Interview with Jean Laherrère

Posted by Luis de Sousa on August 4, 2007 - 10:25am in The Oil Drum: Europe

Jean Laherrère kindly agreed to give an interview to TOD:E by e-mail. For several years he was virtually the sole researcher modelling Coal depletion in the same vein it is done for Oil and Gas. Despite being considerably different from the common sense of limitless Coal, his forecasts were this year confirmed by several studies and reports. TOD:E got some comments on this matter as so on the general Fossil Fuels depletion picture and our future beyond them.

TOD:E : You have been calling for a thorough assessment of future Coal production for some time, claiming that Coal has been wrongly regarded as a virtually infinite resource, and that it will likely peak circa 2050. Since the beginning of the year we had several studies made public, that not only confirm your views on Coal, but show a peak even sooner. Remarkably, two different studies, one by the Energy Watch Group (EWG), another by David Rutledge (California Institute of Technology) point to a Coal peak by 2025. What do you think of these studies?

JL : Both studies are good and rely on BGR (German Federal Institute for Geosciences and Natural Resources) reserves and resources presently known, but it is hard from BGR data to estimate the coal ultimate recovery, because most of coal resources will stay as resources in the ground without being converted into reserves. The Zittel group (EWG) is right to say that data is of poor quality, because contrary to oil and gas there is no scout company collecting technical coal data and compiling a homogeneous world coal inventory. IEA, WEC just give the list of what national agencies report and these data are heterogeneous because nations usually report very optimistic values and there are no strict rules of coal reserves (and resources) definitions. There is always confusion between reserves and resources.

Furthermore in oil and gas fields, pressure gives an indication of the decline, there is not such thing in coal production. Also the conversion of hard and brown coal into barrels of oil equivalent (boe) is difficult and usually a wild guess.

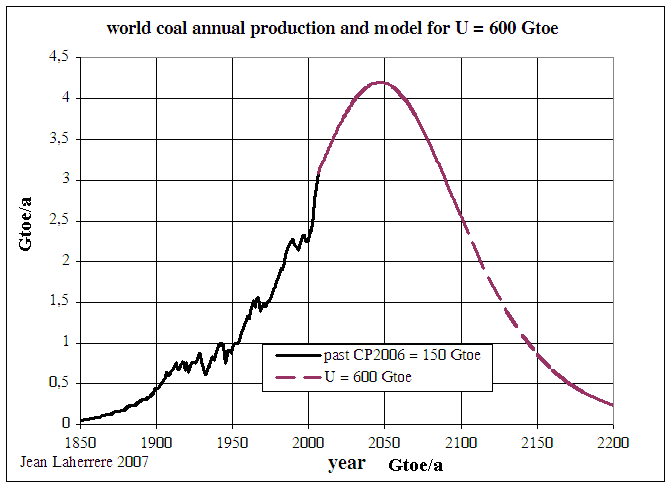

My coal ultimate is 1000 Gt (or 600 Gtoe), because in front of uncertainty I prefer to choose a round number than an accurate wrong one. Using the Hubbert Linearization can lead to wrong estimate when the plot displays several linear parts.

Zittel, and also Rutledge, rightly emphasize the large decreases of coal reserves in countries as Germany and the UK and they use a world ultimate close to mine, taking mainly only BGR reserves. Their coal peak is in the same range.

I always say that my plot of ultimate by a bell-shaped curve with a smooth peak is what the geology can offer, but constraints from the demand and investment may change it into a bumpy plateau.

Figure 1 - World Coal production with an ultimate of 600 Gtoe. Click to enlarge.

Figure 2 - World Coal production as forecasted by the Energy Watch Group. Click to enlarge.

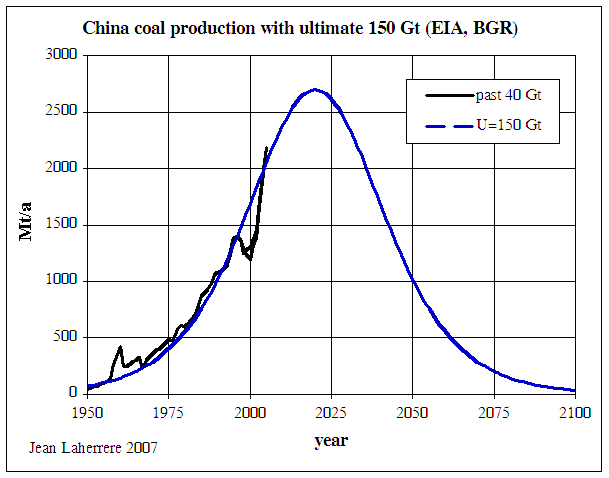

The main coal producer China is difficult to forecast because of the unreliability of data, but using an ultimate of 150 Gt (past production 40 Gt plus the 114 Gt EIA estimate) the peak is around 2,5 Gt (2,2 in 2005) in 2020, in agreement with Zittel. This explains why China is already importing coal. But BGR reports for China remaining reserves of 115 Gt but also 975 Gt of resources. How much of those resources will be converted into reserves?

Figure 3 - Chinese Coal production with an ultimate of 150 Gt. Click to enlarge.

But BGR (Thielemann, Schmidt and Gerling) has just published in the International Journal of Geology 2007 an article «Lignite and hard coal : Energy suppliers for world needs until the year 2100 –an outlook» which is much more optimistic, forecasting no bottleneck in coal supplies and a large potential for CTL.

So, the same data can lead to completely different views.

JL : I am an oil explorer that knows nothing about coal mining, but I see that France has closed in 2004 the last coal mine and has rejected a Scottish proposal to open a surface mine. France more likely will never produce anymore coal, while the BP Statistical Review 2007 is reporting reserves of 15 Mt (hard coal) with an R/P of 30 years. France has no more coal reserves, only coal resources!

France can do so because 80% of its electricity is nuclear, but other European countries cannot refuse nuclear and stop coal mining when oil and gas production is in decline in Europe. Germany is reported by BP as having 183 Mt of hard coal and 6556 Mt of brown coal; the BGR reports 161 Mt reserves + 8384 Mt resources of hard coal and 6556 Mt reserves plus 76 396 Mt resources of soft coal.

So you have to ask Peter Gerling about re-activating old mines in Germany.

JL : As far as I know, offshore coal exploration is done by oil and gas explorers because they log coal measures when drilling. And they found plenty of coal in the North Sea (some being the source-rocks of oil and gas). But offshore coal is considered as uneconomic at the present and the BGR does not count offshore as deep coal because of EROI.

But Underground Coal Gasification (UCG) may change the problem, if successful. I do not know too much on UCG except that many experiments have been carried out, but nothing commercial is in operation now, despite some claims by Ergo Exergy: all onshore.

