The Round-Up: June 29th 2007

Posted by Stoneleigh on June 29, 2007 - 9:24am in The Oil Drum: Canada

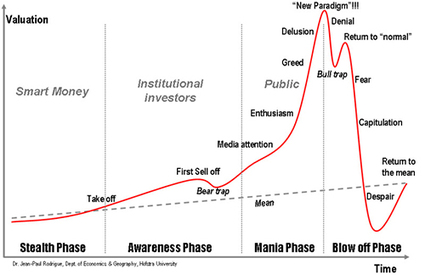

The following applies not just to housing, but in many ways to credit bubbles in general. IMO we should expect to see graphs like the one below across a wide range of asset classes in the not too distant future.

Houses Should Not Be a Commodity

There are technical reasons for a market crash (foreclosures, credit tightening, etc.) and I have discussed those in great detail in earlier analysis posts; however, market psychology plays a large roll in how and why it all plays out. The technical factors cause shifts in psychology among the market participants which exacerbate market moves. Today I will examine the psychology of market bubbles drawing parallels between the commodity futures market and the real estate market. In this post want to clearly illustrate how and why the psychology of market participants will facilitate the ongoing price crash.

Video: Money As Debt (highly recommended)

Looking for Contagion in All the Wrong Places

The right places to look for contagion are therefore not in the white-washed Bear Stearns hedge funds, but in the subprime resets to come and the ultimate effect they will have on the prices of homes the collateral thats so critical in this asset-backed, and therefore interest-sensitive financed-based economy of 2007 and beyond. If delinquencies lead to defaults and then to lower home prices, then we have problems and the potential for an extended not a 27-day Paris Hilton sentence....

....Importantly, as well, and this point is neglected by most pundits, the willingness to extend credit in other areas high yield, bank loans, and even certain segments of the AAA asset-backed commercial paper market should feel the cooling Arctic winds of a liquidity constriction.

The sub-slime that ate Wall Street

The crux of the problem: Mortgage-backed CDO securities aren't traded very often, so determining their true value is difficult at any given moment. But as long as everyone pretends together, no worries! If you want to know why Wall Street has been obsessed with the saga of two Bear-Stearns hedge funds for the past two weeks, there's your answer. When the reality that the Bear Sterns hedge funds were hemorrhaging cash became impossible to turn a blind eye to, a dreaded scenario began to emerge. In order to pay off anxious investors demanding their money back, Bear Stearns might have been forced to auction off all the assets owned by its hedge funds.

But that would have exposed the CDO Emperor's new clothes! A price tag would have been placed on sub-prime mortgage backed CDO securities, and the feeling on the Street is that it would have been a bargain basement number. That means that everyone else who owned such "financial products" would have to strongly consider revaluing their portfolios to reflect actual market conditions, rather than their own optimistic fantasies.

The number one domino that would fall from any such revaluation on a large scale would be liquidity -- the access to cheap credit -- that keeps the wheels of the global financial system greased and rolling. All those private equity buyouts of publicly traded corporations that have been keeping the stock market rolling for the past few years depend on cheap access to finance to pull off their deals. Already, there are strong signs that the great buyout boom of the early 21st century is beginning to peter out.

A real credit crunch would be a very big deal. It might even be the "systemic shock" that critics of derivatives trading have been warning against for what feels like a generation.

Investors fear Bear Stearns flu

The funds invested in securities that are extremely complex and trade infrequently, making it

difficult to know what they are worth. Most firms value them using mathematical models rather than actual trading prices.

Early this year, as subprime loans started defaulting sooner and in greater numbers than expected, Bear Stearns was forced to write down the value of securities in its portfolio. That caused some investors to start pulling money out of the fund. It also caused lenders to start issuing margin calls. In a margin call, a lender tells the borrower to either put up more capital or it will start selling the assets that back the loan.In May, Bear Stearns started selling billions of dollars worth of the fund's higher-grade mortgage securities to meet redemptions and margin calls. But it wasn't enough. On June 14, Merrill reportedly prepared to seize and sell $400 million worth of collateral. If other lenders followed suit, the two funds probably would have to shut down. Even more worrisome: If Merrill sold its collateral, which was mostly lower-quality mortgage securities, and they brought in less than expected, other hedge funds might have to write down the

value of mortgage securities in their portfolios, sparking more investor redemptions and margin calls."No one wanted to see the securities liquidated because they're not sure what kind of bid is out there. If it's really awful ... you get a tsunami effect," says Jim Midanek, chief investment officer with Black Pearl Asset Management.

