| PowerSwitch Event: Peak Speak 3 (UK) | The Oil Drum: Europe | British MP interviews David Strahan, author "The Last Oil Shock" |

Oilwatch Monthly - July 2007

Posted by Rembrandt on July 16, 2007 - 9:50am in The Oil Drum: Europe

The July edition of Oilwatch Monthly can be downloaded at this weblink (PDF, 1.15 MB, 16 pp).

Latest developments:

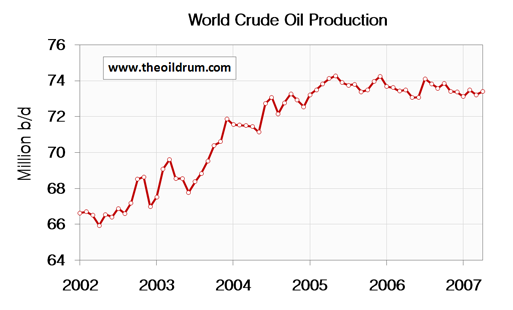

1) Crude oil - Production of crude oil increased by 181,000 b/d from March to April. Total production in April was estimated at 73.40 million b/d by the Energy Information Administration (EIA), which is 850,000 b/d lower than all time high crude oil production of 74.25 million b/d reached in December 2005.

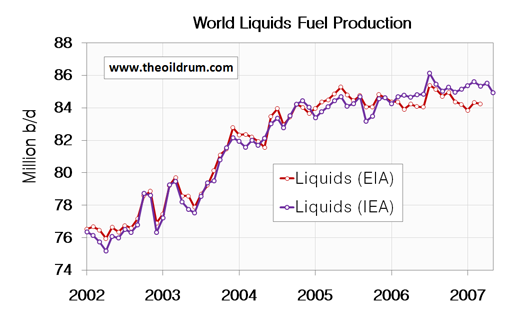

2) Total Liquids - Production of all Liquid fuels decreased by 560,000 barrels per day in May from April according to the latest figures of the International Energy Agency (IEA). Resulting in total world liquids production of 84.94 million b/d, which is 136,000 b/d higher year on year from May 2006 to May 2007 but 1.17 million b/d lower than all time maximum liquids production of 86.11 million b/d reached in July 2006.

3) OPEC - Total crude oil production of the OPEC cartel decreased by 420,000 b/d to a level of 30.07 million b/d, from April to May, according to the latest estimates of the IEA. Preliminary figures from the EIA show a further decrease of 120,000 b/d from May to June resulting in OPEC crude production of 29.94 million b/d. Since July 2006 production from the OPEC cartel has declined with 1.2 million b/d.

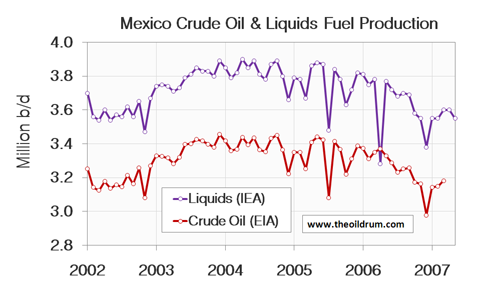

4) Non-OPEC - Total liquids production of non-OPEC decreased by 150,000 b/d, from April to May, according to the latest figures of the IEA. Production has dropped from 50.57 million b/d in February to 50.09 million b/d in May. Large production decreases in that period came from Canada, Norway, the United Kingdom and Norway of in total 630.000 b/d. Production in other countries remained relatively stable. The decline in Mexican production has halted for now, staying near 3.55 mb/d since January.

A selection of charts from this edition:

P.S. I still have to incorporate some of the promised changes from last month. I intend to do so as soon as possible. A definite format for the newsletter is still being found at this stage. All suggestions for additional analysis and data inclusion next to liquids/crude oil production, stock and export data will be taken into consideration.

