ice sheet looks like its going to start draining. A lot of Florida might just go away before too long."

I care not at all about speculators who get caught in the rip tide but this woman behind the counter in the independent book store just wanted a warm place to retire in another ten years. Maybe she'll get that ... just by staying here in Iowa :-(

SacredCowTipper even the IPCC report says that sea level rise of 20" in 100 years is the most, which they have scaled down considerably since the last report. It could very well take 1000 years for Florida to be totally underwater, if at all. Look at the sea level increase for Miami, for example http://tidesandcurrents.noaa.gov/sltrends/sltrends_station.shtml?stnid=8...

It has been increasing only 9.3 inches in 100 years. She is going to be fine there.

Richard Wakefield

London, Ont.

No one is ahead of their time, just the rest of humanity is slow to catch on.

Correlation isn't causation (in either direction) but how is it that the most excited right wingers are also the most vocal denialists about GW, PO and whatever looks like it is antithetical with "business as usual"?

Ever noticed the Voltaire quote appearing sometimes in the top right corner?

"Men argue; Nature acts."

What?

Richard Wakefield

London, Ont.

No one is ahead of their time, just the rest of humanity is slow to catch on.

Please review your sources, jrwakefield.

I suggest that you review the available data and that you actually read the IPCC reports rather than relying on second hand information about what the IPCC reports actually say.

"The greatest shortcoming of the human race is our inability to understand the exponential function." -- Dr. Albert Bartlett

Into the Grey Zone

Not acording to http://en.wikipedia.org/wiki/Sea_level_rise

IPCC 2001 report was 9 - 88 cm/100 years. 34 inches in 100 years.

IPCC 2007 report is now 18 to 59 cm (7.08 to 23.22 in) in 100 years. Looks like a downward change on the high end.

Also note in this link the uncertainties. The bottom line is the Tide and Currents measurments to 2000 DO NOT show any change in the rate of rise of .78 ft/century which is 9.36 inches per 100 years.

http://tidesandcurrents.noaa.gov/sltrends/sltrends_station.shtml?stnid=8...

So my position stands. In 100 years the sea levels MIGHT rise the 20 inches the IPCC claims, but the REAL MEASURMENTS so far do not support that for Florida (or anywhere else for that matter.)

Richard Wakefield

London, Ont.

No one is ahead of their time, just the rest of humanity is slow to catch on.