How Successful Will the SEC Investigations of CDOs and Bear Hedge Funds Be?

“If there is contagion, the problem certainly has sufficient scale to become a financial event,” he said.

Bear Stearns closed 0.2 per cent higher at $139.35 on Tuesday but the stock has fallen 14.4 per cent this year.

John Nestor, a spokesman at the SEC, said: “Because they are bank instruments, there is increased co-operation [between regulators] as we examine these things.”

The worries over subprime exposure on Wall Street have rattled stocks and sparked safe-option buying of short-dated government bonds. Volatility has been rising and corporate bonds have weakened in value.

David Ader, strategist at RBS Greenwich Capital, said: “The CDO worries have progressed to the regulatory level.

“Although it is unclear which firms will be directly impacted by the investigation, one thing does logically follow, this month/quarter-end will see a push toward accurate marks on these assets given the increased regulatory scrutiny.”

Banks 'set to call in a swathe of loans'

The United States faces a severe credit crunch as mounting losses on risky forms of debt catch up with the banks and force them to curb lending and call in existing loans, according to a report by Lombard Street Research.

The group said the fast-moving crisis at two Bear Stearns hedge funds had exposed the underlying rot in the US sub-prime mortgage market, and the vast nexus of collateralised debt obligations known as CDOs.

"Excess liquidity in the global system will be slashed," it said. "Banks' capital is about to be decimated, which will require calling in a swathe of loans. This is going to aggravate the US hard landing."

Charles Dumas, the group's global strategist, said the failed auction of assets seized from one of the Bear Stearns funds by Merrill Lynch had revealed the dark secret of the CDO debt market. The sale had to be called off after buyers took just $200m of the $850m mix.

MISC Postpones Bond Sale on `Market Volatility'

MISC Bhd., the world's biggest owner of liquefied natural gas tankers, postponed a planned dollar- denominated bond sale because of fluctuations in debt yields sparked by losses linked to U.S. subprime mortgages.

Kuala Lumpur-based MISC, a unit of Malaysian state-owned oil company Petroliam Nasional Bhd., hired Citigroup Inc. and Deutsche Bank AG to sell $750 million of 10-year bonds, an e-mail sent to investors earlier this week showed.

"Given the current market volatility, MISC has decided to put their transaction on hold pending more stable market conditions," according to an e-mail sent to investors today by one of the sale's arrangers.

Investors have increased their aversion to riskier investments on concern that losses at two hedge funds run by Bear Stearns Cos. could become more widespread. Credit-default swaps based on $10 million of debt included in the iTraxx Asia ex-Japan Index of 50 companies jumped to $15,750 yesterday, from $10,750 a week ago, according to Morgan Stanley.

"Increased event risk has caused some paring of risky asset positions and some bond issues have been pulled in this hostile climate," said Tim Condon, head of research for Asia at ING Groep NV in Singapore.

Carlyle Postpones $415 Million IPO of Mortgage Fund

Carlyle Group, the buyout firm run by David Rubenstein, postponed a planned $415 million initial public offering of a fund that invests in bonds backed by mortgages after a slump in the U.S. subprime market.

Carlyle is preparing a revised timetable for the sale, it said in a statement today. The Washington-based firm planned to use most of the money from the IPO to buy AAA-rated residential mortgage-backed securities. The fund also targeted loans, high- yield bonds, and collateralized debt obligations.

Rising interest rates in the U.S. have fueled a surge in defaults on subprime home loans used by borrowers with poor credit histories. Investments backed by subprime mortgages are at the center of this month's losses by two hedge funds run by Bear Stearns Cos., the No. 5 U.S. securities firm. Investors are now cutting back on riskier assets.

"Carlyle's fund looked very similar to the Bear Stearns hedge fund," said Toby Nangle, who helps manage $45 billion in assets at Baring Investment Services in London. "They were unlucky with the timing."

Subprime lending: Business as usual

It would appear that subprime lenders have yet to learn from their mistakes. According to a consumer advocate group, abuses persist industry wide, despite the recent subprime mortgage meltdown.