Personnel

Editors

Contributors

Peak Oil Primers

Archives

- November 2010 (3)

- October 2010 (6)

- September 2010 (4)

- August 2010 (7)

- July 2010 (6)

- June 2010 (7)

- May 2010 (2)

- April 2010 (8)

- March 2010 (4)

- February 2010 (6)

- January 2010 (3)

- December 2009 (5)

- November 2009 (8)

- October 2009 (12)

- September 2009 (6)

- August 2009 (5)

- July 2009 (11)

- June 2009 (8)

- May 2009 (16)

- April 2009 (10)

- March 2009 (7)

- February 2009 (10)

- January 2009 (15)

- December 2008 (9)

- November 2008 (9)

- October 2008 (9)

- September 2008 (13)

- August 2008 (10)

- July 2008 (14)

- June 2008 (23)

- May 2008 (16)

- April 2008 (12)

- March 2008 (16)

- February 2008 (9)

- January 2008 (13)

- December 2007 (13)

- November 2007 (16)

- October 2007 (22)

- September 2007 (8)

- August 2007 (9)

- July 2007 (16)

- June 2007 (8)

- May 2007 (7)

- April 2007 (7)

- March 2007 (10)

- February 2007 (10)

- January 2007 (12)

- December 2006 (9)

- November 2006 (15)

- October 2006 (4)

- September 2006 (5)

- August 2006 (5)

- July 2006 (9)

- June 2006 (5)

- May 2006 (10)

- April 2006 (9)

- March 2006 (13)

Vital Trivia

License

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.

Dear Rembrandt

Thanks for another fine post.

Nice to see all data together :-)

Especially the Export part is interesting.

One question. Why are the IEA figures almost always higher than the EIA figures. Is it based in definitions, methodology or?

One point

Fig. 5 Saudi... in your post above has world graph inserted?

kind regards/And1

Sorry, fixed the Saudi graph.

Thanks Chris, my error

Please note the flat production 'again' in KSA. Are you seeing this WT?

So is Mexico so therefore everything will be all right whew.

And I thought their biggest field was in terminal decline.

This is not correct. Oil production by PEMEX was down 70,000 barrels per day in May. The first figure below is All Liquids, the second is Crude.

April 3,603... 3,182

May.. 3,523... 3,110

http://www.pemex.com/files/dcpe/eprohidro_ing.pdf

A new report is due out next Monday the 23rd.

The EIA always uses these exact figures put out by PEMEX, however the IEA often ignores what PEMEX says and puts out their own idea of what they think Mexico produces. I suppose they may put them out before PEMEX does and that is why they are sometimes wrong. But Pemex has had these figures out since June 21st.

Ron Patterson

Interesting, the IEA and EIA indeed put out a higher figure.

The IEA put out a higher figure but the EIA put out the exact figure PEMEX gave for march and April, 3,182,000 bp/d, for both months. If you check the second column in the PEMEX report, (total crude), they are the exact figures reported by the EIA, month after month, going all the way back as far as the report goes.

EIA Mexico

http://www.eia.doe.gov/emeu/ipsr/t11b.xls

PEMEX

http://www.pemex.com/files/dcpe/eprohidro_ing.pdf

Ron Patterson

The flow rates are controlled at the wellhead. Yes they can probably open the taps but at what cost? They are managing their reserves very well and are very conscious to minimise water breakthrough. If production is flat at $75 you can be damn sure they are doing everthing they can to even maintain production and it is an heroic effort.

Marco.

Party Guy,

As we discussed the other day, the decline rate in post peak regions is net. If we look at production on an annual basis, the difference would be:

Last year's production - Declines from existing wells + Increases from workovers/pressure maintenance + New wells = New Annual production rate.

On an annual basis, post-peak regions can show, and have shown, increases in production. What do the following regions have in common: Texas; Lower 48; Total US; North Sea; Russia; Saudi Arabia; Mexico and now the world (crude oil)?

Answer: all of them have shown production peaks that are broadly consistent with their HL models (Texas and Saudi Arabia, as swing producers, peaked at later stages of depletion). Also, many of them have shown production increases post-peak, albeit to production levels below their peak levels.

So, get back to me when Saudi Arabia shows an annual crude oil production rate of 9.6 mbpd or more.

In Saudi Arabia and in virtually every net oil exporting country in the world, flat production = declining oil exports.

BTW, recall the discussions of Saudi Arabia looking into importing coal? Let's see, what would they do after they start importing coal?

http://www.upi.com/Energy/Briefing/2007/07/12/saudi_arabia_invests_in_re...

Saudi Arabia invests in renewables

Published: July 12, 2007 at 5:21 PM

Good morning!

The difference between IEA and EIA figures for Crude Oil results probably because they are handling huge global statistics. They probably have somewhat different sources for the more difficult countries. These result in differences for some countries/regions mainly in the last few months. There are often revisions that close the gap between these differences.