UCG has a long history. The first UCG patent is from 1909, the Soviets were keen about UCG and had commercial plants in 1937, but dropped them in the 60s after the large natural gas discovery in Western Siberia. See the paper by A.Beath & B.Davis «UCG history» 14 Nov. 2006 Kolkata. It is for deep or thin coal onshore and not a word on offshore coal.

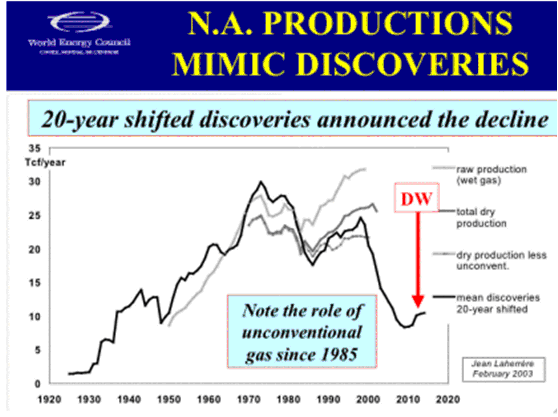

JL : I did warn first on North America natural gas peaking few years ago and my graph was in the WEC programme of studies 2002-2004 report «Drivers of the energy scene».

Figure 4 - Jean Laherrère's North American Natural Gas graph as published In the WEC programme of studies 2002-2004. Click to enlarge.

The US was counting too much on Canadian gas supply but they changed completely from increasing NG imports in AEO 2003 to decreasing imports in AEO 2004 (Laherrère, J.H. 2004 «Future of natural gas supply» ASPO Berlin May 25-26 - pdf).

Then I issued a similar warning for Europe because European NG production is peaking and the overestimation of NG reserves in the FSU (due mainly to a Russian classification based on maximum theoretical recovery giving 3P reserves and underinvestment in the Yamal Peninsula)

JL : The US has the largest coal reserves but the USDOE is forecasting a peak in CBM, despite heavy drilling. CBM production needs frac operations and to get rid of a large quantity of water, before and during production.

US NG production is declining despite a large increase in the number of producing gaswells (many being CBM). The US NG peak was at 22 Tcf/a in 1973 with about 100 000 gaswells, 2005 production was at 19 Tcf/a with 400 000 gaswells.

Figure 5 - US Natural Gas production and producing gaswells. Click to enlarge.

US CBM is a small part (tight reservoir is larger) of unconventional gas and the USDOE AEO 2005 forecasts a plateau in 2010 when the conventional production will be in sharp decline.

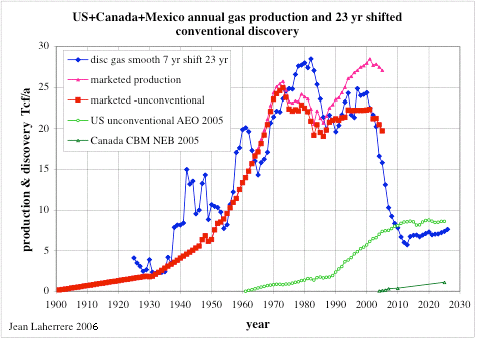

Figure 6 - North American Natural Gas production and shifted discovery.

Canada CBM with large coal reserves will not help much either, because CBM drilling in 2007 is down (lower price) and the CAPP 2007 forecast is less than 1 Tcf/a in 2020.

JL : When showing forecasts with bell-shaped curves, I have since several years warned that because of constraints the peak would be in fact a bumpy plateau.

World oil liquids is indeed presently in a plateau between 84 and 85 Mb/d since May 2005, when it went over 85 Mb/d; the last April production was 84.3 Mb/d, from table 1.4 of EIA. But the present two years step can be as the one in 2001 and 2002.

Figure 7 - World Liquids production 1997 - 2007. Click to enlarge.

For short term the problem is not the size of the tank (reserves and ultimate) but the size of the tap and the way the tap is partly closed by political constraints as insecurity in Iraq, Nigeria or nationalisation (Venezuela, Bolivia, Russia). Also the demand may decrease if there is a world recession and the US housing bubble is a bad sign for a country that has negative savings when borrowing 80% of the world savings!

The best approach for knowing what will be the world production of the next ten years is to look at all the megaprojects, as did Chris Skebowski. After a few revisions where he corrected the optimistic statements in volume and timing, he now forecasts a peak in 2011 at 91 Mb/d. Skrebowski is right to expect time delays (well illustrated by the MacNamara law where the ratio for frontier projects between initial and final is about “pi” for costs and “e” for time) because most megaprojets are late by several years, as Kashagan in the Caspian, Thunder Horse in the Gulf of Mexico, Athabasca new plants, etc.

I trust his forecast for oil, but he is not counting the BTL (biofuels) (large increase in volume, but small in global %) included in the oil supply of 85 Mb/d in 2006 and he has to guess what will be the decline of the present production.

CERA did the same approach and arrived to a completely different result with supply in 2010 being around 100 Mb/d. The difference is mainly due to CERA believing in the optimistic statements of future production but also of decline of present production.

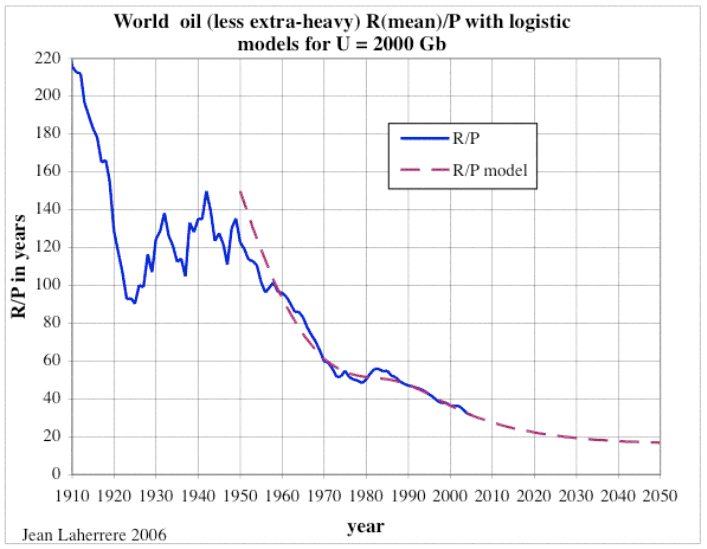

It is hard to say what will be the decline of present world producing fields, because of the lack of data in the Middle East and also quotas. Production mimics discovery with a certain lag and R/P trends towards an asymptote (Broto E. 2006 «General method to set up infinite limit of R/P» poster ASPO 5 Pisa).

R/P is a very poor parameter for forecasting, but it is often used by many.

So at the end of production R/P is constant as:

R=kP

If there is no new discovery:

∆R=-P and ∆R=k∆P

The depletion is:

∆P/P = ∆P/-∆R = -1/k

The depletion is the inverse of R/P. In Pisa I modelled world R/P trending towards 20 years.