At a Senate subcommittee hearing on ending mortgage abuse this week, the Center for Responsible Lending (CRL) presented its findings on subprime loans included in 10 recent packages of mortgage backed securities.

"A lot of the terms that make these loans so dangerous are still being used," said Keith Armstrong, CRL's senior policy counsel. "We had been told that these things are going away."

More than three quarters of the subprime loans CRL looked at turned out to be adjustable rate mortgages (ARMs). 90 percent of those were hybrid ARMs - otherwise known as "exploding" ARMs.

Hybrid ARMs have two- or three-year periods of cheap, low-interest, fixed-rate payments, or "teaser rates." But after two years, the loans reset at much steeper rates, which can prove fatal for homeowners who can't handle the higher payments.

InterOil shares' crash merits probe, RS says

A sudden crash in the share value of a Canadian oil-and-gas explorer that a year ago said it uncorked the largest natural gas discovery ever in Papua New Guinea warrants an investigation, said insider-trading watchdog Market Regulation Services Inc.

Cairns, Australia-headquartered InterOil Corp., a company registered in Canada and with offices in Toronto, Houston and in Port Moresby, Papua New Guinea, released no new material information before a major sell-off late Tuesday saw shares on the Toronto Stock Exchange quickly tumble $12.57, or 26%, to $34.49. Shares had struck a record high of $47.06 as markets closed on Monday.

Quebec's environment minister warns oil companies to expect one-cent tax

Quebec will forge ahead with its plan to tax oil companies to fund environmental programs, the province's environment minister warned on Tuesday.

Line Beauchamp says Quebec will not back down from imposing a tax of nearly one cent per litre on refiners and distributors of petroleum products come Oct. 1.

Canadians scale back spending as energy costs rise: survey

Nearly half of all Canadians were cutting back on using cars, and more than two-thirds were shivering more in the winter and sweating it out this summer due to rising energy costs, a survey suggests.

In fact, only eight per cent of Canadians said they hadn't made any changes in their daily lives as a result of higher energy costs, according to Decima research commissioned by the Investors Group financial services company.

EIA Country Analysis Briefs: Canada

According to Oil and Gas Journal (OGJ), Canada had a reported 179.2 billion barrels of proven oil reserves as of January 2007, second only to Saudi Arabia. The bulk of these reserves (over 95%) are oil sands deposits in Alberta, which are much more difficult to extract and process than conventional crude oil.

Canadas total oil production (including all liquids) was 3.3 million bbl/d in 2006. The country's oil production has steadily increased as new oil sands and offshore projects have come on-stream to replace aging fields in the western provinces: from 1996-2006, Canadas oil sands production has increased from 445,000 bbl/d to 1.2 million bbl/d. Overall, EIA predicts that oil sands production will increase even further in coming years and more than offset the decline in Canadas conventional crude oil production. Canada consumed an estimated 2.2 million bbl/d of oil in 2006. The country sends over 99 percent of its oil exports to the U.S., and it is consistently one of the top three sources of U.S. oil imports.

Farewell, Venezuela hello, oilsands

Less than five years ago, like many of the country's oil and gas companies, Petro-Canada was so outraged by Ottawa's decision to sign the Kyoto Protocol that it announced minutes after it was signed, on Dec. 10, 2002, that it had purchased a 50% interest in the La Ceiba block in Western Venezuela.

The purchase was played up as a hedge against Canada's self-defeating move and a platform from which to grow a much larger presence in the country, just in case the oilsands went offside.

To be sure, the move also reflected CEO Ron Brenneman's own preferences: he was keen to expand internationally, while he wasn't sold on the oilsands. A few months later, the company pulled the plug on its first oilsands strategy due to worries about escalating costs.

This week, the oilsands and Venezuela crossed paths again at Petro-Canada, but reality couldn't be farther from what was envisioned.

Petro-Canada was forced out of Venezuela by the government of Hugo Chavez and, with the Kyoto Protocol a distant memory thanks in large part to opposition from Canada's oil sector, is putting the finishing touches on its plans for the Fort Hills oilsands project, its second major oilsands strategy.

The State of Rhode Island and Newfoundland and Labrador Hydro will conduct an "analysis and assessment of a potential power purchase of up to 200 megawatts of electricity [by Rhode Island] by the year 2015".