So I would guess it's an occupational hazard

--

It's quite interesting to see what's going on, for instance with the US actually increasing production. A trend that will likely continue in the 2nd half if the Hurricane season is a mild one. They have planned to bring the Tahiti field onstream in that period (200,000 barrels per day).

Tahiti was scheduled to come on stream in 2008.

Thunderhorse 250,000 barrels a day and

Atlantis 200,000 barrels a day in the GOM are also delayed.

BP was having problems with the Mad Dog subsalt deep production and "highly mobile tar deposits" at nearly 22,000 feet of total depth. The field is shut in.

Smaller offshore fields peaked and declined much faster than some of what the previous generation was finding to replace production with. Of course there is much new technology, more rigs available, and all sorts of laws and restrictions, in other places lawlessness, to add to the dilemma of predicting the future.

Peak oil will come if it has not already passed. Heavy oil production seems to be a separate foot hill or peak forming.

U.S. average daily crude oil production for the first half of 2007 exceeded crude oil production over 2006 (EIA weekly petroleum report).

per your charts, the difference is non opec, and began late 2006, so perhaps could be isolated. Prior to this eia/iea were in pretty good agreement, so it should be possible to locate what countries are causing the recent divergence.

Looks a bit like plateau to me, the people who deny peak oil don't seem to see any problem with a plateau, but it makes us very sensitive to any outside factor. Good job our economy and environment are so stable :S

I can't see the right side of the graphs which show 2006 and 2007. Is there a way to make a click-on enlargement?

Done.

Thank you!

Would it be appropriate to include a smaller graph of Russian production over a longer time span? (ie 1960-2000?)

Just to give some perspective that russia used to produce 11 Mboe/day?

Large production decreases in that period came from Canada, Norway, the United Kingdom and Norway of in total 630.000 b/d.

Can you confirm that Canadian liquids production do not account for synthetic crudes? And would a Canadians synthetic crude production graph be appropriate?

You can spot the difference partially in the divergence between crude oil and all liquids in the Canada graph. However, the IEA and EIA have since a year or so been counting a part of the synthetic crude as convention oil, making it impossible to separate both streams very well.

The drop in Canadian Crude is most likely due to maintenance of synthetic crude.

Note that the EIA shows that the average annual increase in Canadian net exports (Total Liquids) from 2000 to 2006 has averaged only 60,000 bpd per year.

Based on current data, it would take the average year over year increases in net exports from two producing regions like Canada just to meet the current annual rate of increase in domestic Saudi consumption.

And the "Iron Triangle" continues to advise us to "Party On."

glad im in canada, until we get annexed by the crapper beneath us.

my plan is to take to the hills and hunt Americans in the event of invasion (real or country combining).

We don't want your steenking country. Just your oil and your natural gas and your hydropower. And your water.

I've found that the IEA can be slow in compiling all the production data. I go to the source for russian, norwegion, UK and Mexican production stats. I assume you have the websites for these?

Not for Russia,

which website is that?

Rembrandt

the best I found for russian oil production is the Russian News and Information Agency @ en.rian.ru. Search on "russia oil output" and you'll get the latest news bulletins, along with some extra hits. The news title usually starts as "oil output in russia...". Hope this helps

Thanks! very helpful

Well, it does look like that anticipated flood of oil arrived - shame that it happened on a still ebbing tide, and ended up looking a lot more like an oversized swell while the muddy bottom keeps getting clearer.

Yes and I'm actually doubtful about the numbers. The price of oil has risen strongly over the summer yet production has been fairly constant was the summer driving season in the US sufficient to increase prices like it has. And if so why are they higher in Europe and Asia.

This indicates that WT Export Land/Bidding war may be playing a role.

In any case to me the recent price increases don't fit with these production numbers.

I do have a partial/plausible theory about recent price rises - hurricane season is upon us.

And if you are the gambling type, it is hard to know what will happen - 2005 and 2006 are a study in stark contrast.

2006 was likely atypical, from an insurance company perspective, but then, so was 2005.

Uncertainty tends to drive prices higher.

But this is only a partial explanation - it certainly doesn't cover the entire recent rise in price levels.

Could well be I'm sure its a lot of factors the point is the market is painting a situation that differs from that pointed at by only considering overall supply. Thus we can consider overall supply to be a lagging indicator of the real situation for the global oil supply.

