TWIP (This Week in Petroleum) 8-29-2007

Posted by nate hagens on August 29, 2007 - 6:59pm

This mornings Petroleum supply report released by the EIA showed reasonably high crude oil inventories, but all time record low gasoline inventories, as measured by days of supply. On the day, crude oil rallied $1.78, reformulated gasoline gained 8.5 cents and heating oil gained 6.5 cents.

Below the fold is this weeks TWIP

Good News, Bad News

As the Labor Day weekend approaches, there is both good news and bad news for drivers. The good news is that retail prices have been falling over the last several weeks and, nationally, are the lowest they have been since early April. The bad news, however, is that inventories are very low, especially in terms of days of supply (calculated by taking total gasoline inventories and dividing by the latest four-week average of product supplied). The low inventory level could limit the normal seasonal drop in retail prices after Labor Day.But first, here’s the good news for drivers. The average retail gasoline price is down 47 cents per gallon since its peak the week before Memorial Day. What’s more, the trend has been fairly consistent, with the average national retail price for regular gasoline falling 11 out of the last 14 weeks. High prices seen before Memorial Day spurred increased supply, both by domestic production and increased imports. However, recently, as gasoline demand reached its seasonal peak, imports declined and refinery problems dampened domestic refinery production, such that inventories have been used to meet demand. Over the last four weeks, total gasoline inventories have dropped by more than 12 million barrels, or somewhat faster than normally seen at this time of year. This sharp drop in inventories leads us to the bad news for consumers.

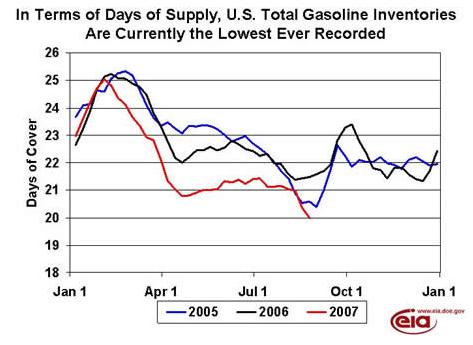

As the chart below indicates, not only is the absolute level of inventories low (see Figure 4 in the Weekly Petroleum Status Report), but in terms of days of supply, it is the lowest ever recorded (the days of supply data goes back to March 1991), reaching just 20 days. This is even fewer days than seen following the hurricanes in 2005. While the absolute level of total gasoline inventories has been slightly lower a few times in recent years, when the level of demand is taken into account, it has not been this low before. Of course, with gasoline demand set to fall significantly after Labor Day, the low level of inventories is not likely to cause a sharp spike in retail prices, but more likely will limit the usual seasonal decline seen after Labor Day, with the possibility remaining of an atypical slight increase over the next few weeks.

In Terms of Days of Supply, U.S. Total Gasoline Inventories Are Currently the Lowest Ever Recorded

What this means is that while retail prices are not expected to jump sharply on a national average, they are also unlikely to fall dramatically over the next few weeks. Of course, this expectation is based on the assumption that there are no major hurricanes or other non-market events impacting petroleum infrastructure over the next few weeks. With no storms forming in the Atlantic as of this writing, that should be considered as another bit of good news for drivers.

Gasoline and Diesel Prices Fall

The U.S. average retail price for regular gasoline dropped 3.6 cents last week to dip to 274.9 cents per gallon as of August 27, 2007, 9.6 cents lower than last year. All regions recorded price declines. East Coast prices fell 3.6 cents to 269.6 cents per gallon. Midwest region prices decreased 3.1 cents this week to 284.0 cents per gallon. Prices for the Gulf Coast were 2.9 cents less, settling at 265.2 cents per gallon, the lowest in the country. The highest prices were found in the Rocky Mountain region, where prices were 280.6 cents per gallon, down 3.5 cents this week and 18.3 cents per gallon below last year. West Coast prices decreased 5.5 cents to 276.8 cents per gallon. The average price for regular grade in California was 7.1 cents lower totaling 279.1 cents per gallon.Continuing the fluctuating trend, retail diesel prices were slightly lower at 286.3 cents per gallon, 0.5 cent under last week. Prices are 16.4 cents per gallon lower than at this time last year. East Coast prices fell by 0.8 cent to 283.4 cents per gallon. In the Midwest, prices rose 0.6 cent to 287.0 cents per gallon, while the Gulf Coast increased 0.1 cent to 280.8 cents per gallon. The Rocky Mountain region price fell by 3.0 cents, to settle at 294.7 cents per gallon. The West Coast price was down by 3.1 cents to 296.5 cents per gallon. California prices fell by 3.0 cents, to 298.6 cents per gallon, 21.4 cents per gallon lower than at this time last year.