Figure 8 - World R/P trend for Oil. Click to enlarge.

So world depletion should be trending towards 5% (1/20).

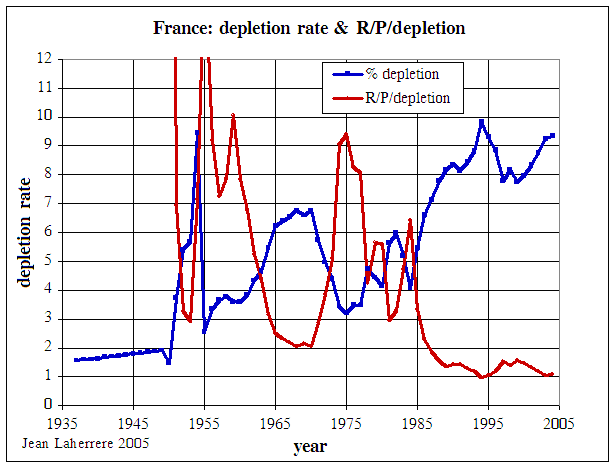

In 2005 I plotted for several European countries (France, UK, Norway, Netherlands, Germany) R/P and R/P/depletion. R/P being at the end the inverse of depletion, the ratio is trending towards 1. In Europe oil depletion seems to trend towards 10%.

Figure 9 - Depletion rate and R/P/depletion for Norway. Click to enlarge.

Figure 10 - Depletion rate and R/P/depletion for the UK. Click to enlarge.

Figure 11 - Depletion rate and R/P/depletion for France. Click to enlarge.

Figure 12 - Depletion rate and R/P/depletion for the Netherlands. Click to enlarge.

If European countries have a depletion rate trending towards 10% and the world towards 5% it means that OPEC countries will have a lower rate.

JL : Contrary to many researchers I use a several cycles model, I do not trust the Hubbert Linearization if the plot is not linear for decades. I use the derivative of the logistic function as model for each cycle because it is the simplest to plot using the peak value of the cycle, the peak date and the width of the cycle in years. Any other bell-shaped curve, as the Gauss (normal) curve, will work as well. I fit the last cycle to the last production value with the last trend (slope).

But I add in the text that this curve is to show simply what the geology can offer with the ultimate being the surface below the curve. But the supply has constraints from investment, politics, wars, insecurity and other constraints of the demand (high prices or recession). Any curve with the same surface below can fit depending the constraints. This is why I was also the first one to speak about a bumpy plateau instead of a peak.

What is important is to give the reader a production curve which has a surface below the curve equal to the ultimate. The curve can be modified to satisfy the constraints as long as the surface is conserved: any area below the model should be compensated by an equal area above the model. Most of forecasts are showing short periods before and after present, when mine are from the beginning to the end.

Hubbert in 1956 was modelling bell-shaped oil production by hand without any equation (he adopted the logistic curve much later) and he was saying that the production curve mimics discovery curve with a certain lag. He was right and often I do not model production, I just show production and shifted discovery to guess the future production by looking at the discovery curve which is ahead of the production time, as for example the natural gas of North America in the above graph in the NG chapter.

JL : I was also one of the first ones to say that, despite knowing little on economy being an oil explorer, I was more worried by a possible coming recession (following 2004 Paul Wolcker’s forecast) than by a peak from supply. I am also adding that geology is rational, when human behaviour is often irrational and this is why I refuse always to make any forecast on oil and gas prices.

I am convinced that the only way to leave to our grandchildren an earth with enough resources and not much pollution and debt is to change our way of life. Our consumption society is based on growth and our politicians and managers are judged on growth of GDP or stock market. Constant growth is impossible in a limited earth. In the past, our growth was possible because there was open space (go west) and large resources. Now we have to constraint our consumption to the limited reserves.

I do not trust a protocol which involves only governments; I believe that the constraint has to be on the consumer. I feel that Fleming’s approach on TEQ (Tradable Energy Quota) is better because each will decide if he wants to consume more than his share by paying much more his excess.

CO2 is the wrong enemy; it is wasting energy which must be reduced. Sequestration of CO2 will consume more energy and it is better not to emit CO2 which can be avoided.

Technology is very good to produce quicker and cheaper conventional fields, but cannot change the geology of the reservoir which determines mainly the recovery of oil and gas - for oil, 3% in a fractured tight reservoir to over 80% in very porous sand (East Texas field) or reef (Leduc, Rainbow in Canada or Intisar in Libya). Horizontal drilling manages to produce quicker (as using several straws to drink a glass of orange juice) but no more (examples that I have shown in my papers for giant fields as Yibal in Yemen, Rabi-Kounga in Gabon).

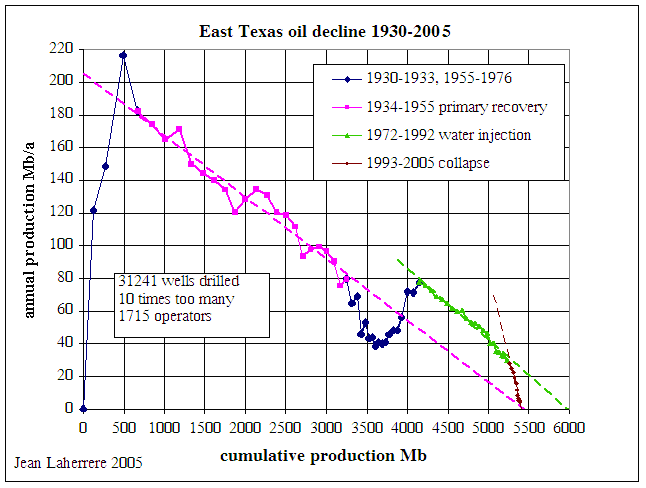

In fact technology allows to produce fields with a decline which gives false hope of ultimate recovery and in fact leads to negative reserve growth; East Texas is a good example because from 1969 to 1990 ultimate reserves were reported as 6 Gb but the collapse of the decline from 1993 to now (almost depletion) leads to a final recovery of about 5.4 Gb (negative growth of 600 Mb!). In fact, water injection (about 15 Gb of salt water) and too many wells (over 30 000 wells = 4 acres/well, because 1715 operators = too many straws) succeed to produce 86% of the oil in place (very well known because the large number of wells).

Figure 13 - East Texas decline 1930 - 2005. Click to enlarge.