The MOU institutes a two-phase process to explore a possible arrangement for the sale and purchase of power. The first part of the process is a six-month mutual assessment of the merits of long-term sale and purchase agreement, as well as the development of an action plan to address any technical, regulatory and statutory requirements of the transaction. Upon completion of Phase I, the parties may enter Phase 2 negotiations for a binding agreement on the sale and purchase of power.

Key to developing the Lower Churchill successfully would be long-term power purchase agreements that would insure creditors can recover investments in the project, which has been estimated to cost upwards of CDN $9.0 billion to complete.

Atlantic leaders look to share electricity

The annual meeting, which wrapped up Tuesday in eastern Prince Edward Island, did not reach any specific agreements, but set New Brunswick Premier Shawn Graham the task of preparing a report for presentation to next year's meeting.

The more populous New England states are hungry for power generated in eastern Canada, but P.E.I. Premier Robert Ghiz, co-chair of the conference, noted this power sharing is also important for his province, which is hoping to export wind power and import power when the wind isn't blowing.

"We don't have the opportunity on P.E.I. to back up our wind power," said Ghiz.

"It's very important to us to have access to energy to back up our wind generation on Prince Edward Island.. What happened today is we saw more regional co-operation when it comes to energy, and that can only benefit Prince Edward Island."

B.C. cities balk at touted trade deal

An interprovincial free-trade agreement that has been lauded by national and international leaders is the subject of a deepening revolt in British Columbia, where the city of Vancouver this week joined a growing list of municipalities who want out.

In a motion passed Tuesday night, Vancouver city council voted to "call on the Province of British Columbia to exempt municipalities" until it and other B.C. towns and cities have been fully consulted by the provincial government.

That vote placed Vancouver, the largest jurisdiction inside the B.C.-Alberta trade, investment and labour mobility agreement (TILMA), on a list of 20 other B.C. governments that have passed similar motions after being pushed by anti-free-trade activists. Several municipalities and the B.C. School Trustees Association have demanded complete exemptions -- regardless of consultations --and even the B.C. Library Association has passed a motion opposing the agreement.

Concerned that the agreement dumps local decision-making power into the hands of private industry and could cost them added legal fees and non-compliance penalties, they are threatening a political scrap that could ultimately result in a reshaping -- and perhaps weakening -- of some of the terms of the agreement.

The groups contend that developing oil shale on Colorado's West Slope will require 12,000 megawatts of electricity, probably from coal-fired power plants.

In a press release, they quoted Dr. Brian Moench, president of Utah Physicians for a Healthy Environment, about oil shale development concerns.

Contacted by the Deseret Morning News, Moench said he believes large-scale development would cause dangerous air pollution.

"The amount of electricity required for that (oil shale) process is just enormous," he said. It would make it "staggeringly unfeasible" to produce the oil.

Oil shale production technology is so speculative that it seems almost like science fiction, Moench added.

"The electricity demands are incredible; the water consumption is also incredible."

It's not as if oil shale is energy-intense, he said. Oil shale is rock with hydrocarbons in it. The hydrocarbons must be released from the rock, which is not like pumping oil from the ground.

"The energy density of oil shale is comparable to a potato. Manure has four times as much energy density as oil shale does," Moench said.

He added that coal produces something like 10 times as much energy per mass as oil shale. Oil shale is "just not a decent energy source," he added.

"Most likely the only way you're going to generate that much electricity (to run oil shale projects) is from coal," he added. To add enough capacity, coal-fired plants would put a great deal of pollution into the air. "You're going to considerably diminish the air quality of the entire western United States."

Britain's Year 2000 Fuel Protests Offer Chilling Look Into Our Future

It was a fuel protest that caused fuel shortages affecting millions of Europeans, yet, if you lived in the USA, you probably never heard about or knew the extent of those two weeks. There were no flashy newspaper headlines. No 'breaking stories' in T.V. news. Nevertheless, we should remember the 5th of September, and if you agree after reading this article, send in your suggestions. What might be the most appropriate name to commemorate the events of those ten days. The 'Petrol Tea Party," "Petrol 9/11" or maybe "Petrol Days of Peril." I'll refer to it hear as the Petrol Sedition.