Propane Stockholders Post Weak Build

Propane stockholders reversed course from the recent modest inventory rebound and posted a relatively weak 0.9-million-barrel build last week, moving inventories up to an estimated 54.3 million barrels as of August 24, 2007. With last week’s build, total propane inventories continued to drift further below the average range for this time of year. Moreover, with less than two months remaining in the typical build cycle prior to the start of the next winter heating season, propane stockholders’ ability of creating any significant inventory safety net by that time appears less assured. East Coast inventories gained the most last week with a 0.9-million-barrel build, while the Midwest and the combined Rocky Mountain/West Coast regions posted similar gains of 0.2 million barrels. During this same time, Gulf Coast inventories posted a loss of 0.4 million barrels. Propylene non-fuel use inventories plunged 0.3 million barrels last week to account for a much lower 4.8 percent share, down from the prior week’s 5.4 percent share.

I'm writing a post on the 'marginal barrel', which will examine the intersection of the market mechanism of setting price, with our natural tendency to discount the future in favor of the present. As long as the market has plenty of gasoline now, (even if the world stopped pumping oil we'd still have 20 days of inventories), futures prices stay subdued as conventional wisdom suggests that at some point gasoline stocks will go back up. At how many days supply will the market (and hence the average person) start to pay attention? (This is a rhetorical question, but perhaps a good one for discussion)

Contact

- Content: editors at theoildrum dot com

- Tech support: support at theoildrum dot com

License

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.

As I recall, we don't really have 20 days of supply. Some of this oil is filling the pipeline, and is in some sense not available for use.

If there is any kind of problem (hurricane coming, for example), and people suddenly start filling the gas tanks on their cars fuller, it would seem like we are already pretty much in to problem territory.

Does anyone have any calculations as to where we really stand? North Dakota is having trouble getting gasoline -one indication supplies are pretty low.

The whole "days of supply" concept is of no value. We could have zero days of supply, but as long as the truck was pulling up when we were, it wouldn't matter. We could have a 1000 days of supply but only one truck.

It's a national number, like real estate, that as you pointed out is meaningless in North Dakota.

Price is still the best indicator of availability.

Then why does the EIA use it?

And the $64,000 question is: Is price the best indicator of immediate availability or of long term availability?

Immediate availability!

C'mon Nate! You have had key posts based on discounting the future for the present.

Well I know what I think, but Im not always right.

It's more than mildly interesting that the markets believe that price is the best indicator of both of short term AND long term availability.

The price at the station is the immediate price. You can get the futures price from the nymex, which is a discounting mechanism based on what people think the future value will be.

http://www.nymex.com/lsco_fut_cso.aspx

Why does the EIA use it? Why do we need another 50B for Iraq? I just don't know.

Sorry - I was being sarcastic.

Im aware that the current price essentially equals the future price for the next 7 years, both on gas and on oil, which led to my statement - Why are the prices nearly identical? Glut of oil today? - futures prices in 2014 drop. Hurricane in the Gulf? 2012 futures rise (though not as much)

As long as there is no unlimited storage, these relationships dont decouple. But even if there was unlimited storage, I think prices of energy would be relatively flat all the way out the strip ( in a way there IS unlimited storage - that of keeping the resource in the ground.)

In other words, prices are going to tell us we have enough, until we don't.

That's cool. I agree with your last line completely.

You know, there are more boats for sale in the spring than in the fall, yet boats cost more in the spring. It's hard to explain the nuance to people that things cost what they cost based on what people will pay. Like I stated below, generic canned corn cost less than the national brand, but not because there is more of it.

When the days of supply does reach zero, I'm sure you and I agree completely on what the price will be that day!