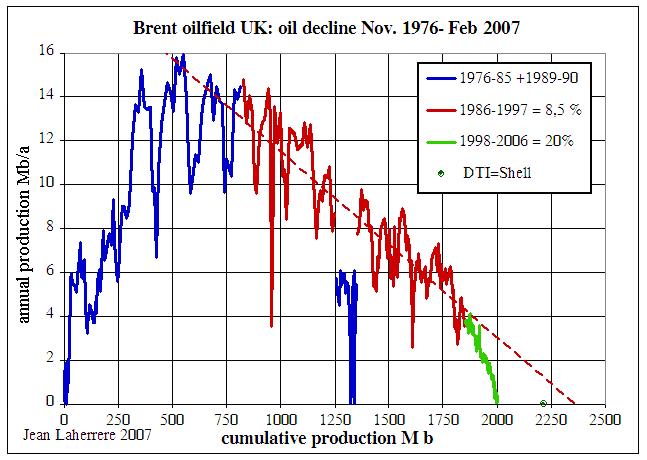

It is amazing to find about the same story for the Brent oil field in the North Sea, where official estimates are higher than the cumulative production of the field, which is almost depleted after the collapse started in 1998 that doubled the decline. Brent is now producing mainly gas and the so called Brent marker is not anymore with Brent oil, but from other fields as the new Buzzard which is of less quality.

Figure 14 - Brent decline 1976 - 2007. Click to enlarge.

Reserve growth occurs in the US because of the obsolete SEC rules which prevents the report of probable reserves as in the rest of the world. Canada dropped such bad practice in 2003. US reserve growth is mainly due to the omission of probable reserves and also to wrong unscientific arithmetic aggregation (a Monte Carlo should be run to be correct).

There are many examples of negative reserve growth and few examples of positive reserve growth where decline improves with time, all that I found are due to exceptional geological conditions as Eugene Island 330 or Ekofisk (compaction of the reservoir with 8 meter seafloor subsidence). These examples cannot be extrapolated to the normal field conditions. But technology can change the viscosity of oil with steam or chemicals or fire in unconventional fields.

We will need all energy that we can produce and no energy can be rejected for irrational reactions, but the best solution is to first save energy. It is obvious that Americans consume twice more energy than Europeans for a similar income, but the big difference is that energy is much more expensive in Europe because of taxes. Americans went to compact cars in 1979 because they feared the tripling gasoline future price (which was completely wrong with the arrival of the counter shock!).

Energy is too cheap everywhere because for the last 40 years world energy cost about 5% of the GDP when experts (Kummel, Ayers) have shown that the contribution of energy to the GDP is about 50%. Everyone knows that an electricity blackout stops immediately all activity in the industrial world. It is a joke to read that the US core inflation excludes food and energy, as if American consumers can live with a car without gas, a house, TV and computer without electricity and meals with only water.

Agriculture uses most of the useful soil and using more will diminish the lungs of Gaia, being the forests. World grain production is flattening and stocks have been reduced from 120 days to less than 60 days. Agriculture cannot feed the world and fill the tanks of the cars.

There is not substitute to oil for transports except synthetic oil. All unconventional oil, as extra-heavy oil (Athabasca and Orinoco) needs time to be produced in large quantity. Lack of workers and infrastructure (as water and cheap energy for steam) leads to peak oil occurring well before they can reach a large volume. It is not possible to have a baby in a month with nine women. It is the same with Gaia.

Oil shale has an EROI and such environment problems which condemn any mining operation after many failures, the last one being in Australia. The in situ Shell experiment (which heats the kerogen with electricity for years in several wells to generate oil and gas when freezing around) is likely to have also a poor EROI, because Shell after many years of research has not yet decided to build a commercial pilot. The USDOE is not counting to any shale oil before 2030, if any.

Oceanic methane hydrates are too dispersed and limited horizontally - to few meters - and vertically - to few millimetres - to be ever produced.

Wind and Solar are intermittent and need back up thermal plants. It is in Germany and Denmark that more windmills are found because they have many coal plants that they can use as backup. This is not possible in France because nuclear is used mainly on a base level. In France we pollute much less than in Germany.

World coal is reported with a R/P of 250 years, with US being the Saudi Arabia of coal. But the US National Academy of Sciences has recently estimated that 100 years is more likely. Global warming is now well considered as a threat and will soon replace nuclear fears. So constraints on coal will increase.

Nuclear is the least dangerous energy, but there are limited uranium 235 (0.7% of mined uranium) reserves with present reactors techniques, fast breeders are needed to use uranium 238 and thorium. In France 80% of the electricity is produced since decades from nuclear plants and no one was killed, but when during the same time hundreds of people were killed by natural gas explosions in their houses. Coal is killing tens of thousands of people in the world mines. Wood fires are killing also many in developing countries because of smokes.

Technology can be a big help in developing new energy if succeeding in the following research fields, which have started decades ago:

- cheap photovoltaic

- light, cheap and powerful batteries to store renewable intermittent energy

- cellulosic ethanol (miracle enzymes to be found)

- in situ coal gasification

- fast breeders (fourth generation) and accelerator driven systems (ADS) proposed by Rubbia to use uranium 238, thorium's large reserves and also nuclear wastes

- fusion

Let us hope than at least one of them will succeed. Simple techniques to save energy are well known but need motivation and change of live to be carried out.

Information on the energy future problems is the first and best technique to convince people to save energy. I feel that The Oil Drum is doing a good job for that.

Biography

Born May 30, 1931. After graduation from Ecole Polytechnique and Ecole Nationale du Pétrole in Paris, he participated with Compagnie Francaise des Pétroles (now TOTAL) in the Sahara exploration with the discoveries of two supergiant fields: Hassi Messaoud and Hassi R'Mel. He went to explore Central, Southern and Western Australia. He was in charge of exploration in Canada for TOTAL in Calgary where he started exploring Labrador Sea and Michigan. After 15 years overseas, he went to TOTAL headquarters in Paris where he was in charge successively of the new ventures negotiation, technical services and research, basin exploration departments and finally deputy exploration manager. He was member of the Safety Panel of the Ocean Drilling Program (JOIDES). He was President of the Exploration Commission of the Comité des Techniciens of the Union Française de l'Industrie Pétrolière where he directed the publication of a dozen of manuals. He was director of Compagnie Génerale de Geophysique, Petrosystems and various TOTAL subsidiaries. After 37 years of worldwide exploration with TOTAL, he retired in 1991. He is now writing articles and giving lectures. He has written several reports with Petroconsultants and Petroleum Economist on world's oil and gas potential and future production. He was a member of the "Society of Petroleum Engineers/World Petroleum Congress ad hoc Committee on joint definitions of petroleum reserves" and also a member of the task force on "Perspectives Energie 2010-2020" for the "Commissariat Général du Plan". His graphs are used in the International Energy Agency 1998 report "World International Outlook" and in the World Energy Council reports 2000 "Energy for tomorrow's world - Acting Now" & 2004 "Drivers of the energy scene". He chaired the 2002 World Petroleum Congress (Rio of Janeiro) panel on hydrates (RFP9 "Economic Use of Hydrates: Dream or Reality?"). He is a member of ASPO (Association for the Study of Peak Oil and gas).