Environment and US policy top global fears

The US comes in for sharp criticism. "Global distrust of American leadership is reflected in increasing disapproval of the cornerstones of US foreign policy," the survey says. "Not only is there worldwide support for a withdrawal of US troops from Iraq but there is also considerable opposition to US and Nato operations in Afghanistan ... The US image remains abysmal in most Muslim countries in the Middle East and Asia and continues to decline among the publics of America's oldest allies."

Nine per cent of Turks, 13% of Palestinians and 15% of Pakistanis take a favourable view of the US. In Germany, the figure is 30%, in France 39% and in Britain 51% - all down on previous surveys. Only in Israel, Ghana, Nigeria and Kenya do majorities believe US forces should stay in Iraq.In an implicit rejection of the Bush administration's "freedom agenda", the survey also finds "a broad and deepening dislike of American values and a global backlash against the spread of American ideas and customs. Majorities or pluralities in most countries surveyed say they dislike American ideas about democracy."

And among key allies in western Europe, the view that the US unilaterally ignores the interests of other countries is deep-rooted.

Putin's Arctic invasion: Russia lays claim to the North Pole - and all its gas, oil, and diamonds

Russian leader Vladimir Putin has made an astonishing bid to grab a vast chunk of the Arctic, giving himself claim to its vast potential oil, gas and mineral wealth.

His audacious argument that an underwater Russian ridge is linked to the North Pole is likely to lead to an international outcry.

Some commentators have already observed it is further evidence of growing Russian assertiveness under its authoritarian president.

The Russian media trumpeted the findings of a Moscow scientific mission to the region which boasts "sensational" geological discoveries enabling the Kremlin to make the territorial claim.

Populist newspaper Komsomolskaya Pravda - a cheerleader for Putin - printed a map of the North Pole showing a "new addition" to Russia, a triangle five times the size of Britain with twice as much oil as Saudi Arabia.

Enterprise Joins Fleet Near Iran

The USS Enterprise CVN 65-Big E Strike Group, the US Navy’s largest air carrier, will join the USS Stennis and the USS Nimitz carriers, building up the largest sea, air, marine concentration the United States has ever deployed opposite Iran.

The drumbeat of disaster that heralds global warming quickened its tempo this week; some parts of Britain had a sixth of their annual rainfall in 12 hours - some statistic. It has all been foreseen, and for far too long. After the Met Office first briefed Mrs Thatcher on climate change 17 years ago, she predicted: "There would surely be a great migration of population away from areas of the world liable to flooding."

Just over a year later, the Yangtze threw 10 million Chinese from their homes. In 1993, after the worst American floods in memory, cornfields across nine states were under water that covered farm buildings. In 1995 the Rhine rose 55ft above sea level, forcing a quarter of a million people in the Netherlands to evacuate, and the Oder spread a "once in a thousand years" flood across tracts of Poland, the Czech Republic and eastern Germany. Let me pause the historical playback at this point, more than a decade ago, to emphasise how long that drumbeat has been rolling.

Climate change is all about extremes. The American cornfields of 1993 had a few years earlier been shrivelling in the worst drought in living memory. The flood-prone Rhine nearly dried up in October 2003. You could wade across it in some places.

Consider what such escalating extremes of climate can do to national economies. The 1991 Yangtze floods submerged 20% of China's croplands. The European drought of 2003 cut plant growth by 30%. Monday saw a state of emergency in Hull, but in March 2000, floods turned the whole of Mozambique into a state of emergency, setting the national economy back by years.

Desertification threat to global stability-UN study

Desertification could drive tens of millions of people from their homes, mainly in sub-Saharan Africa and central Asia, a U.N. study warned on Thursday.

People displaced by desertification put new strains on natural resources and on other societies nearby and threaten international instability, the 46-page study by the U.N. University showed.

"There is a chain reaction. It leads to social turmoil," Zafaar Adeel, the study's lead author and head of the U.N. University's International Network on Water, Environment and Health, said.

Climate Change Threatens North Africa Food Supply

Increasingly frequent droughts in North Africa will force governments to import more food, placing their economies under severe strain unless global warming is checked, a senior UN climate expert said.