I have been wondering if EIA's seasonal adjustment factors are getting out of whack. They keep saying we have don't have enough gasoline. I see no shortages anywhere. The doomsters cling to a single station closed in Missouri etc., when there are 200,000 gasoline stations n the USA.

Another query: If the EIA keeps warning about low supply, do station owners "top off" their tanks more than otherwise? I would, if I were a staion owner. So, do we have additional days supply in station tanks?

Lastly, as pointed out here, gasoline demand may finally be cooling off. Year-over-year increases in demand are shrinking. Given new models of cars have higher MPGs, we may be at the inflection point. Demand will start going down in the future.

When gasoline hits $4 a gallon ($1 in 1979 dollars) then we probably will see a big consumer shift. Back in 1979 we saw it. Gasoline is now $2.65 a gallon in Los Angeles. Much cheaper than 28 years ago.

You really can't criticize consumers for responding to price signals. The price signal today is that gasoline is not scarce, and takes an even smaller fraction of income than in 1979. Nevertheless, thanks to improving technologies, we are seeing demand flatline.

I suspect we will ease into an era of annual and secular declines in gasoline demand very soon. Since our refinery capacity will be bumped up slightly, I think we are nearly though the woods now. Worldwide refinery capacity is rising rapidly, and is predicted to actually glut markets by 2010.

Addtionally, in a couple of years, ethanol will male up 6 percent of US gasoline by volume, and it is not counted in the EIA survey.

I, too, would prefer a little more cushion than we seem to have now (I am still skeptical about the EIA seasonal adjustment factors). But, hey, there seems to be plenty of gasoline.

You're dreaming. What this will do is guarantee that we'll be stuck with w/an inefficient fleet in a time of shortage. Where's the beef!? re mileage? The reality is that people are still buying big cars because gas is cheap. Where's the beef!? re demand? We use an astronomical amount of fuel. This is the deadly flaw in capitalism is that it allows things to be much cheaper than long-term scarcity should dictate. We will almost certainly have shortages by next summer IMO and yet we have cheap gas this.

Matt

Hey, whaddya know, BenjaminCole's back on the scene.

Fossil Flatheads rejoice!!!

The Fossil Flatheads are strong. They are growing. They are handsome. But mostly, they are right.

it is obviously antidoomer. either he got banned, or he likes lots of sock puppets.

"Days of supply" is a good indicator as to what sort of buffer we would have in an emergency. Less "days of supply" mean we have less room to maneuver with any sort of difficulties. There would be less supply for evacuations or emergency vehicles. This is where the SPR might make a big difference for us, if we reserve its use for real emergencies, of course.

Does that confuse crude with gasoline? We can't count SPR as days of supply for gasoline unless we account for the lag time between pulling the oil out and processing it.

Westexas has a post in todays drumbeat that say 2.4 days of supply in excess of MOL.

I often agree with WTs assumtions on things, but here ... no-no

Personally I don’t buy the idea that the”pipeline-content” is part of any statistics – no way. The transit oil is “the last oil” so to speak – and an added bonus to the post-oil tribes..

Of course the US has more than 1-2-3 days of backup supply – that is a no-brainer IMO.

On the contrary if the wrong guy farted in the Gulf – The US would have been empty in a week – because it takes at least a week for the smell to go by the jet stream, and as the strategic reserves are bound up in a small geo-spot, as I understand.. they will not yield much far and fast...

Sorry for being away for a while, (visited cali, nevada/vegas, and some inbetween states from there to michigan)

I lurked earlier, and WT understands that the MOL (minimum operating level) is the amount of crude needed to transport within the pipelines.

A given pipeline has a minimum and maximum value for transportation, go too high and the pipe will be air or a medium which is does not occupy enough of the tube to actually be pumped at any efficient level by the current pumps installed on the lines. If we are only 5 days worth of oil above that MOL, and 20 days of MOL is needed for regular transport, then if supply falls below the 25 day MOL (this is all hypothetical) the pipe will simply STOP WORKING PROPERLY.

Then all the oil will have to be moved on river barges, rail, and trucks!

The pipes having a min and max flow rate need to be understood as such, you cannot simply say put 10 barrels a day to MN and 45 to NV, the mins are quite high, and dictated by the pumps/infrastructure in use.

cheers, someone correct me if i am wrong here.