As far as hurricanes go the US market has been well supplied with oil and indeed the price of oil is depressed in the US market while the rest of the worlds benchmarks are diverging to the higher end. So I think the hurricane issue is covered and in general that more of a refinery issue than a oil supply issue. Storing a lot of oil does little good if you don't have the refining capacity. So sure it adds some pressure but in general I think hurricane effects are dependent on the exact nature of the event and generally occur after the full extent of the damage caused by a particular hurricane is assessed.

Its I'm sure a very complex relationship but it seems that unless oil supplies actually increase substantially other factors are in control of the actual price of crude with effectively flat oil supplies.

The problem of course is we don't know how these factors will influence price once we start seeing actual declines in oil supply since we in effect no longer know whats controlling price.

ELM of course points to a dire outcome and so far in my opinion the market is supporting something like ELM controlling prices.

I've said a few hundred times once oil peaks globally models based on geologic decline are not valid post peak other factors will drive the real oil markets with geologic decline a best case scenario. So yes geologic decline is underlying our problems its simply not the controlling factor and these models may be very optimistic as we pass global peak.

To the extent geologic decline can be considered the upper limit, you're right - a sort of top down way to view maximum production values, as compared to a bottom up analysis to determine production increases.

The complexity is daunting, and we are starting to enter new territory.

One thing I find interesting, for example, is how fuel is currently being distributed in the U.S. - areas running short of fuel are also areas where food is grown - and yet, the market feels that ensuring enough fuel for Wal-mart and hedge fund managers' jets is a valid use as determined by price.

I'm not sure how this figures into a broader picture, but even minor disruptions in the Midwest may have major impact in ways all too clear, always somehow remaining beyond resolution.

And yet, a reasonable person could say such problems have nothing to do with peak oil per se, just with the price of fuel.

I think our vocabulary and perspectives will require a lot of adapting. In part, this is a responce to an earlier point - I too think the numbers have been growing intentionally murkier for a while, helping prevent a clear discussion of what is going on. Call it the haze at the peak.

Its just a complex system suffering catastrophic failure. We actually understand the dynamics quite well just are unwilling I think to apply them to the oil economy.

In a sense we are in a unique position similar to Romans as the Roman empire fell I'm sure more than a few understood why the empire was crumbling and even figured out ways to stop and even reverse the decline. In the end the empire still fell. The oil age will end much faster than the Roman Empire but its crumbling is certain.

In a way its driven by a corollary of Jevon's Paradox. In a supply constrained situation no one is willing to give up short term economic advantage for long term gains by moving off oil. Norway and the EU as notable exceptions. We would rather eat the golden goose than share the eggs.

The sad part is everyone will focus on the increasing failures of the oil industry and economy and never realize or accept the real cause depletion. And on the other hand a lot of people that track the underlying geologic peak will not accept that it will be soon overridden by these same above ground factors having served its purpose and initiated the failure modes of the system.

As far as I know, we had hurricanes in

2005 at 60 a barrel

2004 at 45 a barrel

2003 at 30 a barrel

2002 at 25 a barrel

Doesn't seem like there has been much correlation between hurricane frequency and oil prices, especially with all that spare OPEC capacity waiting to be tapped.

I do know what you're referring to, though. The August contract expires I think Friday, but for sure by Monday at the latest( I forget which way it rolls when the 22 is on a weekend). It was the August expiration last year when prices gapped downward. Assuming no hurricanes by Monday, this should be a good price barometer coming up. If it stays high, it's about supply.

@Memmel

Strange I would interpret the recent price rises as being in accordance with production numbers. Production is hardly rising while we want demand to go up, seems as a good explanation to me?

Looking at the currency market the actual cause for the recent price increases are probably simply a result of the falling dollar it does not look like we are seeing much of a price increase in other currencies.

Next production has been flat for a long time but in the past the world did not use all the production capacity all the time demand is not constant what I think is happening is production is moving toward full capacity all the time to make up for increasing demand once this does not work and enough regions draw down reserves then we will see real price increases.

I think this condition finally arrives this fall.

Thanks Rembrant.

A very minor point, EIA has peak production of crude oil in May, 2005 at 74.272 MB/Day their December 2005 production figure was 74.253.

The big picture is looking more and more ominous.

According to the EIA the all time high in Crude oil production was May of 2005.

May 2005, 74.272 mb/d

Dec 2005, 74,253 mb/d

http://www.eia.doe.gov/emeu/ipsr/t11d.xls

Ron Patterson

Missed that one, thanks for the keenness.