It is stunning to think that the Amazon – a humid land of frogs, anacondas and parasitic strangler figs – could disappear in this century. Environmentalists have been predicting dire consequences for the rain forest for years, but a new report from the United Nation’s Intergovernmental Panel on Climate Change finds that the Amazon could be on an irreversible course to extinction. Some researchers add to the report’s predictions saying the conservative climate models used in the IPCC’s projections underestimate regional drying.

Armies must prepare for global warming role, says British defense chief

Jock Stirrup, chief of the defense staff, said risks that climate change could cause weakened states to

disintegrate and produce major humanitarian disasters or exploitation by armed groups had to become a feature of military planning.But he said first analyses showed planners would not have to switch their geographical focus, because the areas most vulnerable to climate change are those where security risks are already high. "Just glance at a map of the areas most likely to be affected and you are struck at once by the fact

that they are exactly those parts of the world where we see fragility, instability and weak governance

today.

Death toll rises from heatwave in Europe

A heatwave has killed at least 35 people in parts of southeast Europe and hit wildlife and crops, from the humble toad in Greek lagoons to grain across the region, while fruit is ripening weeks early in Italy.

West Virginia Declares Drought Emergency

Agriculture producers of all types in the state have been adversely affected by the dry weather, Douglass said. “We have to go back to 1939 to find a drier May than what we had this year,” he said. “My farm in Mason County is in the thick of all of this. June brought us no relief. Livestock is one of the hardest hit. Cattle are drinking water like it’s going out of style — and it is.”

Western counties appear to be hit the hardest, with most receiving less than an inch of rain in May, according to information from Douglass’ office. The average normally is 4 to 5 inches.

Because of the shortfall, farmers are being forced to haul water to their herds, Douglass said. That significantly increases costs because of fuel prices. And the problems don’t end there. The first crop of hay this year was 20 to 50 percent short of the norm, Douglass said. “Hay is in jeopardy,” Douglass said. “All indications are that there will be no second crop.”

Farmers already have started feeding their cattle winter hay, he said. With a second crop unlikely, they might be forced to sell early, which likely means farmers will receive lower prices for their cattle, he said. As for consumers, they might see a short-term benefit with cheaper beef on the market this fall, Douglass said. But once that is gone, prices could skyrocket because of shortages.

When Conflicts of Interest Threaten Scientific Integrity

The growing commercialization of scientific research has increasingly forced biomedical publishers to grapple with real and perceived conflicts of interest. Every scientist has a competing interest when it comes to getting published in a high-profile journal—a prestigious publication record brings status, research funds, job security, and other personal benefits—but more and more scientific research is funded by companies with a vested interest in the outcome of that research.

It's the Broken Society, stupid

Many social trends, under governments of the Left and Right, have encouraged the fracturing of families and the undermining of values which have created the underclass. The Broken Society has many fathers. However the welfare system, which Mr Blair promised to reform by 'thinking the unthinkable' but which remains largely untouched a decade later, has been its fertiliser. It traps millions into welfare dependency and penalises anybody foolish enough to try and get a legitimate job.

Labour ministers still like to remind us of Mrs Thatcher's three million unemployed. They do not mention that, under their care and despite a growing economy, almost 5.3 million people of working age do not work but live on various benefits. Many are behaving entirely logically: they are better off doing nothing. The marginal tax rate for those who try to better themselves through work can be as high as 90 per cent for the poorest - over twice the marginal rate of tax paid by the City boys on their million-pound bonuses.

Personnel

Archives

- December 2008 (1)

- October 2008 (1)

- July 2008 (2)

- June 2008 (2)

- May 2008 (6)

- January 2008 (2)

- December 2007 (8)

- November 2007 (9)

- October 2007 (11)

- September 2007 (14)

- August 2007 (14)

- July 2007 (10)

- June 2007 (9)

- May 2007 (11)

- April 2007 (9)

- March 2007 (11)

- February 2007 (11)

- January 2007 (11)

- December 2006 (12)

- November 2006 (16)

- October 2006 (13)

License

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.

Purely anecdotal but…

In ’95 my brother in-law bought a shack on a dirt road in Santa Cruz, CA. for 80k.

6 years later he sold it for 750k . He did a little fixing up but it is still a shack on a dirt road.

That was when I grabbed my family and got the heck out of CA.

He is in real estate and seriously believes it can only keep going up.

He has not sold a property in almost a year. Prices are going down.