You are incorrect. The EIA itself has noted that the inventory numbers includes the MOL (Minimum Operating Level) which is what is in the pipelines. If that is the definition that the EIA uses for inventory then who are you to contradict them?

"The greatest shortcoming of the human race is our inability to understand the exponential function." -- Dr. Albert Bartlett

Into the Grey Zone

Ohh ,… thx GreyZone and jteehan .. and WT

… in this case I’m sorry for doubting these claims! BUT you didn’t actually provide me any usefull “direct” links for this …. Did you ?

Normally I prefer the idea of having trustworthy sources (knowledge) on my hand, before I argue something… this time “I only used my own logics”..

So what you actually are saying is that, according to EIA, the USA has only 1-3 days of overhead petroleum – I mean just in case of emergency? My man …

And the spite this, all you Americans feel all fine and your president sleeps well at night? How can Wall Street actually be working seemingly normally, with this in mind - ??

Parenthesis :

(I don’t get it; there must be more to these statistics)

Our president always sleeps well, after all he is blessed with a total lack of consciousness and an empty conscience. And Wall Street is nowhere near normal. Central Banks have injected over $1 TRILLION in "liquidity" into the markets in the past 2 weeks to prop up the markets from our subprime mess (much more than our compromised press is actually reporting).

I wonder if any of us will be giving thanks at Thanksgiving when we can't afford a turkey because of the bail out of the banking establishment? But I'm sure our Presidente will have a great feast and sleep very well with all of the extra tryptophan.

hehe yeah ckaupp - but you know what they say on Wall Street (?) - the fundamentals are all fine AND I reckon the US Oil Inventories are the pinnacle fundamental!

- and AFAIK the subprime-ramifications are not yet linked to any oil-issue so to speak - BUT as this posting is on oil-inventories, I'm having that in my puzzled mind here :-)

Certainly not all Americans feel fine. I certainly don't. This crap makes my stomach churn. I have no idea how anybody can go about business as normal after even a cursory review of energy, agriculture, and climate statistics.

- Scott

"Try sour grapes; you might like them."

Cultural insanity. Historians (if there is any civilization left) will look back on this era with incredulity and wonder how so many people could ignore what was plainly staring them in the face.

The asinine notion that we can treat the combined problems facing humans today with just the "free market" (ha! what a damned lie THAT is!) to solve them is beyond comprehension. If we were actually at war, the "free market" would have long ago been damned and we would have reacted to that as a crisis. And that is where the world is now - facing a combined crisis as serious as any global war could be. The problems facing us are huge and need addressed as the emergencies which they are, not as "business as usual" opportunities for one group of apes to screw another group of apes.

"The greatest shortcoming of the human race is our inability to understand the exponential function." -- Dr. Albert Bartlett

Into the Grey Zone

I didn't find exactly what you were looking for, but the title of the EIA report is Crude Oil Stocks at Tank Farms and Pipelines.

http://tonto.eia.doe.gov/dnav/pet/pet_stoc_cu_s1_m.htm

Pipelines are indeed used in the calculation.

According to the NPC report, Lowest Operational Inventories are:

Crude 260-270M

Gasoline 185M

Distillates 85M

I didn't copy the report because it's 96 pages, but it's (officially anyway) everything you ever wanted to know about petroleum storage. (About page 53) http://www.npc.org/reports/R-I_121704.pdf

I have tended to be sceptical of comments by Matt Simmons and others that it will be shortages rather than high prices that will mark the crisis when it comes, but cutting inventories so close to the bone really makes it much more likely that it will indeed be shortages that finally gets people's attention.

Realisticaly, something needs to happen because here in LA, while people are bummed about the real estate quagmire, they are still happy driving the big SUV's the cash out refis bought. There just isn't any sense that $2.75 gasoline won't go on forever. Unless that price moves, or supplies run out, or people become unemployed, they will continue to feed the beast.

Great moniker!

As I noted yesterday, if we use the 185 mb number of the MOL for gasoline, we have less than one day of supply in excess of MOL. This means that, as noted above, there have to be spot shortages already occurring around the country.