On behalf of the team at The Oil Drum: Europe, I’m glad to thank Jean Laherrère for taking this interview and fully committing to it, even updating his graphs and providing them for publication.

Luís de Sousa

Personnel

Editors

Contributors

Peak Oil Primers

Archives

- November 2010 (3)

- October 2010 (6)

- September 2010 (4)

- August 2010 (7)

- July 2010 (6)

- June 2010 (7)

- May 2010 (2)

- April 2010 (8)

- March 2010 (4)

- February 2010 (6)

- January 2010 (3)

- December 2009 (5)

- November 2009 (8)

- October 2009 (12)

- September 2009 (6)

- August 2009 (5)

- July 2009 (11)

- June 2009 (8)

- May 2009 (16)

- April 2009 (10)

- March 2009 (7)

- February 2009 (10)

- January 2009 (15)

- December 2008 (9)

- November 2008 (9)

- October 2008 (9)

- September 2008 (13)

- August 2008 (10)

- July 2008 (14)

- June 2008 (23)

- May 2008 (16)

- April 2008 (12)

- March 2008 (16)

- February 2008 (9)

- January 2008 (13)

- December 2007 (13)

- November 2007 (16)

- October 2007 (22)

- September 2007 (8)

- August 2007 (9)

- July 2007 (16)

- June 2007 (8)

- May 2007 (7)

- April 2007 (7)

- March 2007 (10)

- February 2007 (10)

- January 2007 (12)

- December 2006 (9)

- November 2006 (15)

- October 2006 (4)

- September 2006 (5)

- August 2006 (5)

- July 2006 (9)

- June 2006 (5)

- May 2006 (10)

- April 2006 (9)

- March 2006 (13)

Vital Trivia

License

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.

A lot of this sounds reasonable. Re coalbed methane one part of the world claims enough resources to export a liquefied gas http://www.smh.com.au/news/business/santos-to-build-5bn-lng-plant-for-ex..., to hot bleach bauxite into alumina and electrolytically smelt aluminium. Mind you they pay no carbon taxes.

I totally agree the emphasis should be on emission prevention not capture or claimed offsetting. Months ago a TOD poster suggested an oxidation tax which covers most manmade CO2 somewhere along the line; for example even if the final fuel burn is steam reformed hydrogen. A no-credits oxygen tax is hard to avoid or scam.

Since P/R is an indeterminate form (0/0) as depletion approaches I think commentators should say depletion is now x% but is expected to be y% in 5 years, or somesuch.

Jean Laherrère says,

"The Zittel group (EWG) is right to say that data is of poor quality, because contrary to oil and gas there is no scout company collecting technical coal data and compiling a homogeneous world coal inventory."

By this remark I would asume that Laherre're is implying that the data concerning coal is worse even than data concerning oil and gas...

That is almost completely incomprehensible....imagine ANY data about ANY thing being worse even than the data we have concerning remaining reserses and resoursed about oil and gas...it simply does not seem possible.

Based on that, I have to be honest here and say that one could make just about about any "conjecture" concerning the remaining coal resourse/reserves/future production and be completely impossible to refute.

The whole thing becomes nothing more than a complex superstition on all sides.

Roger Conner Jr.

Remember, we are only one cubic mile from freedom

Luis - what an amazing amount of work - packed with information. Thanks alot to you and Mr Laherrere for putting this out.

When looked at in this way, I don't see how this can't be viewed as an 'energy' problem instead of just an oil problem. So many of our energy resources are interwoven - if coal and natural gas (in NA), will also be facing cost/depletion pressures, I don't see how we are going to avoid an energy train wreck.

One note - the (ominous) natural gas vs wells graphs in Figure 5 ends in 2005 - the US has increased NG production in both 2006 and ytd 2007, though not up to 1973 or 2000 numbers.

Above all blame Jean! I only wrote the questions.

Yes, for now we are facing a liquid fuels problem, a much worse problem with energy will unfold when Natural Gas and Coal start loosing their growth momentum by 2020.

Jean gave us good clues on that, life style change and some interesting alternatives like the Rubia reactor – a personal favourite of mine.

NG production is indeed growing in the US, but with Canada beyond peak and the recent collapse in prices the North American picture still isn’t that good.

Carlo Rubbia is the inventor of the 'Rubia (sic) reactor'. He is a Particle Physicist of very considerable scientific talent. And also a very skilled self promoter (very important to gaining a leadership position in Particle Physics). His proposal, I think, involves the use of Particle Accelerators to maintain a fission reaction. He appeared to never had a serious of working on development of this idea HIMSELF. It was a proposal designed to promote the development of bigger and more powerful Particle Accelerators, which would facilitate his scientific research program, and maybe acquisition of another Nobel Prize.

I think one should not count on this idea ever becoming a reality. It will be like controlled (non-explosive) nuclear fusion - always in the future.

As I noted over on the Drumbeat thread, the Kashagan Field is the only confirmed one mbpd and larger field on the horizon, with recoverable reserves of about 9 Gb or so.

From nuclear + fossil fuel sources, the world uses the energy equivalent of 9 Gb of oil every 45 days.

BTW, I have been expecting--based on the HL (logistic model)--to see a decline in Russian crude oil production. When Russian crude oil production does start declining, I expect the decline to be rapid. If their production declines at 10% per year, and if the consumption continues to increase at about 5% per year, their net oil exports will be down by about 50% in three years.

Jeffrey J. Brown

http://www.energyintel.com/DocumentDetail.asp?Try=Yes&document_id=208885...

Russia Cuts August Black Sea Crude Exports, Maintains Baltic

Tuesday, July 31, 2007

One concern I see expressed with regards to oil production over and over is that it's possible to prop up production today at the expense of production tomorrow. It seems to me (please correct me if I'm wrong) that this concern should be even greater when it comes to natural gas. What is there to stop us from using our natural gas at large production rates up until the last bit is used? With oil there is a loss of pressure to mitigate this (as I understand it). And with gas?

The notion of production increase after 2005 is misleading. The issue is really suppressed production in 2005 relative to the other years due to the hurricanes in the Gulf. Dry gas production dropped over 500 Bcf from 2004 to 2005, which is almost exactly the hurricane impact. There was still some modest ongoing loss from hurricanes in 2006. What appears as an increased NG production is simply a recovery from the hurricanes. The numbers from EIA in Bcf:

2003 19099

2004 18591

2005 18074

2006 18531

First 5 months in 2007 so far total: 7756

first 5 of 2004, prior to hurricanes was: 7806

What we really have is a slow drift down in production despite all the increased drilling.