These values were revised last month for 2005 and now the IPM and the MER from the EIA (I'm speaking in acronyms, oh my!) now reflect the same values and should be considered final for 2005.

Fantastic work Rembrandt, thanks alot. The report has some very very interesting information in it now! I think the current format is great (and I think the addition of OPEC quotas will be very useful in future :-) )

Cuchulainn

I really like your graphs. They are nice and clear.

A couple of minor comments- I take it that world crude production in Figure 2 is based on EIA data. You might label it as such.

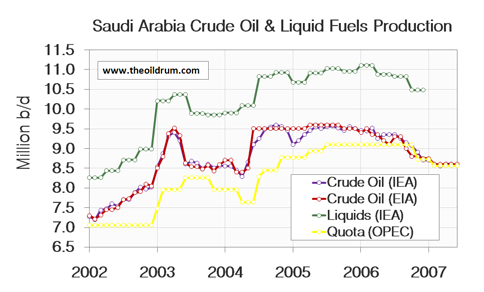

On Figure 3, it lookes to me like the OPEC data ends at May, not June.

I think these graphs are a really good idea. It will be interesting to see what the data looks like when the IAE data through June with the big drop in the second quarter comes through.

I have a question on OPEC quotas. The yellow line on the graph is presumably the amount they are allowed to produce by agreement? According to that, Figure 5 above (Chart 21 in the pdf) suggests that KSA has sat exactly on the quota line for the past year as the quota has dropped, implying declining production is merely them adhering strictly to their quota. I'm curious if this is really the case though, Other countries like Kuwait appear to be way above their quota and ignoring the recent decline required of them. Does that mean they are cheating on their quota? I'd be surprised if it would be that transparent.

Anyway, I'm just curious what this all means, as a relative newcomer to this site. Thanks for any information.

I noticed that too. Truth be told I sincerely hope that they decided to get their production in line with their Quota. There are 2 possibilities:

1) KSA believes there is enough oil on the market that they are easing off the taps to stay in line with their quota. In theory, able to boost output to over 9.5 mbpd when the need arises, while allowing some wells to rest.

2) KSA has been battling relentless watercut and precipitous decline rates in their aging fields. Despite bringing new megaprojects onstream, KSA is doing everything possible to mitigate declines and opts to hover at the Quota line to mask the deline rates and pressure their quota output downward to appear that nothing unusual is going on. No crash here, merely thrifty stewardship of our well heads.

The only way we will know for sure is with the movement of time. If they are experiencing serious declines it would make sense to drop output as much as possible without alarming the world in an effort to ease back the fields and dig more wells.

Out of all the data circulating I am watching what KSA does. But, like you, I am new to a lot of this and I would like some feedback as well.

TOD has a tough time predicting SA future production, tho many try, not least Stuart. Presumably SA could and does do a better job. Current quotas are relatively recent, first agreement was in oct for nov, then around dec for feb. One might assume SA could guess their max production at least thru 07, their accuracy no doubt aided by the decline that had already become well established during the months leading up to the Oct agrement. A good question is, 'did the second agreement for cuts, leading to the Feb level, come about as a result of continued price weakness, or did it come about because SA quickly realized that their Oct guess for 07 production was too high?'

Quotas are set by agreement... but, in this case, SA, with 30% of opec production, has heroically agreed to shoulder 80% of opec implemented cuts. One might imagine that other countries would happily agree with SA to allow them to cut their production by 1Mb/d. There is nothing magic about SA following the opec agreed cuts given their prime position in establishing the quotas, and no clear indication that any of these cuts are voluntary.

Crude markets are, by normal measures of OECD stocks, well supplied, just as SA often says. But IEA and others are seeing higher demand 2h07 along with stagnant non-opec production, the latter a big surprise to many, not least iea/eia, expecting a non-opec wall of oil some time ago that has yet to arrive. It could be that higher prices this month are simply buyers paying attention to supply and demand predictions, in which case the market is performing exactly as one would expect.

TOday oil and the broad market are both up a further bit, but oil shares are down sharply. The market, logical or not, does exactly what it wants to do. Imo investors outperform traders, and sleep better too.

Although this is a somewhat flawed analysis, it is good that OPEC’s role in Saudi Arabian production is at least finally being discussed.

It was first discussed here in the comments section:

http://www.econbrowser.com/archives/2007/07/iea_becomes_mor.html

Saudi Arabia’s cuts are proportionate to their share of the total OPEC quota which has been a constant 32.5% over the last several years, not due to any heroics. Am I correct in guessing that you were being sarcastic?