In regard to crude oil, we have about 4.3 days of supply in excess of MOL, versus around 8-10 days that we used to carry in the Eighties to early Nineties. Presumably, the industry has gone to a Just In Time inventory situation, because of the SPR.

So, we don't have any short term crude oil supply problems, because of the SPR. However, the risk we run is that the SPR will die a "death of a thousand cuts," as we slowly drain it because of declining world crude oil exports.

As noted above, gasoline is a different situation, and I would expect to see reports of empty gas stations this weekend.

Is the gas-station business run communistically or by collusion? That would be the only way I could comprehend shortage resulting from such low levels of gasoline inventory. Were it a free market, I'd expect prices to run up to the point where the shortages reliably occurred in the poorest areas, and not "randomly".

Actually, I suspect that we are looking at spot shortages because prices are too low, encouraging consumption. It's pure speculation on my part, but I wonder if major oil companies have been deliberately trying to keep prices at the pump down.

In any case, I'm not an expert on this issue, but it's really not that easy, for a number of reasons, to shift supplies around the country. We actually experienced some closed gasoline stations here in the Dallas area in the spring, when distributors moved gasoline out of the Dallas market to Chicago, but they had to do it with caravans of tanker trucks.

If one reads George Ure then one would know that his people expect something to happen over the weekend.

Now reading your post what popped into my mind for no reason is "what if a statistically significant number of people traveling over the holiday couldn't find gas to get home?"

Or just some of them with the MSM playing Eveready Bunny?

Charlie Fox in capital letters, eh?

"Price is the still the best indicator of availability"

Ahh, that explains why gas is always 10 to 15 cents/gallon more where I live versus in my in-law's city about 60 miles away. Mind you, this is all in the Los Angeles metropolitan area. I suppose one could conclude that gas is less available in my neighborhood than my in-laws. But that appears to be highly unlikely. We are served by the same mix of gasoline retailers, equally as far from the refineries in Long Beach, and equally as "reachable" from those refineries by freeway. I conclude that price is strongly influenced by the retailers ability to charge what the local market will bear. Is there collusion amongst the retailers? Heck if I know, but it remains a mystery to me why such large price gradients exist in the LA area.

the quote you mention is asinine at best

price indicates how much the consumer is willing to pay for a good, with an inelastic good such as fuel, the price will rise rapidly with decreasing supply. Price is suppose to signal to suppliers to increase production, however this cannot be maintained indefinitely. Eventually the demand for a good lowers (demand destruction) and everyone adjusts to the lower standard of living!

The ease of reaching a gas station is the likely culprit for the price discrimination in your area (or the affluence of residence, higher wages means more dollars chasing the same goods) if it is tough to build up new gas stations, then the incumbent gas stations can maintain their advantage by charging a premium which is caused by a lack of competition. (ie 1 gas station in 3 sq miles versus 10 in 2 sq miles, the 1 gas station will charge out the ass ,and the 10 will strongly compete for highest total revenue!)

The difference between Del Monte corn and Sunnyside corn is 15 cents and I can reach both cans without moving my cart.

Are you suggesting there is less Del Monte corn?

Maybe your in-laws live within a mile of a terminal and you live 61 miles from the terminal. Maybe it's a conspiracy to charge you more. Maybe it just costs more where you live.

And BTW, you don't get your gas from a refinery. I challenge you to find a single truck leaving a refinery. It's comes from a terminal, probably near an airport or real close to the rail road tracks where the pipelines are.

An acquaintance of mine owns a few gas stations. He claims three things. First that unlike the consumers of his gas, he doesn't get to decide when to order gasoline. The truck rolls in and pumps gasoline when they feel he should have it. He thinks that this allows them to supply him with gas on whichever side of a price swing that is most profitable to his supplier. Second, he claims that he only gets #0.12 per gallon of which $0.05 goes to the attendant. Finally, this slender margin $0.07 is too slight, so he is forced to hire family to keep as much as possible in his home. If the same is true in your area, then the price differences may be due to the station suppliers more than due to the station owners.

Anyone else notice the steep drop off on the chart the weekend after daylights savings? If we had the same schedule from a year ago, we might have been in MUCH better shape...