IMO we were set up. That’s all I’m gonna say about that.

"A lot of pension funds are gambling, they just don't know it at this point,'' said Jarislowsky, whose firm oversees C$64 billion in pension and endowment funds. ``When the thing goes poof, then they'll ask themselves: `How could I have been so stupid?'"

Canadian Pension Funds Turn to LBOs as Yields on Bonds Diminish

Canada's three-largest pension fund managers, unable to meet the long-term needs of retirees with returns from stocks and bonds, plan to increase private-equity investments after spending about C$50 billion ($47 billion) buying companies, toll roads and gas pipelines.

Canada Pension Plan Investment Board and the Ontario Teachers' Pension Plan are leading rival groups that submitted bids this week to acquire BCE Inc., Canada's No. 1 telephone company, in what would be the country's largest takeover. Canada Pension, the country's second-biggest pension fund with C$117 billion of assets, also has offered to buy Auckland International Airport Ltd. shares, sparking a possible bidding contest for New Zealand's busiest airport.

The pension funds added C$31.7 billion to private equity holdings in their most recent fiscal year, almost double the amount of the previous 12 months. The retirement plans are buying riskier assets because they don't expect publicly traded securities to provide high enough returns to pay the more than C$1.56 trillion of benefits owed to retirees over the next 50 years, according to annual reports from the pension funds.

This will go awfully wrong. Gambling with other people's money, never a good idea. If you were born after 1960, you will never see a penny in pension money.

Thanks for posting that.

You're right that this will be a huge issue, and in the worst sort of way. So many people are relying on money that won't be there - be it pensions, savings, investments, employment income etc. IMO as unpayable debts go into default, the money supply will dry up (see the video at the top under the fold), with enormous impact on every part of the economy.

stoneleigh

I was glad I took the time to watch the "money and debt" video. Thanks for posting it.

Kudos for posting the Gross newletter. I love his writing style and he does yoga, too!

Thanks. IMO everyone should watch that video.

Which by the way is called Money AS Debt.

Which is the basic idea behind it.

No more debts, no more money, a highly counterintuitive fact.

As the movie says: every individual, every company, every government is in debt. How is that possible?

Thanks for pointing that out - I fixed it.

Another anecdote that I find very reflective of what is keeping this whole circus afloat.

I have a small biz in Oregon, with about 200 to 250 customers a day.

When we opened 2 years ago about 75%+ of the transactions were cash, 25% card.

Now it is reversed and the bulk is credit, even on $10.00 and under.

Get informed, guys, this will hurt you too. Stop focusung on the housing bubble, it's much bigger than a few buildings.

The roof is caving in, with an earthquake approaching fast. That rumble you hear is just the start.

As Bloomberg states below, Wall Street is lying and hiding all they can. The reality now is that millions of private investors and institutions (pension funds!!) hold hundreds of billions of dollars in securities and other paper, that have already lost 25% of their value. Thing is, nobody knows it yet.

Nobody? Not quite. Moody's and Fitch do. But they ain't telling, and that is a risky move. If and when news leaks out that they have been selling off their assets while lying about the ratings, there'll be lawsuits from here to kingdon come, and big names will fall. Bear Stearns is just the first.

PS I'll post this on the drumbeat as well

Thanks again HISF - we are indeed very close to the beginning of an exceptionally serious financial crisis. Rating agencies will hold off on downgrades for as long as they can in order not to lose business (note the conflict of interest), but will eventually be forced to downgrade.

As with Enron, the downgrades will be too late to be of use and will probably precipitate a rush for the exits. It will be a very dangerous time to trade as executing trades will probably be difficult to impossible during periods of rapid decline, and counterparty risk would be increasing all the time. In other words, getting out at the top will not be possible for many institutions, let alone for ordinary people.

As you noted before, pension funds are holding many of the 'assets' that won't be able to be sold at any price - the so-called 'toxic waste' CDOs among other things. In chasing yield they have taken on staggering amounts of risk they didn't understand. Ordinary people will pay the price.

Tanta covers the Bloomberg article too. It's a bit long, but I'll post the whole thing anyway. Hope that's OK. She's interesting.

Stoneleigh, Thank you again for taking the time and posting all this good stuff. I do visit and I do forward the site URL and snippets.

You're doing good work.

John