While the view that Saudi cuts were not voluntary is quite popular here, it is basically non-existent in the rest of the world. In fact, the situation is the exact opposite of what you say. There is no proof or evidence that they are anything but voluntary.

Why would one need to imagine? What could be better than to have another member shoulder the burden while you reap the benefits of the higher prices?

The second cuts were pushed because it was obvious after the first round that the others members were lacking in compliance, pushing up the numbers an extra 500,000 barrels seems to have worked slightly better. The original compliance level would not have achieved the desired price floor. In fact compliance(other than Saudi Arabia which is at 100%) is only 60 or 65%. The second part of your sentence suggests a conspiracy which you will need to outline in greater detail before it can be discussed adequately. Is it possible, yes, but very hard to keep a secret for more than a few months. By September 11th when OPEC meets next and probably the earliest the 8.6 mbpd level changes, it will be 8 months of perfectly level production at the quota level. It is starting to look like a very strange terminal decline.

Sunset over Weyburn Oilfield -- royalty free stock photo

OPEC reported falling world oil production for June 2007

Page 40

Looks like bad news for summer driving.

That link doesn't seem to work. Is this one the one?

http://www.opec.org/home/Monthly%20Oil%20Market%20Reports/2007/pdf/MR072...

Ron Patterson

I don't get it. It can feel very safe reading that OPEC june report. I suppose that is the point...

Summary: All is well, we have all you will ever need, move along.

A lot of that report talks about more transparency yet they wont let anyone verify their production data or the health of their fields.

Question 1: Is this typical OPEC language?

Question 2: Is this all stock market pleasing BS?

Question 3: Do you really think they have grown spare capacity by 15%?

Part of me really wants to believe that they have it all figured out and that us worry warts are a pesky fringe minority.

Don't get me wrong, I am not hoping they are wrong, but it would help me sleep better at night if they are being honest. Hell I would sleep better at night if they openly said we are running out of oil. Then it would not be smoke and mirrors anymore and I can say: "ok, this is the real deal, time to redouble efforts in personal preparation"

I read the report every month, but not for the oil numbers as they only use 3rd party sources for their numbers. (Isn't that a hoot?)

Anyway, their economics team is the best in the world in my opinion. Their models regarding worldwide economic activities are just right on the money every month.

Too bad the OPEC report doesn't actually report on OPEC.

From the PDF:

Back down in the 83mbpd range? This is a rather ominous announcement.

Ghawar Is Dying as we slide Into the Grey Zone

"The greatest shortcoming of the human race is our inability to understand the exponential function.

me and my friends are flying down to california.

its going to be a wowzor of a trip.

airfares are 370 $CD and then jump to 1500+ $CD for a one way ticket. (remember than Canbucks will reach parity with American prob by the end of the year. possibly even sooner)

we are driving back up to the great land of Canada, i didn't tell my friends my unofficial name for the trip, "last visit to rome before the fall" and probably won't.

Rembrandt, a stunningly interesting collection of info. Thanks.

I do wonder if more exploration of the OECD forward supply might be in order. Your PDF states:

{obvious}But crude is the [main] feedstock for product,{/obvious}, so the forward supply for all stocks is of much more import than just the days of crude available.

So from page 1 of http://omrpublic.iea.org/currentissues/full.pdf -- or some other link if one's prepared to pay for the not-out-of-date-version -- we get:

But much more interesting... MUCH more interesting, is the graph at he bottom of page 29 of the PDF, which shows that 'flat' in this case is a result of rounding (top of p28), and actually, OECD total stocks in terms of forward-supply have been declining remarkably linearly for the first few months of 2007, quite contrary to the average historic trend.

In the context of Export Lands, does this deserve a bit more coverage? (and can anyone tell me if the trend continues in the most recent [paid] version of the IEA report?)

--

Jaymax

Great post, thanks so much!

Two additional things I think we would all benefit from seeing compiled and posted on a monthly basis - either as a part of your work or by someone else:

1) Data on oil exports by exporting country and globally. Given WT's ELM model, it is really important to start monitoring this.

2) Crude oil price trends, not just in US$ but also in Euros, Yens, & Pounds (and maybe some weighted global currency index?) Lots of discussion wrt what extent oil price increases are just an artifact of US$ depreciation vs. something real.