Damage from rapid production in oil wells typically relates to either:

1.) A loss of the gas in solution due to pressure drops (gas solution drive reservoirs) The result is otherwise producible oil with nothing to make it mobile. It just sits there rather than moving toward what should be the lower pressure of the producing well bore. These sorts of depleted reservoirs are often excellent candidates for water flood redevelopment.

2.) Coning of water as the rapidly produced wells draw water from deeper in the produing formation rather than producing water free oil from the top of the formation. (Water drive reservoirs) This has the effect of leaving oil behind and bypassed. In fill drilling can tap into the by passed oil, but drilling new wells is an expensive proposition.

3.) Expanding gas caps as gas comes out of solution in the reservoir. This gas sits on top of the formation where the producing oil wells are now only capable of gas production. Producing that gas causes more problems are pressures drop further (the gas cap stays in place and probably grows with the loss of energy as noted in "1" becoming a real problem. Reduced pressure can also result in finicky pump performance when the pressure drop is very localized restricting or stopping production as a "gas lock" develops in the pump. This is sometimes a big deal with low perm reservoirs. You have to be patient and let the oil come to the well bore.

4.) Overly aggressive attempts at stimulation [ill advised or overly large frac jobs and acid jobs] can lead to "breaking into water as either the well is opened to an adjacent and potentially non oil bearing zone, or a highly permiable but largely vertical streak is opened up [think of a straw going to the bottom of a drink when the good stuff is right on top -- the "Super K" zones that occasionaly are mentioned as one of the issues facing Ghawar are an example of this sort of problem.]

The point is that gas wells typically don't have these issues. Producing a gas well flat out will somtimes leave behind some oil like liquids [and some "gas wells" make quite a lot of these liquids] and overly agrressive stimulation can lead to opening up zones that are not productive just like in an oil well ... but rapid production of a gas well typically doesn't cause the same type or severity of problems as too rapid production does for oil wells.

Hardly a technical explanation, but I hope that helped.

Thanks, RW Reactionary,

Thats a quick, short and sweet summary of overproduction issues.

I think one of the great oil business moneymakers in the next 20 years will be identifing reservoirs that were abandoned early because of overproduction, and going in and reengineering them. There's a ton of Texas and Louisiana salt dome fields and shallow fields in the Ft. Worth basin, Oklahoma and California that need to be reevaluated. I suspect we can get the URR* of these fields up by 10%-20% fairly easily.

Of course, this will only help moderate the peak. Its not the size of the tank, its the size of the tap. Once original pressure has been disipated, its hard to get a huge flow again. And the lifting costs are very high, with a big expense for water treatment and disposal. Land costs are outrageous. I've got several prospects like this that I'm working up.

*URR=Ultimate Recoverable Reserves

Bob Ebersole

Perfectly correct , we are not going to avoid an energy train wreck ,

It probably will be a modern democratic society train wreck ,

miserable third world peasants will not feel a thing

urban service providers living in mega cities will disappears first

I suppose it will stabilize itself eventually at a sustainable level , once the population had adjusted to new (old) numbers and new (old)lifestyles

Long term , there is no problems

There is not substitute to oil for transports except synthetic oil

Yes there is !

http://www.energybulletin.net/31824.html

Best Hopes for Understanding Alternatives,

Alan

Alan,

Obviously we are talking here of energy vector substitutes for current systems. Electricity, although possibly a better and more lasting vector, implies major infrastructure changes - as you know better than anyone.

Not as major as you think.

Electrifying existing railroads is, quite frankly, not that big a deal in the scope of other solutions suggested. (even South Africa, with all of their problems, has electrified 1,600 km of their main rail line with more to come).

An electric railroad works like a diesel railroad, except it accelerates & brakes faster. It is really not a "new system".

Adding back tracks torn up 30 or so years ago is also not a "big deal" compared to Tar Sands or other alternatives.

Building significant amounts of Urban Rail could be done with the current new highway budget.

Increasing bicycling requires trivial new resources. And electric trolley buses have lower life cycle costs than diesel buses.

Best Hopes for Expanding the View of What is Possible and Easily Doable,

Alan

PHEV's will require very little infrastructure. 90% of vehicle owners have off-street parking, and could just plug them in.

Hmm, that you're only aiming for 10% cut in 10 years doesn't sound nearly ambitious enough.

As high a cut would surely be more simply acheived by fuel economy improvements: after all, the Europeans already have an average fuel economy nearly 50% higher than the U.S., implying a 30% cut in oil usage, so if a third of Americans collectively upgraded to vehicles that averaged European fuel economy ratings over the next 10 years, that's an 10% cut right there.

Of course, combine the two, and you've got a 20% reduction in 10 years...which might be just enough to keep up with oil import depletion rates.

-10% is a conservative, quite defensible estimate under a modest decline in world oil exports. A modified BAU situation.

Rail has elasticity of supply. The worse things get, the more people and freight it can move (to upper limits).

And once we start building it, we can build more faster. The savings in the second ten years will be larger than the first ten years.

It is a "silver BB", not a silver bullet. Hummers will have to go ! Do this and other steps to mitigate post-Peak Oil.

Best Hopes,

Alan

In some ways I see "electrification of transport" in general, including replacing all private vehicles with PHEVs and EVs, and of course electrification of mass transit (heavy and light rail), as the only realistic way to allow civilisation to continue without oil.

In that sense, it is "the silver bullet". But calling it that might convey the impression that it means little has to change, whereas of course in reality, it means massive change, over many many decades...although, it must be said, not necessarily any more massive than the amount of change that happened throughout the either half of the 20th Century.

I see "electrification of transport" in general, including replacing all private vehicles with PHEVs and EVs, and of course electrification of mass transit (heavy and light rail), as the only realistic way to allow civilisation to continue without oil

Grenoble France is working towards a walk + bicycle + tram (+ TGV for longer distances) solution. I think that bicycles (including electric bikes, especially for elderly) can take a larger role than EVs.

But it will take more than a decade to get to a minimal oil infrastructure.

Best Hopes,

Alan

Thanks Luís for this interview of Jean Laherrère! it was long overdue. Jean is a very important person within the PO community. Personally, his work has motivated me to crunch the numbers.

Luis and Jean:

Thank you both for this excellent interview and presentation. It seems obvious that the both of you spent a huge amount of time editing, polishing and researching this great summary of the world energy situation.

Questions about coal bed methane:

Coal bed methane production requires horizontal drilling, fracturing and dewatering of the coal, including a huge cost for water disposal. Does methane extraction improve the economics of the ultimate use of the coal by dewatering the coal? Does the methane extraction decrease the BTU content of the coal, or is this methane that otherwise would have been vented to the atmosphere by mining? Does anyone have much of a handle on the size of the resource, or the costs of drilling and completing the wells? How shallow can the wells be drilled and completed?

Bob Ebersole

Brine disposal is the key to coal bed methane.