Daylight savings cannot save energy, if you are up earlier and it is light, then it gets dark earlier and you need to turn lights on at night earlier. Ditto for any other application or appliance you have in the house.

It's more useful to understand it in the 'think of the children walking to school' brain-fart, rather than 'it saves us energy, uh-hun!'.

I'm referring to the fact that Daylights Saving Time was a few weeks earlier this year. Numerous Golf Courses and Malls reported dramatic increases in players and shoppers, indicating that people were more inclined to go out driving to do activities. The decline this year almost perfectly coincides with this...

It seems to me having watched this unfold over the summer that gasoline imports are the critical component. Also we don't refine anywhere near the amount of gasoline we use.

But we also have a lot of ability to use the cheaper high sulfur and heavy crudes. We should be able to keep our oil supplies reasonable for some time. And of course the SPR. This means that although we have to compete for oil and pay market prices it will be some time before actual oil shortages are and issues.

However I've not seen any numbers on how much external gasoline capacity exists that can refine oil for our market. Also once the global oil supply becomes tight enough that 1/2 world economies are having problems I doubt the amount of gasoline refined for export may drop quickly.

In general the refined gasoline market for export seems to be similar to the oil export land model and we can conceivably expect a significant drop in the amount of gasoline available for export to the US in the near future.

This double export land concept with export land effecting oil then export land applied to gasoline points to a real and significant chance of a rapid decrease in gasoline available for export and/or a rapid increase in the price of exported gasoline with an absolute limit as countries with spare refining capacity refusing to export if they are having trouble securing oil for their internal needs.

So as these countries have less oil imports the first thing they will cut is gasoline exports. This will drive up the price of oil yes but as I mentioned above export gasoline may have a significant premium. And finally at some point their just is not enough oil to meet America's gasoline importing needs.

This crunch in gasoline exports or double export land model is one reason I think we will see serious peak oil problems as early as next summer.

"... once the global oil supply becomes tight enough that 1/2 world economies are having problems ..."

- I noticed that the recently-published list of countries currently with serious energy shortfalls is not only long, but it includes about 1/2 of the world population. I didn't do the precise tally, but the list includes China and India to start with, and some other large countries such as Pakistan and Bangladesh.

Understand that in many cases its not crude oil imports that are the issue but imports of gasoline/diesel or other refined products. These suffer a double export land condition. I.e limited by both imports and demand inside the countries with refineries. So if demand is high internally and oil supplies are tight your going to import oil meet internal needs and export whatever finished products are left over. Regardless of the prices for export. No country with finished product export capability is going to suffer internal shortages while supplying the export market. This forces a increasing premium on exported finished products. And a HUGE political issue.

The finished product exporters probably have more clout than the countries that export raw crude. I suspect that some of the finished products reaching America from Europe are politically motivated. It would be cool if we could find out who ships what where and the volumes. I suspect that political issues are becoming important.

So if you look at your list of countries having problems I think you will find that they are dependent on fairly large finished product imports and if the double export land model is correct these will indeed be the countries having the most problems and it will and seems to be happening ahead of crude oil export land issues. So the double export land of finished products will lead the WT export land model by quite a bit and offer a warning that more trouble is brewing soon.

Like I said the US will get wiped out by not being able to import gasoline long before we have problems importing crude oil. I expect the first serious shortages from gasoline import issues this summer. Crude import problems not till later in 2009.

US and iran compete for gasoline imports, tho less now because they are now rationing it. Accordingly, gasoline should become a bit more available on world markets and price is likely to decline... or, may already have done so.

Seems to me the US market should be buying every barrel of foreign gasoline possible, meaning selling crude (spr stands ready to deliver) and buying gasoline. WHy is this not happening, especially with gasoline cheap? A good thing for the gov to encourage... bush popularity will drop further if we run out.

Jkissing: Mexico is also importing a lot of gasoline.

Thanks for including propane in your report -- that is important to some of us.

Just wondering if you might consider the use of a service like Audiodizer (used by the MIT Technology Review Podcast) to turn TWIP into a weekly audio download/podcast?

http://www.audiodizer.com/

Although I do not work for the company and have no idea what the cost might be, it works really well for MIT and others.

-jason