Everything else is just money and steel.

Bob:

Getting the water and the gas out of the coal before it is mined improves both the safety and economics of the latter. For safety reasons the gas is a problem when still present during mining, since the concentration must be diluted, by puping in additional air, to ensure that it stays at safe levels.

Removing the gas does not affect the coal BTU content, and if it can be removed, pre-mining it can improve the economics, because it can be collected and sold. If it is left to vent into the mine workings during mining, it becomes too dilute to be worth collecting for use.

Drilling very shallow horizontal holes can be a problem, though there are some technical solutions (most aggressively pursued in Australia) that show a lot of promise.

Jean,

Thank you for the great post. I am glad to see the new R/P plots. Can't bash on them enough. Your multi-cycle plots work extremely well for coal.

"MacNamara law where the ratio for frontier projects between initial and final is about “pi” for costs and “e” for time"

This is a great comment. Is it from Robert McNamara, the Vietnam era US Defense Secretary? Any hope of an original reference for it?

Luis,

Thanks for facilitating.

"Agriculture uses most of the useful soil and using more will diminish the lungs of Gaia, being the forests. World grain production is flattening and stocks have been reduced from 120 days to less than 60 days. Agriculture cannot feed the world and fill the tanks of the cars."

Very good point. But as I said in a previous post, if current agro-exporting countries can keep running after PO by maximizing biodiesel production they WILL do it. So while the last sentence is certainly true, the implied advice is useless because "the world" does not make decisions as one unit. The most probable outcome is that some parts of the world will have their tanks filled and some other parts will not have food, at least for their current populations, much less for hypothetical larger ones.

Excellent interview!

Only comment: I don't think France's nuclear experience can be be ramped up to meet the needs of the world. Would France ever dream of letting US (or Russian) firms run their reactors? Or worse still, contract out regulating them?

I don't understand what you are saying. Can't we let the French, Americans and Russians all run their own reactors?

What I'm saying is that a proliferation of reactors in the world in proportion to the rate they are used in France would lead to a safety record far worse than France's in many, most or all cases. Yes, let the Albanians, the Americans, the Russians each run their own reactors! You're ok with that?

Thank you Mr. Laherrère it gets tiresome to hear all the plans for alternate energy that merely end up meaning more energy for us energy pigs.

France has no coal reserves only resources?!...I am tempted to use the acronym for Laugh out Loud. On this continent the idea of keeping the coal buried is considered incomprehensible even if using it means death of a planet. Nuke takes too much time and money, much better to use that time to turn Iraq and Afghanistan into charnal heaps instead of using those resources to go nuclear and leave all FF in the ground. Who knows maybe produce enough electrical energy to be able send Alan's Electric Train to the moon, play golf and be back in time for tea and buns. North America is the land of NIMBY as far nuclear (and much else).

We have a world with it's sun that is a closed working entity, call it Gaia and we have built a mechanism which is tearing that entity apart, any additional energy will add to that problem no matter how politicaly warm, fuzzy and alternate it is.

Here is a plausible place to post a comment of puzzlement:

Is there any real prospect for transition to a post fossil-fuel World without massive societal disruption somewhere in the World? I think not. Is it at all safe for the World as a whole, to have ANY nuclear power plants in a place where there is massive societal disruption? Surely, not.

So why think that nuclear power can be part of the least bad option for the future? Surely the least bad option is to go directly to a World powered by solar and its derivatives, namely biofuels, wind, hydro, PV, etc., and leave all the nuclear power radioactive wastes uncreated.

Considering we have no problem leaving our C02 waste around for thousands of years I don't think nuclear will be considered.

I look at it this way, if it is in the ground the reserve estimates are just that, estimates. Which means that you really don't know how much you have for sure. That ought to give people pause before they buy that next big SUV or monster house.

I think that if we use renewable energy and slow the use of fossil fuels, the air will be cleaner, the environment will be cleaner and we will be generally better off. The fossil fuels will remain in the ground where they have been for millions of years. They are not going anywhere, they are a savings account. It is not like we have to quickly dig them up and burn them up before they go bad.

Mr. Laherrère

Thanks for your post. I've become increasingly concerned about the ability of the energy industry to operate as resources peak. The energy industry itself seems to be heavily dependent on a ready supply of cheap energy and other basic resources such as steel. Since the energy industry in general denies peak and seems to dismiss the problem of operating in a expensive energy regime.

I however believe that as resource production declines it will have a major negative impact on the ability of the energy industry to operate and extract resources. This means problems across the board from price to availability and ability to initiate and budget for projects. So I expect to see massive cost overruns and delays from shortages and these events will increasingly prevent the energy industry from being able to effectively exploit remaining reserves. This of course lowers production leading to more shortages.

I've not seen anyone address the issue of how peaking in resources will effect the energy industry maybe you would be willing to look at the issue.

ok let's see..

a) 50% of GDP is from energy, and rest is supposibly from employee's effort,

b) at least 50% of all energy is coal, oil, NG (hydrocarbons)

does this mean that if price of energy triples, inflation goes 200% ?

is it so that if price of OIL goes 5 or 6-fold, the price of energy (approximately) triples?

in 7 years of time this approximately means that inflation could be

10% yearly, on average of course.

c) price elasticity of oil is 0.2 (??):

if supply gap is 5% the price of oil quadruples

hmm, what about this assumption:

d) if the supply gap goes like this:

2007: 0% (assumed that OPEC can sell its 2mbarrel of heavy oil (or whatever) = so called "spare capacity")

2008: 1%

2009: 2%

2010: 3%

2011: 4%

2012: 5%

2013: 6%

2014: 7% price of oil is 6 times more than in 2007, 450 $ / barrel.

This d) was based on growing population, which needs at least 1% more oil

(world population grows something like 1% yearly). It is also assumed that

depletion is managed by somehow, water injection / biofuels etc. so that the supply

can be at the same level all a time (surely it cannot be increased but maybe the same level

can be sustained).

Does this mean that we are going to have at least 10% inflation (yearly)

on average?

What It could be on year-on-year basis?

I cant calculate the level of inflation for 2008 if supply gap is 1% ??

Is there limit for the price of oil? I mean... there are not so many substitutes in large scale.

What about coal-to-liquids, I read somewhere it can be produced economically viably if

the price of barrel is ~ 50 $ per barrel?

(and yes, I admit: these are most positive assumptions you can get!!)

greets,

telkola

------------------

...change of the world as we know it

.

Thanks a lot Jean it's an honor to get good info from you

I appreciate your diffidence about the rubbery nature of the coal figures , the picture should be clearer in a few years time when oil and gas will be in decline .

You seems to share the distrust of what I call the fallacy of accuracy

I care little for the timing of peak , but worry a lot about the rate of the energy down slope,

I consider energy to be the greatest influence on human lifestyle ,

If we had the energy usage of the 1950 we would have the lifestyle of the 50ies ,

if the energy consumption of the 1850ies we would have the human rights of the 1850ies

if the power usage of the roman empire we would have the industrial relations of the roman empire.

if you want to imagine the lifestyle on renewable only , it's about 1700 ! 90% of the population is farmers , a few cities break the million mark

the population then was 0.5 billions , the population soon will be 7 billions ,

our increase in population and lifestyle is our increase in power consumption

the downward adjustment would follow the slope of the energy decline ,

imagine the great depression , every two years , again and again relentlessly for a century

most societies would crack or be brutalized by it

There is no solution

.

memmel

There are 2 Peaks

1. The real energy peak

2. The time prior to that when it becomes apparent.

We are living at about the time of the second noted = hence Cheney and his invasion of Middle East to secure their oil.

The result is exactly as sparky points out, which in itself reflects the comments by Jean about thcon flict between the energy component of the GDP (whatever the hell that is) and the enrgy componenet of the Consumer Price Index (whatever the hell that is).

At (or about) current energy consumption the world is too small for the population.

The result must be a decline in population the slope of which will reflect both the decline in energy usage with a bumpy ride down - natural disasters, wars, famine.

Maybe the reduction in Black Sea oil exports noted elsewhere is, in a way a tiny straw in the wind, as Russia / Putin and the silovaki decide that as wise virgins they should keep a little bit in the cupboard.

you are asking the right questions:

1. what really is energy component of GDP ?

--> this we know from the interview, it affects 50%

2. how price of energy (or lack of energy) affects CPI ?

--> is it the same 50% ?? if energy prices triples, CPI doubles? Please notice that not all energy comes from hydrocarbons, and energy mix varies; it is different in different countries

I want to add one more:

3. how big inflation is sustainable / bearable ?

--> 10% or slightly more is not unknown in western countries

these are actually interesting from the practical point of view. If we can somehow conclude that when the inflation or CPI starts to surge, we can ready ourselves for it.

There are some countries suffering inflation levels like 1000% and more.. they are completely in chaos, check out Mugabe's country!! but still, people are still living there!

(but lacking everything, even basic supplies)

---------------------

...change of the world as we know it

Your on the right track.

But what no one is looking at is how this effects the energy industry itself. Its probably our largest industry and is a heavy energy user. So you can expect the issues you have outlined to have a negative impact on the energy industry. And of course outright shortages which in my opinion cause the most damage.

I see a energy industry that is far from ready to deal with the problems of expensive/scarce energy and this will ensure that they will be unable to extract fossil fuels at the depletion limit.

In fact this breakdown of the energy industry itself will it seems have a huge impact on the production rates shortly after we enter a high price/shortage regime.

In general most of our base industries will be heavily impacted but its energy in particular that has me concerned since problems in the energy industry because of expensive/scarce energy supplies leads to a slow down in production and ....

Do we have examples of a base industry that was critically dependent on its own product and how this worked out during depletion ?

Whale Oil does not work since it was not needed by the Whaling ships and they could also produce themselves.

The closest I can think of is famine or a army running out of bullets and these simply lead to disaster. But you can see why I'm very concerned about the ability of the energy industry to function effectively as we move down the peak oil slope.

sounds pretty right that there would be many recessions, maybe you meant that after every supply crunch there is crisis again and again.

of course this facilitiates inventions for better energy solutions. Recessions can work technology drivers. But im worrying that these "energy inventions" will be like "buying cheap labour from 3rd world country to work in very dangerous coal mines for us", which would be, kinda modern-day-equivalent of slavery.

or how this "invention" sounds:

"attacking our neighbour country which has more energy

resources than we do"

:O

I do think there is a solution: some kind of high technology will save us! but supposedly it takes decades to achieve that (fusion energy? nano-tech?). This is what history teaches us, how we moved from steam to electrical energy etc. The shift needed a recession and world war I..

-------------------

...change of the world as we know it

We're trying to look at the future of electric energy in New Mexico and coal source dependence on oil and rail transport.

http://www.prosefights.org/pnmelectric/pnmelectric.htm

Re: NG

USA production and consumption recent peak was 2003. 2004 was down due to declining production, with hurricane effects added in 2005. 2007 production is up but not back to 2003 level, imports from Canada are down, and LNG imports are up but not enough to make up for Canadian decline. Active drilling rigs in USA were just over 1100 in late 2002 and near 2800 today. This huge increase in drilling has not quite kept pace with decline of existing production. Further increases in drilling are not possible due to lack of rigs. The fleet is near full occupation. LNG imports can't increase much due to lack of available shipping capacity, now worsened by the Japan earthquake temporarily shutting down their largest nuke facility and increasing their NG demand. Canada supply is likely to be down 10%+ y-o-y in Q4, and we apparently haven't yet hit the cliff implied by J. Laherrere's shifted discovery curve. Demand growth has been held in check for 3 years by amazingly clement weather in the main consuming regions. Supply collapse could happen at any time. NG will be the big energy wake-up call in the USA. Murray

The graph implies cliff/collapse to me also, even though Chesapeake Energy (disclosure: I own some stock) by itself has 80 Tcf of natural gas -- enough for about 4 years US gas consumption.

DMZ

Memmel- Imagine trying to plan a project like the Alaska gas Pipeline. Even if the contracts were signed today, it would be ten years before the gas would flow. The Alaska gas pipeline must compete with nuclear power which also has a long "POP" (put on production) time. How can investers perceive future material costs in the light of diminishing energy resources?

I don't think Nuclear is the issue its the destruction of the American middle class or at least the suburban/suv lifestyle that will cause big oil to have problems investing long term.

Demand will start going down. And price although probably high will fluctuate a lot. I think it will tip over to a big desire to move off oil not sure at that point if we can but I can't see people making expensive long term investments with 25% or more of the market at risk.

I think in 2008 you will see a rash of projects stopped because of funding fears and all kinds of logistic problems along with massive cost overruns just managing existing fields.

In my opinion the oil industry is not prepared for peak oil and will suffer especially big oil private and national.

By 2010/2011 I actually expect the oil industry to be in a major upheaval. I think the smaller companies will make out well but the big companies and national oil companies will have serious problems with spiraling costs and will be fighting to keep production up in existing fields forget about large new projects. On the political side it will be very ugly since they all claim with money they can do anything and when they don't deliver ...

Couple this with export land and we can expect production and exports to drop sharply starting in about 2010.

And of course countries like the US with a large internal production will probably see the investment and logistic problems cause increases in decline rates. The point is that although demand destruction from a foundering economy will probably decrease demand the combination of export land plus internal oil industry issues will ensure that the price of oil and extraction costs will increase.

It would be neat if Laherrere would post his natural gas discovery data without the moving average applied.